Analysis of 2016 Premium Changes and Insurer Participation in the Affordable Care Act’s Health Insurance Marketplaces

An updated analysis of 2016 premiums in Affordable Care Act marketplaces is available here.

An updated analysis of insurer participation in 2016 Affordable Care Act marketplaces is available here.

INTRODUCTION

Premium growth in the Affordable Care Act’s Health Insurance Marketplaces has been an area of significant interest, as this is one of the most tangible and measurable indicators of whether the ACA is working to keep health insurance affordable. The ACA’s rate review provision requires premium increases over ten percent to be made public. As a number of individual market insurers are requesting 2016 increases well above 10 percent, concern has been raised over the affordability of premiums in the coming year. However, these increases are not necessarily representative of the range of products from which consumers will be able to choose, and similar data is not widely available for the plans with moderate increases or decreases.

This brief presents an early analysis of changes in the premiums for the lowest- and second-lowest cost silver marketplace plans in major cities in 10 states plus the District of Columbia, where we were able to find complete data on rates for all insurers. It follows a similar approach to our September 2013 and 2014 analyses of Marketplace premiums.

In most of these 11 major cities, we find that the costs for the lowest and second-lowest cost silver plans – where the bulk of enrollees tend to migrate – are changing relatively modestly in 2016, although increases are generally bigger than in 2015. The cost of a benchmark silver plan in these cities is on average 4.4% higher in 2016 than in 2015. These premiums are still preliminary in some cases and could be raised or lowered through these states’ rate review processes, and it is difficult to generalize to all states based on this small sample of states where all rate filings are available. We also find that the number of insurers participating has stayed the same or increased in 9 states, while insurer participation decreased in Michigan and the District of Columbia.

Approach

In preparation for open enrollment for coverage in 2016, insurers filed premiums with state insurance departments. States vary in whether and when they release those filings. Our analysis is based on the 10 states plus the District of Columbia where we were able to find comprehensive filings or other information about the rates of the lowest-cost plans. Other states have released summary information, but not sufficient detail to identify the lowest-cost silver plans. In many cases, premiums are still under review by insurance departments and may change prior to the start of open enrollment.

We examine premiums in the rating area that includes a major city in each state. Premiums vary significantly within states, with the rating area being the smallest geographic unit by which insurers are allowed to vary rates. For each rating area, we look at premiums for the two lowest-cost silver plans. We focus on silver plans because they are the basis for federal premium subsidies and because these are the plans that most marketplace enrollees (68%) have chosen.

