Repayments and Refunds: Estimating the Effects of 2014 Premium Tax Credit Reconciliation

Issue Brief

In January 2014, the Affordable Care Act (ACA) began making federal premium tax credits available to eligible individuals who purchased health coverage through exchanges, or Marketplaces. These subsidies are a centerpiece of the law and are designed to provide financial assistance to millions of Americans who could not otherwise afford health coverage.

Taxpayers may claim a premium tax credit for themselves and other family members based on their income for the year. An individual or family may also elect to receive an advance premium tax credit (APTC) based on projected household income. Projected income may be based on previous income history and may be documented with the most recent available tax return or with other evidence of income. These advance credits are an estimate and must be reconciled based on actual income when people file their taxes. People who received an overpayment of the premium tax credit (for example, due to an unexpected increase in income midyear) have to repay some of or the entire amount overpaid when they file their taxes. Conversely, people who received an underpayment of the tax credit may get a refund when reconciling their advance payments with their actual annual income and subsidy eligibility.

There are several reasons that may cause people to need to reconcile their advance credits. The simplest is just that their income may change. Another is that there may be a change in the size of the family (e.g., birth, death, divorce), which affects the family’s income as a percent of poverty. People are encouraged to report these changes to the Marketplace so that their advance credit may be modified, but notification may not happen in all cases and even when midyear changes are reported, some reconciliation will likely occur when taxes are filed.

In this brief, we focus on reconciliation based only on income changes (prior year v. current year), and estimate that 50% of subsidy-eligible tax households would owe some repayment and 45% would receive a refund. Subsidy-eligible tax households with starting incomes under 200% of poverty would be somewhat more likely to owe a repayment (54%) and somewhat less likely to receive a refund (40%). (Throughout this brief we define “subsidy-eligible tax households” as those households containing any individual who would have been determined eligible for advance payment of the premium tax credit based on their starting incomes).

Among those projected to owe a repayment, the average repayment amounts would be $667 for taxpayers with starting incomes under 200% of poverty, $886 for taxpayers with starting incomes of 200-300% of poverty, and $1,380 for taxpayers with starting incomes of 300-400% of poverty. Among those projected to receive a refund, the average refund amounts would be $412 for taxpayers with starting incomes under 200% of poverty, $1,016 for taxpayers with starting incomes of 200-300% of poverty, and $1,601 for taxpayers with starting incomes of 300-400% of poverty. Overall, the estimated average repayment is $794 and the refund is $773.

Overview of Reconciliation of the Premium Tax Credit

The premium tax credit is a refundable tax credit available to U.S. citizens and legal immigrants with incomes in the range of 100-400% of the federal poverty level who are not eligible for other affordable coverage. Offered on a sliding scale based on income, the premium tax credit limits what people will be required to pay for a benchmark health plan to a percentage of their income (ranging in 2014 from 2% to 9.5% of income).

The law allows eligible enrollees to take the premium tax credit in the form of an advance payment because low- and moderate-income people generally would not be able to afford the coverage without upfront assistance. When enrollees choose the advance payment option, their tax credits are paid directly to the insurer they select. Enrollees then pay the remaining share of the monthly premium to the insurer (and out-of-pocket costs if they use health care).

The amount of the premium tax credit a family ultimately receives, though, is based on their annual household income as reported on their tax return. For those who choose to wait and claim the entire credit when they file their taxes the following year, the credit will be applied against any taxes they owe or will be sent as a refund to those who do not owe any taxes. For people who choose advance payments the process is different. Because their coming year’s annual income will not be known at the time they apply for advance payment of the tax credit, eligibility for advance payment is based on an estimate of income for the year and may be verified using their most recent tax return or, if current income is different, pay stubs or other documentation.

People applying early in open enrollment for advance payments beginning in January 2014, therefore, would have likely had their incomes verified by their 2012 tax returns (as this was the most recent tax return they would have had). Unless applicants actively accounted for changes between 2012 and current income, their subsidies may have been based on an already out-of-date income. People applying toward the end of 2014 open enrollment may have been more likely to use 2013 income in their applications, particularly if they had filed their 2013 taxes before applying, but they still may have experienced changes in income during 2014.

As shown below, household incomes change, sometimes significantly, over the course of a year. Enrollees are expected to contact the Marketplace when they experience changes in their incomes so that their subsidies can be recalculated, but there is as of yet no indication of how often this contact is made.

