Health insurance coverage is an important factor in making health care affordable and accessible to women.1 Women with health coverage are more likely to obtain needed preventive, primary, and specialty care services, and have better access to new advances in women’s health. Among the 97.5 million women ages 19 to 64 residing in the U.S., most had some form of coverage in 2023. Over the past decade, the Affordable Care Act (ACA) has expanded access to affordable coverage through a combination of Medicaid expansions, private insurance reforms, and premium tax credits. However, while the uninsured rate has declined significantly in the past decade, gaps in private sector coverage, enrollment and eligibility barriers in publicly-funded programs, and persistent affordability challenges have left one in ten women uninsured. This factsheet reviews major sources of coverage for women residing in the U.S. in 2023, discusses the impact of the ACA on women’s coverage, and the coverage challenges that many women continue to face.

Sources of Health Insurance Coverage

Employer-Sponsored Insurance

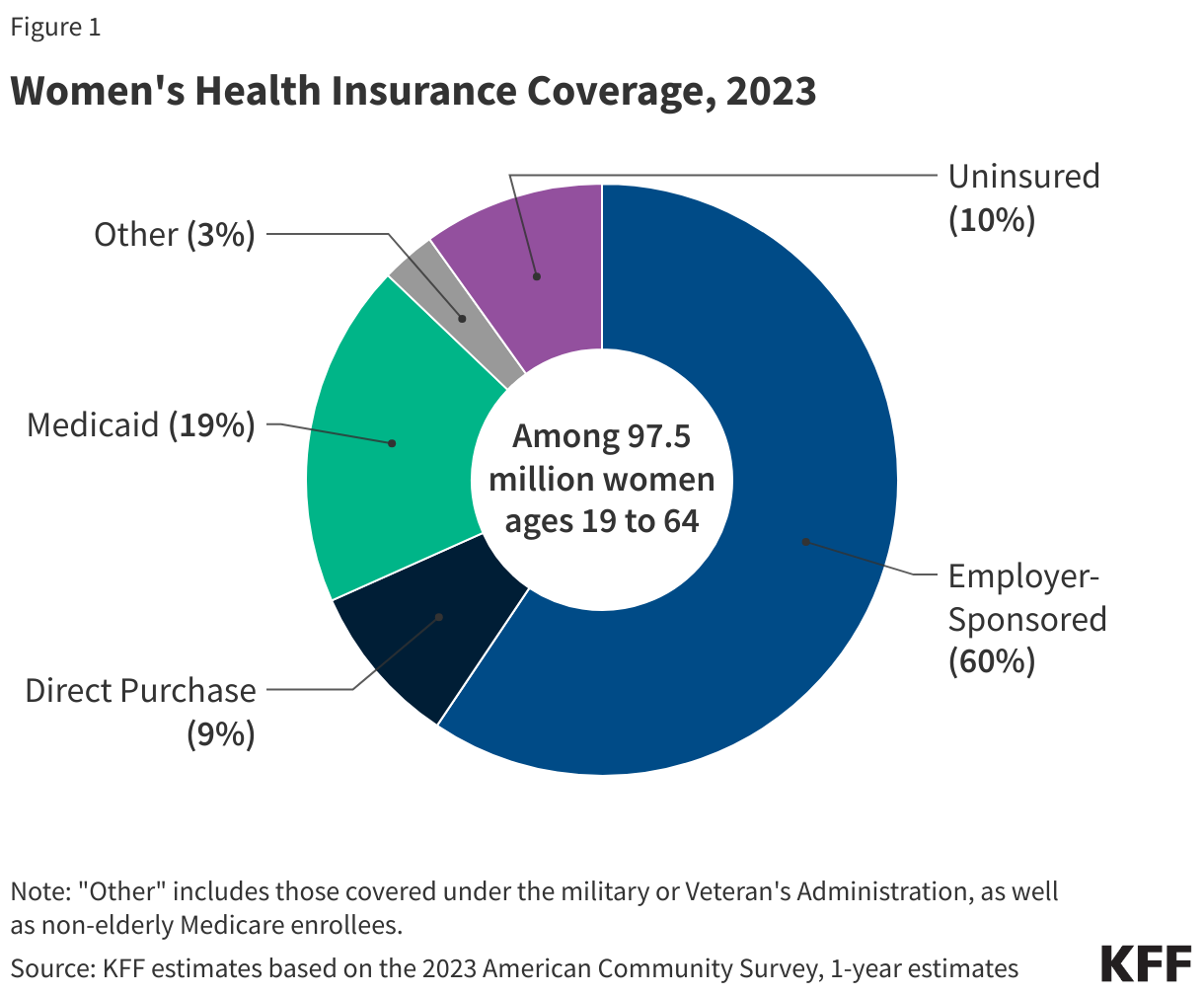

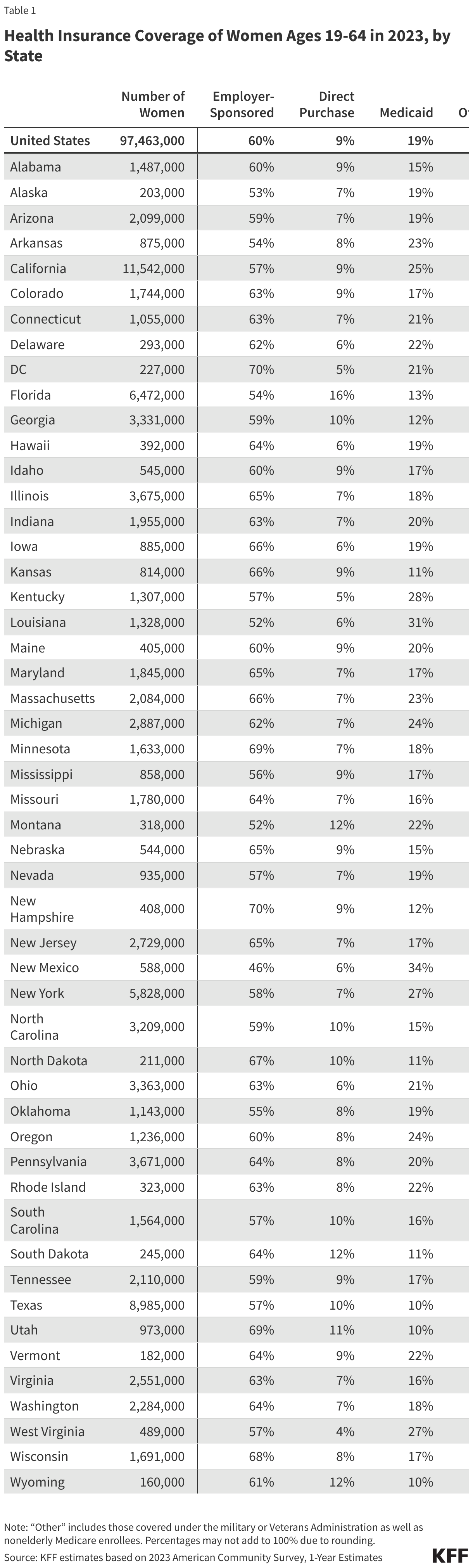

Approximately 58.6 million women ages 19-64 (60%) received their health coverage from employer-sponsored insurance in 2023 (Figure 1).2

- Women in families with at least one full-time worker are more likely to have job-based coverage (70%) than women in families with only part time workers (33%) or without any workers (17%).3

- In 2023, annual insurance premiums for employer sponsored insurance averaged $8,435 for individuals and $23,968 for families. Family premiums have increased 43% over the last decade. On average, workers paid 17% of premiums for individual coverage and 29% for family coverage with the employers picking up the balance.

