Assessing ACA Marketplace Enrollment

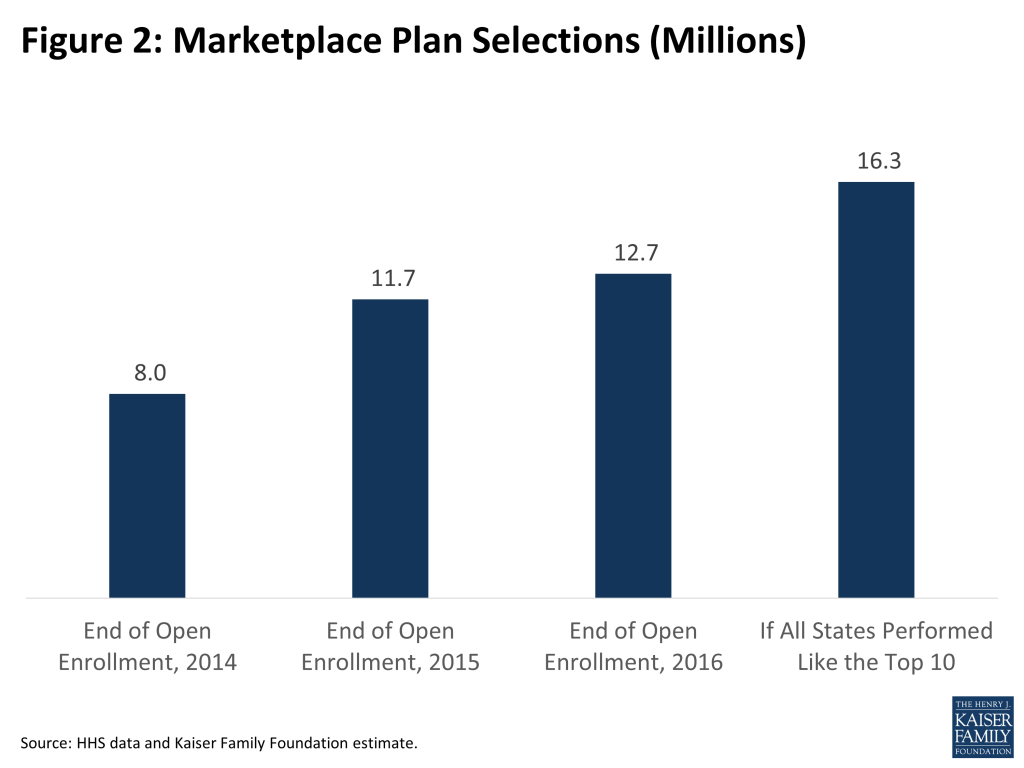

As of the end of the third open enrollment under the Affordable Care Act (ACA), 12.7 million people had signed up for coverage in the health insurance marketplaces, up from 11.7 million last year and 8.0 million in 2014.

Actual enrollment will end up somewhat lower than this because some people will not pay their premiums or will have their coverage terminated due to inconsistencies on their applications, and there is typically additional attrition as the year progresses (e.g., as some enrollees get jobs with health benefits). For example, in 2015 paid enrollees totaled 10.2 million as of end of March and 9.3 million as of the end of September. If a similar pattern holds, actual enrollment should end 2016 over 10 million, which was the target established by the Department of Health and Human Services (HHS). (There are reasons to believe that attrition may be lower this year, including the fact that terminations occurring during open enrollment have already been subtracted from official signup figures, which was not the case previously.)

While enrollment is in line with the HHS target announced in advance of this year’s open enrollment, it is short of earlier projections by the Congressional Budget Office (CBO), which became an implicit yardstick for judging the law. In March 2015, CBO projected average monthly marketplace enrollment of 21 million in calendar year 2016, though recently lowered that forecast to 13 million.

In this analysis, we look at why enrollment may be lower than projected by CBO and discuss the potential for future enrollment growth.

Why Is Enrollment Lower Than Projected?

There are several reasons why marketplace enrollment may be lower than what CBO projected:

The availability of employer coverage has not declined. People with access to affordable employer coverage are not eligible for marketplace premium subsidies, so there was an expectation that some employers might drop coverage to allow their employees to take advantage of those subsidies.

