Assessing Americans’ Familiarity With Health Insurance Terms and Concepts

Findings

With the approaching launch of the second open enrollment period for the Affordable Care Act’s (ACA) health insurance exchanges and at a time when open enrollment is also happening for many job-based plans, the Kaiser Family Foundation conducted a nationally representative survey of 1,292 U.S. adults to shed light on Americans’ understanding of basic health insurance terms and concepts, and to identify gaps in awareness that could lead to difficulties for some individuals as they choose new plans or use their health plans. If you want to test your own knowledge of health insurance terms and concepts before reading on, you can take the 10-question quiz online.

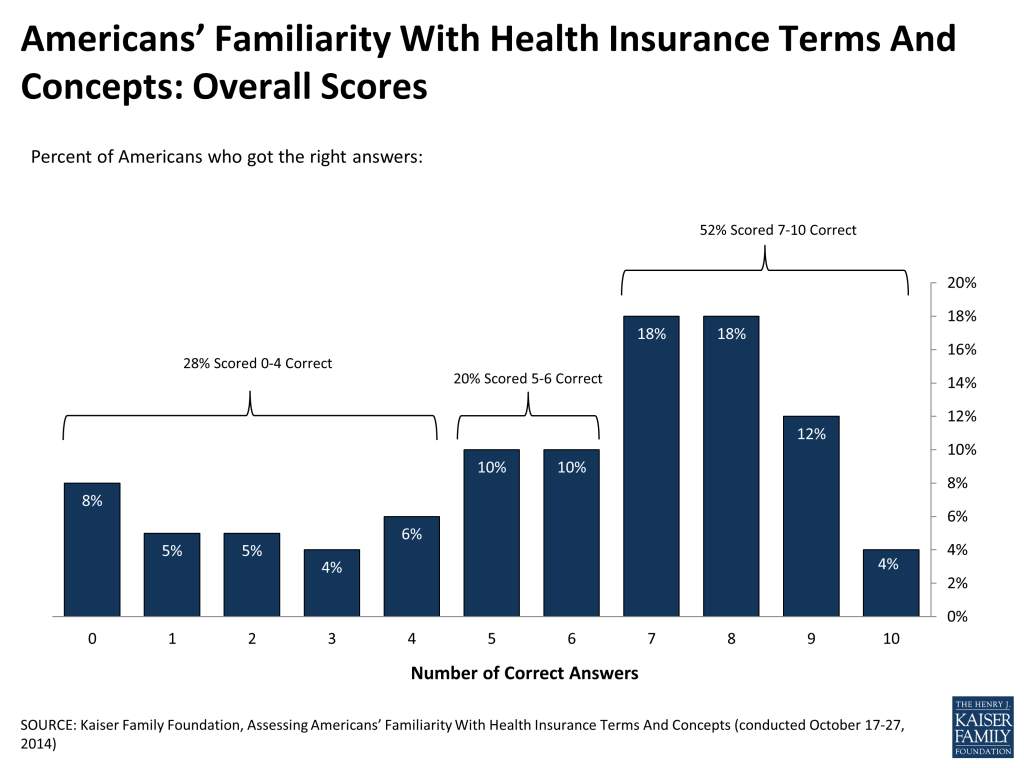

Overall Scores

When asked a series of questions about health insurance terms and concepts, including some that require calculating out-of-pocket costs, over half of the public (52 percent) scored an impressive grade of at least 7 out of 10 right answers, but only 4 percent answered all 10 questions correctly. On the other side of the spectrum, nearly three in ten (28 percent) gave correct answers to 4 or fewer questions, with 8 percent giving no correct answers at all.