Non-Group Insurance

The ACA expanded access to the non-group or individually purchased insurance market by offering premium tax credits to help individuals afford coverage purchase through state-based health insurance Marketplaces. It also included many insurance reforms to alleviate some of the long-standing barriers to coverage (such as gender rating, lack of maternity coverage, and pre-existing conditions having a disproportionate effect on women) in the non-group insurance market. In 2023, about 9% of women ages 19 to 64 (approximately 8.4 million women) and 8% of their male counterparts purchased insurance in the non-group market.4 This includes individuals who purchased private policies from the ACA Marketplace in their state, as well as those who purchased coverage from private insurers that operate outside of Marketplaces.

- Most individuals who seek insurance policies in their state’s Marketplace qualify for assistance with the costs of coverage. Individuals with incomes below $58,320 (400% of the Federal Poverty Level in 2023) can qualify for assistance in the form of federal tax credits which lower premium costs. The American Rescue Act (ARPA) of 2021, and subsequently the Inflation Reduction Act of 2022, have provided a temporary extension of Marketplace subsidies to people with higher income levels and led to record high enrollments in the ACA marketplace. These subsidies are set to expire at the end of 2025 and if they are not renewed, it would lead to a steep increase in insurance premium payments for ACA Marketplace enrollees. It is unclear whether the incoming Trump Administration plans to extend these subsidies or let them expire.

