Assessing the Impact of the Affordable Care Act on Health Insurance Coverage of People with HIV

INTRODUCTION

The Affordable Care Act (ACA), signed into law in 2010, is expected to expand insurance coverage for millions of people in the United States, including people with HIV. While several provisions of the ACA have implications for people with HIV,1 two are expected the have the most far reaching effects on coverage – the expansion of Medicaid eligibility to include most Americans with incomes up to 138% of the federal poverty level (FPL) (although the Supreme Court’s 2012 ruling effectively made the Medicaid expansion optional for states) and the creation of new Health Insurance Marketplaces where individuals can purchase private coverage, including subsidized coverage for those with lower incomes.

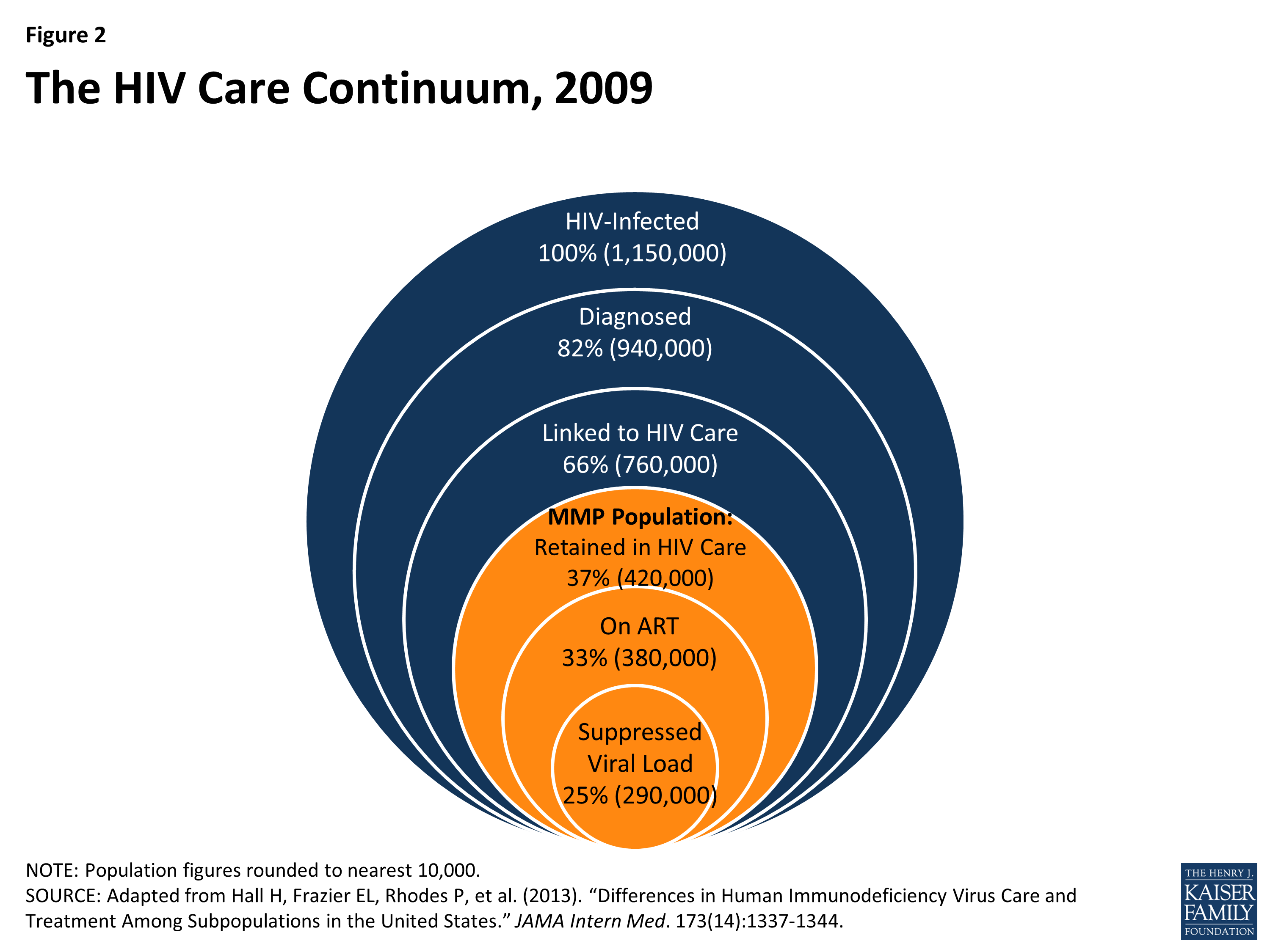

Despite the importance of these provisions for people with HIV, there are currently no national estimates of the number of people with HIV likely to gain new insurance coverage due to the ACA.2 This issue brief, based on analysis of nationally representative data from the Centers for Disease Control and Prevention’s (CDC’s) Medical Monitoring Project (MMP), provides the first such estimates, looking at how many uninsured people with HIV in care could gain new Medicaid coverage, as well as how many could be eligible for subsidized coverage in state Marketplaces. We estimate the impact of state decisions about expanding Medicaid on the reach of the ACA for people with HIV. We also discuss the current and estimated future role of the Ryan White HIV/AIDS Program, which provides care to people with HIV who are uninsured or underinsured. Finally, while our analysis focuses on those who are already in regular care (an estimated 37% of all people living with HIV in the United States, or 45% of those who have been diagnosed with HIV), we also discuss the implications of the ACA for the more than 700,000 people with HIV who remain either undiagnosed or not in regular HIV care.3 A detailed description of our methods can be found in Appendix A.