Changes in Lowest Two Silver Plans

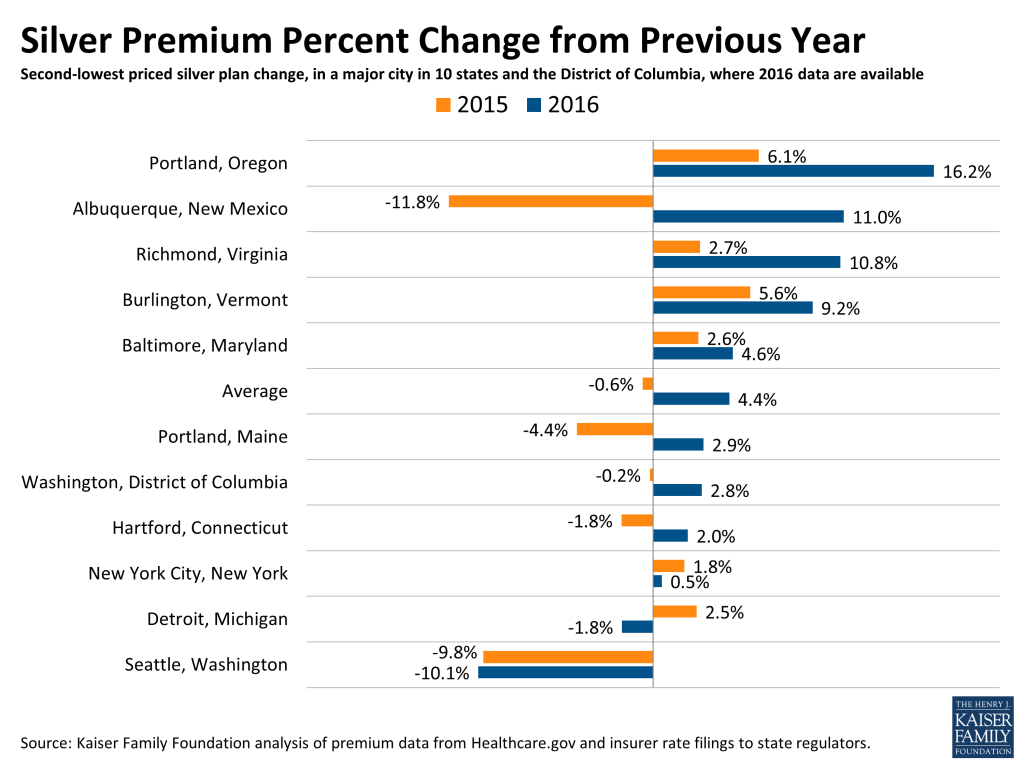

Across the 11 cities we examined, the premium for the second-lowest-cost silver plan in the Marketplace – before accounting for any tax credit – is increasing by an average of 4.4%. By contrast, in these cities, the average change in the benchmark silver plan was -0.6% from 2014 to 2015. (The nationwide average increase in this plan was 2% from 2014 to 2015).

Benchmark premium changes in 2016 vary significantly across the cities, ranging from a decrease of 10.1% in Seattle, Washington to an increase of 16.2% in Portland, Oregon.

| Table 1: Monthly Benchmark Silver Premiums for a 40 Year Old Non-Smoker Making $30,000 / Year | |||||||

| State | Rating Area(Major City) | 2nd Lowest Cost Silver Before Tax Credit | 2nd Lowest Cost Silver After Tax Credit | ||||

| 2015 | 2016 | % Change from 2015 | 2015 | 2016 | % Change from 2015 | ||

| Connecticut | 2 (Hartford) | $322 | $328 | 2.0% | $208 | $208 | 0.2% |

| DC | 1 (Washington) | $242 | $248 | 2.8% | $208 | $208 | 0.2% |

| Maine | 1 (Portland) | $282 | $290 | 2.9% | $208 | $208 | 0.2% |

| Maryland | 1 (Baltimore) | $235 | $246 | 4.6% | $208 | $208 | 0.2% |

| Michigan | 1 (Detroit) | $230 | $226 | -1.8% | $208 | $208 | 0.2% |

| New Mexico | 1 (Albuquerque) | $171 | $190 | 11.0% | $171* | $190* | 11.0%* |

| New York | 4 (New York City) | $372 | $374 | 0.5% | $208 | $208 | 0.2% |

| Oregon | 1 (Portland) | $213 | $248 | 16.2% | $208 | $208 | 0.2% |

| Vermont | 1 (Burlington) | $436 | $476 | 9.2% | $208 | $208 | 0.2% |

| Virginia | 7 (Richmond) | $260 | $288 | 10.8% | $208 | $208 | 0.2% |

| Washington | 1 (Seattle) | $254 | $228 | -10.1% | $208 | $208 | 0.2% |

| Average % change from 2015 | 4.4% | 1.2% | |||||

| SOURCE: Kaiser Family Foundation analysis of 2016 insurer rate filings to state regulators.NOTES: Rates are not yet final and subject to review by the state. Oregon rates reflect preliminary changes from the state. *Unsubsidized Albuquerque premiums are so low that a 40 year old making $30,000 per year would not qualify for a premium tax credit in 2016 | |||||||

As shown in the final column of the above table, the amount paid by an enrollee after accounting for the premium tax credit will depend on his or her income and family size. In 2015, a 40-year-old single enrollee making $30,000 per year would have paid $208 per month in most areas of the country, and a similar person would pay approximately the same in 2015. (Although premium caps are increasing for 2016, the poverty guidelines are also changing such that a single person making $30,000 will be at a slightly lower percent of poverty than he or she would be this year. These two changes in effect cancel each other out, leaving monthly payments for the benchmark plan very similar from year-to-year.)