- The ACA set new standards for all individually purchased plans, including plans available through the Marketplace as well as those that existed prior to the ACA. The ACA bars plans from charging women higher premiums than men for the same level of coverage (gender rating) or from disqualifying women from coverage because they had certain pre-existing medical conditions, including pregnancy. All direct purchase plans must also cover certain “essential health benefits” (EHBs) that fall under 10 different categories, including maternity and newborn care, mental health, and preventive care.

Medicaid

The state-federal program for individuals with low-incomes, Medicaid, covered 19% of adult women ages 19 to 64 in 2023, compared to 14% of men. Historically, to qualify for Medicaid, women had to have very low incomes and be in one of Medicaid’s eligibility categories: pregnant, mothers of children 18 and younger, a person with a disability, or over 65. Women who didn’t fall into these categories typically were not eligible regardless of how poor they were. The ACA allowed states to broaden Medicaid eligibility to most individuals with incomes less than 138% of the FPL regardless of their family or disability status, effective January 2014. As of December 2024, 40 states and DC have expanded their Medicaid programs under the ACA.

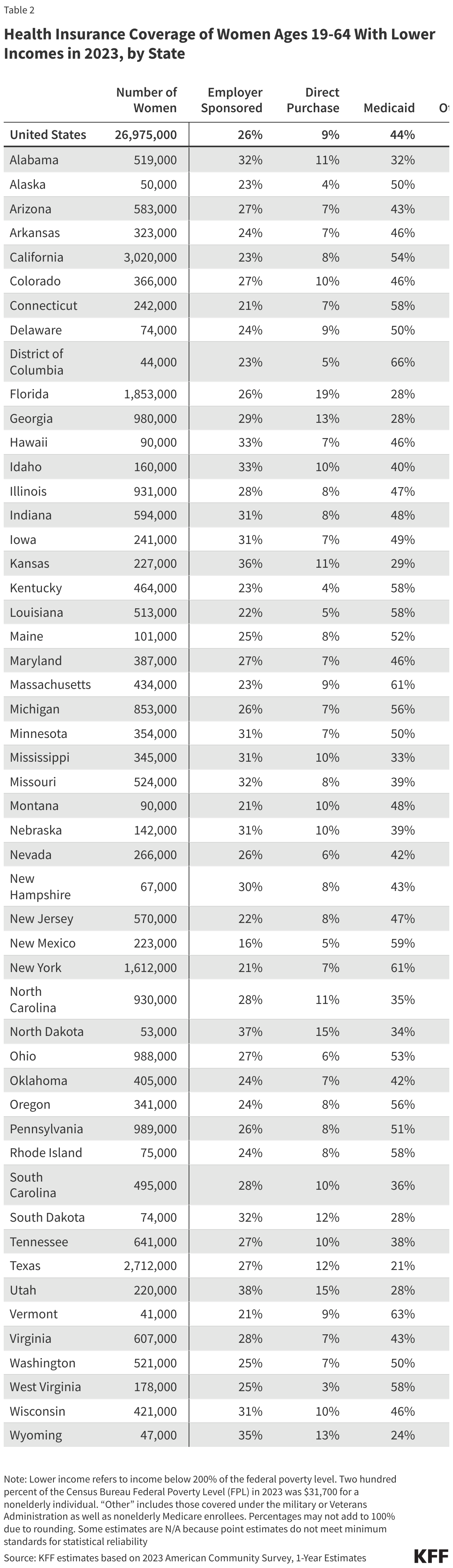

- Medicaid covers the poorest population of women. Forty-four percent of women with low-incomes (below 200% FPL) and 52% of women living below the federal poverty level have Medicaid coverage.5

- By federal law, all states must provide Medicaid coverage to pregnant women with incomes up to 133% of the federal poverty level (FPL) through 60 days postpartum. However, in recent years, there has been a growing interest in expanding the length of the postpartum coverage period, and to date, all but two states have taken steps to extend postpartum Medicaid coverage to 12 months.