BACKGROUND ON KEY ACA INSURANCE EXPANSION PROVISIONS FOR PEOPLE WITH HIV

This issue brief analyzes the potential impact of two key ACA-related provisions for people with HIV – the expansion of Medicaid eligibility and the creation of new Health Insurance Marketplaces in each state.1

Medicaid Expansion

One of the most important components of the ACA for people with HIV is the expansion of Medicaid eligibility. Medicaid is the largest payer of HIV care in the United States and a critical source of care and services, including antiretroviral therapy (ART), for people with HIV.4 However, under current Medicaid eligibility rules, to qualify for the program, one has to meet financial eligibility criteria and belong to a group that is “categorically eligible” for Medicaid (such as children, parents with dependent children, pregnant women, and individuals with disabilities). Federal law categorically excludes non-disabled adults without dependent children, unless a state has obtained a waiver or uses state-only dollars to cover them. Medicaid eligibility rules have presented a “catch-22” for many low-income people with HIV who cannot qualify for Medicaid until they are already quite sick and disabled (usually having progressed to an AIDS diagnosis), despite the fact that early access to ART could help stave off disability and progression of HIV disease as well as prevent further HIV transmission. Because of the benefits of treatment, current national HIV treatment guidelines recommend initiation of ART as soon as one is diagnosed with HIV.5

Yet current Medicaid eligibility for low income childless adults is quite limited. Only nine states, which account for 22% of people diagnosed with HIV, provide Medicaid benefits to this population. An additional 16 states, accounting for 30% of people diagnosed with HIV, provide coverage that is more limited than Medicaid (e.g., more limited benefits). Almost half (48%) of people with HIV live in the twenty-six states that provide no coverage at all for low-income childless adults.6,7

