Survey of Health Insurance Marketplace Assister Programs

Executive Summary

The Affordable Care Act (ACA) provides for a substantial new infrastructure of consumer assistance in health insurance. All state Marketplaces are required to have Navigators and other similar Assister Programs to help consumers understand their coverage options, apply for assistance, and enroll. In addition, comprehensive State Ombudsman or Consumer Assistance Programs (CAPs) are established under the ACA to provide a full range of help – outreach and enrollment assistance as well as help with post-enrollment problems such as appealing denied claims – to all state residents in all types of group and non-group health plan coverage. Throughout the first Open Enrollment period, public attention focused on the number of people who would enroll in qualified health plans (QHPs) offered through the Marketplace and in Medicaid. People will continue to enroll in coverage throughout the year, and even more people are projected to enroll next year, but the close of Open Enrollment affords an opportunity to examine the role of Assister Programs in helping people to enroll and remain enrolled in coverage.

This report is based on findings from the 2014 Kaiser Family Foundation survey of Health Insurance Marketplace Assister Programs. This internet survey was conducted from April 24 to May 12, 2014, shortly after the first Open Enrollment period concluded. Federal and state-operated Marketplaces provided email contact information for directors of their Assister Programs, all of whom were invited to participate. This report examines the experience of Assister Programs across the states in conducting outreach and enrollment assistance during the first Open Enrollment period for health insurance Marketplaces established by the ACA. Based on responses to this survey extrapolated to the total number of Assister Programs, this report offers the first nationwide assessment of the number and type of Assister Programs and the number of people they helped. This report also examines the nature of help consumers needed, both pre- and post-enrollment, and the extent to which Assister Programs could meet consumer needs. In addition, it discusses key factors that impacted the effectiveness of Assister Programs at the outset and the outlook for consumer assistance in the future.

More than 4,400 Assister Programs, employing more than 28,000 full-time-equivalent staff and volunteers, helped an estimated 10.6 million people during the first Open Enrollment period.

Assistance resources were not evenly distributed across states. In states with State-based Marketplaces (SBM) and Consumer Assistance Partnership Marketplaces (FPM), there were about twice as many Assisters available per 10,000 uninsured, compared to states with a Federally-facilitated Marketplace (FFM). The number of people helped per 1,000 uninsured was also greater in State and Partnership Marketplaces; SBMs helped about twice as many people relative to the uninsured population compared to FFMs, while FPMs helped about 1.5 times as many relative to the uninsured population. Some people who were helped enrolled in new QHPs, and some in Medicaid and CHIP. Others who sought help didn’t enroll in coverage, for example, if they were ineligible for both Medicaid and premium tax credits.

During the first year more than 70% of Assister Programs were supported privately or by a federal safety net clinic program.

Under the ACA, Marketplaces are required to support consumer assistance through operating revenue. All Marketplaces did directly support Assister Programs in 2013-2014, but of all Assister Programs established in the first year, most were funded by sources other than Marketplaces. Certified Application Counselors (CAC) Programs, which generally receive no Marketplace funding, and Programs sponsored by federal health centers funded by grants from the Health Resources and Services Administration (HRSA) together account for 71% of all Assister Programs and account for more than 60% of people who received help.

Overwhelmingly, Assister Programs report people sought help because they simply do not understand the ACA or health insurance and lacked confidence to apply on their own.

Many consumers in search of health insurance sought a more human touch to find their way through the enrollment process. Over 80% of Assister Programs report most or nearly all consumers who sought help didn’t understand the ACA or the coverage choices offered them or simply lacked confidence to apply on their own. Almost 90% of Programs report the majority of consumers they helped were uninsured. Almost three-quarters of Programs say most consumers who sought help struggled to understand even basic health insurance terms such as “deductible” or “network service.” Balky web sites also drove consumers to Assister Programs, as did the application process itself, which can require understanding of the tax code, immigration rules, or family law, depending on a person’s circumstances. Also, because most Marketplaces have not yet completed the single streamlined application that determines eligibility for all forms of subsidized coverage, many consumers sought help obtaining Medicaid eligibility determinations.

Helping consumers was not always an efficient process and took a significant amount of time per case.

Sixty-four percent of Assister Programs reported spending between one and two hours helping each consumer, on average. Explaining rules and options to people with limited understanding of the ACA and health insurance took time. So did waits on hold with Marketplace call centers and frozen computer screens. Programs also report that often consumer questions about health plans couldn’t be easily answered by information posted on Marketplace web sites.

Ninety percent of Assister Programs have already been re-contacted by consumers with post-enrollment questions and problems.

Post-enrollment problems range from consumers not having received their insurance card, to not understanding how to use new health insurance or how to appeal a denied claim. Most Marketplace Assisters are not trained to help consumers appeal denied claims or resolve problems with insurers. Instead, they are supposed to refer consumers to state ombudsman or CAPs, also established by the ACA. CAPs are funded by federal grants, though the last grants were awarded in 2012 and, as a result, some CAPs have stopped providing services and some others are operating at reduced levels. Many Marketplace Assister Programs appear to be unfamiliar with CAPs, even where they are still operating. When Assister Programs encounter post-enrollment problems they can’t help with, they mostly refer consumers to the Marketplace call center or back to their health plan.

Assister Programs believe some key changes could help them work more effectively.

Assister Programs that collaborated with others reported this coordination to be very helpful, though more than half of Assister Programs seldom or never coordinated with other Programs. When coordination did take place, it was most often initiated by Assister Programs themselves or facilitated by outside groups, less often by the Marketplaces. Programs report coordination was useful for directing consumers to the nearest Program with available appointments, in strategic planning of enrollment and outreach events, in sharing specialized staff (such as those who could provide interpreter services), and in troubleshooting and problem solving on complex cases. Some State-based Marketplaces also made dedicated call centers for Assisters, and built Assister portals into their online application system so that Programs could track clients’ status. Programs reported that these features also helped them to work more efficiently.

Three-quarters of Assister Programs say it is very likely they will continue to provide Marketplace assistance next year.

Prior to the first Open Enrollment, 30% of Assister Programs had no prior experience helping consumers and just 16% had experience helping consumers enroll in private health plans. Because so many Assister Programs expect to continue operating next year, the level of experience will likely increase going forward. If Marketplaces continue to invest in resources to support Assister Programs, there could develop a profession of expert Assisters who understand consumer needs and how ACA rules and coverage options apply to them.

Assister Programs will likely play a key role in determining how much enrollment grows in 2015.

The Congressional Budget Office has projected that 13 million people could enroll in Marketplace health plans in 2015, 5 million more than signed up during the first Open Enrollment period. Increasing enrollment will first require maintaining coverage for current enrollees. Many people may need help re-applying for coverage or subsidies. Others with post-enrollment problems may need help resolving them in order to decide if coverage is worth maintaining. Some Assister Programs were already stretched to capacity in 2014. For the first Open Enrollment period overall, most Programs could help most of the people who sought help most of the time. Close to 40% of Programs, though, said they could not help all who sought assistance, with 12% saying demand far outpaced capacity. During the final weeks of Open Enrollment almost half of Assister Programs had to turn away at least some consumers.

Enrolling millions of new consumers also presents challenges. Public understanding of the ACA remains limited. If the first wave of enrollment in 2014 was comprised of those consumers who were the most resourceful and motivated to seek coverage, then investment in consumer assistance will be all the more key in the year to come.

About the Assister Programs Described in this Report

Several types of Assister Programs provide outreach and enrollment assistance to individuals, families, and small businesses seeking to obtain health insurance coverage through new Health Insurance Marketplaces and through the Medicaid expansion available in some states. In this report, we use the following terms to describe different types of Assister Programs.

Navigator refers to Assister Programs that contract directly with the U.S. Centers for Medicare & Medicaid Services (CMS) to provide free outreach and enrollment assistance services to consumers in FFM and in FPM states.1 ,2 Under the ACA, Navigators must conduct public education and outreach, help consumers apply for subsidies, facilitate enrollment in qualified health plans (QHP), and provide consumers with fair and impartial information about their QHP options. In addition, Navigators must refer consumers to applicable state ombudsman or Consumer Assistance Programs (CAPs) for help with any grievance, complaint or question about coverage once enrolled. Navigators must complete 20-30 hours of federal training to become certified; in some states additional state training requirements apply. CMS also requires Navigators in FFM and FPM states to periodically report data on their activities and performance. Under the ACA, Navigators must be funded by grants from Marketplace operating revenue. However, because there was no operating revenue as of the first Open Enrollment period, CMS funded Navigators out of their pool of other implementation funds. For Fiscal Year 2014, CMS awarded $67 million in federal grants to federal Navigators in 34 states (29 FFM and 5 FPM states).

In Person Assister (IPA) refers to Assister Programs that contract directly with SBMs or FPMs to provide free outreach and enrollment assistance. The duties and standards for IPAs generally mirror those of Navigators. This category of Assister Program was created through federal regulations to allow SBMs and FPMs to use federal exchange establishment grants to fund Assistance Programs.3 In later years, these Marketplaces, like all others, will be required to fund Navigator Programs out of Marketplace operating revenue. Unlike Navigators, which operate under a standard set of rules across states, there is more variation in the size, structure, and functions of IPA Programs. In some states, IPAs are paid on a per-enrollment basis, while in other states they are funded through grants. Additionally, in some states IPAs provide both outreach and enrollment assistance while in other states their primary responsibility is enrollment assistance. In some states, IPA Programs are also called Navigators; however, for purposes of this report, they are categorized as IPAs. For Fiscal Year 2014, 17 SBM and 5 FPM states together allocated over $100 million for their IPA Programs.

Certified Application Counselor (CAC) refers to an Assister Program that is recognized by a Marketplace as a trained Assister but that does not receive direct funding from a Marketplace. CACs also must provide assistance to consumers free of charge. Under federal rules, the duties of CACs are less extensive than that of Navigators or IPAs. In particular, CACs are not required to engage in outreach, though many do. Training requirements for CACs are also less extensive than for Navigators or IPAs. States have flexibility to require additional standards for CACs. CAC Programs must register with the Marketplace and must ensure that their individual Assisters follow applicable standards. Although not funded by the Marketplaces, many CAC Programs received funding from outside sources.

Federally Qualified Health Center (FQHC) refers to Assister Programs operated by health centers that receive federal funding to provide comprehensive primary care services. These health centers have a mission to treat anyone regardless of their ability to pay; as a result, their patients are primarily low-income and many are uninsured. Health centers also have a long history of helping patients apply for Medicaid, the Children’s Health Insurance Program (CHIP), or other coverage. In July 2013, HRSA awarded $150 million to 1,159 health centers in every state and DC to facilitate enrollment of uninsured people into new coverage options available under the ACA. In December 2013, HRSA awarded an additional $58 million in one-time funding to support the anticipated surge in demand for enrollment assistance. In addition, HRSA awarded $6.4 million to state and regional Primary Care Associations (PCA) to provide technical assistance and other support to FQHC Assister Programs. Some FQHC Assister Programs also applied to be Navigators or IPAs and received additional direct funding from Marketplaces. For purposes of this report, all FQHCs are categorized as FQHC Assister Programs even if they also served as Navigators or IPAs.

Federal Enrollment Assistance Program (FEAP) refers to Assister Programs that contracted with CMS to provide supplemental enrollment assistance services within FFM and FPM states in select communities with large numbers of uninsured. Duties and requirements of FEAPs are similar to those of federal Navigators, except that FEAPs provide “surge” assistance. Most have rolled back staff and operations since Open Enrollment ended. In the fall of 2013, CMS awarded contracts totaling $37.5 million to two organizations to establish FEAPs in 13 states.4 FEAP contracts were for one year, with an option for CMS to elect a second year of work by the end of July 2014.