- During the COVID-19 public health emergency (PHE), states provided continuous coverage to all Medicaid enrollees who had been enrolled in the program since March 18, 2020. This requirement ended on March 31, 2023, and states have gone through the process of redeterminations for Medicaid eligibility. In total, over 25 million Medicaid enrollees were disenrolled from the Medicaid program. Disenrollment rates varied across states and despite millions being disenrolled during the unwinding process, currently there are over 10 million more people enrolled in Medicaid than there were at the start of the pandemic.

- Medicaid financed 41% of births in the U.S. in 2022, accounts for 75% of all publicly-funded family planning services and over half (61%) of all long-term care spending, which is critical for many frail elderly women.

- Over half of the states have established programs that use Medicaid funds to cover the costs of family planning services for women with lower incomes who remain uninsured, and most states have limited scope Medicaid programs to pay for breast and cervical cancer treatment for certain low-income uninsured women.

- Under federal law Medicaid coverage of abortion is very limited. The federal Hyde Amendment prohibits federal spending on abortions, except when the pregnancy is a result of rape or incest, or when it jeopardizes the life of the pregnant person. Twenty states use their own unmatched funds to pay for abortions for Medicaid enrollees who seek abortion in other circumstances. On June 24, 2022, the Supreme Court overturned Roe v. Wade, eliminating the federal Constitutional standard that had protected the right to abortion. Absent any federal standard addressing a right to abortion, states may set their own policies banning or protecting abortion. Among the 37 states and DC where abortion remains legal, 17 states and DC follow the Hyde restrictions, greatly limiting coverage for people who seek abortion care in those states.

Uninsured

On average, women have lower incomes and have been more likely to qualify for Medicaid than men under one of Medicaid’s eligibility categories; pregnant, parent of children under 18, disabled, or over 65. As a result, women are more likely than men to qualify for Medicaid and less likely to be uninsured. In 2023, 13% of men ages 19-64 were uninsured compared to approximately 10% of women in the same age bracket (9.3 million women).

Uninsured women often have inadequate access to care, get a lower standard of care when they are in the health system, and have poorer health outcomes. Compared to women with insurance, uninsured women have lower use of important preventive services such as mammograms, Pap tests, and timely blood pressure checks. They are also less likely to report having a regular doctor.