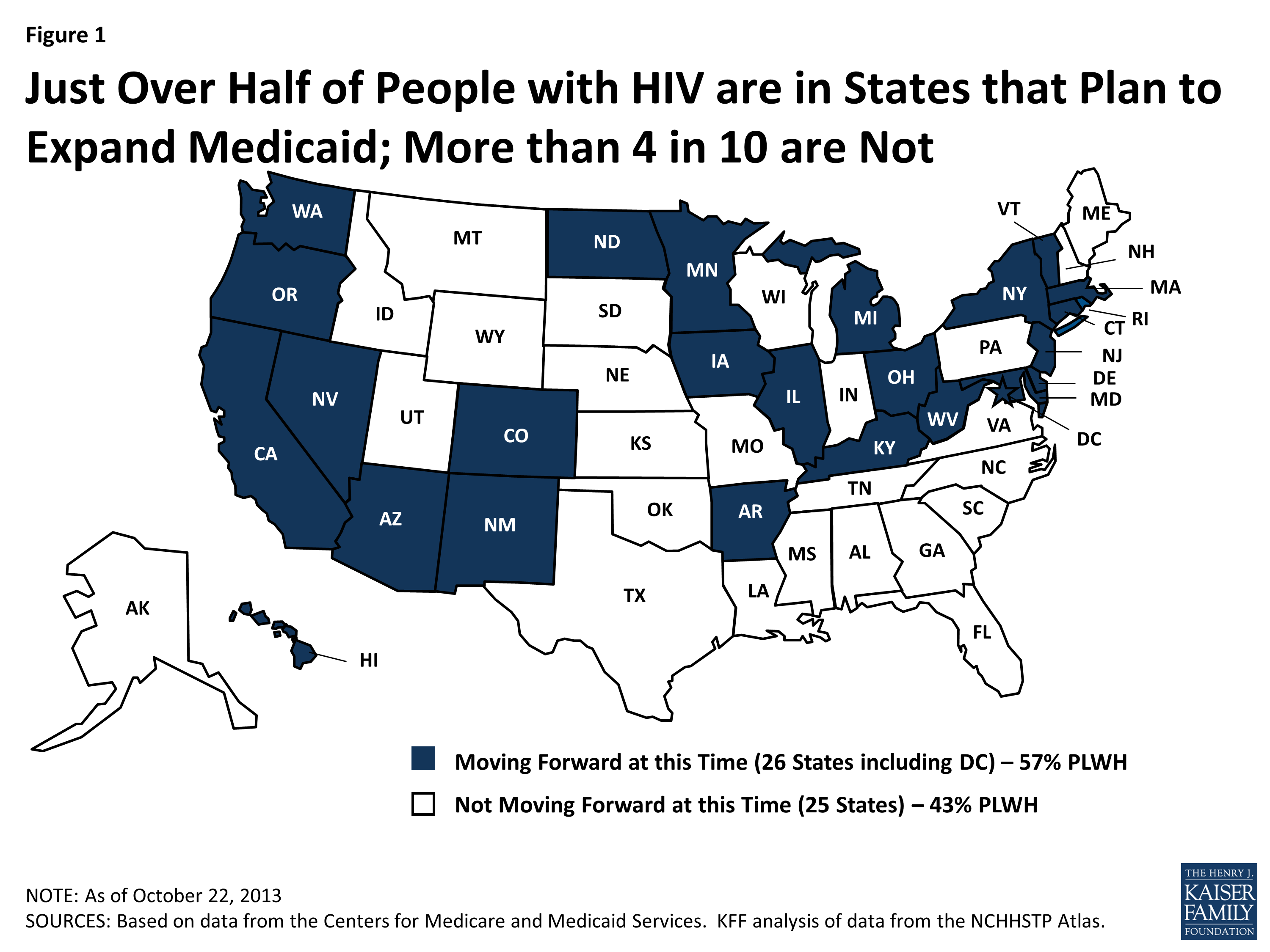

The ACA established a new minimum Medicaid income eligibility level of 138% FPL (about $16,000 for an individual in 2013) for most citizens and legal residents and removed the categorical eligibility requirement. The law requires all states to expand eligibility as of 2014. However, a Supreme Court ruling in June 2012, while upholding the ACA, effectively made Medicaid expansion a state option, and it is uncertain how many states will expand. As of October 22, 2013, 26 states have indicated they will expand Medicaid (57% of people with HIV live in these states), while 25 are not planning to expand Medicaid at this time (43% of people with HIV live in these states).8 (See Figure 1).

Figure 1 : Just Over Half of People with HIV are in States that Plan to Expand Medicaid; More than 4 in 10 are Not

Health Insurance Marketplaces (Exchanges)

The ACA requires most U.S. citizens and legal residents to have qualifying health insurance as of 2014. To help people access affordable coverage, the ACA creates new Health Insurance Marketplaces (also called “exchanges”) in every state as of 2014. Health Insurance Marketplaces are intended to create a more competitive market for individuals and small businesses buying health insurance. They offer a choice of different health plans, certifying plans that participate and providing information to help consumers better understand their options by making it easier to compare benefits across plans. Importantly, the ACA provides financial assistance for people with low incomes to purchase insurance in the Marketplace. These include tax credits to offset premium costs for those with incomes between 100% FPL and 400% FPL and subsidies to reduce cost-sharing expenses for those with incomes between 100% and 250% FPL.

Other Key Provisions for People with HIV

The ACA also includes insurance protections to help individuals obtain coverage in the Marketplace and elsewhere, including: an end to pre-existing condition exclusions (which had allowed insurers to deny coverage for those with health conditions such as HIV), a ban on premium rate setting based on health status, and an end to annual and lifetime caps on coverage. These provisions address issues that have presented particular barriers to people with HIV (and others with pre-existing health conditions and/or high care costs).

FINDINGS

The findings below are based on analysis of data from CDC’s MMP, focusing on non-elderly adults (ages 19-64) with HIV who were in regular care in 2009 (see methodology for more detail). As mentioned above, MMP collects data representative of the 37% of all people with HIV in the United States (or 45% of those who have been diagnosed) who are in care. (See Figure 2).