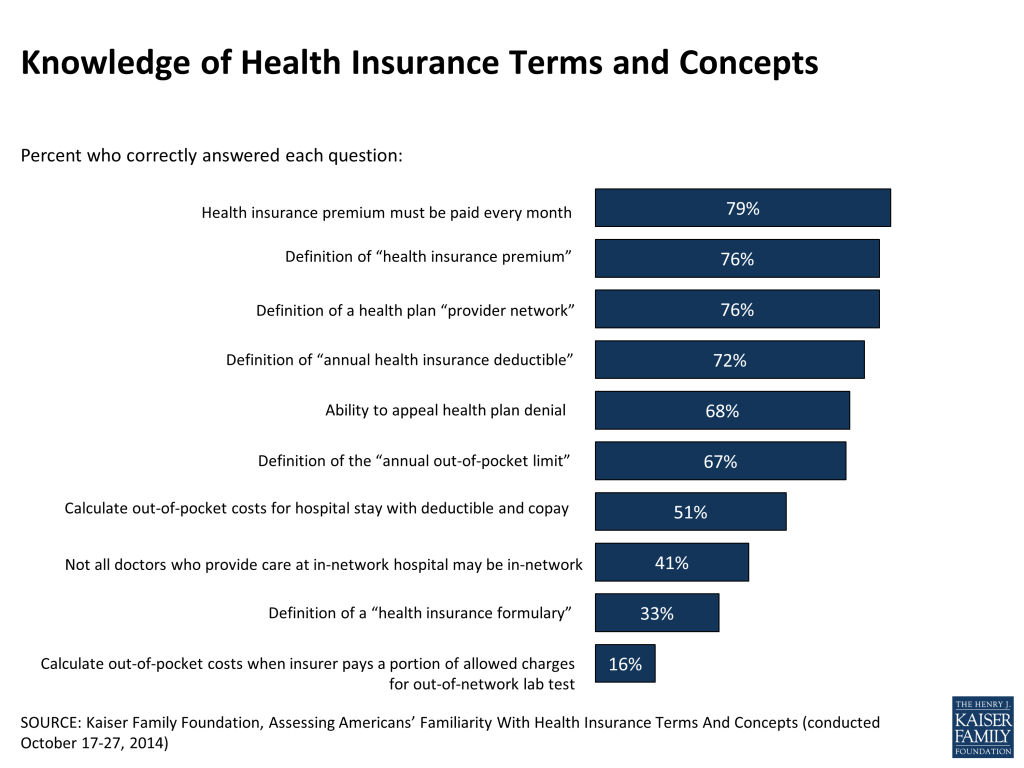

Of the 10 questions asked, 6 proved relatively easy for the public to answer, with at least two-thirds answering each correctly. About eight in ten (79 percent) responded correctly that a health insurance premium must be paid every month, as opposed to only in months when health care services are used. Large majorities were also able to correctly identify the definitions of insurance terms like premium (76 percent), provider network (76 percent), annual deductible (72 percent), and annual out-of-pocket limit (67 percent). Over two-thirds (68 percent) also know that if a health plan refuses to pay for a medically recommended service, an insured person has the right to appeal the plan’s decision.

Four other questions proved more difficult for people to answer. Two of these questions asked respondents to calculate the amount they would have to pay out of their own pocket in different care-use scenarios. Although these questions may seem to be testing math skills rather than health literacy, math skills are an important component in understanding the complicated maze of health insurance payments and billing. Just over half (51 percent) were correctly able to calculate how much they would have to pay for a 4-day hospital stay with a $1000 deductible and $250-per-day copay. Far fewer – only 16 percent – could correctly calculate how much they would have to pay for an out-of-network lab test when the insurer pays 60% of allowed charges.

Many Americans are also confused about the term “health insurance formulary,” with only a third (33 percent) identifying the correct definition (a list of prescription drugs covered by a health plan). Another 14 percent selected an incorrect definition of formulary, and over half (53 percent) said they didn’t know.

Another area where there are gaps in awareness has to do with care received from doctors during an in-network hospital stay. About four in ten (41 percent) are aware that doctors providing care at an in-network hospital may not necessarily be in-network providers themselves, while about three in ten incorrectly believe that all care received at an in-network hospital will be from in-network doctors and another three in ten say they don’t know (29 percent each).

| FIGURE 3: Awareness Among General Public Of Health Insurance Terms And Concepts | ||||

| CORRECT ANSWER | CORRECT | INCORRECT | ||

| WrongAnswer | Don’tKnow | |||

| How often you have to pay your health insurance premium | Must pay every month, regardless of whether you use services | 79% | 5% | 15% |

| Best definition of “health insurance premium” | Amount health insurance companies charge each month for coverage | 76% | 8% | 16% |

| Best description of a health plan “provider network” | The hospitals and doctors that contract with your health plan to provide services for an agreed-upon rate or fee schedule | 76% | 7% | 16% |

| Best definition of “annual health insurance deductible” | Amount of covered health expenses you must pay yourself each year before your insurance will begin to pay | 72% | 10% | 17% |

| If your health insurance plan refuses to pay for a service that you think is covered and your doctor says you need, you can appeal the denial and possibly get the insurance company to pay the claim. | True | 68% | 6% | 25% |

| Best description of the “annual out-of-pocket limit” | Most you will have to pay in deductibles, copays, and coinsurance for covered care received in network for the year | 67% | 12% | 18% |

| Calculation of out-of-pocket charges for a 4-day hospital stay with a total bill of $6,000 with a $1,000 deductible and $250 per day copay | $2,000 | 51% | 30% | 18% |

| If you receive inpatient care at a hospital that participates in your health plan’s provider network, all the doctors who care for you while you’re in the hospital will also be in network | False | 41% | 29% | 29% |

| Best description of a “health insurance formulary” | List of prescription drugs your health plan will cover | 33% | 14% | 53% |

| Calculation of out-of-pocket costs for an out-of-network lab test with a total bill of $100 when plan pays 60% of allowed charges and allowed charge is $20 | $88 | 16% | 62% | 20% |

| Note: Those who did not respond (1-2% for each question) were not included in this table. Question wording is abbreviated for some items. See topline for full question wording. | ||||

Where Are The Biggest Gaps In Awareness?