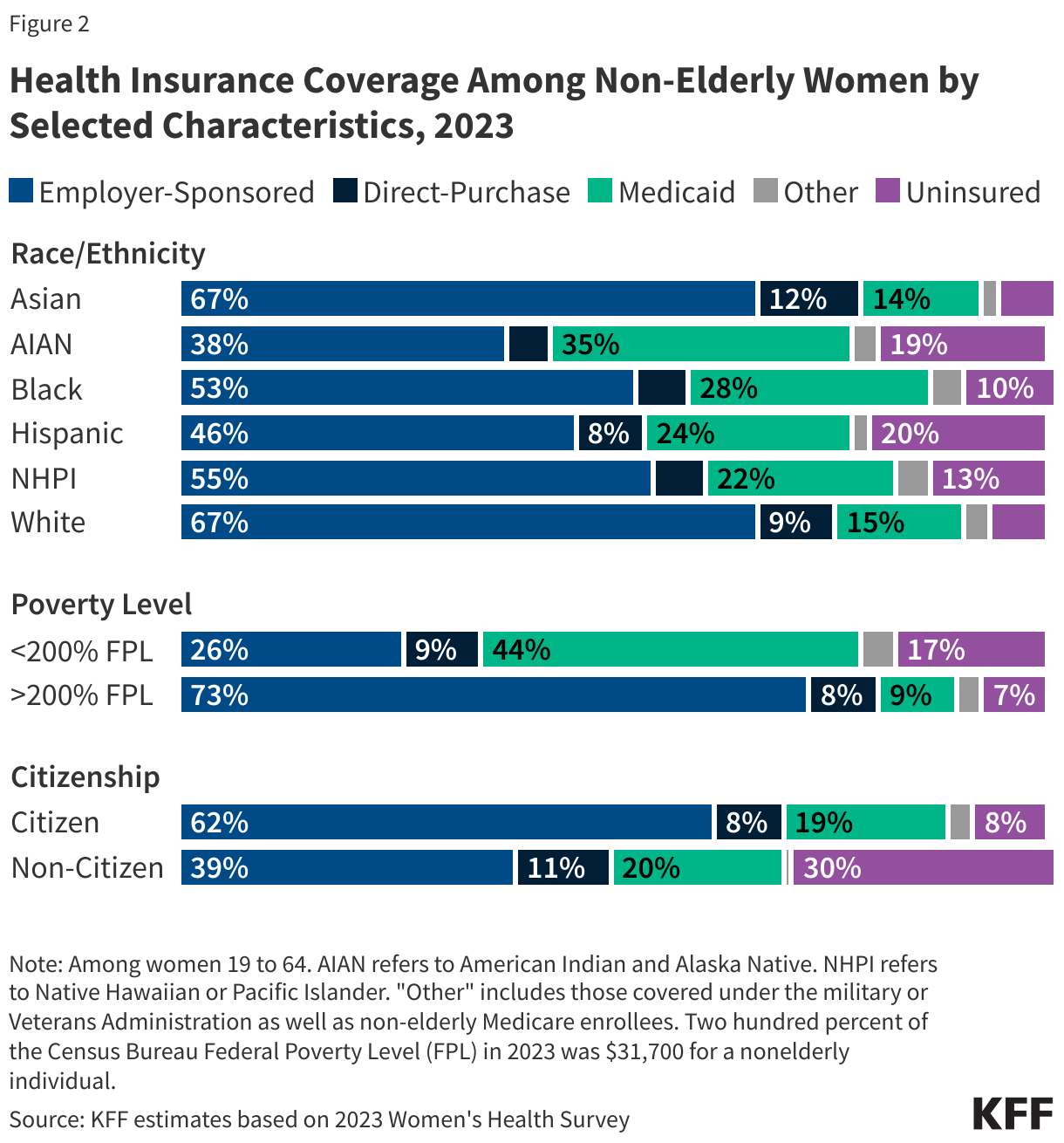

- Women with lower incomes, women of color, and women who are non-citizens are at greater risk of being uninsured (Figure 2). One in five (17%) women with incomes under 200% of the FPL ($31,700 for an individual in 2023) are uninsured (Table 2), compared to 7% of women with incomes at or above 200% FPL. One in five Hispanic (20%) and American Indian and Alaska Native (19%) women are uninsured. A higher share of women in single parent households are uninsured (10%) than women in two-parent households (7%) (data not shown).6

- The majority of women who are uninsured live in a household where someone is working: 69% are in families with at least one adult working full-time and 82% are in families with at least one part-time or full-time worker.7