Figure 2: The HIV Care Continuum, 2009

Insurance Coverage and Income of Nonelderly Adults with HIV in Care

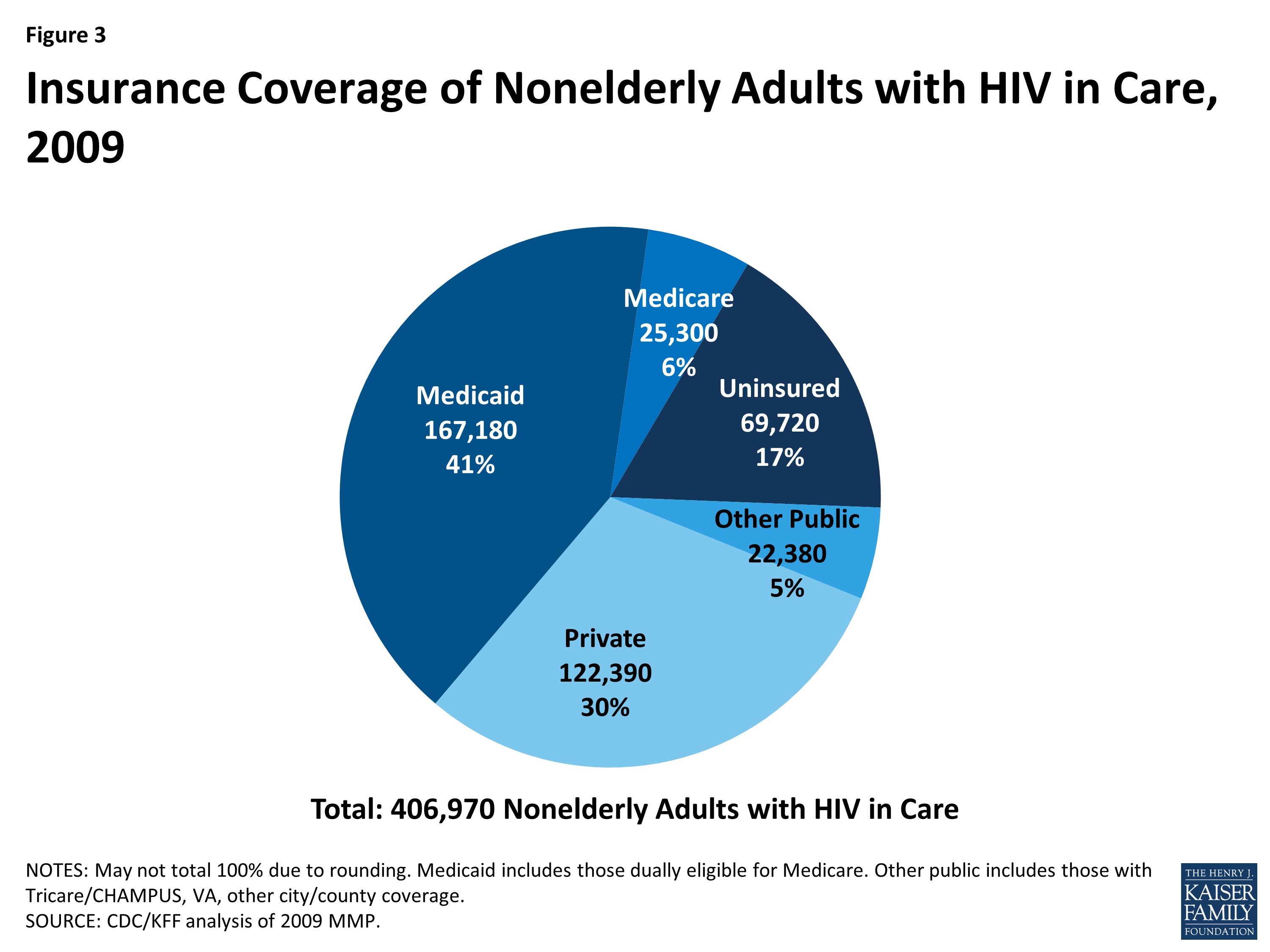

There were an estimated 406,970 non-elderly adults (ages 19-64) with HIV in care in January to April 2009. Medicaid was the largest source of insurance coverage (41%, including those dually covered by Medicare), followed by private insurance (30%). A much smaller share were covered by Medicare alone (6%), and 17% were uninsured. The remaining 5% were covered by other public sources. (See Figure 3).