CBO projected a decline in employer coverage relative to what would have happened in the absence of the ACA of 1 million people in 2015 and 6 million in 2016. So far, there are no signs of such a decline due to the ACA. A federal survey of employers found that fewer private sector employees were in establishments that offered health insurance coverage in 2014 as the ACA took effect, but that was consistent with a longer term trend that predated the ACA. The Kaiser-HRET Employer Health Benefits Survey showed 57% of firms offering health benefits in 2015, statistically unchanged from 55% in 2014.

It may be that the incentives for employers to maintain health benefits are more powerful than expected, at least so far. Employers with 50 or more full-time employees face penalties under the ACA if they do not offer affordable coverage to their full-time workers, and employer-based insurance benefits are provided tax-free to employees.

Many people are still buying their own insurance outside of the marketplaces. There are three types of individual coverage outside of the marketplaces:

- ACA-compliant plans. Anyone buying individual coverage effective starting January 1, 2014 had to purchase an ACA-compliant plan, whether it was offered inside a marketplace or on the outside market. These plans must follow virtually all of the same rules as marketplace plans – including no discrimination against people with pre-existing conditions and inclusion of essential health benefits – and their premiums are set as part of one insurance risk pool. The main distinguishing feature is that premium subsidies for low and middle-income enrollees are only available inside a marketplace. For people not eligible for premium subsidies, there is little advantage to buying through the marketplace. Insurers and brokers may also prefer the application process outside of the marketplaces when enrolling people not eligible for premium subsidies.

- “Grandfathered” plans. These are plans that were purchased prior to the enactment of the ACA in March 2010, and can exist in perpetuity largely under pre-ACA insurance rules. Given substantial turnover in the individual insurance market, the prevalence of these plans will diminish over time.

- “Transitional” plans. These plans – also referred to as “grandmothered” coverage – include coverage that was purchased after the enactment of the ACA but before the beginning of the first open enrollment period in October 2013. Following controversy over these plans being cancelled because they did not comply with new insurance market rules taking effect in 2014 under the ACA, the Obama Administration issued guidance that permits these plans to remain in effect until December 31, 2017). The federal rules granted discretion to states and individual insurers, so transitional plans have not been allowed to continue in all cases.

Current data regarding how many people are purchasing individual coverage outside of the marketplaces is difficult to come by. As of the end of 2014, we estimated that 57% of all individual market coverage was purchased outside of the marketplaces (including ACA-compliant, grandfathered, and transitional plans). That share may have fallen since then as market churn lowers the number of grandfathered and grandmothered policies. However, it is still quite common for people not eligible for subsidies to buy in the outside market, evidenced by the fact that 82% of marketplace enrollees are receiving subsidies. There is, in some sense, an artificial distinction between ACA-compliant plans purchased on or off the marketplaces, since they offer equivalent coverage and are part of the same insurance risk pool.

Affordability remains a challenge. A recent Kaiser poll found that the overwhelming reason why people who are uninsured say they are uncovered is cost – 46% of uninsured, non-elderly adults say they tried to get coverage but found that it was too expensive. However, it is difficult to separate lack of affordability from lack of awareness of financial help that may be available, which could be addressed through more intensive outreach. For example, going into this last open enrollment period, another poll found that 82% of uninsured adults had not been contacted in the previous 6 months about the health law.

One way to gauge where affordability or outreach challenges may exists is to look at how the number of people uninsured has changed by income group. Figure 1 shows the change in the number of uninsured in the first year of the ACA among those who are potential purchasers of marketplace coverage (i.e., those who are ineligible for Medicaid or employer coverage and are not undocumented immigrants, excluding people below poverty in states that have not expanded Medicaid).

The two groups that saw the least gains in coverage were those who were very low income (below 150% of the poverty level) and those with incomes 300-400% of the poverty level.

The lowest income group qualifies for the biggest premium subsidies, but they still generally have to pay something towards the premium (up to about 4% of income for those at 150% of poverty to enroll in a benchmark Silver plan). And, while cost-sharing subsidies are available to enrollees with incomes up to 250% of the poverty level, the deductibles and copays may still feel high for a family struggling with a very low income. These low-income households – who would mostly qualify for Medicaid if their states chose to expand eligibility up to the ACA standard of 138% of the poverty level – may also be hard to reach given their often unstable financial and employment circumstances.

Those with incomes 300-400% of the poverty level had the smallest gains in coverage. Premium subsidies phase out quickly in that income range, and may provide insufficient incentive for them to purchase insurance.