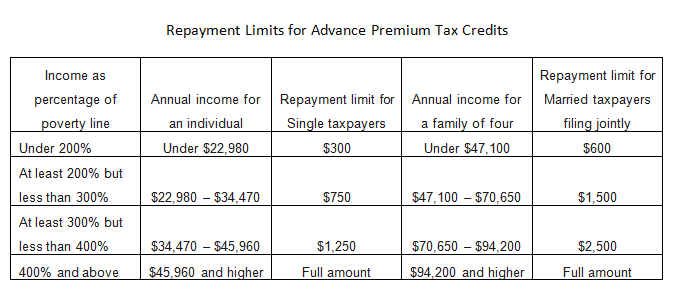

The law requires that any advance payments received in a year be reconciled against the tax credits for which individuals and families are eligible based on their annual income reported on their tax return. If the advance payment exceeded the amount of the credit for which individuals were ultimately eligible, a portion of the overpayment must be repaid. While the ACA originally limited the amount that had to be repaid to $250 for an individual and $400 for a family, Congress subsequently raised the repayment caps and created a scaled repayment structure, as shown in the table below.

| Figure 1: Limits on Repayments For Advanced Payment of the Premium Tax Credit | ||

| Annual 2014 Income (as a % of 2013 FPL) | Maximum repayment amount for a single individual | Maximum repayment amount for couples and families |

| 100% to <200% | $300 | $600 |

| 200% to <300% | $750 | $1,500 |

| 300% to 400% | $1,250 | $2,500 |

| Greater than 400% FPL | Full amount | Full amount |

| Note: Enrollees with incomes that fall below poverty at the time of reconciliation are not expected to repay the tax credit.Source: 2012-24 Internal Revenue Bulletin, § 1.36B–4. | ||

Households that end up having an annual income within the subsidy range (100-400% of poverty) will have caps on their repayment amounts. Those whose incomes rise above the subsidy range (over 400% of poverty) have no limit on repayment and therefore may be subject to sizeable repayments when they file their taxes. Some households may have a decrease in income during the year that puts them below the subsidy range. In this case, though, the person or family would not be subject to a repayment and may even receive a refund.

For example, a single 40-year-old living in Atlanta, GA with a starting income of $17,000 (148% of 2013 FPL) may have qualified for advance payments totaling $2,614 for 2014. If the enrollee’s annual 2014 income increased to $23,000 (200% of 2013 FPL), she ultimately would qualify for $1,824 in premium assistance. Assuming she did not notify the Marketplace of her income change, she would owe a repayment of $750 (because $2,614 minus $1,824 equals $790, which exceeds her repayment cap of $750). If her annual 2014 income rose even higher to $46,000 (which is above 400% of 2013 FPL), she would no longer be eligible for assistance and would be required to repay the entire $2,614 she received in advance payments.

Some Marketplace shoppers were eligible for two types of assistance: the premium tax credit described above and a second form of assistance called cost sharing reductions, which limit out-of-pocket costs for the lowest income enrollees. The cost sharing reductions are not subject to reconciliation.

Estimates of Repayments and Refunds

We use the Survey of Income and Program Participation to model the subsidy-eligible population at the start of 2014 and to track income changes over time among this group in order to estimate how many would face repayment or receive refunds this tax season and the amounts of their repayments or refunds. We focus on the cohort of households that were subsidy eligible at the beginning of the year and follow them through the year. Eligible people are assumed to retain Marketplace coverage unless they obtain public coverage or they obtain or become eligible for employer-sponsored coverage. Because we are looking at changes in income, we exclude tax households with changes in household size – such as a birth, death, or marriage – during the year.

We made several assumptions in this model, which are described in more detail in the methods section. Most notably, we assume that everyone who was eligible for a premium tax credit opted for advanced payment in the full amount; that they all received the maximum potential subsidy in the year; and that they did not report changes in income during the year or receive an adjustment to their tax credit midyear. We assume that people who obtain other coverage inform the Marketplace and stop receiving subsidies at that time.