Some groups are more likely than others to demonstrate a better understanding of health insurance terms and concepts, while certain groups may be less familiar with health insurance. Those who scored lower on this health insurance literacy quiz include people with lower levels of education, younger Americans, and the uninsured. There was not a significant difference between the average scores of men and women.

| Figure 4:Health Insurance Awareness Scores by Gender, Age, Education, and Insurance Status | ||||

| Low Scorers (0-4 Correct) | Moderate Scorers (5-6 Correct) | High Scorers (7-10 Correct) | Mean Score | |

| Overall | 28% | 20% | 52% | 5.8 |

| Insurance Status | ||||

| Insured (ages 18-64) | 23 | 19 | 58 | 6.2 |

| Uninsured (age 18-64) | 47 | 26 | 27 | 4.4 |

| Age | ||||

| 18-29 | 43 | 20 | 36 | 4.7 |

| 30-49 | 31 | 18 | 51 | 5.7 |

| 50-64 | 20 | 20 | 61 | 6.4 |

| 65+ | 19 | 24 | 57 | 6.4 |

| Gender | ||||

| Male | 28 | 19 | 53 | 5.8 |

| Female | 29 | 21 | 50 | 5.8 |

| Education | ||||

| High school or less | 45 | 23 | 32 | 4.5 |

| Some college | 24 | 19 | 57 | 6.2 |

| College graduate | 10 | 16 | 74 | 7.2 |

Differences by Education:

Education has a strong correlation with health insurance literacy, with those who never attended college significantly less likely than those with college degrees to answer health insurance questions correctly. For instance, nearly all college graduates (93 percent) identified the correct definition of a health plan’s provider network, compared to 60 percent of those with high school education or less. Average overall scores range from 4.5 correct items for those who never attended college, to 6.1 among those with some college education, to 7.2 for college graduates.

Differences by Age:

The survey also sheds light on the information needs of younger Americans, who demonstrate a lower level of understanding of health insurance concepts than older Americans. For example, about four in ten (39 percent) of those ages 18-29 were able to correctly calculate the out-of-pocket cost for a hospital stay with a given copay and deductible, compared with over half of adults over age 30. A similar gap exists in understanding the nature of a health insurance premium. While 63 percent of younger adults correctly indicate that premiums must be paid every month – not only when health care services are used – this is at least 15 percentage points lower than among older age groups. On average, adults under age 30 answered 4.7 questions correctly, compared with scores of 5.7 for those ages 30-49, and 6.4 for those ages 50 and over.

Differences by Insurance Status:

Perhaps most importantly, given that open enrollment is around the corner, this survey uncovered a significant information gap among the uninsured, with substantial shares expressing a lack of familiarity with health insurance terms and concepts. Uninsured Americans under age 65 (who also tend to have fewer years of education) have lower average quiz scores than those with insurance (average 4.4 correct versus 6.2), and are more likely to answer zero questions correctly (13 percent versus 4 percent). For example, fewer of those ages 18-64 without health insurance correctly identified the definition of a health insurance premium (57 percent) compared to those with health insurance (83 percent). While some uninsured people provided incorrect answers, across the 10 questions asked, about a quarter or more of the uninsured selected “don’t know” rather than picking an answer.

| FIGURE 5: Awareness Among Uninsured Of Health Insurance Terms And Concepts | ||||

| Among those ages 18-64 who are uninsured: | CORRECT ANSWER | CORRECT | INCORRECT | |

| WrongAnswer | Don’tKnow | |||

| How often you have to pay your health insurance premium | Must pay every month, regardless of whether you use services | 64% | 6% | 28% |

| Best definition of “health insurance premium” | Amount health insurance companies charge each month for coverage | 57% | 8% | 35% |

| Best description of a health plan “provider network” | The hospitals and doctors that contract with your health plan to provide services for an agreed-upon rate or fee schedule | 57% | 16% | 26% |

| Best definition of “annual health insurance deductible” | Amount of covered health expenses you must pay yourself each year before your insurance will begin to pay | 53% | 20% | 27% |

| If your health insurance plan refuses to pay for a service that you think is covered and your doctor says you need, you can appeal the denial and possibly get the insurance company to pay the claim. | True | 53% | 12% | 33% |