Similar patterns can be seen for the lowest-cost silver plan in each city. On average, the premium for the lowest-cost-silver plan in these cities is increasing by 4.5% from 2015 to 2016, ranging from a decrease of 4.2% in Seattle, Washington to an increase of 19.0% in Richmond, Virginia.

| Table 2: Monthly Lowest-Cost Silver Premiums for a 40 Year Old Non-Smoker Making $30,000 / Year | |||||||

| State | Rating Area(Major City) | Lowest Cost Silver Before Tax Credit | Lowest Cost Silver After Tax Credit | ||||

| 2015 | 2016 | % Change from 2015 | 2015 | 2016 | % Change from 2015 | ||

| Connecticut | 2 (Hartford) | $321 | $327 | 1.9% | $207 | $207 | 0.1% |

| DC | 1 (Washington) | $239 | $244 | 2.1% | $205 | $204 | -0.6% |

| Maine | 1 (Portland) | $275 | $284 | 3.4% | $201 | $202 | 0.7% |

| Maryland | 1 (Baltimore) | $226 | $232 | 2.6% | $199 | $194 | -2.2% |

| Michigan | 1 (Detroit) | $219 | $210 | -4.2% | $197 | $192 | -2.3% |

| New Mexico | 1 (Albuquerque) | $167 | $186 | 11.5% | $167* | $186* | 11.5%* |

| New York | 4 (New York City) | $372 | $369 | -0.7% | $207 | $203 | -1.9% |

| Oregon | 1 (Portland) | $212 | $228 | 7.7% | $207 | $189 | -8.6% |

| Vermont | 1 (Burlington) | $428 | $471 | 10.0% | $200 | $203 | 1.6% |

| Virginia | 7 (Richmond) | $241 | $287 | 19.0% | $189 | $208 | 9.8% |

| Washington | 1 (Seattle) | $235 | $225 | -4.2% | $189 | $205 | 8.6% |

| Average % change from 2015 | 4.5% | 1.5% | |||||

| SOURCE: Kaiser Family Foundation analysis of 2016 insurer rate filings to state regulators.NOTES: Rates are not yet final and subject to review by the state. Oregon rates reflect preliminary changes from the state. *Unsubsidized Albuquerque premiums are so low that a 40 year old making $30,000 per year would not qualify for a premium tax credit in 2016 | |||||||

Active Renewal and Premium Changes

As was the case last year, the plans that had the lowest premiums in 2015 were usually no longer one of the two lowest-cost silver plans in 2016. Among the 10 major cities where we could identify the product offered as the lowest and second-lowest silver plan, in only one city (Portland, Maine) would a person who signed up for either of the two lowest-cost silver plans in 2015 be able to stay in the same plan and still be enrolled in one of the two lowest silver plans in 2016.

| Table 3: Changes in Lowest-Cost Silver Products | |||

| State | Rating Area(Major City) | Is the 2015 Lowest-Cost Silver Still One of Two Lowest Silvers in 2016? | Is the 2015 Second-Lowest-Cost Silver Still One of Two Lowest Silvers in 2016? |

| Connecticut | 2 (Hartford) | Yes | No |

| DC | 1 (Washington) | N/A* | N/A* |

| Maine | 1 (Portland) | Yes | Yes |

| Maryland | 1 (Baltimore) | Yes | No |

| Michigan | 1 (Detroit) | Yes | No |

| New Mexico | 1 (Albuquerque) | No | No |

| New York | 4 (New York City) | No | No |

| Oregon | 1 (Portland) | No | No |

| Vermont | 1 (Burlington) | Yes | No |

| Virginia | 7 (Richmond) | No | No |

| Washington | 1 (Seattle) | Yes | No |

| SOURCE: Kaiser Family Foundation analysis of 2016 insurer rate filings to state regulatorsNOTES: Rates are not yet final and subject to review by the state.*The District of Columbia did not public sufficient detail to determine whether plans are the same as those offered in 2015, but the insurers are the same. | |||