In addition to Marketplace Assister Programs, the ACA authorized creation of state-based ombudsman programs, also called Consumer Assistance Programs, or CAPs. CAPs offer eligibility and enrollment assistance to all state residents, those seeking to enroll through Marketplaces as well as people covered under large employer plans and other non-Marketplace coverage. CAPs also help consumers resolve questions and problems with health coverage once they are enrolled – including appealing denied claims on consumers’ behalf – and health plans must include notice about CAP help on all explanation of benefit (EOB) statements. Under the ACA, Navigators and other Marketplace Assister Programs are required to refer consumers to CAPs for help with such post-enrollment problems. Thirty-five state CAPs were established with federal grants in 2010. Subsequent funding awards were made in 2011 and 2012, but none since. Many CAPs continue to operate, though some at reduced levels. In addition, some CAPs are working as Navigators, IPAs, and CACs. This report discusses coordination with CAPs by other Assister Programs.

Key Findings: Section 1: Characteristics Of Assister Programs

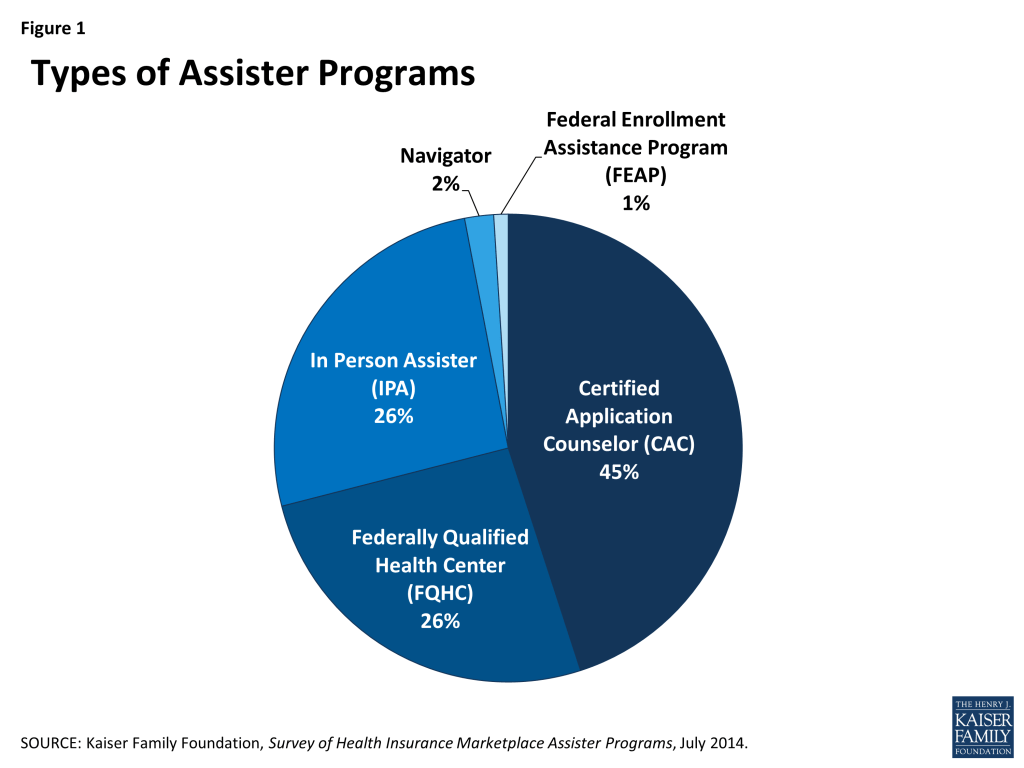

In all, more than 4,400 Marketplace Assister Programs were established to help consumers during the first Open Enrollment. This total is based on Program data provided by all state and federal Marketplaces. Certified Application Counselor Programs (CACs) account for the largest number of Assister Programs, representing 45% of the total Programs and operating in most states. These Programs are likely most numerous because they faced fewer requirements to get started, needing only to complete the online training and register with the Marketplace. Programs sponsored by Federally Qualified Health Centers (FQHCs) accounted for 26% of total Assister Programs and operated in every Marketplace. Another 26% of Assister Programs are In Person Assisters (IPAs) operating in states with State-based Marketplaces (SBMs) and Consumer Assistance Federal Partnership Marketplaces (FPMs). While Navigators, which operated in states with a Federally-facilitated Marketplace (FFM), represented only 2% of the total number of Assister Programs, they were more likely to subcontract with other organizations. As a result, the total number of organizations that operated as Navigators is likely somewhat greater than this figure suggests (Figure 1).

Health care providers, including FQHCs and hospitals, along with non-profit community-based organizations sponsored the majority of Assister Programs. Although a variety of organizations decided to develop and implement Assister Programs, FQHCs and other health care providers sponsored 43% of Assister Programs nationwide. Provider organizations have long played a role in connecting consumers to coverage so it is perhaps not surprising that they signed up in large numbers. Nonprofit community service organizations sponsored another 38% of Assister Programs nationwide. State and local agencies make up about 8% of Assister Programs, though these mostly operate in states that elected to expand Medicaid eligibility. Churches, legal aid organizations, colleges and universities, and trade associations also sponsored Assister Programs (Figure 2).

Most Assister Programs (70%) report having some prior experience providing consumer assistance. Two-thirds of Programs had experience helping people enroll in Medicaid and CHIP prior to Open Enrollment. Just over one-quarter of Programs had helped consumers with post-enrollment health coverage problems, such as denied claims. Only 16% of Programs had previously helped consumers enroll in private health insurance. Nine percent reported experience helping with tax preparation or filing for tax subsidies (Figure 3).

Most Assister Programs served specific geographic areas or targeted population groups. Just 13% of Assister Programs operated in a statewide service area, the rest served more targeted regions or populations.5 Programs that contracted directly with Marketplaces (Navigators, IPAs and FEAPs) were somewhat more likely to report statewide service areas. This is likely because Marketplaces sometimes favored applicants who would operate statewide. Most Assister Programs also operated independently, but one-in-five worked as part of a formal network or coalition of sub-contracting organizations. Navigators, IPAs and FEAPs were more likely to operate as part of a formal coalition (Table 1).

Assister Programs varied in size and in the number of consumers they helped. The majority of Programs have a small staff; 71% have five or fewer full-time-equivalent (FTE) staff (paid or volunteer), while 5% of Programs have more than 20 FTE staff. CACs were more likely than other Assister Programs to have small staffs, with 81% reporting fewer than five FTEs. CACs were also more likely to rely primarily on volunteers (18% vs. 2% for FQHCs and 9% for other Programs).

Almost half of all Assister Programs report providing eligibility and enrollment assistance to no more than 500 people during Open Enrollment, with 20% of Programs helping 100 or fewer people. The CAC Programs were most likely to report helping smaller numbers of people; only 19% of CAC Programs said they helped more than 1,000 people. By contrast, 67% of FQHC Programs and 36% of other Marketplace Assister Programs reported helping more than 1,000 people during Open Enrollment.

| Table 1. Assister Programs by Size, Service Area, and Numbers of People Helped | ||||

| Program Characteristics | All Assister Programs | Program Type | ||

| CAC | FQHC | IPA, Navigator, and FEAP | ||

| Independent vs. part of a coalition | ||||

| Independent | 72% | 76%c | 73%c | 64% |

| Part of a coalition | 20% | 16% | 17% | 28%ab |

| Don’t know/No answer | 8% | 8% | 9% | 8% |

| Statewide vs. specific geographic service area | ||||

| Statewide | 13% | 12% | 8% | 18%ab |

| Specific area within state | 85% | 86% | 88% | 81% |

| Other | 2% | 2% | 4% | 2% |

| Paid staff vs. volunteer | ||||

| Most/all volunteers | 11% | 18%bc | 2% | 9%b |

| Most/all paid staff | 89% | 82% | 98% | 91% |

| Number of full-time-equivalent staff and volunteers | ||||

| 5 or fewer | 71% | 81%bc | 63% | 64% |

| 6-10 | 16% | 9% | 25%ac | 18%a |

| 11-20 | 7% | 6% | 6% | 9% |

| 21-50 | 3% | 1% | 3% | 6%a |

| More than 50 | 2% | <1% | 1% | 4%b |

| Don’t know/No answer | 1% | 1% | 1% | <1% |

| Number of consumers helped during Open Enrollment | ||||

| 100 or fewer | 20% | 33%bc | 1% | 17%b |

| 101-500 | 29% | 35%b | 16% | 31%b |

| 501-1,000 | 14% | 14% | 15% | 14% |

| 1,001-2,500 | 17% | 10% | 33%ac | 13% |

| 2,501-5,000 | 10% | 6% | 17%ac | 9% |

| More than 5,000 | 10% | 3% | 17%a | 14%a |

| No answer | 1% | <1% | 1% | <1% |

| a indicates a statistically significant difference from CAC, p<.05b indicates a statistically significant difference from FQHC, p<.05c indicates a statistically significant difference from IPA, Navigator, FEAP, p<.05NOTE: Numbers may not sum to 100% due to rounding. | ||||

Assister Program budgets were mostly modest. Thirty percent of all Assister Programs report having an annual budget of $50,000 or less.6 Almost as many Programs (26%) had annual budgets between $50,000 and $200,000. Only 5% of Programs reported annual budgets larger than $500,000. CACs tended to have the smallest Program budgets compared to other types of Assister Programs7 (Table 2).

CACs were most likely to rely on re-programmed resources from their sponsoring organization or on other private sector support. FQHCs relied more heavily on grants from HRSA, while Marketplace Assister Programs (IPAs, Navigators and FEAPs) relied more heavily on direct payments from the Marketplaces.

| Table 2. Assister Program Budgets and Sources of Funding, FY 2014 | ||||

| All Assister Programs | by Program Type | |||

| CAC | FQHC | IPA, Navigator, FEAP | ||

| FY 2014 Program budget | ||||

| Up to $50,000 | 30% | 46%bc | 9% | 25%b |

| $50,001 – $200,000 | 26% | 16% | 45%ac | 25%a |

| $200,001 – $500,000 | 9% | 3% | 13%a | 15%a |

| $500,001 – $1,000,000 | 4% | 1% | 2% | 11%ab |

| More than $1,000,000 | 1% | 0% | 1% | 3% |

| Don’t know/No answer | 29% | 33% | 29% | 22% |

| a indicates statistically different from CAC, p<.05b indicates statistically different from FQHC, p<.05c indicates statistically different from IPA, Navigator, FEAP, p<.05Numbers may not sum to 100% due to rounding. | ||||

| Programs receiving most (>50%) of budget from this funding source* | ||||

| Grants or other direct payment from Marketplace | 24% | 20%†b | 7% | 51%ab |

| Grants from HRSA, other federal agency | 30% | 14%c | 81%ac | 4% |

| Grants or payments from other state agencies | 8% | 6% | 4% | 19%ab |

| Grants from private foundations | 6% | 8% | 1% | 4% |

| Grants from other outside private sources | 2% | 5% | 0% | 0% |

| Funds re-programmed from sponsoring organization’s own budget | 22% | 41%bc | 5% | 14%b |

| † Though not required to do so, some SBMs provided funding for CAC Assister Programs.a indicates a statistically significant difference from CAC, p<.05b indicates a statistically significant difference from FQHC , p<.05c indicates a statistically significant difference from IPA, Navigator, FEAP, p<.05*Percentages reflect Programs responding. Numbers do not sum to 100% because not all Programs received most funding from single source. | ||||

Assister Programs engaged in a range of activities during Open Enrollment. Virtually all Assister Programs reported providing eligibility and enrollment help to consumers, helping them apply for private health insurance and subsidies, as well as Medicaid and CHIP coverage when these options were available. Over 80% of Programs also provided outreach and education to individuals and families. These outreach efforts were important to making sure consumers understood what their coverage options were and how to apply for financial assistance.