Figure 3: Insurance Coverage of Nonelderly Adults with HIV in Care, 2009

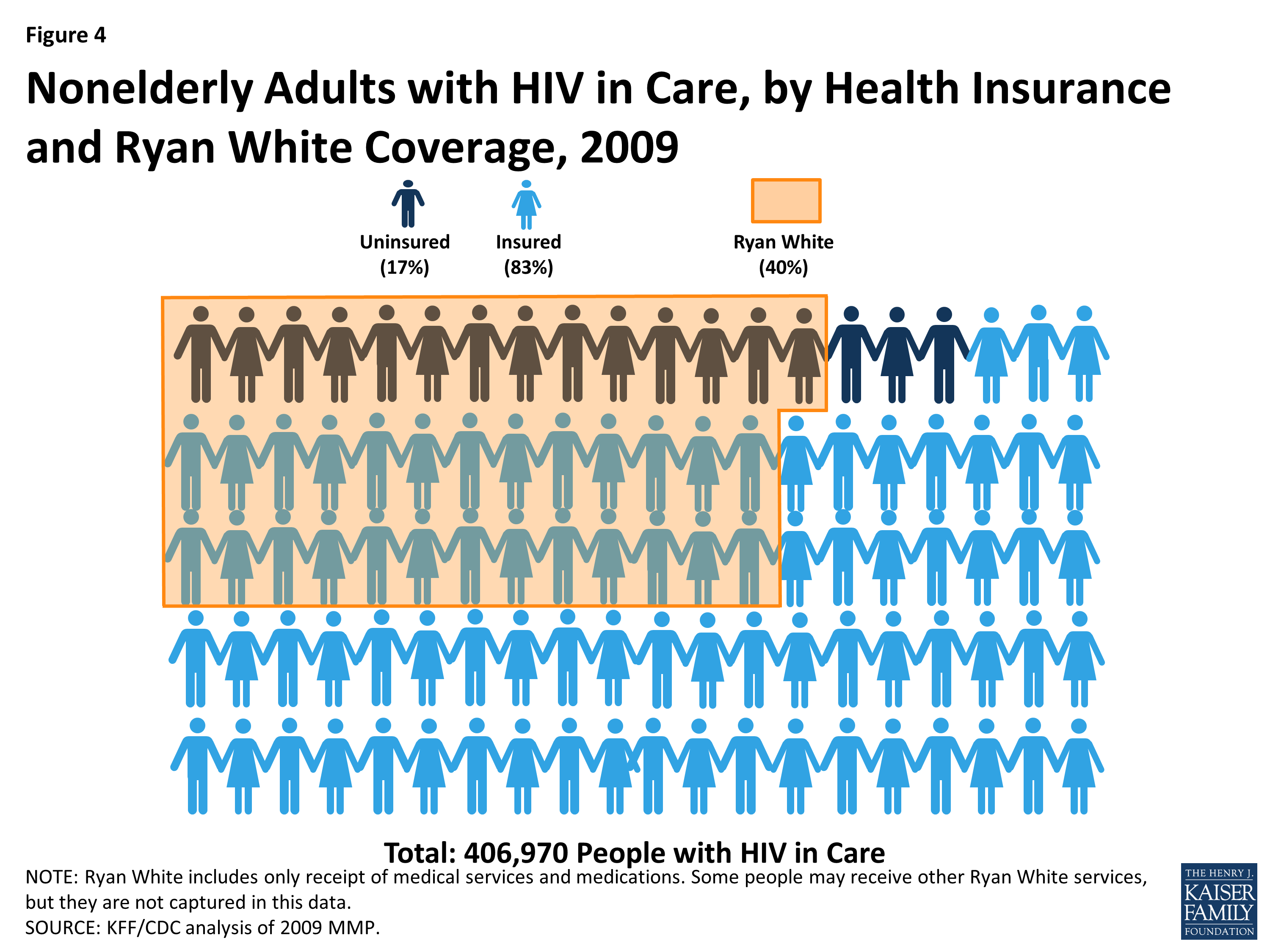

The Ryan White HIV/AIDS Program plays a significant role for people with HIV in care, including both those who have insurance and those who are uninsured. In 2009, 40% of all people with HIV in care received medical services, medications, or other services through the Ryan White HIV/AIDS Program. The program played a bigger role for those who were uninsured than those who were insured. Among the uninsured, 81% relied on the Ryan White HIV/AIDS Program. Almost a third (31%), however, of the insured also relied on the Ryan White Program, suggesting that a significant proportion of insured persons needed services that were not covered by their insurance. In fact, of those receiving services through the Ryan White HIV/AIDS Program, two thirds (65%) were insured (See Figure 4). Overall, it is likely that the Ryan White HIV/AIDS Program played an even bigger role for people with HIV than estimated here, since this analysis only included those who were aware of and self-reported receiving medical services, medications or other services through the program. As the Ryan White HIV/AIDS Program provides funds directly to service organizations, some persons might not have known that the services they received were paid for by the Ryan White HIV/AIDS Program.

Figure 4: Nonelderly Adults with HIV in Care, by Health Insurance and Ryan White Coverage, 2009

Six in 10 (61%) nonelderly adults with HIV in care were low income, with incomes at or below 138% FPL; more than four in ten (44%) had incomes below 100% FPL ($10,830 for single person in 2009 and $11,490 in 2013). About a quarter (26%) had incomes between 139% FPL and 400% FPL. (See Table 1).

|

Table 1: Income Distribution of Nonelderly Adults with HIV In Care, 2009

|

||

|

Income Range

|

Number

|

%

|

|

<100% FPL

|

179,130

|

44%

|

|

100-138% FPL

|

68,520

|

17%

|

|

139-399% FPL

|

104,510

|

26%

|

|

400%+ FPL

|

54,820

|

13%

|

|

Total

|

406,970

|

100%

|

|

Totals may not sum due to rounding.

FPL=Federal Poverty Level

The FPL in 2009 was $10,830 for an individual.