Although this analysis models tax households containing individuals who would have been potentially eligible to enroll with an advance payment of the tax credit, the income distribution of the households in our model is similar to that of actual Marketplace enrollees in HealthCare.gov states, according to data published by HHS.1

We use 2013 annual income in this analysis, which we call “starting income,” to determine eligibility for advance premium tax credits, and 2014 annual income as the basis for determining final tax credit eligibility. We recognize that some families may have to use their income tax return from two years earlier (their most recent available return) to verify income at the time of application, while others would provide documentation of their current income. In the appendix, we also provide results for two other scenarios: 2012 annual income (which addresses those who applied early in open enrollment and by default used their 2012 income tax return to verify their incomes); and March 2014 income (which captures those who signed up toward the end of open enrollment and used their current monthly incomes in their application).

Throughout this brief, we provide estimates by starting income (i.e. 2013 annual income) shown in poverty ranges. Under the ACA, eligibility for advance and final premium tax credits for 2014 is based on 2013 poverty levels2 , which range from $11,490 (100% FPL) to $45,960 (400% FPL) for a single individual; the 2014 subsidy eligibility range for a family of four was $23,550 to $94,200.

Estimates of 2014 Tax Households Owing Repayment or Receiving Refund

Incomes can change quite a bit over a year, and because premium tax credits vary continuously with income, these changes mean that most subsidized households will have a repayment or refund. Ninety-five percent of tax households experience a change in income over the year, with 49% experiencing an increase of decrease of more than 20% (Figure 2).

| Figure 2: Estimated Annual Income Volatility from 2013 to 2014 among tax households eligible to receive advance payments of tax credit | |||||

| Annual 2013 Income (%FPL) | Percent of tax households experiencing a change in annual income from 2013 to 2014 | ||||

| Decrease of 20% or more | Decrease of less than 20% | No Change | Increase of less than 20% | Increase of 20% or more | |

| 100% to <200% | 22% | 18% | 6% | 25% | 29% |

| 200% to <300% | 25% | 24% | 4% | 26% | 21% |

| 300% to 400% | 25% | 26% | 3% | 24% | 21% |

| All (100-400%) | 23% | 21% | 5% | 25% | 26% |

| Note: Households with a change in the tax filing unit size (e.g. due to birth, death, divorce) are not included in this analysis.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | |||||

Due to these midyear changes in income, one-half (50%) of tax households who were eligible to receive advance payments of the tax credit in 2014 would face a repayment of some or all of the tax credit and 45% would receive a refund. Relative to the other starting income groups, those households with starting incomes below 200% percent of poverty would be more likely to have a repayment (54% v. 46%).

These findings are similar to reports from tax preparers Jackson Hewitt and H&R Block of the experiences of early tax households, which respectively have reported that 53% and 52% of their early filing clients have been required to issue a repayment.3

How Many People Could be Subject to Reconciliation?

There is no definitive data yet on the number of people who received premium tax credits during 2014 and will be required to reconcile those tax credits based on actual income on their tax returns.

As of the end of open enrollment for 2014, 6.7 million people selected a plan and qualified for premium tax credits through a state or the federal Marketplace. That figure may be over-stated because not all of those people paid their premiums and actually ended up receiving advance tax credits, though it may also be under-stated because additional people qualifying for special enrollment periods signed up throughout the year. The Treasury Department has estimated that three to five percent of all taxpayers received advance premium tax credits in 2014. Based on an estimated 150 million returns filed, that would translate to 4.5 to 7.5 million tax households receiving advance payments of the premium tax credit in 2014 (with some households including more than one person).

The current number of people signed up and qualifying for subsidized coverage for 2015 is just under 10 million, and the Congressional Budget Office (CBO) projects that 18 million people will receive subsidies through the Marketplace on average each month by 2017.

Amounts of Repayments and Refunds

Repayment and refund amounts will depend on how much income changes during the year. As shown in Figure 1 above, tax households with annual income below 400% of poverty may have their repayments capped while those with higher incomes would be required to repay the entire advance credit amount.

Average repayment and refund amounts are shown in Figure 3. Among tax households who would owe a repayment, the average repayment amounts are $667 for those with starting incomes below 200% of poverty, $886 for those with starting incomes of 200-300% of poverty, and $1,380 for those with starting incomes of 300-400% of poverty. Among tax households who would receive a refund, the average refund amounts are $412 for those with starting incomes below 200% of poverty, $1,016 for those with staring incomes of 200-300% of poverty, and $1,601 for those with starting incomes of 300-400% of poverty.