After eligibility and enrollment assistance and outreach to individuals, the next most-often named activity (named by 77% of Programs) was helping consumers with post-enrollment questions and problems, such as denied claims. More than half of Programs also reported helping people appeal eligibility determinations. Only about one-third of Assister Programs engaged in outreach and enrollment assistance to small businesses (Table 3).

| Table 3: Assistance Activities Conducted by Assister Programs | |

| Activity | % Programs |

| Help individuals apply for premium tax credits and cost sharing subsidies | 91% |

| Help individuals apply for Medicaid/Children’s Health Insurance Program | 88% |

| Help individuals compare private health insurance plan (QHP) options | 83% |

| Outreach and public education to individuals and families | 82% |

| Help individuals with post-enrollment questions and problems (e.g., denied claims) | 77% |

| Help individuals with appeals of eligibility determinations | 59% |

| Help individuals apply for exemptions from the individual responsibility requirement | 50% |

| Help other Assister Program staff resolve questions or problems for their clients | 49% |

| Help individuals apply for other public benefits and services | 47% |

| Outreach and public education to small businesses | 31% |

| Help employees of small businesses enroll in health coverage | 28% |

Key Findings: Section 2: How Many Assisters Are There And How Many People Did They Help?

Based on numbers of staff reported by Assister Programs, we estimate all Programs combined employed at least 28,000 full-time equivalent (FTE) staff and volunteers to provide assistance across the country. In addition, we estimate this cadre of trained Assisters together helped 10.6 million people apply for coverage and financial assistance during the Open Enrollment period from October 1, 2013 through the end of April, 2014. These estimates were derived by extrapolating survey responses (on how many full time equivalent staff worked for Assister Programs and how many people Programs helped) to data on the number of Assister Programs nationwide collected from the Marketplaces.

The estimated number of consumers helped includes those who ultimately enrolled in QHPs as well as those determined eligible for Medicaid and CHIP, both in states that expanded Medicaid coverage and in states that did not. This number also includes individuals who received assistance applying for coverage even if they fell into the “coverage gap” in states not expanding Medicaid – meaning they had income too low to qualify for premium tax credits (which are only available at incomes between 100% and 400% of the federal poverty level) and were also not eligible for Medicaid – and others who did not enroll in coverage for other reasons (Appendix Table 1).

Key Findings: Section 3: How Assistance Was Distributed Across State Marketplaces

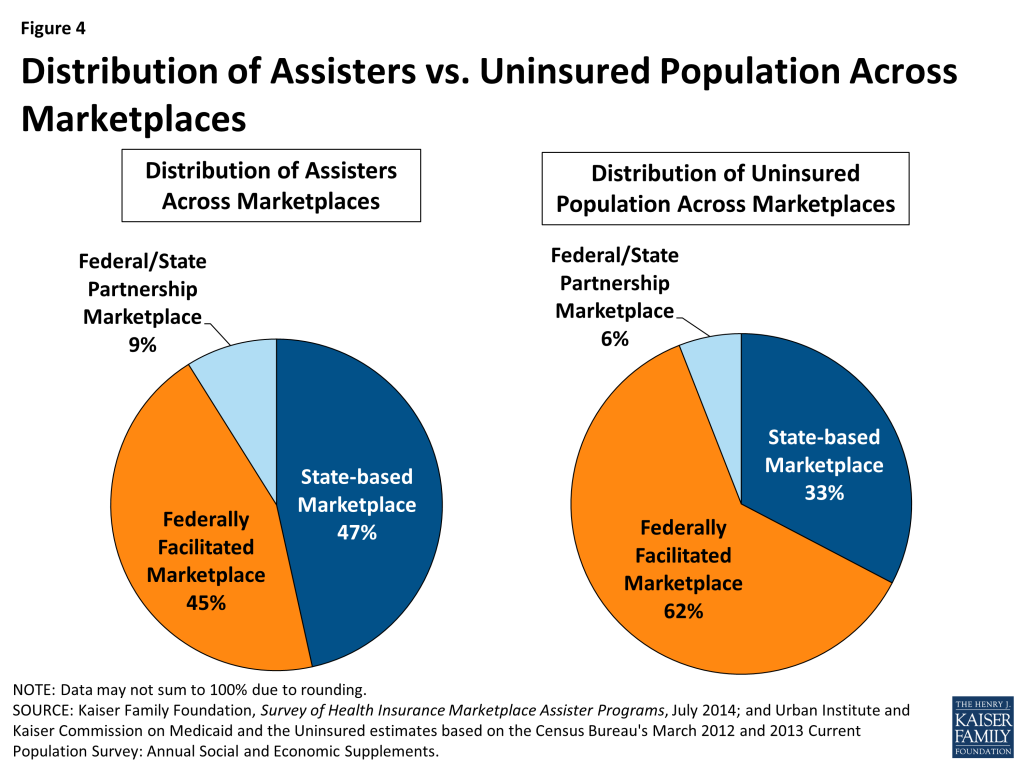

Of the estimated 28,000 Assisters, 47% worked in the 16 states and the District of Columbia with an SBM, 45% worked in the 29 states with a FFM, and 9% worked in the five states with a FPM. The distribution of the U.S. uninsured population across state Marketplaces is somewhat different. Only 33% of the uninsured live in SBM states, while 62% live in FFM states, and 6% live in FPM states (Figure 4).

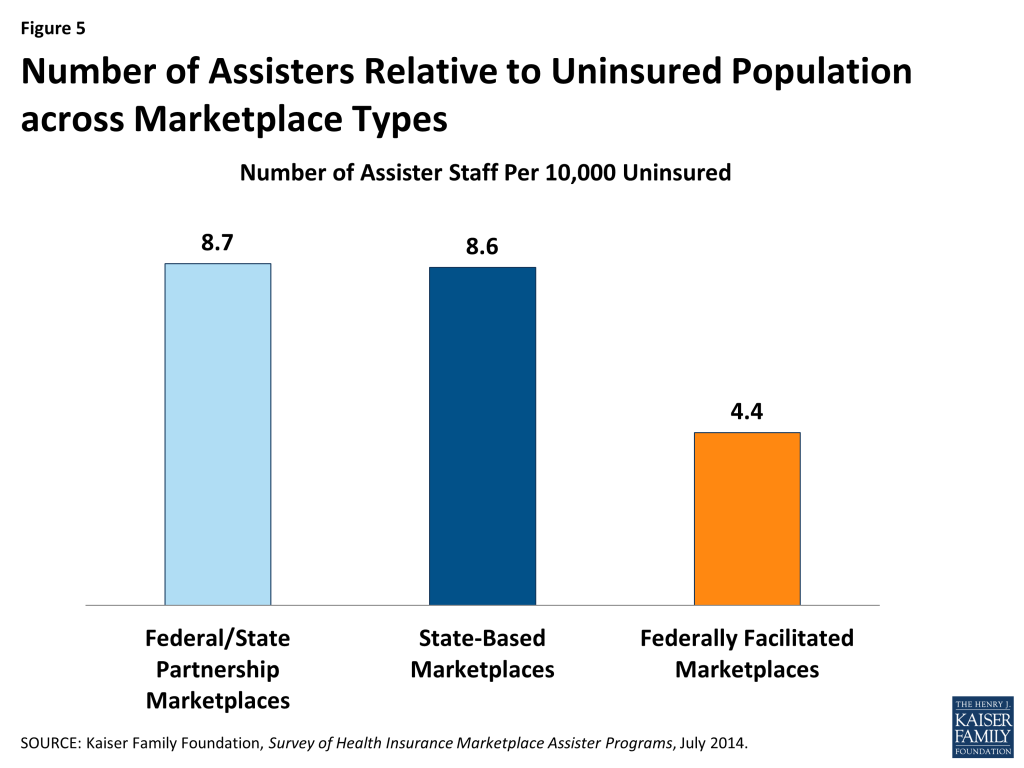

As a result, FFM states, on average, had about half the number of Assisters per 10,000 uninsured compared to FPM states and SBM states (Figure 5).

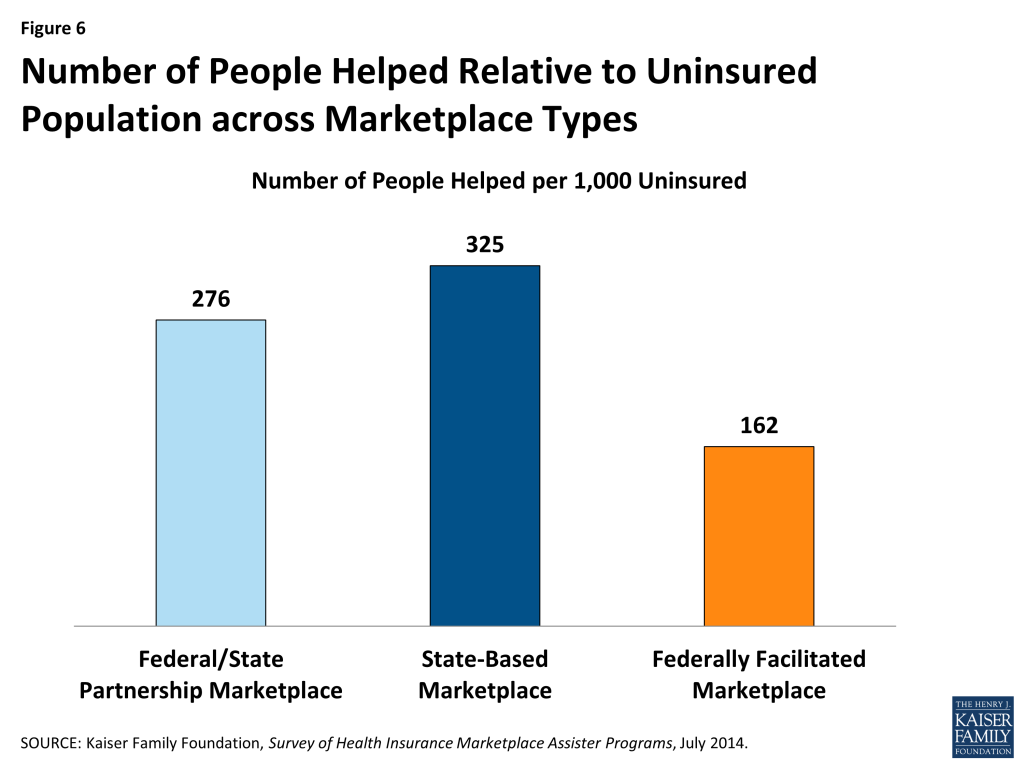

The number of people helped by Assister Programs was similarly distributed across Marketplaces. We estimate a total of 5.0 million people were helped in SBM states, 4.8 million in FFM states, and 0.8 million in FPM states. Expressed relative to the uninsured population in these types of Marketplaces, an estimated 325 people received help per 1,000 uninsured living in SBM states and 276 people per 1,000 uninsured in FPM states. By contrast, 162 people per 1,000 uninsured are estimated to have received help in FFM states (Figure 6).