Source: CDC/KFF analysis of 2009 MMP.

|

||

Looking at the distribution of people with HIV in care by both coverage type and income, those who were uninsured or covered by Medicaid had lower incomes than those with Medicare, private or other public coverage: more than half of those who were uninsured or covered by Medicaid had incomes less than 100% FPL. A higher proportion of the privately insured had incomes at or greater than 400% FPL (See Table 2).

| Table 2: Income Distribution of Nonelderly Adults with HIV in Care by Type Insurance Coverage, 2009 | ||||||||||

| Income Range | Uninsured | Medicaid* | Medicare | Private | Other** | |||||

| Number | Percent | Number | Percent | Number | Percent | Number | Percent | Number | Percent | |

| <100% FPL | 35,630 | 51% | 109,020 | 65% | 8,030 | 32% | 17,530 | 14% | 8,920 | 40% |

| 100-138% FPL | 11,280 | 16% | 34,450 | 21% | 7,250 | 29% | 10,650 | 9% | *** | 22% |

| 139-399% FPL | 20,290 | 29% | 20,730 | 12% | 8,450 | 33% | 47,380 | 39% | 7,650 | 34% |

| 400% FPL+ | 2,520 | 4% | *** | *** | 1,570 | 6% | 46,840 | 38% | *** | *** |

| 69,720 | 100% | 167,180 | 100% | 25,300 | 100% | 122,390 | 100% | 22,380 | 100% | |

|

FPL=Federal Poverty Level

*Includes those also covered by Medicare

**Tricare/CHAMPUS, VA, other city/county

*** Estimate does not meet standard for statistical reliability. Note: Numbers may not sum to totals due to rounding. Source: CDC/KFF analysis of 2009 MMP.

|

||||||||||

Estimates of the Effects of ACA Insurance Expansions in 2014

Nearly 70,000 adults with HIV in care were uninsured. Given the income profile of the uninsured population with HIV in care, the vast majority (96%) would likely be eligible for free or subsidized coverage under the ACA’s Medicaid or Marketplace provisions if all states expanded Medicaid. If not all states expand, fewer will be eligible for Medicaid, and a small number of those who are ineligible because their state does not expand could obtain subsidized coverage in the Marketplace.

Medicaid Expansion

If all states were to expand Medicaid, almost 47,000 uninsured adults with HIV in care could gain Medicaid coverage. If this entire group enrolled, the share of people with HIV in care who are covered by Medicaid would increase from 41% to 53%. However, if only the 26 states currently planning to expand Medicaid do so, then fewer uninsured adults with HIV would be newly eligible for the program. As described above, 43% of people with HIV live in states that are currently not planning to expand Medicaid. Because data on the income and insurance distribution of people living with HIV at the state level were unavailable, we applied the national income and insurance distribution to states that are not planning to expand Medicaid. Assuming that the HIV population in states not planning to expand Medicaid has the same income and insurance distribution as people with HIV in care nationally, state decisions not to expand Medicaid could decrease the number of eligible uninsured with HIV by more than 20,000 people, to 26,560. An estimated 20,350 of those who could gain new Medicaid eligibility if their state expanded Medicaid live in states not planning to expand, with Texas and Florida alone accounting for about half. (See Table 3).

|

Table 3: Potential Impact of State Decisions to Expand Medicaid on Medicaid Coverage of Nonelderly, Uninsured Adults with HIV in Care

|

||

|

Number of Uninsured Potentially Eligible for Medicaid

|

%

|

|

|

States moving forward with expansion (26 states)

|

26,560

|

57%

|

|

States NOT moving forward with expansion (25 states)

|

20,350

|

43%

|

|

Total

|

46,910

|

100%

|

|

*State Medicaid decisions as of October 22, 2013.

Sources: CDC/KFF analysis of 2009 MMP; KFF State Health Facts, https://www.kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/; 2010 NCHHSTP Atlas data, http://www.cdc.gov/nchhstp/atlas/. |