Surprisingly, there was a 22% decline in the number of marketplace-eligible uninsured with incomes above 400% of the poverty level, given that they are not eligible for any premium subsidies. It may be that the so-called “individual mandate” had an effect on this group. Some people were also likely excluded from insurance previously because they had pre-existing health conditions.

What Is A Reasonable Expectation for Future Marketplace Enrollment Growth?

While marketplace enrollment has continued to grow in the third year of operation, that growth is slower than it was in year two – an increase of 1 million plan selections during 2016 open enrollment versus 3.7 million in 2015.

A key question for the future of the marketplace is whether enrollment will continue to grow and by how much. Enrollment growth is important for several reasons, including:

- Higher enrollment among those who would otherwise be uninsured would increase the number of people with insurance, which is a primary aim of the ACA.

- Since it is likely the case that many people who are sick already obtained coverage once pre-existing condition exclusions were prohibited starting in 2014, increasing enrollment would bring healthier people into the risk pool and help to stabilize premiums.

- A growing market would be more attractive to insurers, whose participation is central to the success of the marketplaces.

Any effort to forecast marketplace enrollment is subject to substantial uncertainty, as illustrated by the wide gap between what CBO has projected and actual enrollment so far. One way to estimate potential growth is to look at the experience of the top-performing states.

We estimate that the 12.7 million signups so far represent 46% of the “potential market” for the marketplaces. The potential market includes people who are uninsured or purchasing their own coverage. It excludes those who have an employer offer of insurance, are eligible for Medicaid, are undocumented immigrants, or who have incomes below the poverty level and live in states that have not expanded Medicaid (the methodology for this calculation can be found here.)

The 10 best-performing states – which include several large states such as Florida, North Carolina, and California — have collectively signed up 59% of the potential market. While that might appear to leave room for substantial further growth, there are reasons to believe that enrollment has close to plateaued in those states. The potential market includes people who are buying their own coverage outside the marketplaces, many of whom do not qualify for subsidies. The experience so far is that the vast majority (82%) of marketplaces enrollees are receiving premium subsidies, while people who are ineligible for subsidies typically buy coverage on the outside market. In fact, we estimate that in the top-performing states the number of people who have selected a plan and qualified for a subsidy represents more than 90% of subsidy-eligible people. This is a very high take-up rate for a public program, suggesting there is very little potential for growth in these states. The only way enrollment could grow substantially is to attract people not eligible for subsidies who are already buying their own coverage directly.

However, there is still considerable room for enrollment growth among states that have enrolled a lower share of the potential market. If all states improved to at least the average of the 10 best-performing states, we estimate that total marketplace signups would reach 16.3 million. Assuming that around 10% of these people would not pay their first month’s premium, this would translate into an “effectuated” enrollment total of 14.7 million. This may provide a reasonable estimate of a ceiling on what marketplace enrollment could grow to over the next several years, assuming current levels of premium subsidies and outreach.

Discussion

Marketplace enrollment under the ACA is lower than projected, though signups continue to grow and the program appears sustainable overall. It is important that enrollment continue to grow to fulfill expectations for reducing the number of people uninsured, to keep premiums stable, and to remain attractive to insurers. Since insurance risk is pooled at the state level, problems in certain states could develop if enrollment stagnates and skews towards sicker-than-average individuals.

Judging by the experience of the top performing states, there is considerable room for enrollment growth over the next several years. However, even if all states signed people up at the rate of the top 10 states, enrollment would still fall well short of projections by CBO, suggesting that those forecasts may have been unrealistic.

There are a number of areas of uncertainty that will affect marketplace enrollment. Enrollment could grow if larger numbers of employers drop health benefits for their workers, or if the buying experience in the marketplaces continues to improve and attracts people now buying their own insurance in the outside market. The pool of purchasers could also grow as transitional policies get terminated over the next year and a half. On the other hand, enrollment could shrink if more states expand Medicaid, pulling people with incomes between 100% and 138% of the poverty level out of the marketplace. There are also concerns that some existing enrollees may drop coverage if premiums become unaffordable or the cost-sharing is too high to offer sufficient value.

There are signs that marketplace coverage could continue to grow modestly in the years ahead. But, absent a substantial boost in outreach or changes to the subsidies to make insurance more affordable, substantial increases in marketplace enrollment are unlikely.