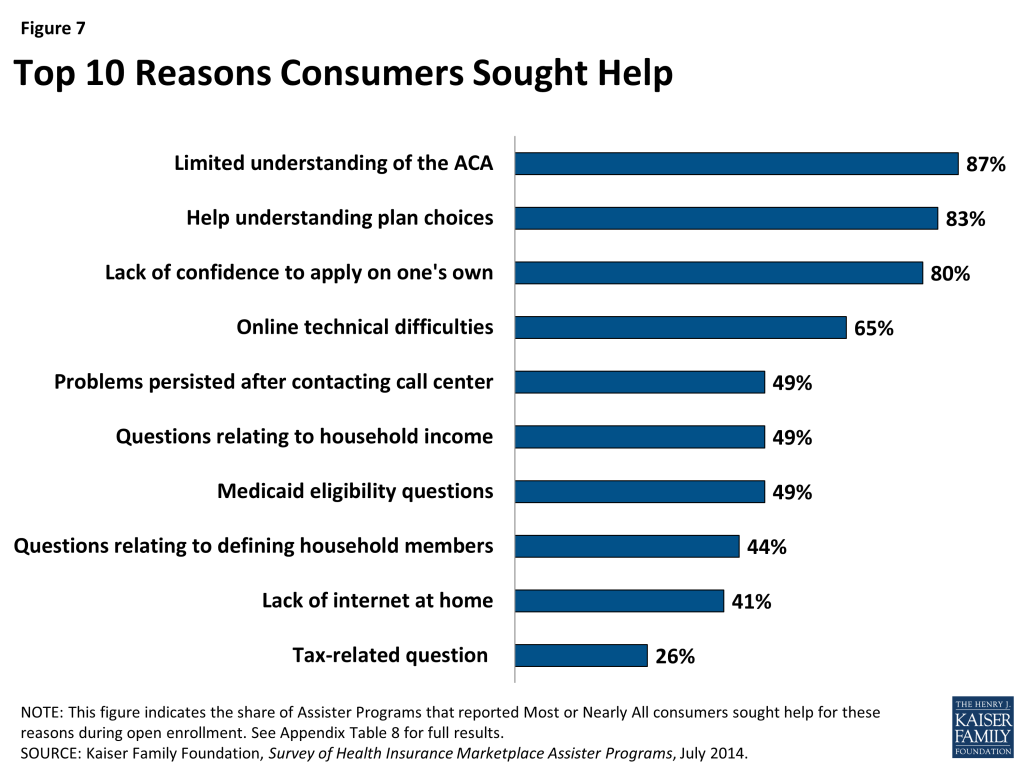

Key Findings: Section 4: Why Did Consumers Seek Help?

Many consumers in search of health insurance sought a more human touch to find their way through the enrollment process. Assister Programs report that, in large numbers, consumers sought help because they didn’t understand the ACA, didn’t understand health insurance, or lacked confidence to apply for coverage and financial assistance on their own. Assister Programs also report that consumers struggled with web site outages, subsidy eligibility rules based on the tax code, and breakdowns in communication between Marketplace systems and Medicaid agencies. Marketplace call centers couldn’t resolve all problems over the phone and significant numbers of consumers lacked internet service at home (Figure 7). For these and other reasons, consumers sought help from Assister Programs.

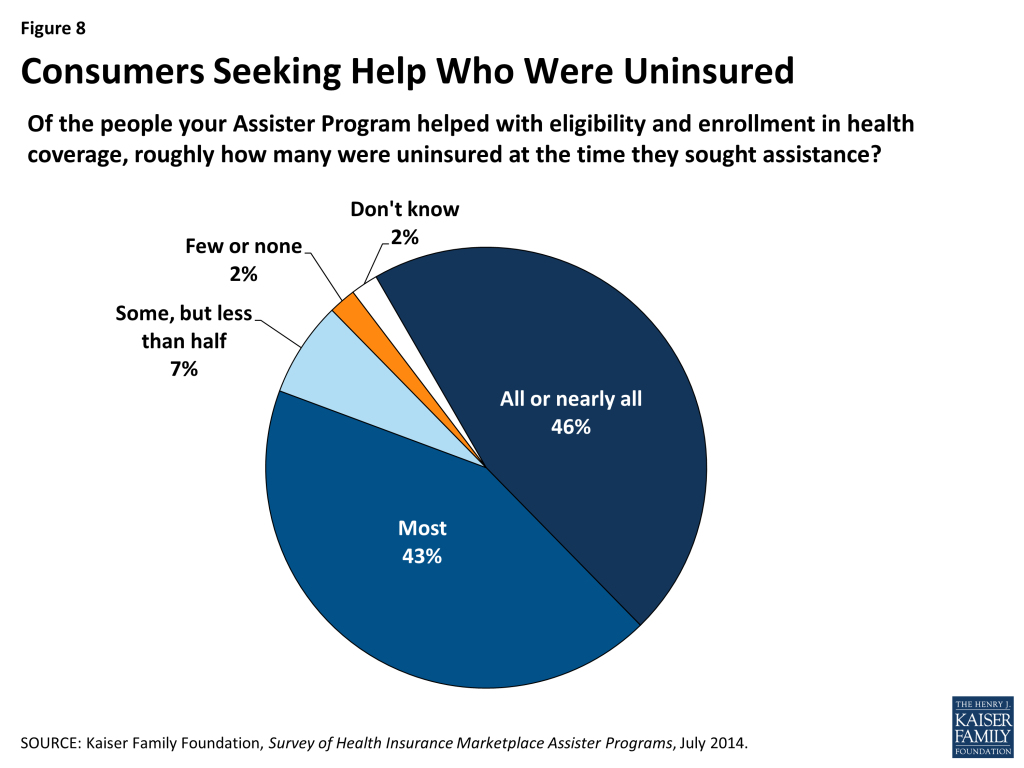

Most who sought help were uninsured. Almost 90% of Assister Programs say most or nearly all of their clients were uninsured at the time they sought help (Figure 8).

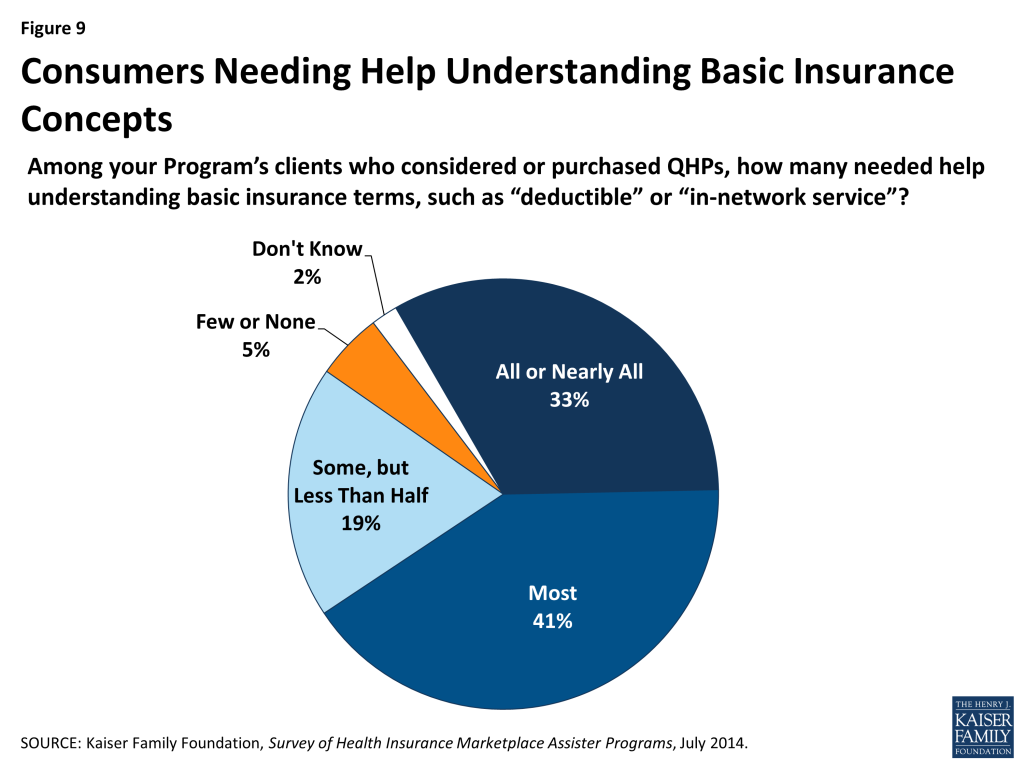

Many who sought help also had limited health insurance literacy. About three-quarters of Assister Programs said that most or nearly all clients who considered buying private coverage needed help understanding basic insurance terms and concepts such as “deductible” and “in-network service” (Figure 9).

Key Findings: Section 5: Challenges Facing Assister Programs

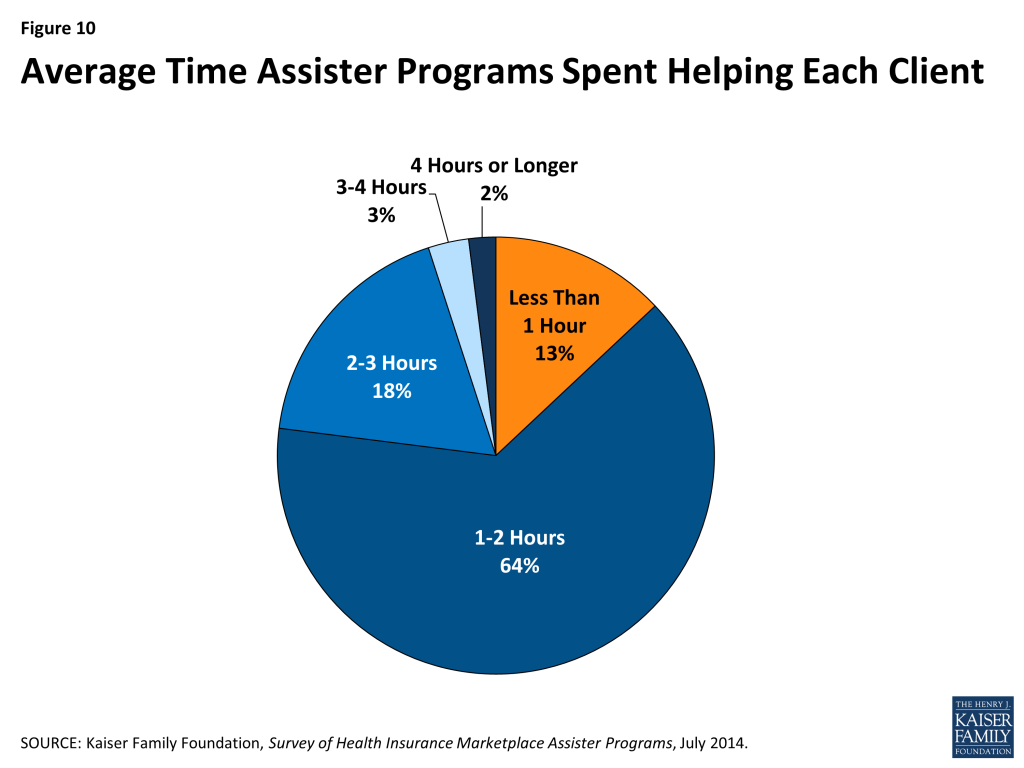

Eligibility and enrollment assistance is time-intensive. More than 60% of Programs report that eligibility and enrollment assistance required, on average, one to two hours per person. For another 23% of Programs, the average time spent helping an individual exceeded two hours. Only 13% of Programs report taking less than one hour, on average, to help each person (Figure 10).