||

Health Insurance Marketplaces

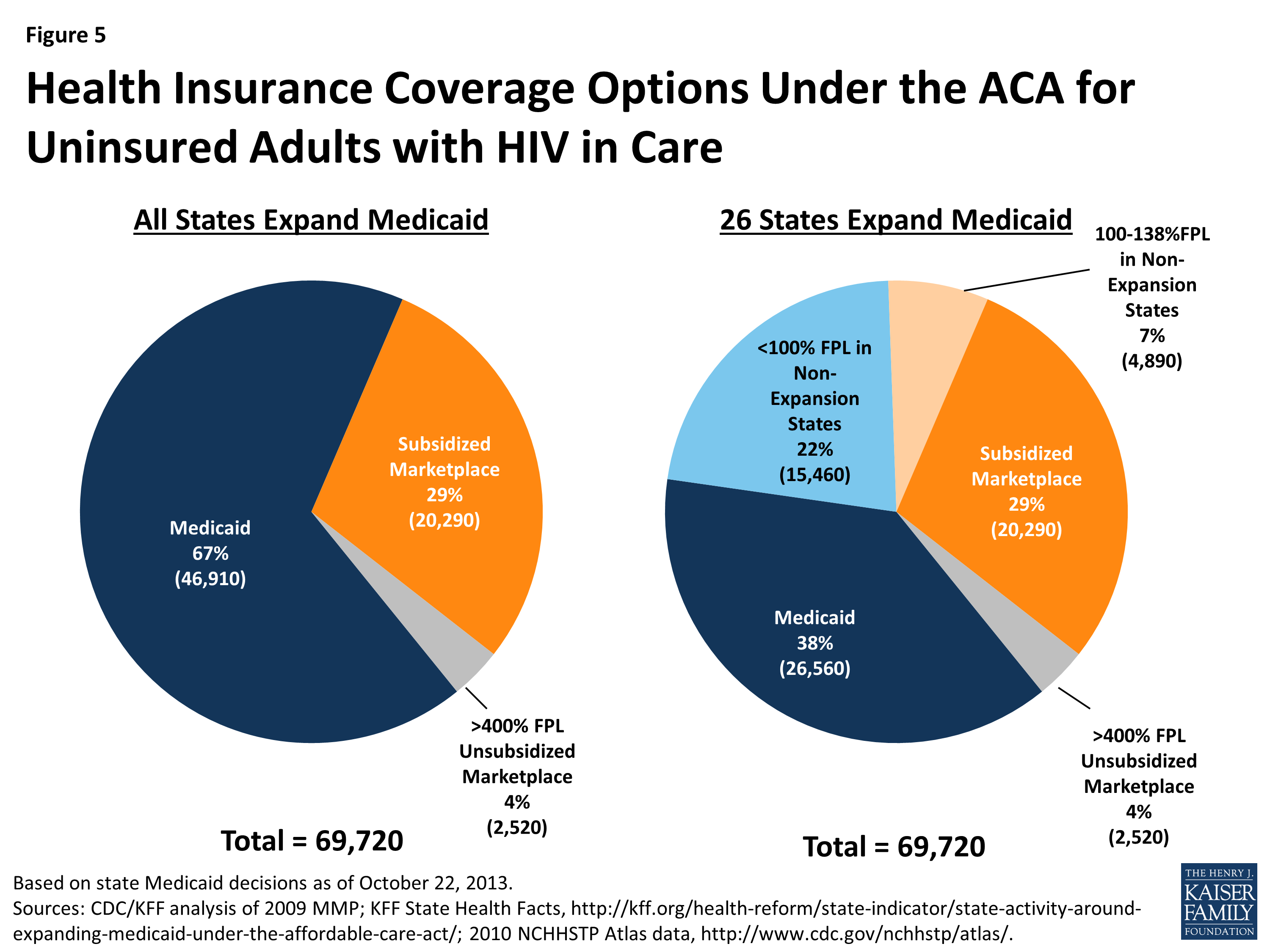

As of 2014, almost 20,300 currently uninsured people with HIV in care could be newly eligible for subsidized coverage in Health Insurance Marketplaces, meaning their incomes are between 139% FPL and 400% FPL. Just over 2,500 uninsured adults with HIV in care who have incomes above 400% may also gain coverage under the ACA through Health Insurance Marketplaces, although they would not be eligible for financial assistance. It is possible that many people in this group cannot currently afford coverage due to their illness. While subsidies are not available for people in this income range, these individuals may benefit from new rules that cap annual and lifetime dollar limits on coverage, ban premium rate setting based on health status, and end pre-existing condition exclusions.

However, the number of people who would be eligible for and seek subsidized coverage through Marketplaces is dependent on whether or not states decide to expand Medicaid. In states that do not expand Medicaid, uninsured individuals with incomes between 100% FPL and 138% FPL may be eligible for subsidized coverage in Marketplaces. Thus, a small share of low-income people with HIV who would be left out of the Medicaid expansion due to their state’s decision not to expand could gain subsidized Marketplace coverage. We estimate that approximately 4,890 people with HIV in care have incomes between 100 and 138% FPL and live in states that are not expanding Medicaid. People with incomes below 100% FPL in states that do not expand Medicaid may be left without an ACA coverage option as they are neither eligible for Medicaid nor subsidized coverage. While they could purchase coverage through the Marketplaces, they are not eligible for subsidized coverage, and coverage is likely to be unaffordable. We estimate that approximately 15,460 people with HIV in care fall into this category. (See Figure 5). For these individuals, the Ryan White HIV/AIDS Program could play a significant role in helping them to purchase private coverage in the Marketplace.