For the 2014 benefit year, 100% of poverty was $11,490 for a single individual and $23,550 for a family of four; 400% of poverty was $45,960 for a single individual and $94,200 for a family of four.

| Figure 3: Estimated Average Amount of Repayment or Refundamong tax households owing repayment or receiving a refund | ||

| Annual 2013 Income (%FPL) | Average Repayment | Average Refund |

| 100% to <200% | $667 | $412 |

| 200% to <300% | $886 | $1,016 |

| 300% to 400% | $1,380 | $1,601 |

| All (100-400%) | $794 | $773 |

| Note: Repayment and refund amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | ||

The amounts of repayments and refunds vary with income change, which means that there is considerable variation around these average amounts. For example, among tax households who would owe a repayment, 15% would repay less than $50 and 18% would repay between $50 and $200 (Figure 4). At the other end of the distribution, seven percent of tax households owing a repayment would owe between $2,000 and $5,000, and two percent would owe $5,000 or more. Refund amounts show a similarly wide distribution.

| Figure 4: Estimated Percent of Subsidy-Eligible Tax Households Owing Repayment or Receiving a Refund, by Amount of Adjustmentamong tax households projected to owe repayment or receive refund | ||

| Reconciliation Adjustment | Repayment | Refund |

| Less than $50 | 15% | 14% |

| $50 to <$200 | 18% | 19% |

| $200 to <$500 | 22% | 22% |

| $500 to <$1000 | 24% | 20% |

| $1000 to <$2000 | 12% | 16% |

| $2000 to <$5000 | 7% | 9% |

| More than $5000 | 2% | 1% |

| Note: Repayment and refund amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | ||

Looking more closely at those who would be required to make a repayment, the average repayment amounts are significantly influenced by repayments for households whose final incomes exceeded 400% of poverty and who would therefore be required to repay their entire advance credit without any cap on repayment.

| Figure 5: Estimated Average Repayments Amounts, by Starting and Final Incomeamong tax households owing repayment | |||

| Annual 2013 Income (%FPL) | Percent of households with annual 2014 incomes that exceed 400% FPL | Average repayment among households with annual 2014 incomes that exceed 400% FPL | Average repayment among households with annual 2014 incomes that do not exceed 400% FPL |

| 100% to <200% | 6% | $3,837 | $472 |

| 200% to <300% | 15% | $2,610 | $577 |

| 300% to 400% | 57% | $2,306 | $157 |

| Note: Repayment and refund amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | |||

Figure 5 shows average repayment amounts for these households and for the other repaying households whose final incomes remain below 400% of poverty. While the share of repaying households with final incomes exceeding 400% of poverty are relatively small, particularly among households with starting incomes below 300% of poverty, their average repayment amounts would be quite high: $3,837 for those with starting incomes below 200% of poverty; $2,610 for those with starting incomes at 200-300% of poverty; and, $2,306 for those with staring incomes at 300-400% of poverty.

Another way to look at the amounts that households would repay or receive is to look at the difference between the total premium credit amounts that ultimately would be paid to people (i.e., post reconciliation) and the advance credit amounts (which are what people qualify for based on their starting income). While final tax credits that people ultimately receive after reconciliation are very close on average to the advance credit amounts, these overall numbers mask substantial differences across households that would be required to make a repayment and those that would receive a refund.

Repaying households would return 27% of their advance credits, with households with starting incomes below 200% of poverty repaying 20% of the advance credit amounts, households with starting income at 200-300% of poverty repaying 36% of the advance tax credits, and households with starting incomes at 300-400% of poverty repaying 65% of the advance tax credits. The large percentage for the higher-income group occurs because 57% of households owing repayments who started out with incomes between 300-400% of poverty end the year with income of 400% of poverty or more and would be required to repay the entire advance amount.