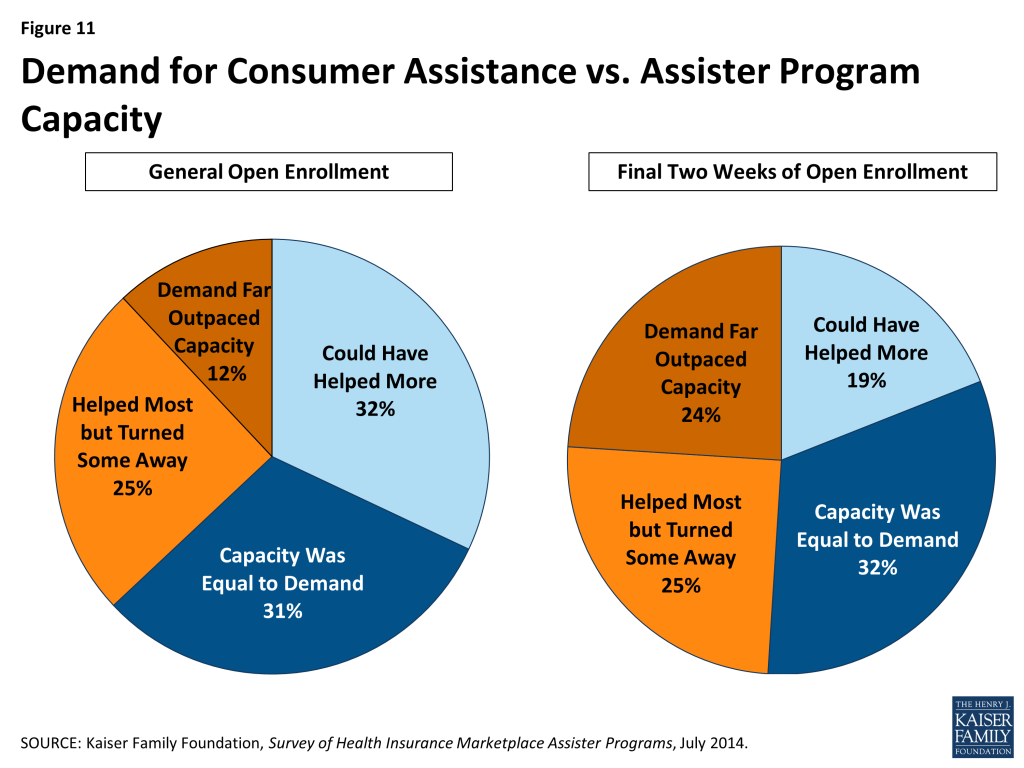

Demand for consumer assistance sometimes exceeded capacity. For the first Open Enrollment period overall, most Assister Programs found they had enough staff and other resources to help most people who sought help most of the time. Close to four in ten Assister Programs, though, report they could not help all who sought assistance; 12% said the demand for help far exceeded their capacity to provide it.

In the last few weeks of Open Enrollment, when over three million people enrolled in QHPs, capacity was further strained.8 One in four Assister Programs report demand for help far outpaced their capacity to provide it during the final two weeks of Open Enrollment (Figure 11).

Helping consumers overcome web site problems posed the greatest challenge for Assister Programs. Just like consumers, Assister Program staff often had difficulty overcoming Marketplace web site problems. Sometimes Assisters could figure out workarounds to bypass online glitches. (For example, faced with persistent problems getting clients through the online application identity verification process, Assisters learned that entering a client’s data in all capital letters could often resolve the problem.) Even so, Assister Programs faced many online technical difficulties. Figure 12 shows the consumer problems and questions Assister Programs found most difficult to resolve.

Shortcomings in available health plan information hindered the ability of Assister Programs to help consumers evaluate QHPs. Another common challenge had to do with the quantity and quality of health plan information available through the Marketplace. Eighty-nine percent of Assister Programs report that at least some of their clients who considered QHPs had questions that weren’t easily answered by information posted on the Marketplace web site; 41% said this was often or almost always a problem for their clients (Figure 13). This finding varied little by Marketplace type or Program type.

To provide better support for consumers evaluating QHP options, 39% of Assister Programs would like to receive more training on the health plans offered in their Marketplace (Appendix Table 2). In response to open ended questions, Programs also expressed hope that Marketplaces will develop more health plan rating tools and online plan comparison tools. Some Assister Programs reported that they received briefings by insurance companies on the health plans they offer and found this very helpful. Other Programs recommended that Marketplaces provide Assisters with more comprehensive QHP information (or require insurers to provide it), and that Marketplaces require insurance companies to make dedicated help lines available to Assister Programs. Some Programs partnered with insurance brokers and agents, who often have access to additional plan information and marketing materials; Programs that did so reported these types of partnerships were helpful.

Explaining ACA requirements to consumers was most difficult for one in four Assister Programs. This likely reflects the complexity of new ACA eligibility rules and processes, generally. It may also reflect unique complexities for populations targeted by some Assister Programs – for example, immigrant populations or families with mixed-eligibility status. Some Programs sought help from outsiders with specialized expertise – for example, tax preparers, immigration advocates, or family lawyers – and when they did so, generally found these partnerships very helpful.

Immigration verification and other identity verification problems were encountered less often by Assister Programs, but when these problems arose they could be challenging. Twenty-two percent of Programs cited immigration-related problems as the most difficult to help with. For example, some immigrants who did not have established credit ratings had difficulty proving their identity and establishing a Marketplace account. Others encountered “the yellow screen of death,” a term Assisters used to describe a web site crash triggered when Marketplace computers and Department of Homeland Security computers could not communicate effectively. Some low-income immigrants who had been living in the U.S. less than five years had difficulty applying for coverage when the Marketplace determined they should be eligible for Medicaid, even though immigrants in this situation cannot enroll in Medicaid and are supposed to be offered premium tax credits instead. Eventually CMS established a “limited circumstances special enrollment period (SEP)” for immigrants who received incorrect eligibility determinations due to system errors so that they would have a chance to re-apply for private coverage and subsidies.9

Programs also report difficulty resolving identity verification problems for consumers. Nearly one in five Assister Programs reported these cases were the most difficult to help. (Figure 12) Such problems could arise among young adults with no established credit history. The Marketplaces relied on a commercial credit rating company to automatically verify consumer identification; if people with no credit history could not pass the online system, they would have to provide paper documents to prove their identity before they could complete applications.

Problems with Medicaid and CHIP eligibility determinations also proved challenging for some Assister Programs. Though the ACA requires a single, streamlined application system for all insurance affordability programs – whether private plan subsidies, Medicaid, or CHIP – this was not operational in most states for the first Open Enrollment period. In addition, the FFM had ongoing technical difficulties transmitting consumers’ application data to state Medicaid programs.10

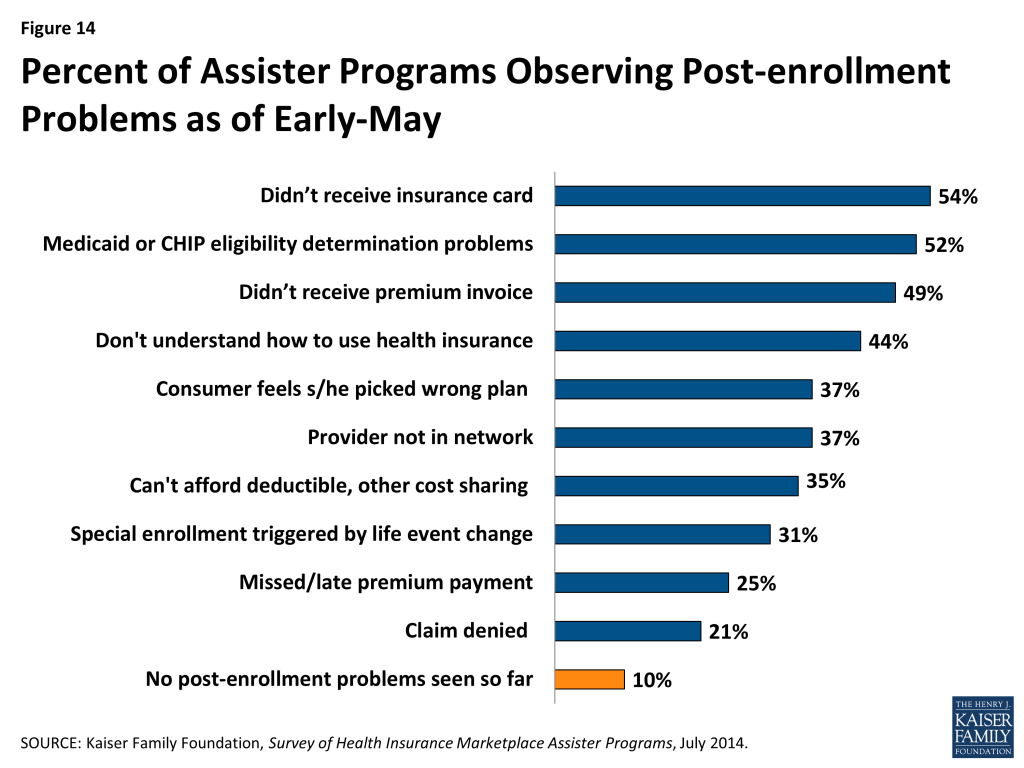

Nine in ten Assister Programs have already seen clients with post-enrollment problems. Within days after the first Open Enrollment ended, nearly all Assister Programs reported consumers were already returning to seek help with post-enrollment problems. Some of these problems had to do with consumers not yet having received their new insurance cards or their first premium invoice from the health insurer. But other post-enrollment problems related to consumers not understanding how coverage works. Programs have also been contacted for help resolving denied claims, out-of-network claims, or deductible and co-pay expenses that consumers can’t afford to pay (Figure 14).

Nearly all Assister Programs report they will try to help consumers with denied claims, disputes with insurers, and other such post-enrollment problems, even though most lack training in this area (Appendix Table 2), and even though they are not required to do so. The ACA requires Marketplace Assisters (Navigators, IPAs, and FEAPs) to refer consumers with post-enrollment problems to state CAPs.

Under the ACA, State Consumer Ombudsman or CAPs are established to provide comprehensive services to all state residents, including people in employer plans or other non- Marketplace coverage. Like other Marketplace Assisters, CAPs are required to conduct public education and outreach, help people apply for subsidies, and answer questions. In addition, CAPs are required to help consumers resolve disputes and appeal denied claims. Furthermore, all health plans are required to include on all claims statements contact information for the state CAP and a notice that CAPs can file appeals on behalf of consumers.

The ACA appropriated $30 million in initial CAP funding and authorized future appropriations at “such sums as may be necessary,” but to date no new appropriations have been legislated. Thirty-five state CAPs were established in 2010 with the initial appropriation, and the last round of CAP grants were awarded in 2012.11 Pending additional federal funding, some CAPs remain operational, albeit at reduced levels.

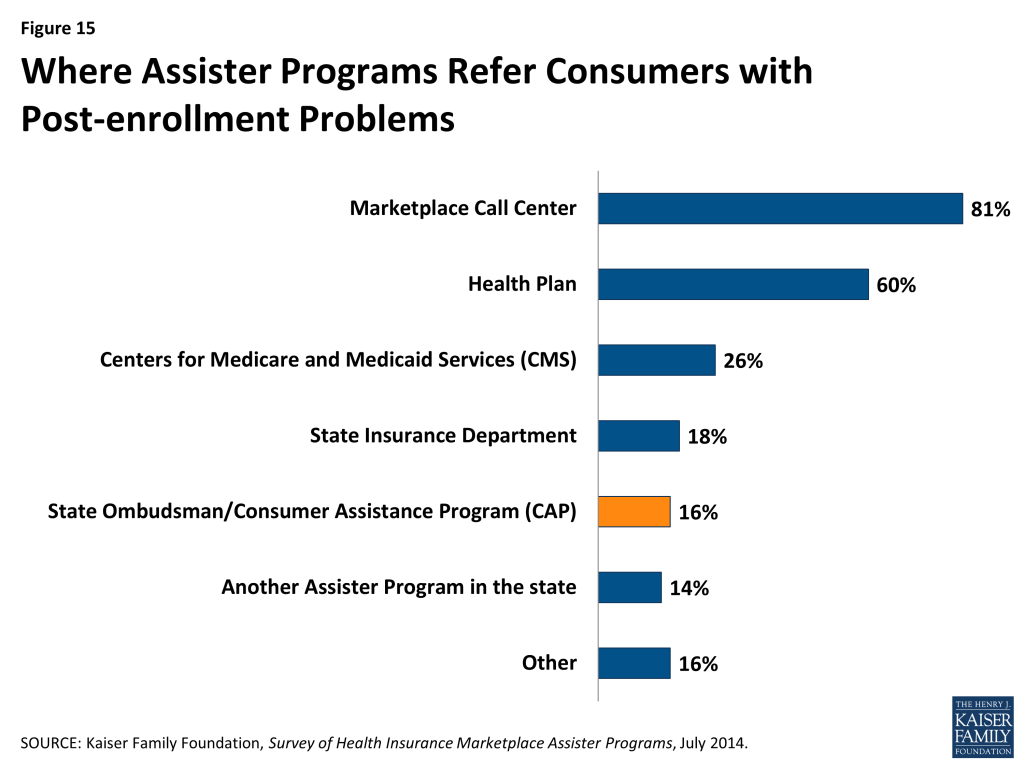

For the most part, Marketplace Assister Programs do not refer consumers with post-enrollment problems to CAPs. Instead, when they encounter a post-enrollment problem they can’t resolve themselves, 81% say they refer consumers to the Marketplace call center, while 60% refer consumers back to their health plan (Figure 15).