Figure 5: Health Insurance Coverage Options Under the ACA for Uninsured Adults with HIV in Care

Overall Impact

Taken together, the combination of Medicaid expansion and the ACA’s Health Insurance Marketplace could provide new coverage to the close to 70,000 people with HIV in care who are currently uninsured. If all states expanded Medicaid, 46,910 of these people would be eligible for Medicaid and 20,290 would be eligible for subsidized coverage in the Marketplace. If only the 26 states planning to expand Medicaid as of October 2013 do so, 26,560 would be eligible for Medicaid and more (25,190) would qualify for subsidized coverage in the Marketplace. However, 17,980 would remain ineligible for Medicaid and would not be eligible for financial assistance in the Marketplace. (See Table 4 and Figure 5). For these individuals, the Ryan White HIV/AIDS Program will be an important source of care and other HIV services.

|

Table 4: Estimated Number of Nonelderly, Uninsured Adults with HIV in Care

Who Could Gain New Coverage

|

||||||

|

New Coverage Source

|

If All States Expand Medicaid

|

If Only 26 States Expand Medicaid, and 25 Do Not*

|

Difference Between All States Expanding Medicaid and Only 26 Expanding

|

|||

|

Number

|

%

|

Number

|

%

|

Difference

|

Percent

Change |

|

|

Expanded Medicaid

|

46,910

|

67%

|

26,560

|

38%

|

-20,350

|

-43%

|

|

Subsidized Marketplace Coverage

|

20,290

|

29%

|

25,190

|

36%

|

4,900

|

24%

|

|

Unsubsidized Marketplace Coverage

|

2,520

|

4%

|

17,980

|

26%

|

15,460

|

613%

|

|

Total

|

69,720

|

100%

|

69,720

|

100%

|

—

|

—

|

|

*State Medicaid decisions as of October 22, 2013.

Note: Figures may not sum to total due to rounding.

Sources: CDC/KFF analysis of 2009 MMP; KFF State Health Facts, https://www.kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act/; 2010 NCHHSTP Atlas data, http://www.cdc.gov/nchhstp/atlas/.

|

||||||

In addition, while most people with HIV who already have insurance will not experience a change in their coverage after ACA implementation, it is possible that some may choose to change their coverage type. For example, some of those who currently have private coverage may purchase that coverage on their own directly from an insurer, rather than receiving it as a fringe benefit through a job. These individuals could choose to take advantage of the Marketplaces, as well as the subsidies available, where they may have lower premiums and broader benefits packages. We do not have estimates of the number or share of people with HIV in care who purchase coverage on their own (versus receive group coverage through an employer). However, the share of the general population with nongroup coverage is quite low (5%),9 and it is unlikely that a much higher share of people with HIV obtain nongroup coverage (particularly given the pre-existing condition exclusions that have been in place and did not end until January 1, 2014).

Further, some people with HIV in care who have private coverage may become newly-eligible for Medicaid (although research on the general population indicates that a very small share overall switches from private coverage to Medicaid when Medicaid is newly-available to them.)10

DISCUSSION

Key insurance expansion provisions of the Affordable Care Act will provide new health coverage for the approximately 70,000 uninsured individuals living with HIV in care today and may also provide new options to some who already have coverage. As this analysis finds, close to 47,000 people with HIV who are currently uninsured could be eligible for Medicaid if all states choose to expand Medicaid eligibility to 138% FPL; an additional 20,290 could be eligible for subsidized coverage in the new Health Insurance Marketplaces, and about 2,500 have incomes too high to be eligible for financial assistance but could purchase coverage in the Marketplace. However, if not all states expand Medicaid – and only 26 have indicated that they will as of October 2013– many fewer will be eligible for Medicaid. While some of these individuals will be able to obtain subsidized coverage in the Marketplace, the majority of uninsured people with HIV have incomes below 100% FPL, making them ineligible for subsidized coverage. For this subset, the Ryan White HIV/AIDS Program would remain a critical source of support. The Ryan White HIV/AIDS Program will also likely continue to be important for many who gain new coverage, given that two-thirds of current Ryan White HIV/AIDS Program clients already have insurance.

While this analysis focuses on people with HIV who are already in the care system, there are more than 700,000 who currently are not in care, either because they remain undiagnosed or are not receiving regular medical care. (See Figure 1). Many of these individuals are also likely to be eligible for new coverage. While little is known about their current health insurance and income status, to the extent that it matches that of people with HIV in care, an additional 124,000 people with HIV not receiving regular medical care could be newly eligible for coverage either through Medicaid or in the Marketplace. This would bring the total estimated number of people with HIV who could gain new coverage to close to 200,000.

It is important to note that although the ACA will significantly expand coverage for people with HIV, this newly insured population represents only a fraction (<1%) of the 25 million people expected to gain coverage overall and is therefore unlikely to substantially affect the risk pool of people gaining new coverage;11 currently, people with HIV on Medicaid represent less than 2% of total Medicaid costs and less than 1% of enrollees.12 The ACA represents an important opportunity to draw this high-need population into broader coverage and to address ongoing unmet needs for coverage and care. At the same time, the Ryan White HIV/AIDS Program will continue to be an important source of care and other HIV-related services for those who do not gain new coverage or need additional financial assistance to pay for their HIV care going forward.

Jennifer Kates, Rachel Garfield, and Katherine Young are with the Kaiser Family Foundation. Kelly Quinn, Emma Frazier, and Jacek Skarbinski are with the Centers for Disease Control and Prevention.