This underscores the importance of enrollees actively shopping each open enrollment period. For example, in Seattle, Washington, Bridgespan offered the second-lowest-cost silver plan in 2015 at a premium of $254 per month for a single 40 year-old before taking a tax credit into account. Bridgespan is increasing this plan’s rate to $286 per month for 2016, but another insurer (Ambetter) is undercutting it and offering two lower-cost silver options for $225 and $228 per month. An unsubsidized person enrolled in the 2015 second-lowest silver plan offered by Bridgespan would see a 12.6% increase if she stayed in the same plan. Conversely, if she switched to the new second-lowest silver plan offered by Ambetter, her premium would drop -10.1% (before accounting for the relatively small effect aging up a year would have on her premiums).

The effect of changes in the benchmark premium relative to other plans is magnified for subsidized enrollees because the tax credit is tied to the premium for the second-lowest cost silver plan in a given year. If the same 40 year-old in the example above makes $30,000, she would be paying $208 per month in 2015 for the benchmark plan (offered by Bridgespan) and the federal government covers the rest through a tax credit. In 2016, if she switches to the new benchmark (offered by Ambetter), she would continue to pay $208 per month (assuming she continues to have the same income and family size in 2016). However, if she stayed in the Bridgespan plan, she would have to pay that amount plus the premium difference between the Bridgespan and Ambetter plans, or a total of approximately $266 (an increase of about 28%, before accounting for a relatively small increase resulting from aging one year). To keep her lower premium, she has to be willing to switch plans. Similar situations arise in the 9 cities where a low-cost insurer is raising its premiums faster than other carriers, or where a different insurer is offering lower premium.

In addition to switching plans, the person in the example above would also have to switch insurance companies in order to avoid a significant premium increase. Similar situations could arise for people enrolled in at least one of the two lowest-cost silver plans in 2015 in seven out of eleven major cities.

| Table 4: Changes in Insurers Offering the Lowest-Cost Silver Products | |||

| State | Rating Area (Major City) | Would person enrolled in 2015 Lowest-Cost Silver Have to Switch Insurers to Stay in One of Two Lowest Plans? | Would person enrolled in 2015 Second-Lowest-Cost Silver Have to Switch Insurers to Stay in One of Two Lowest Plans? |

| Connecticut | 2 (Hartford) | No | No |

| DC | 1 (Washington) | No | No |

| Maine | 1 (Portland) | No | No |

| Maryland | 1 (Baltimore) | No | Yes |

| Michigan | 1 (Detroit) | No | Yes |

| New Mexico | 1 (Albuquerque) | Yes | No |

| New York | 4 (New York City) | Yes | Yes |

| Oregon | 1 (Portland) | No | Yes |

| Vermont | 1 (Burlington) | No | No |

| Virginia | 7 (Richmond) | Yes | Yes |

| Washington | 1 (Seattle) | No | Yes |

| SOURCE: Kaiser Family Foundation analysis of 2016 insurer rate filings to state regulatorsNOTES: Rates are not yet final and subject to review by the state. | |||

Although switching insurance carries could help stimulate competition in the exchange – which, to some extent, is how the premium tax credit is designed to work – changing insurance carriers can cause challenges for some enrollees, in particular potentially needing to change doctors (although staying with the same carrier from year-to-year does not necessarily guarantee a consistent network of doctors either).