Key Findings: Section 6: What Improvements Do Assister Programs Seek?

In response to open ended questions, Assister Programs identified key resources that helped them be more effective in helping consumers. For example, 40% of Program directors cited training provided by the Marketplaces – in particular, trainings provided throughout the Open Enrollment period as Marketplaces modified online applications to improve functionality, as well as more in depth training modules on key issues covered in initial training sessions. Almost 40% of Assister Programs also said the Marketplace call center helped them to be more effective. The ACA requires all Marketplaces to operate a toll-free call center, and Assister Programs relied on this resource when faced with technical online problems and to resolve more complex consumer problems (Appendix Table 10).

Assister Programs also identified a number of improvements they believe are important to help them assist consumers more effectively.

Assister Programs want more and more timely training. All Assister Program staff undergo initial training to be certified by Marketplaces. Assisters in the FFM had to complete between 5 and 30 hours of training before they could begin helping consumers. In some states, federally certified Assisters were required to complete additional state-required training, which could take up to 3-4 more weeks to complete, before they could begin work. In order to be re-certified next year, Assister Programs recommend that revised training courses be available sufficiently ahead of the start of the next Open Enrollment.

The content of initial training varied depending on the Assister Program. CAC training developed by the federal Marketplace was the most basic, covering information about the individual mandate, assistance available through the Marketplace, the application process, and rules about protecting clients’ personally identifiable information. Federal training for Navigators was somewhat more detailed. Regardless of their initial training, though, 92% of Assister Programs say they would like to receive additional, more in-depth training on specific topics. Training on post-enrollment problems and tax-related issues top the list, followed by immigration-related issues and more training on QHP features and differences (Appendix Table 2). In response to open ended questions, some Assister Programs also recommended training on the online application system itself (Appendix Table 10).

Assister Programs suggest strengthening Marketplace call centers. Virtually all Programs relied heavily on their Marketplace call center to answer questions and resolve problems, though with mixed success. Assister Programs gave Marketplace call centers lower marks for helpfulness (only 69% of Assister Programs rate Marketplace call centers as very or somewhat helpful). In response to an open ended question about what Marketplaces should improve, half of Programs cited their call center. Programs say it could be difficult to get through to call center operators, particularly during peak enrollment periods. They also cited shortages in bilingual call center staff. In addition, some complain that call center representatives didn’t always provide accurate or consistent information (Appendix Table 9 and 10).

Programs in Marketplaces that provided a dedicated call center line for Assisters reported this technical assistance was more effective. Programs in Marketplaces without a dedicated Assister help line expressed the need for one. (Appendix Table 10)

Assister Programs acknowledged the value of coordination among Programs. Assister Programs that coordinated efforts reported improved efficiency in a number of areas, though not all Programs coordinated. Almost one-quarter of Assister Programs report they coordinate with other Programs often and on a regular basis. Another 22% coordinated often but on an ad hoc basis, while 54% of programs report they never coordinated with other Programs or did so only infrequently (Figure 16).

When Programs did coordinate with each other, most often they said coordination was initiated by Assisters themselves or facilitated by an outside entity other than the Marketplace. Less than 20% of Programs said their Marketplace facilitated coordination among Assisters. However, in SBM states, regular coordination among Assister Programs was more often initiated by the Marketplace (Figure 17).

Overall, Programs that did coordinate said this was very or somewhat important to their effectiveness in planning outreach events and activities (80%), and in resolving consumers’ complex questions and problems (81%).

Most regularly-coordinating Programs also said it was important in scheduling appointments. In North Carolina, for example, Assister Programs operated a centralized scheduling system. Residents of that state could call a single number and be referred to the nearest Assister Program with available appointments. Programs that coordinated with each other could also share bilingual staff and contractors, and so found it easier to make interpreter services available to consumers (Appendix Table 3). In response to open ended questions, several Programs from states that facilitated coordination also noted the importance of being able to offer real-time feedback to Marketplace officials.

Assister Programs that coordinated regularly with each other tended to engage in a wider range of activities, including outreach and public education, helping small employers, helping individuals with post-enrollment problems, and appeals of eligibility determinations. Coordinating Assister Programs also were much more likely to report helping other Assister Programs (Appendix Table 4).

Other improvements were also suggested by Programs in response to open ended questions. These include:

Web Site Reliability

Programs emphasized the need for better surge capacity to reduce web site slow-downs and repairs of other glitches. They also recommended improvements to Marketplace web site functionality, including development of online chat systems to answer consumer questions, pop-up windows with more detailed instructions on how to complete the online application, better plan comparison tools, and translation of web sites into more languages. Some Programs also urged that consumers not be required to submit an email address in order to apply online.

Assister portal to access the Marketplace enrollment system

In some states Assisters could log into the Marketplace web site through a secure portal, then help consumers complete online applications and track their status. Programs with such access emphasized its usefulness to case management. They could contact the Marketplace about pending verifications and eligibility determinations, and they could re-contact consumers to remind them of needed follow up. Without a portal, case management could be more difficult. For example, 30% of Assister Programs said they did not know the enrollment outcome for a majority of their clients. If consumers delayed picking a plan to a later time, it could be impractical for Assisters to follow up to offer reminders and additional help. Assister portals also facilitated data collection, helping both Marketplaces and Assister Programs, themselves, track performance patterns and the need for further training and technical assistance.

More Marketplace resources for Assisters

In response to an open ended question about suggested improvements, 12% of Programs recommended increasing Marketplace resources, including increased funding for Assister Programs. Some Programs also urged that Marketplaces pay directly for more media advertising and sponsor more outreach and public education events. In addition, some Programs want Marketplaces to make more consumer information resources available, such as handouts explaining ACA requirements and health insurance terms. Some stressed the need for materials translated into other languages and urged that the accuracy of translation needs to be improved in some cases (Appendix Table 10).

Privacy and security standards

Most Programs were satisfied with Marketplace rules for safeguarding clients’ personally identifiable information (PII), but 40% said safeguards were so rigid as to interfere with Assisters’ ability to track client cases and provide follow up assistance (Appendix Table 5). Programs often developed workarounds – for example, all Marketplaces required Assisters to obtain signed consent to provide assistance, and some Programs designed consent forms to also include other key information, such as the client’s eligibility determination, needed follow up steps, and contact information. Other Programs created worksheets for consumers to take with them that recorded account numbers, passwords, information about the plan selected, next-step instructions, and other key information consumers would need to keep and track on their own.

Other Assister Program best practices

In an open ended question about best practices, Programs also recommended strategies they followed to improve the assistance process. For example, 10% of Programs described “pre-screening” procedures they used while making appointments to advise consumers on the kinds of information they might need during the application process. This helped the actual assistance appointment to proceed more smoothly. Some Programs also designated staff to “pre-assist” consumers by helping them set up an email account in advance if they didn’t already have one.

Thirty-three percent of Programs also described partnerships with others in their community who could help with effective outreach or key resources such as meeting space or computer labs. Programs also formed strategic partnerships with tax assisters, insurance brokers, and others offering specialized expertise.

In addition, Programs emphasized the importance of in-house coordination, including regular meetings to share information and seek peer advice. Programs also adopted creative approaches to staff specialization, designating the most expert staff to consult on complex cases and mentor new hires, scheduling specialists to pre-screen clients and ensure availability of interpreter services or accessible assistance when needed, and training specialists assigned to monitor all Marketplace updates and trainings and ensure information was imparted to colleagues (Appendix Table 10).

Key Findings: Section 7: Looking Ahead

The vast majority (84%) of Assister Programs say they will continue operating this year after Open Enrollment has closed (Figure 18). People eligible for Medicaid and CHIP can enroll throughout the year, and enrollment in small group health plans is also open to small businesses year round. In addition, millions will qualify for Special Enrollment Periods (SEP) enabling them to enroll in plans outside of Open Enrollment.12

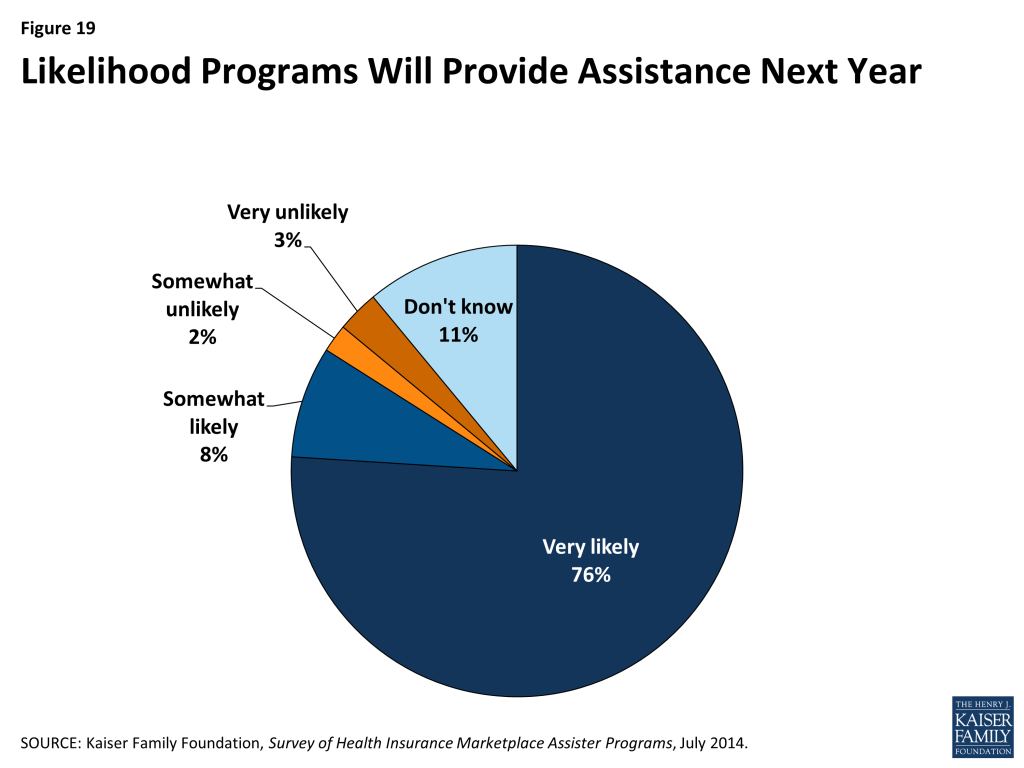

Three-quarters of Programs say it is very likely they will continue offering consumer assistance in the next Open Enrollment Period and into 2015 (Figure 19). This seems to vary based on Programs’ perception of their funding continuity. For example, nearly 90% of FQHCs say they’ll likely continue working next year (Appendix Table 6). HRSA enrollment assistance funds to FQHCs will be ongoing and have been built into health center budgets. FEAPs signed a two-year contract with CMS, though CMS has until later this summer to exercise the option for the second year and had not yet done so when this survey was fielded. CMS announced the availability of funding for FFM Navigators after this survey had closed. At that time, a number of state based Marketplace funding decisions for 2015 were also still pending.

