Medicaid Reforms to Expand Coverage, Control Costs and Improve Care: Results from a 50-State Medicaid Budget Survey for State Fiscal Years 2015 and 2016

Provider Rates, Taxes and Benefits

| Key Section Findings |

Tables 15 through 17 provide a complete listing of Medicaid provider rate changes and provider taxes and fees in place in FY 2015 and FY 2016; Tables 19 through 21 provide a complete listing of Medicaid benefit and pharmacy changes for FY 2015 and FY 2016. These tables are also available in a downloadable PDF. |

Provider Rates

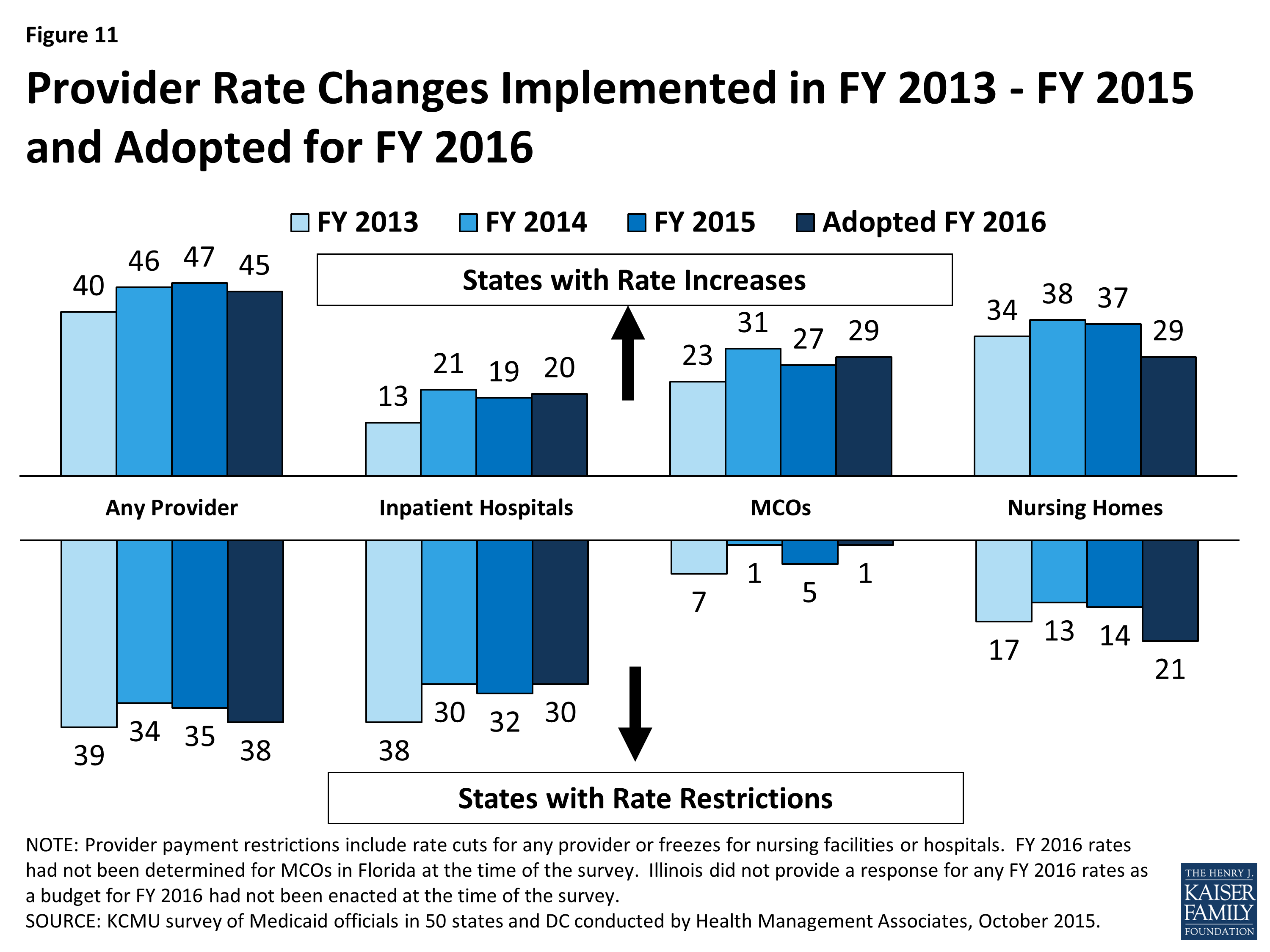

State fiscal conditions have a direct impact on Medicaid provider rates. During economic downturns, states often turn to provider rate cuts to control costs. Improving state finances in recent years have resulted in more states restoring or enhancing rates than restricting rates overall. In both FY 2015 and FY 2016, more states implemented or planned rate increases (47 and 45 states) compared to rate restrictions (35 states and 38 states) in those years. (Figure 11) Data for FY 2016 was not available for Illinois as budget deliberations were in process in September 2015.1 The number of states with rate increases exceeded the number of states with restrictions in FY 2015 and FY 2016 across all major categories of providers (physicians, MCOs and nursing homes) except for inpatient rates for hospitals.2

Figure 11: Provider Rate Changes Implemented in FY 2013 – FY 2015 and Adopted for FY 2016

For the purposes of this report, provider rate restrictions include cuts to fee-for-service rates for physicians, dentists, outpatient hospitals, and to capitation rates for managed care organizations, as well as cuts or freezes in rates for inpatient hospitals and nursing homes. States were asked to report aggregate changes for each major provider category. The ultimate impact of some rate changes may differ across states depending on the delivery system. For example, the effect of fee-for-service rate restrictions for hospitals, physicians, and nursing facilities rates may have less impact on providers in states that rely heavily on managed care than in states that have little or no managed care presence.