The refund amounts for tax households eligible to receive them would average 29% of the advance credit amounts, with households with starting incomes below 200% of poverty receiving an additional 13% on average, households with starting income at 200-300% of poverty receiving an additional 45% on average, and households with starting incomes at 300-400% of poverty receiving an additional 87% on average. The relatively large percentage for the higher income group reflects the relatively low advance credit amounts that some of these households initially qualified for.

| Figure 6: Estimated Repayment or Refund as a Share of Tax Credit Advance Payments | |||

| Annual 2013 Income (%FPL) | Among tax households projected to owe repayment or receive refund | Among all tax households that received an advance payment | |

| Average percentage of advance payment repaid | Average percentage received in excess of advance payment | Average adjustment to advance payment | |

| 100% to <200% | -20% | +13% | -6% |

| 200% to <300% | -36% | +45% | +4% |

| 300% to 400% | -65% | +87% | +12% |

| All (100-400%) | -27% | +29% | +2% |

| Note: Repayment and refund amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | |||

Discussion

Whether applicants use their prior year’s income or more current income when applying for the advance payments, it is likely that their estimated incomes will be different from what is ultimately reported on the tax return at the end of the year. Many people’s income fluctuates throughout the year: the income of hourly workers can change as the number of hours worked varies, and even salaried workers with more stable earnings can receive bonus payments that increase their income. Changes in circumstances, such as job loss or job gain can also alter income from what may have been used to determine the advance payments.

Reconciliation of premium subsidies under the ACA is a natural outgrowth of using the tax system to provide those subsidies. Income taxes – and the various credits and deductions that affect them – are generally based on actual annual income, which can only be known after the fact. Taxes that are withheld from paychecks or paid on an estimated basis by self-employed people are always reconciled on the tax return in the following year. In this respect, the ACA’s premium subsidies are no different.

However, the reconciliation of premium subsidies poses some particular challenges. The subsidies primarily go to lower-income households with very little discretionary income. An unanticipated repayment – which may require tax households to actually write a check to the IRS or get a lower-than-expected tax refund – may be difficult for these household to handle financially, even though it would only happen if their income is higher than originally estimated. Also, the premium tax credits are designed to make health insurance more affordable and encourage people who are uninsured to get covered. To the extent people are uncertain about how much of a subsidy they will ultimately qualify for, they may be more hesitant to sign up for insurance.

Repayments can be minimized – though not necessarily avoided entirely – if people promptly report any changes in income and household composition. In the first year, many people did not even realize they were receiving subsidies. State and federal marketplaces, as well as brokers and navigators, can play an important role in helping people to understand the subsidy reconciliation process and encouraging them to report any changes throughout the year. Over time, this reporting may improve as subsidy beneficiaries become more familiar with the process.

Appendix

2012 Annual Income Scenario

This scenario addresses people who applied early in open enrollment and by default used their 2012 income tax return to verify their incomes at the time of application.

| Estimates of Premium Tax Credit Repayments and Refunds for 2014 Benefit Year | ||||

| Among tax households who defaulted to using 2012 annual income at time of application for 2014 tax credit | Annual 2012 Income (As a % of 2013 FPL) | |||

| 100% to <200% | 200% to <300% | 300% to 400% | All (100 – 400%) | |

| Estimated percent of 2014 subsidy-eligible tax households experiencing a change in income by end of 2014 | ||||

| Decrease of 20% or more | 25% | 36% | 30% | 29% |

| Decrease of less than 20% | 16% | 18% | 22% | 17% |

| Increase of 20% or more | 35% | 24% | 29% | 31% |

| Increase of less than 20% | 19% | 20% | 17% | 19% |

| No Change | 5% | 2% | 2% | 4% |

| Estimated percent of 2014 subsidy-eligible tax households with a repayment or refund of premium tax credit | ||||

| Required to repay some or all of tax credit | 54% | 44% | 46% | 50% |

| Receive a refund for remaining tax credit | 41% | 55% | 52% | 47% |

| No adjustment | 5% | 2% | 2% | 4% |

| Estimated amount of repayment or refund, among tax households projected to owe repayment or receive a refund | ||||

| Average repayment | $899 | $1,105 | $1,681 | $1,048 |

| Average refund | $483 | $1,322 | $1,535 | $963 |

| Estimated repayment or refund as a share of tax credit advance payments, among tax households projected to owe repayment or receive refund | ||||

| Repayment: Average percentage of advance payment repaid | -25% | -41% | -81% | -34% |

| Refund: Average percentage received in excess of advance payment | +15% | +54% | +83% | +35% |

| Notes: Households with a change in the tax filing unit size (e.g. due to birth, death, divorce) are not included in this analysis. Repayment amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | ||||

2013 Annual Income Scenario

This scenario captures people who applied early in open enrollment and used their 2013 income, verified through pay stubs or other documentation.