Among Programs reporting they were likely to continue operating, 65% say they expect nearly all of their paid staff and volunteers to continue (Appendix Table 7). This suggests some Assister Programs will need to engage in significant new hiring and certification of staff before the fall. But it also reveals the establishment of a new foundation of assistance capacity in many Programs that, if built upon, can develop into a profession of individuals who understand what consumers need and have the expertise to help them get it.

Key Findings: Implications

The establishment of extensive new consumer assistance resources under the ACA is a significant development in the insurance system. Many consumers have traditionally relied on insurance agents and brokers to help enroll in private coverage and answer insurance-related questions. Even so, consumers have long faced challenges understanding how to navigate coverage options, and have had difficulties understanding their coverage and how to use it once enrolled. And now, for millions of consumers, applying for coverage also requires a new process of applying for financial assistance. Professional Assisters not only can help consumers answer questions, apply for help, and connect to coverage, they can serve as an interface between consumers and Marketplace officials and regulators, providing feedback on what consumers need and how well Marketplaces and health plans are working.During the first Open Enrollment, Assister Programs played a key role in achieving first year enrollment results that exceeded most expectations. In the second year, when Open Enrollment (November 15, 2014 to February 15, 2015) is only half as long, the demand for consumer assistance may very well increase. The Congressional Budget Office projects 13 million people will enroll in QHPs in 2015, compared to 8 million who enrolled during the first Open Enrollment.13 Increasing enrollment will depend first on retention of those already enrolled. Many who are already enrolled may require help renewing their coverage and subsidies, particularly if they experience a change in income or family size that affects their eligibility for subsidies. In addition, nearly all Assister Programs report seeing post-enrollment problems, such as denied claims, missed premiums, or inability to afford cost sharing. Such problems, if not addressed, could prompt some consumers to drop coverage.Ramping up enrollment will also require reaching millions of new people, educating them about what the ACA offers and requires, and getting them enrolled. If it is the case that first year enrollment included people who were most highly motivated or aware of the ACA, then the next increment of enrollment could be somewhat harder to achieve. Assister Programs already working at capacity may be stretched even further in light of these potential increases in consumer demand. In FFM states, especially, where there were fewer Assisters relative to the size of the uninsured population, continued investment in consumer assistance will matter.

Marketplaces can take a number of steps to improve the overall efficiency of Assister Programs. Officials can be encouraged that so many Assister Programs and staff intend to stay on the job. Experience can only enhance Assister efficiency. Marketplaces can seek other ways to foster the professional development of Assisters so that they continue this work over the long term. In addition, Marketplaces can take steps improve their web sites and call centers to reduce delays for both consumers and Assisters. Building Assister portals into online Marketplace application systems could reduce Assister time on hold with call centers and enhance ability to follow up with clients and ensure completed enrollments. Marketplaces can also expand training and technical assistance resources to enhance efficiency of Assister Programs.

Financial support of Assister Programs will also surely matter. The ACA requires that all Marketplaces establish Navigator Programs and pay for them out of Marketplace operating revenues – in effect, building the cost of consumer assistance into the overall cost of coverage. Because Marketplaces did not have operating revenues in time for the first Open Enrollment, this is not how most Programs were financed in the first year. Instead, about $100 million in funding came from Exchange establishment grants, another $208 million came from HRSA grants to FQHCs, and $105 million came from CMS ACA implementation funds.

In fiscal year 2015, CMS expects to collect about $1.2 billion in operating revenue through an assessment on insurers that participate in FFM states.14 For the 2014-2015 cycle, CMS has announced that $60 million will be available for grants to Navigators in FFM states, 90% of the first year total. CMS has not specified the source of this funding or indicated whether an ongoing portion of Marketplace operating revenue may be set aside for consumer assistance or in what amounts.15 In addition, no decision has yet been announced on whether to continue funding for FEAPs for a second year. Most states have yet to announce what the amount or source of their Marketplace Assister Program funding will be for next year. For 2015, HRSA anticipates that health center funding for outreach and enrollment will continue at about the level awarded in July 2013 ($150 million). The level of financial resources for Marketplace Assister Programs (and for CAPs tasked with addressing post-enrollment problems) available in the future remains to be seen.

Methods

The Kaiser Family Foundation (KFF) Survey of Health Insurance Marketplace Assister Programs was designed and analyzed by KFF researchers and administered by Davis Research.The survey was conducted through an online questionnaire from April 24 through May 12, 2014 among Assister Programs nationwide. State- and federal-Marketplaces were asked to provide contact information for all of their Assister Programs. All organizations received an initial email inviting the director of the Assister Program to participate and included a link to the survey. In the event the person receiving the survey was not the appropriate person to complete it, they were asked to provide the contact name and email for someone else with their organization or at an affiliated organization. The survey included Navigators, Certified Application Counselors (CACs), Federally Qualified Health Centers (FQHCs), In-Person Assisters (IPAs), and Federal Enrollment Assistance Programs (FEAPs). To compile the contact information for these Assister Programs, we asked officials from the Federal Marketplace, each of the State-based Marketplaces, and states with a Consumer Assistance Partnership Marketplace to provide names and email contact information for all of their Assister Programs. In addition, we requested contact information for the FQHCs from the Health Resources and Services Administration (HRSA).Although we attempted to include the universe of Assister Programs in the survey, there were some challenges associated with compiling a comprehensive set of Programs. Some Program contacts we collected from the FFM did not include email address information, so we were unable to invite these Programs to participate in the study. As a result, our study may have slightly undercounted the number of Assister Programs in FFM states. It is also important to note that one-in-five respondents (including 28% of IPAs and 42% of Navigators) reported that they operate as part of a coalition of Assister Programs that subcontract with each other. Though respondents were invited to answer survey questions on behalf of their entire Program, most of these coalition respondents told us they provided information only about their member Program within the coalition. As a result, we may have underrepresented IPAs and Navigators for some states in our sample.In analyzing the results, we grouped the Assister Programs by type using the categorization provided to us by the FFM or by the states for Assister Programs in SBMs or FPMs, with the exception of FQHCs. We created a separate category for FQHCs and identified them using the contact list provided by HRSA. All FQHCs, regardless of any other categorization they may have had, were placed in the FQHC category. Because IPAs and Navigators performed similar functions in SBMs and were funded with state resources, we further grouped IPAs and Navigators in these states into a single IPA category. In FPMs, where IPAs were funded with state grants and Navigators funded through federal grants, we kept the Navigator and IPA categories distinct.

A total of 4,445 programs were invited by email to participate in the study, and 843 programs responded and were included (for a response rate of 19%). Some program types were more likely to respond than others, so the data was weighted to reflect the distribution of programs in the initial sample by program type and Marketplace type (SBM, FPM, or FFM). Weighted and unweighted proportions of the final sample by program type are shown in the table below.

| Unweighted % of total | Weighted % of total | |

| FFM CAC | 22% | 33% |

| FFM FQHC | 18% | 14% |

| FFM Navigator/FEAP | 6% | 3% |

| FPM CAC | 2% | 4% |

| FPM FQHC | 2% | 2% |

| FPM Navigator/IPA/FEAP | 4% | 2% |

| SBM CAC | 8% | 8% |

| SBM FQHC | 12% | 10% |

| SBM Navigator/IPA | 26% | 24% |

The number of Assister staff nationwide was estimated by analyzing self-reported figures given by survey respondents. Survey participants were asked to provide the number of full-time equivalent Assisters in their Program by selecting from a range of staff sizes on the questionnaire. For respondents who selected a range response, the midpoint of the range was used. When respondents selected the range, “less than five” a response of 1 was estimated. When respondents selected the range “more than 75” a response of 76 was estimated. For respondents who did not provide a response, staff size was imputed based on the Assister Program type.

The number of consumers helped nationwide was likewise estimated by analyzing self-reported figures given by survey respondents. For respondents who provided a numeric value for the number of people their Program helped, either in person or by phone, those responses were used. For respondents who gave an answer by selecting a range, the midpoint of the range was used. For respondents who did not provide a response, the number of consumers helped was imputed based on the Assister Program type.

Survey toplines with overall frequencies for all survey questions are available at https://www.kff.org/health-reform/report/survey-of-health-insurance-marketplace-assister-programs/

All statistical tests of significance account for the effect of weighting. The sample size and margin of sampling error (MOSE) for the total sample and key subgroups are shown in the table below.

| Group | N (unweighted) | MOSE |

| Total | 843 | +/-4 percentage points |

| CAC | 274 | +/-6 percentage points |

| FQHC | 265 | +/-6 percentage points |

| Navigator, IPA, and FEAP | 304 | +/-6 percentage points |

Appendix Tables

Table A1. Eligibility Determinations Observed by Assister Programs | |||||

Proportion of clients with eligibility determination | Eligible for qualified health plan (QHP) and premium tax credit (PTC) | Eligible for QHP, income too high to qualify for PTC | Eligible for Medicaid or CHIP | Income too high for Medicaid and too low for PTC (“coverage gap”) | Income too high for Medicaid and too low for PTC (“coverage gap”) |

| Few or none | 10% | 65% | 16% | 41% | 41% |

| Some, but less than half | 40% | 26% | 33% | 36% | 36% |

| Most | 38% | 3% | 38% | 12% | 12% |

| All or nearly all | 8% | 0% | 6% | 1% | 1% |

| DK/NA | 5% | 5% | 6% | 10% | 10% |

| Table A2. Topics on which Assister Programs Would Like Additional Training | |

| Topic | % Programs |

| Assisting people with post-enrollment questions about their health plan | 41% |

| Tax filing issues | 41% |

| Immigration-related eligibility | 39% |

| Qualified health plan features and how to distinguish differences between plan options | 39% |

| Appeals | 36% |

| Medicaid and Children’s Health Insurance Program (CHIP) eligibility | 35% |

| Medicare-related issues | 34% |

| Low health insurance literacy | 34% |

| Exemptions | 33% |

| Eligibility for premium tax credits and cost sharing reductions | 32% |

| Special enrollment periods | 27% |

| Using the on-line application system | 26% |

| Availability of employer sponsored coverage | 25% |

| Assisting people who need translation services | 12% |

| Providing culturally competent assistance | 11% |

| Using the paper application | 11% |

| Accessibility for people with disabilities | 8% |

| Privacy and security | 6% |

| There are no additional topics or issues for which we would like additional training | 8% |

| Other | 7% |

| Table A3. Importance of Coordination to Effectiveness of Assistance Activities | ||||||

| Importance of Coordination | Planning Outreach Events | Developing Consumer Information Material | Scheduling Appointments for Enrollment Assistance | Resolve complex questions and problems | Assure availability of translation services | Assure accessible services for people with disabilities |

| Very important | 50% | 38% | 29% | 50% | 25% | 25% |

| Somewhat important | 30% | 32% | 23% | 31% | 22% | 22% |

| Not very important | 10% | 16% | 22% | 8% | 20% | 20% |

| Not at all important | 5% | 9% | 22% | 8% | 24% | 25% |

| DK/NA | 4% | 5% | 4% | 3% | 8% | 8% |

| Table A4. Percentage of Programs Conducting Assistance Activities | ||||

| Activity | Programs that Never Coordinated | Programs that Coordinated a Few Times | Programs that Coordinated Numerous times on Ad Hoc Basis | Programs that Coordinated Numerous Times on Regular Basis |