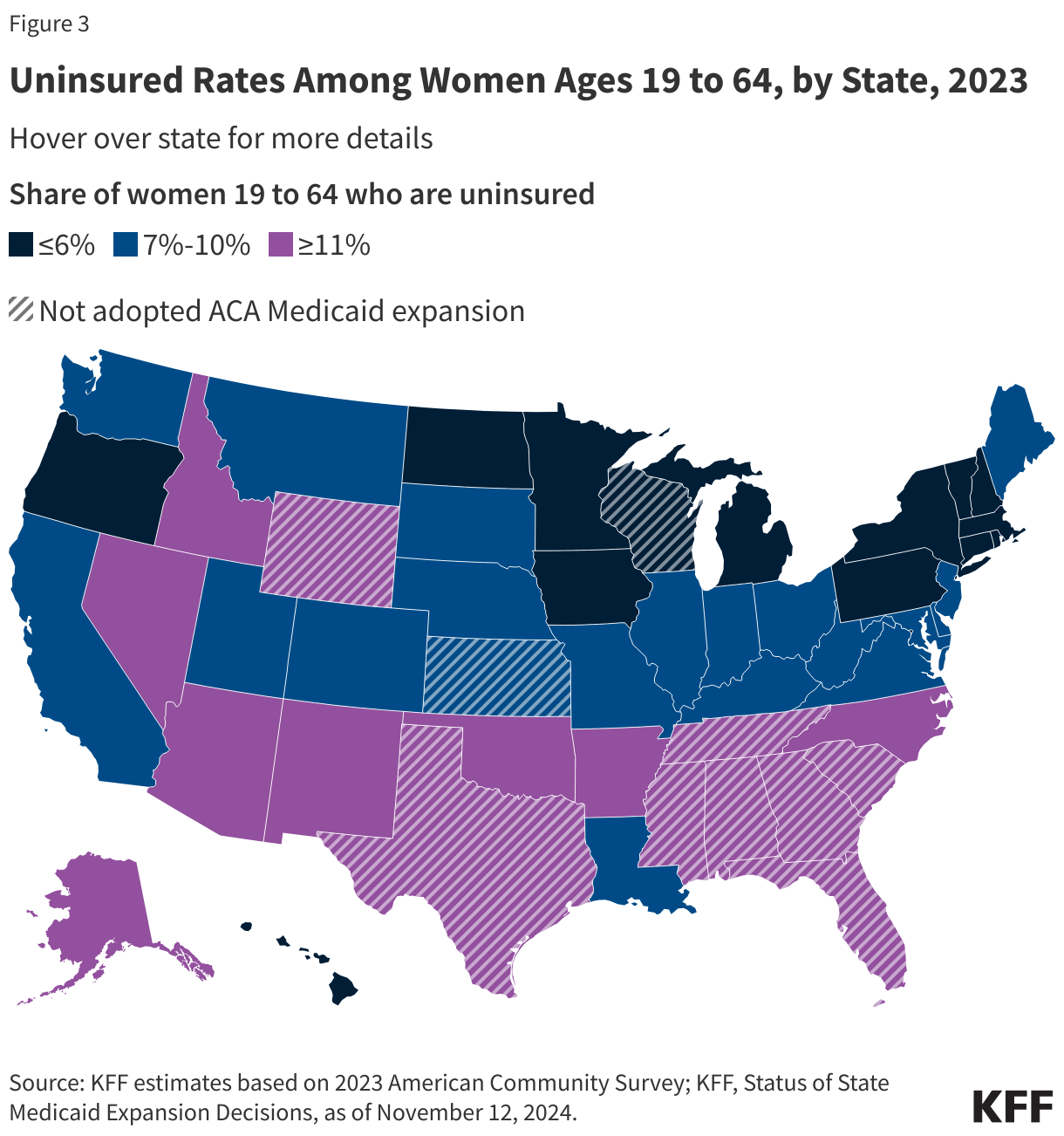

- There is considerable state-level variation in uninsured rates across the nation, ranging from 20% of women in Texas to 3% of women in Hawaii, DC, Massachusetts, and Vermont (Figure 3). Of the 16 states with uninsured rates above the national average (10%), eight have not adopted the ACA Medicaid expansion.

- Many women who are uninsured are potentially eligible for financial assistance with coverage. Some are likely eligible for Medicaid but are not enrolled, while others qualify for subsidized Marketplace plans but may not be aware of coverage options or may face barriers to enrollment. However, in states that have not adopted the ACA Medicaid expansion, some women who are poor and uninsured fall into a “coverage gap” because they earn too much to qualify for Medicaid but not enough to qualify for Marketplace premium tax credits. Other uninsured women are not eligible for any assistance with health coverage due to their immigration status, their income, or because they have an offer from an employer.

Scope of Coverage and Affordability

The ACA set national standards for the scope of benefits offered in private plans. In addition to the broad categories of essential health benefits (EHBs) offered by marketplace plans, all privately purchased plans must cover maternity care which had been historically excluded from most individually purchased plans. In addition, most private plans must cover preventive services without co-payments or other cost sharing. This includes screenings for breast and cervical cancers, well woman visits (including prenatal visits), prescribed contraceptives, breastfeeding supplies and supports such as breast pumps, and several STI services. There have been several legal challenges over elements of the preventive services policy, including in the pending case, Braidwood Management Inc. v. Becerra, which could affect whether the preventive services requirement remains intact in the future. Twenty-five states have laws banning coverage of most abortions from the plans available through the state Marketplaces. These restrictions were in place prior to the Supreme Court’s decision to overturn Roe v Wade.

Affordability of coverage continues to be a significant concern for many women, both for those who are uninsured as well as those with coverage. The leading reason why uninsured adults report that they haven’t obtained coverage is that it is too expensive. Under employer-sponsored insurance, the major source of coverage for women, 60% of all covered workers with a general annual deductible have deductibles of at least $1,000 for single coverage. Thirty-seven percent of women with employer sponsored coverage report that it is difficult to meet their deductibles.8

Endnotes

This factsheet is based on KFF analysis of data from the American Community Survey (ACS), which stratifies data by an individual's sex as male or female. Throughout this brief we refer to “women” but recognize that not all people who are born as females identify as "women."

KFF estimates based on 2023 American Community Survey, 1-Year Estimates.

Ibid.

Ibid.

Ibid.

KFF estimates based on 2023 American Community Survey, 1-Year Estimates.

Ibid.

KFF June 2019 Health Tracking Poll.