Only three states in FY 2015 and five states in FY 2016 had implemented or planned inpatient hospital rate reductions; the vast majority of hospital rate restrictions were freezes in rates. A few states noted that restrictions to inpatient hospital rates were a reflection of shifting some funding from inpatient to outpatient hospital rates. The number of states increasing nursing home rates dropped sharply in FY 2016. One state (Illinois3) cut nursing home rates in FY 2015 and four states indicated plans to cut nursing home rates in FY 2016. The other nursing home rate restrictions are rate freezes. (Figure 11)

Capitation payments for Medicaid Managed Care Organizations (MCOs) are generally bolstered by the federal requirement that states pay actuarially sound rates. In FY 2015 and FY 2016, the majority of the 39 states with Medicaid MCOs implemented or planned increases in MCO rates. Only five states reported MCO rate cuts in 2015, and only one state plans to cut MCO rates in FY 2016. To meet the federally required test of actuarial soundness, reductions to MCO rates may occur as a correction to previous rates that were set too high or to reflect reductions in fee-for-service rates or competitive price bids.

| Primary Care Payments |

The ACA included a provision to increase Medicaid payment rates for primary care services to Medicare rates from January 1, 2013 through December 31, 2014. The federal government funded 100 percent of the difference between Medicaid rates that were in effect as of July 1, 2009 and the full Medicare rates for these two years. States were asked about their plans to extend this provision for FY 2016 (at regular FMAP rates). The significance of this rate differential varies greatly across states; a 2012 survey of Medicaid physician fees showed that in a small number of states, Medicaid rates for physician services were already at or close to 100 percent of Medicare rates while other states paid sixty percent or less of Medicare rates.4

Among the states that did not continue the ACA primary care rate increase in FY 2015, seven states (Indiana, Missouri, New Jersey, New York, Ohio, South Dakota and Vermont) reported plans to increase primary care physician rates in FY 2016 from FY 2015 levels. |