| Outreach to individuals and families | 50% | 81%a | 91%ab | 94%abc |

| Help with post-enrollment problems | 67% | 74% | 78% | 86%ab |

| Help with appeals of eligibility determinations | 45% | 53% | 65%ab | 71%ab |

| Help other Assister Programs | 20% | 40%a | 63%ab | 66%abc |

| Outreach to small businesses | 11% | 30%a | 34%a | 41%ab |

| a indicates a statistically significant difference from “Never”, p<.05b indicates a statistically significant difference from “A few times”, p<.05c indicates a statistically significant difference from “Numerous, ad hoc”, p<.05 | ||||

| Table A5. How Assister Programs View Balance of Privacy Rules and Ability to Conduct Assistance | |

| Level of Balance | % Programs |

| The balance was about right | 58% |

| The balance tipped too much in favor of privacy and security, limiting ability to track clients and provide follow up assistance | 40% |

| The balance tipped too much in favor of Assister access to PII, reducing privacy and security of client information | 2% |

| Table A6. Likelihood Assister Programs Will Continue for 2014-2015 Open Enrollment | ||||

| Likelihood | All Programs | CAC | FQHC | IPA, Navigator, FEAP |

| Very likely | 76% | 71% | 88%ac | 72% |

| Somewhat likely | 8% | 10%b | 5% | 8% |

| Somewhat unlikely | 2% | 3% | 0% | 2% |

| Very unlikely | 3% | 2% | 1% | 5%b |

| Not sure | 11% | 14% | 5% | 12% |

| a indicates a statistically significant difference from CAC, p<.05c indicates a statistically significant difference from IPA, Navigator, FEAP, p<.05 | ||||

| Table A7. Number of Assister Programs that Expect Staff to Continue Working During 2014-2015 Open Enrollment | |

| Assister Staff Who Will Continue | % Programs |

| Almost all will continue | 65% |

| Most will continue, some will not | 20% |

| Some will continue, most will not | 7% |

| Almost none will continue | 1% |

| DK/NA | 7% |

| Table A8. Reasons Consumers Sought Help and Problems Assister Programs Found Most Difficult to Help With | ||

| Reason | % Programs who say most/nearly all clients sought help for this reason | % Programs who say this reason was the most difficult to help with |

| Limited understanding of ACA | 87% | 27% |

| Help understanding/evaluating plan choices | 83% | 37% |

| Lack of confidence to apply on one’s own | 80% | — |

| Online technical difficulties | 65% | 55% |

| Problems persisting after contacting call center | 49% | — |

| Questions relating to household income | 49% | 13% |

| Medicaid eligibility questions | 49% | 16% |

| Questions relating to defining household members | 44% | 8% |

| Lack of internet access at home | 41% | 17% |

| Tax-related question | 26% | 14% |

| Need translation assistance | 18% | 13% |

| Question related to verifying immigration status | 10% | 22% |

| Help filing exemption | 10% | 7% |

| Questions related to ESI/COBRA | 8% | 17% |

| Other ID proofing question (not immigration related) | 7% | 19% |

| Help with disability | 5% | 3% |

| Table A9. Sources and Usefulness of Technical Assistance for Assister Programs | |||||

| Technical Assistance Offered by Marketplace | Outside Sources of Technical Assistance | ||||

| Resource | % Programs Using Resource | % Rating Very or Somewhat Helpful* | Resource | % Programs Using Resource | % Rating Very or Somewhat Helpful* |

| Online resources, tips, updates for Assisters | 57% | 90% | State primary care association | 15% | 94% |

| Newsletter for Assisters | 51% | 88% | Other Assister Programs | 27% | 93% |

| Webinars for Assisters | 66% | 87% | HRSA | 15% | 93% |

| Periodic networking meetings with other Assisters | 31% | 84% | Technical Assistance offered by other private entities | 9% | 92% |

| Regular calls with Marketplace staff | 37% | 82% | Brokers and agents | 13% | 92% |

| Ad hoc calls with Marketplace staff | 19% | 82% | State insurance department | 11% | 90% |

| Help line dedicated for Assisters | 43% | 77% | Tax preparation organizations | 6% | 81% |

| State Marketplace call center | 46% | 69% | Health insurance company help lines | 18% | 79% |

| Federal Marketplace Call Center | 50% | 69% | State Medicaid agency | 36% | 73% |

| * percentage based on respondents who used the resource | |||||

| Table A10. Assister Program Responses to Open Ended Questions about What Worked Well and What Changes Would Help them be More Effective | |

| Feature or Resource | Percent of Assister Programs |

| Briefly describe up to 3 things the Marketplace did that helped make the work of your Assister Program more effective | |

| Training (net) | 40% |

| Updated training/webinars | 25% |

| Initial training | 9% |

| Call Center (net) | 39% |

| Call center was helpful, generally | 25% |

| Dedicated line for Assister Programs | 12% |

| Assister Resources (net) | 18% |

| Consumer materials by Marketplace | 10% |

| Online resources for Assisters | 6% |

| Funding for Assisters | 2% |

| Marketplace Website | 16% |

| Online application | 8% |

| Live “chat” feature | 2% |

| QHP “window shopping” feature | 2% |

| Coordinating Assisters (net) | 14% |

| Regular calls to share information | 10% |

| Formal networking of Assister Programs | 3% |

| Marketplace staff responsiveness | 5% |

| Outreach by Marketplace (net) | 5% |

| NA | 11% |

| Briefly describe up to 3 things the Marketplace might change to help make the work of your Assister Program more effective | |

| Call Center (net) | 48% |

| Strengthen staff training | 25% |

| Provide dedicated line for Assisters | 16% |

| More call center staff | 12% |

| Website (net) | 42% |

| Fix website glitches | 22% |

| Create portal for Assister online access | 11% |

| Create live “chat” functionality | 5% |

| Training (net) | 27% |

| Make available for initial certification, updates | 14% |

| More in-depth training on specific topics | 7% |

| Training version of online application | 6% |

| Assister Resources (net) | 12% |

| More funding for Assister Programs | 6% |

| More printed resources for consumers | 5% |

| Increase number of Assister Programs | 2% |

| Policy Changes (net) | 8% |

| Improve Marketplace staff responsiveness | 2% |

| Conduct appeals of eligibility denials | 1% |

| Clearer consumer notices | 1% |

| Improve Coordination with Medicaid | 7% |

| Increase Outreach by Marketplace | 6% |

| Coordinate Assister Programs | 5% |

| NA | 6% |

| Briefly describe up to 3 practices of your Assister Program that you would recommend as best practices to others | |

| Model Work Practices | 50% |

| Scheduling strategies | 20% |

| Pre-screen clients to prepare for their appointment | 10% |

| Professional standards | 10% |

| Periodic meetings to coordinate Program staff | 6% |

| Hiring practices | 6% |

| Specialization of Assister staff | 4% |

| Strategic Partnerships | 33% |

| Community partners for outreach | 26% |

| Community partners for expertise | 6% |

| Counseling Skills | 11% |

| Training | 11% |

| Develop Helpful Forms/Worksheets | 10% |

| Casework Strategies | 7% |

| NA | 13% |

Endnotes

- Under the ACA, if a state does not elect to operate a health insurance Marketplace, the federal government must do so. A third option, created by regulation, allows states to take on some of the Marketplace functions in partnership with the federal government. In this report, Partnership Marketplace refers to one where they state has agreed to provide consumer assistance services. In these Marketplaces, states must use exchange establishment grant resources to help finance Assister Programs. The federal government also assumes some responsibility for financing Assister Programs in FPMs. In this report, state grant-funded Assister Programs in FPMs are referred to as IPAs, while federally-funded Assister Programs in FPMs are referred to as Navigators. ↩︎

- or 2014 the FFM states are Alabama, Alaska, Arizona, Florida, Georgia, Indiana, Iowa, Kansas, Louisiana, Maine, Michigan, Mississippi, Missouri, Montana, Nebraska, New Jersey, North Carolina, North Dakota, Ohio, Oklahoma, Pennsylvania, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Wisconsin, and Wyoming. Iowa and Michigan are considered Partnership Marketplaces, but not with respect to consumer assistance duties. The Consumer Assistance FPM states are Arkansas, Delaware, Illinois, New Hampshire, and West Virginia. The SBM states are California, Colorado, Connecticut, DC, Hawaii, Idaho, Kentucky, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, New York, Oregon, Rhode Island, Vermont, and Washington. ↩︎

- The ACA makes available to states a program of grants to finance the establishment of exchanges, or Marketplaces. These exchange establishment grants are unlimited in amount and are available through the end of 2014. To date more than $4.6 billion in state exchange establishment grants has been awarded. Establishment grants may not be used to finance Navigators, per se, but can be used to support other Assistance resources in the early years of state Marketplace operations. ↩︎

- During the first Open Enrollment period, FEAPs operated in Arizona, Florida, Georgia, Indiana, Louisiana, Montana, North Carolina, New Hampshire, New Jersey, Ohio, Pennsylvania, Texas and Wisconsin. ↩︎

- Some organizations sponsored Assister Programs in multiple states. In such cases, respondents were asked to answer survey questions with respect to a single state and were invited to re-take the survey to answer with respect to the other state(s) in which they operated. ↩︎

- Budget refers to the annual resources for the Assister Program, not the budget for the sponsoring entity as a whole. ↩︎

- Questions about Assister Program budgets produced the highest non-response rate; 29% of survey respondents did not supply an answer to this question. ↩︎

- US Department of Health and Human Services, “Health Insurance Marketplace: Summary Enrollment Report for the Initial Annual Open Enrollment Period,” May 1, 2014. Available at http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib_2014Apr_enrollment.pdf ↩︎

- See “Helping Consumers Enroll in Special Enrollment Periods in the Health Insurance Marketplace,” available at http://marketplace.cms.gov/help-us/complex-cases-sep.pdf ↩︎

- Kliff S, “HealthCare.gov is having trouble signing people up for Medicaid,” Washington Post, December 4, 2013. Available at http://www.washingtonpost.com/blogs/wonkblog/wp/2013/12/04/healthcare-gov-is-having-trouble-signing-people-up-for-medicaid/ ↩︎

- For more information about ACA Consumer Assistance Program grants to states, see https://modern.kff.org/health-reform/state-indicator/consumer-assistance-program-grants/ ↩︎

- Life changes that can trigger a special enrollment period (SEP) include, among others, marriage, birth of a child, and loss of eligibility for other coverage due to job change, a move, or other circumstances. See Curtis R and Graves J, “Open Enrollment Season Marks the Beginning (Not the End) of Exchange Enrollment,” Health Affairs blog, November 26, 2013, at http://healthaffairs.org/blog/2013/11/26/open-enrollment-season-marks-the-beginning-not-the-end-of-exchange-enrollment/ ↩︎

- Congressional Budget Office, Updated Estimates of the Effects of the Insurance Coverage Provisions of the Affordable Care Act, April 2014. Available at http://cbo.gov/sites/default/files/cbofiles/attachments/45231-ACA_Estimates.pdf ↩︎

- US Department of Health and Human Services, Fiscal Year 2015 Justification of Estimates for Appropriations Committees, Available at http://www.cms.gov/About-CMS/Agency-Information/PerformanceBudget/Downloads/FY2015-CJ-Final.pdf ↩︎

- The funding announcement says, “HHS expects to award $60,000,000 to recipients pending the availability of funds. If additional funds become available at the end of FY 2014 to award the Navigator cooperative agreements, HHS may award funds in excess of $60 million to applicants applying through this FOA…” See US Department of Health and Human Services, “Cooperative Agreement to Support Navigators in Federally-facilitated and State Partnership Marketplaces,” Initial Announcement, Funding Opportunity Number: CA-NAV-14-002, CFDA: 93.332, June 10, 2014.” ↩︎