Insurer Participation

On average, 7 insurers (grouped by parent company) will offer coverage in these states in 2016, which is a similar number that participated in 2015 and an increase from 6 in 2014. Insurer participation has increased or remained stable in all of the states but Michigan, where the number dropped from 13 to 12 and the District of Columbia, where the number dropped from 3 to 2. The number of insurers participating in these states’ Marketplaces ranges from 2 in Vermont and DC to 16 in New York.

| Table 5: Number of Insurers, Grouped by Parent Company, Participating in Marketplaces, 2014 – 2016 | |||

| State | 2014 | 2015 | 2016 |

| Connecticut | 3 | 4 | 4 |

| DC | 3 | 3 | 2 (Aetna exited) |

| Maine | 2 | 3 | 4 (Aetna entered) |

| Maryland | 4 | 5 | 5 |

| Michigan | 9 | 13 | 12 (Assurant exited) |

| New Mexico | 4 | 5 | 5 |

| New York | 16 | 16 | 16 |

| Oregon | 11 | 10 | 11 (Zoom Health entered) |

| Vermont | 2 | 2 | 2 |

| Virginia | 5 | 6 | 6 |

| Washington | 7 | 9 | 11 (UnitedHealth and Health Alliance entered) |

| AVERAGE | 6.0 | 6.9 | 7.1 |

| SOURCE: Kaiser Family Foundation analysis of 2016 insurer rate filings to state regulatorsNOTES: Filings are not yet final and subject to review by the state. | |||

Discussion

Premium changes for 2016 will vary substantially across areas and across insurers within a given region. At this time, with complete premium information only available in 10 states plus DC, and still awaiting final reviews by state regulators, it is too soon to draw conclusions about the premiums nationally. As a result of the ACA’s rate review provision, data has become public on rate increases over 10 percent, with some insurers requesting average increases well into the double digits. However, the patterns in these 10 states and DC, where more complete information is available, suggest that the premiums for the two lowest-cost silver plans – where the bulk of enrollees tend to migrate – are not necessarily increasing, and where they are increasing, the growth has generally been moderate.

As discussed in detail in our previous analysis, there are a variety of factors that may influence variations in premium changes, including the accuracy with which insurers had predicted their rates in 2014 and 2015, the composition of the risk pool, the steadiness of enrollment growth, and competitive dynamics. The proposed rates for 2016 represent the first year where insurers are able to set premiums based on actual claims experience for Marketplace enrollees. Even so, insurers only have annual data from 2014, which was incomplete (as most enrollees did not effectuate coverage until mid-year, whereas deductibles are annual) and not necessarily representative (as there was likely pent-up demand for health services among people who were previously uninsured).

Some of this remaining uncertainty is mitigated by the ACA’s “3 R’s” programs. These programs – risk adjustment, reinsurance, and risk corridors – redistribute risk among insurance carriers so that plans that enroll disproportionately sicker or higher-cost enrollees can be prevented from having to significantly raise premiums. However, two of these three programs (reinsurance and risk corridors) were only intended to be transitional, and reinsurance funding is phasing out from a maximum of $10 billion in 2014 to $4 billion in 2016. Another potential driver of 2016 premium increases is that the underlying cost of health care is expected to increase next year, particularly for prescription drugs.

Factors that could have a downward effect on premiums in 2016 include competitive forces (for which average growth in the number of insurers is a positive sign); increases in enrollment among the uninsured (which would bring healthier enrollees into the risk pool); and the movement of healthier enrollees from “grandmothered” plans into ACA-compliant plans either on- or off- of the exchange.

Finalized information on 2016 Marketplace premiums will become available for these and other states over the next few months, with complete information for all 50 states typically becoming public shortly before open enrollment, which begins November 1, 2015.

Methods

Data were collected from health insurer rate filing submitted to state regulators. These submissions are publicly available for the states we analyzed. Most rate information is available in the form of a SERFF filing (System for Electronic Rate and Form Filing) that includes a base rate and other factors that build up to an individual rate. In states where filings were unavailable, we gathered data from tables released by state insurance departments. Filings are still preliminary. All premiums in this analysis are at the rating area level, and some plans may not be available in all cities or counties within the rating area. Rating areas are typically groups of neighboring counties, so a major city in the area was chosen for identification purposes.