| Estimates of Premium Tax Credit Repayments and Refunds for 2014 Benefit Year | ||||

| Among tax households who used their 2013 income for 2014 tax credit | Annual 2013 Income (As a % of 2013 FPL) | |||

| 100% to <200% | 200% to <300% | 300% to 400% | All (100 – 400%) | |

| Estimated percent of 2014 subsidy-eligible tax households experiencing a change in income by end of 2014 | ||||

| Decrease of 20% or more | 22% | 25% | 25% | 23% |

| Decrease of less than 20% | 18% | 24% | 26% | 21% |

| Increase of 20% or more | 29% | 21% | 21% | 26% |

| Increase of less than 20% | 25% | 25% | 24% | 25% |

| No Change | 6% | 4% | 3% | 5% |

| Estimated percent of 2014 subsidy-eligible tax households with a repayment or refund of premium tax credit | ||||

| Required to repay some or all of tax credit | 54% | 46% | 44% | 50% |

| Receive a refund for remaining tax credit | 40% | 50% | 53% | 45% |

| No adjustment | 6% | 4% | 3% | 5% |

| Estimated amount of repayment or refund, among tax households projected to owe repayment or receive a refund | ||||

| Average repayment | $667 | $886 | $1,380 | $794 |

| Average refund | $412 | $1,016 | $1,601 | $773 |

| Estimated repayment or refund as a share of tax credit advance payments, among tax households projected to owe repayment or receive refund | ||||

| Repayment: Average percentage of advance payment repaid | -20% | -36% | -65% | -27% |

| Refund: Average percentage received in excess of advance payment | +13% | +45% | +87% | +29% |

| Notes: Households with a change in the tax filing unit size (e.g. due to birth, death, divorce) are not included in this analysis. Repayment amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | ||||

March, 2014 Income Scenario

This scenario captures people who signed up toward the end of open enrollment and used their current (March, 2014) income in their application.

| Estimates of Premium Tax Credit Repayments and Refunds for 2014 Benefit Year | ||||

| Among tax households who used March, 2014 income at time of application for 2014 tax credit | Annualized March 2014 Income (As a % of 2013 FPL) | |||

| 100% to <200% | 200% to <300% | 300% to 400% | All (100 – 400%) | |

| Estimated percent of 2014 subsidy-eligible tax households experiencing a change in income by end of 2014 | ||||

| Decrease of 20% or more | 16% | 20% | 23% | 18% |

| Decrease of less than 20% | 29% | 29% | 30% | 29% |

| Increase of 20% or more | 14% | 15% | 8% | 14% |

| Increase of less than 20% | 26% | 23% | 27% | 25% |

| No Change | 15% | 13% | 12% | 14% |

| Estimated percent of 2014 subsidy-eligible tax households with a repayment or refund of premium tax credit | ||||

| Required to repay some or all of tax credit | 40% | 38% | 35% | 39% |

| Receive a refund for remaining tax credit | 45% | 50% | 53% | 47% |

| No adjustment | 15% | 12% | 12% | 14% |

| Estimated amount of repayment or refund, among tax households projected to owe repayment or receive a refund | ||||

| Average repayment | $487 | $692 | $792 | $585 |

| Average refund | $306 | $835 | $1,179 | $598 |

| Estimated repayment or refund as a share of tax credit advance payments, among tax households projected to owe repayment or receive refund | ||||

| Repayment: Average percentage of advance payment repaid | -15% | -28% | -35% | -20% |

| Refund: Average percentage received in excess of advance payment | +10% | +31% | +58% | +21% |

| Notes: Households with a change in the tax filing unit size (e.g. due to birth, death, divorce) are not included in this analysis. Repayment amounts are estimated per tax household, and therefore represent the amount per tax-filing unit (household); not per person or per enrollee.Source: Kaiser Family Foundation analysis of 2008 Survey of Income and Program Participation (SIPP) panel data. | ||||

Methods

We applied our Current Population Survey (CPS) modeling work to the Survey of Income and Program Participation (SIPP) 2008 Panel to estimate the experience of tax claimants over two full calendar years. We computed each individual’s health insurance coverage, Medicaid and advance premium tax credit (APTC) poverty level, and eligibility category under the ACA (Medicaid-eligible, subsidy-eligible, coverage gap, etc.) following the methods discussed in depth in the appendices of our state estimates of the coverage gap and subsidy-eligible individuals.