| Best description of the “annual out-of-pocket limit” | Most you will have to pay in deductibles, copays, and coinsurance for covered care received in network for the year | 53% | 18% | 27% |

| Calculation of out-of-pocket charges for a 4-day hospital stay with a total bill of $6,000 with a $1,000 deductible and $250 per day copay | $2,000 | 39% | 34% | 27% |

| If you receive inpatient care at a hospital that participates in your health plan’s provider network, all the doctors who care for you while you’re in the hospital will also be in network | False | 29% | 32% | 37% |

| Best description of a “health insurance formulary” | List of prescription drugs your health plan will cover | 21% | 18% | 58% |

| Calculation of out-of-pocket costs for an out-of-network lab test with a total bill of $100 when plan pays 60% of allowed charges and allowed charge is $20 | $88 | 9% | 66% | 24% |

| Note: Those who did not respond (1-2% for each question) were not included in this table. Question wording is abbreviated for some items. See topline for full question wording | ||||

Implications

Most U.S. adults appear to have a pretty firm grasp on basic health insurance terms and how insurance works in general. Understanding is lower in some areas, however, including calculating out-of-pocket costs and knowing that an insured person might get care from an out-of-network doctor at an in-network hospital.

Younger adults, those who haven’t attended college and the uninsured score somewhat lower on these basic measures of health insurance literacy. As more people gain insurance under the ACA, these individuals may need extra help navigating their plans, particularly if they are becoming insured for the first time. Levels of health insurance literacy may rise as more people have access to, learn to navigate and use health insurance.

Assessing Americans' Familiarity With Health Insurance Terms And Concepts: Methodology

This Kaiser Family Foundation Survey, Assessing Americans’ Familiarity with Health Insurance Terms and Concepts, was designed and analyzed by researchers at the Kaiser Family Foundation (KFF), and was conducted October 17-27, 2014, among a nationally representative sample of 1,292 adults ages 18 and older, including an oversample of adults age 18-64 who have no health insurance. KFF paid for all costs associated with the survey. Interviews were conducted in English and Spanish using GfK’s KnowledgePanel, an online research panel. KnowledgePanel members are recruited through probability sampling methods and include both those with internet access and those without (KnowledgePanel provides internet access for those who do not have it and, if needed, a device to access the internet when they join the panel). A combination of random digit dialing (RDD) and address-based sampling (ABS) methodologies have been used to recruit panel members (in 2009 KnowledgePanel switched its sampling methodology for recruiting panel members from RDD to ABS). The panel comprises households with landlines and cellular phones, including those with only cell phones, and those without a phone. Both the RDD and ABS samples were provided by Marketing Systems Group (MSG). KnowledgePanel continually recruits new panel members throughout the year to offset panel attrition as people leave the panel.

The survey data were weighted to be representative of adults nationwide. Weighting took place in two stages. First, all members of the panel carry a weight designed to produce a nationally representative sample of the U.S. adult population based on gender, age, race/ethnicity, education, region, household income, home ownership status, metropolitan area, and Internet access. In the second stage, design weights were adjusted to account for the oversample and adjust for any differential survey non-response. An iterative procedure was used to adjust the final sample to match benchmarks from the March 2014 Supplement to the Census Bureau’s Current Population Survey (CPS) on age, gender, race/ethnicity, region, education, metropolitan area, household income, internet access, and primary language (English Dominant, Bilingual, Spanish Dominant, Non-Hispanic).1

Margins of sampling error and tests of statistical significance take into account the effect of weighting. The margin of sampling error including the design effect for the full sample of 1,292 adults is plus or minus 3 percentage points. Numbers of respondents and margin of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll.

| Group | N (unweighted) | M.O.S.E. | ||

| Total | 1,292 | ± 3 percentage points | ||

| Insurance Status | ||||

| Insured, age 18-64 | 794 | ± 4 percentage points | ||

| Uninsured, age 18-64 | 194 | ± 8 percentage points | ||

| Age | ||||

| 18-29 | 204 | ± 8 percentage points | ||

| 30-49 | 413 | ± 5 percentage points | ||

| 50-64 | 425 | ± 5 percentage points | ||

| 65+ | 250 | ± 7 percentage points | ||

| Gender | ||||

| Men | 650 | ± 4 percentage points | ||

| Women | 642 | ± 4 percentage points | ||

| Education | ||||

| High school grad or less | 549 | ± 5 percentage points | ||

| Some college | 349 | ± 5 percentage points | ||

| College grad or more | 394 | ± 5 percentage points | ||

Endnotes

- Details about KnowledgePanel sampling, recruitment, and weighting methodology, including details about how design weights are calculated, are available at http://www.knowledgenetworks.com/knpanel/docs/knowledgepanel(R)-design-summary-description.pdf ↩︎