The income, employment, and health insurance sections of the CPS and SIPP questionnaires include many of the same questions. Implementing our CPS algorithm in SIPP produces similar calendar year-weighted estimates of both insurance coverage and ACA eligibility. CPS produces reliable estimates at the state-level at a single point in time while SIPP follows a cohort of individuals and families on a monthly basis over a period of four years, making SIPP the preferred microdata for estimating the dynamics of income and ACA eligibility.

We assessed tax claimants’ ability to predict their final 2014 annual income in late 2013 by shifting survey responses forward by two calendar years. The current SIPP 2008 Panel includes a four-year, person-weighted sample of about 45,000 individuals over the 48-month period of 2009 to 2012. Respondents’ annualized income and health insurance coverage status at the end of 2011 served as the point of initial enrollment (displayed throughout the text as 2013) and annual income collected during survey year 2012 provided amounts for the final tax reconciliation (displayed as 2014). Both values were inflated with the Bureau of Labor Statistics factor from 2012 to 2014 when compared to 2014 premiums.

To accommodate the added dimension of time in SIPP, we imputed documentation status only at the beginning of the panel but imputed an offer of employer-sponsored insurance (ESI) for each unique job over the period. Otherwise, both of these techniques mirrored the strategy outlined in the immigration status and offer imputation appendices of our prior work.

This analysis estimates the reconciliation experience of tax filers who were either eligible for an APTC themselves or who claimed a dependent eligible for APTC based on filing unit 2013 Modified Adjusted Gross Income (MAGI). Additionally, that subsidy-eligible individual must have been a part of the potential marketplace population in January of 2014. To create a tax filing unit weight, person-weights for single filers and heads of household were maintained, married couples’ person-weights were each divided by two, and all tax dependents’ weights were zeroed out. This resulted in a starting population of approximately 11 million tax households based on an unweighted sample of 1,918 records. Approximately ten percent of claimants experienced a change in tax filing unit structure at some point during the reconciliation year (2014) due to birth, death, marriage, divorce, or income or residence changes of a dependent relative. Since a change in family size (and with it, monthly marketplace premiums) might precipitate the APTC recipient to report any revised income, these units were excluded from the analysis.

Starting in January 2014, we determined each individual’s monthly premium based on actual reported monthly insurance coverage. All individuals without insurance, or with nongroup, unknown private coverage, or dependent ESI who also did not have access to an imputed offer of ESI for the month were designated as a marketplace enrollee for that month in need of coverage. Their premiums were summed alongside others in their tax filing unit, and then capped according to their tax filing unit’s subsidy-eligibility from the point of application (2013 annual income) for a single pro-rated month. After computing all twelve months of potential marketplace subsidies, this process was repeated using the tax filing unit’s subsidy-eligibility from the point of reconciliation (2014 annual income). After capping based on current-law repayment limits, the difference between these two APTC amounts provided our final estimates of required repayments, overpayments, and net adjustments shown.

{kind=link}

Endnotes

- We estimate that 61% of subsidy-eligible tax households in the 37 Healthcare.gov states had starting incomes between 100-200% of poverty; 31% were between 200-300% of poverty, and 8% were between 300-400% of poverty. HHS reported that 65% of enrollees had starting incomes between 100-200% of poverty; 23% were between 200-300% of poverty, and 8% were between 300-400% of poverty. ↩︎

- Refers to the federal poverty guideline in the 48 contiguous states; note that Alaska and Hawaii follow different poverty guidelines. ↩︎

- We estimate that the average repayment amount would be $794 and the refund would be $773, while H&R Block has reported average repayments of $530 and average premium tax credit refunds of $365 among its early filers, as of February 2015. These differences could be explained by timing (as the distribution of clients filing early returns may differ from overall subsidy-eligible filers) as well as possible differences between the income distribution of H&R Block clients and that of our model. Additionally, in the 2013 income scenario of our model, we assume that eligible household members are enrolled for the entire year (unless they became eligible for other coverage), but most enrollees signed up later in open enrollment, meaning that they were not covered through the Marketplace for the entire year. Finally, our model assumes that no tax households notified the exchange of mid-year income changes, but in reality some enrollees likely would have notified the exchange of income changes and therefore faced smaller repayments at the time of reconciliation. ↩︎