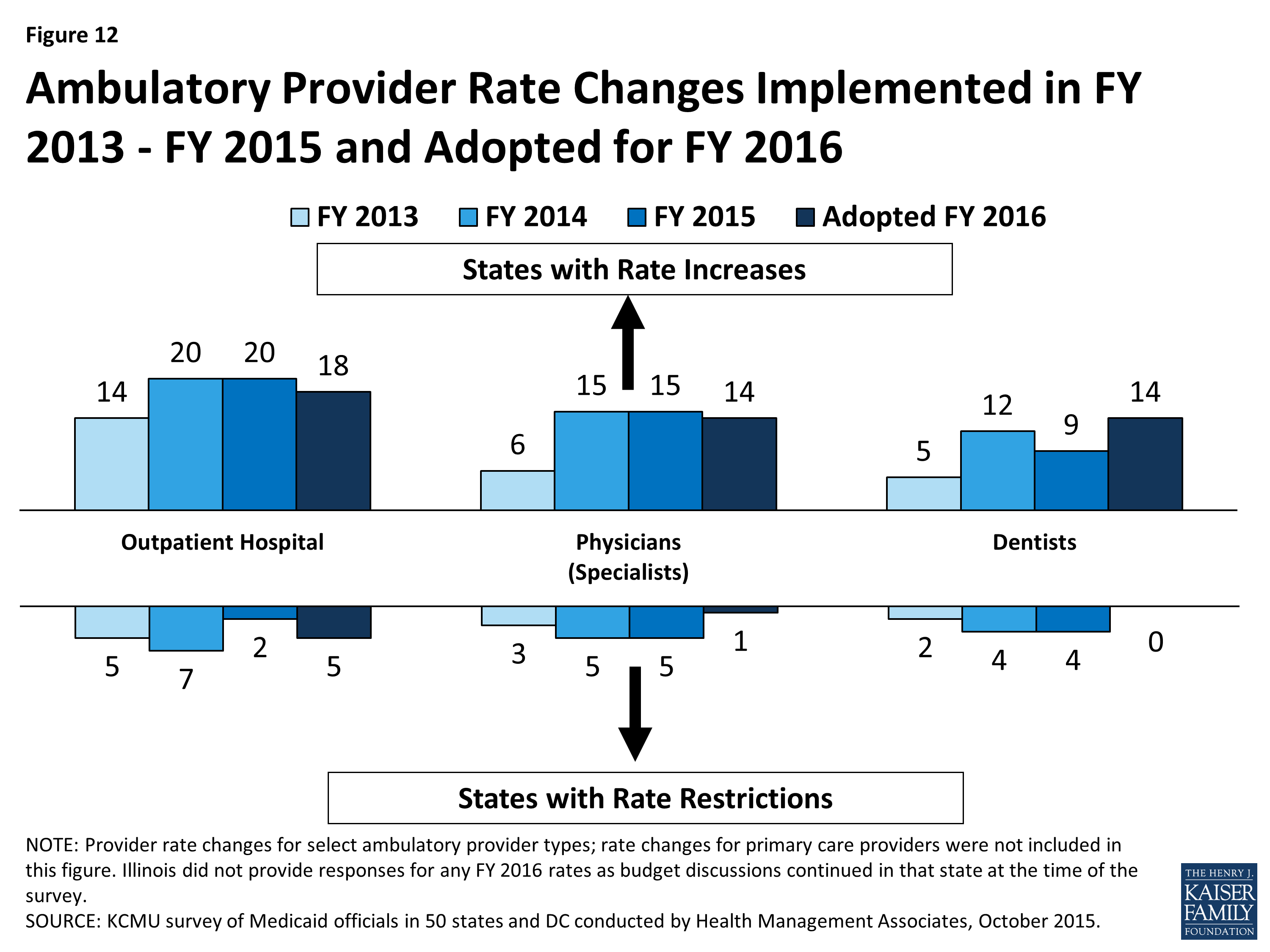

In addition to primary care providers, the survey also asked about rates for specialist physicians, dentists and for outpatient services. For each of these categories, states reported more rate increases than rate cuts, particularly in FY 2015 and FY 2016. (Figure 12)

Figure 12: Ambulatory Provider Rate Changes Implemented in FY 2013 – FY 2015 and Adopted for FY 2016

Potentially Preventable Readmissions

States were asked if they had or planned to implement an inpatient hospital reimbursement incentive/policy for potentially preventable readmissions. Fifteen (15) states indicated that they had such policies in place in FY 2014 and two more states implemented such policies in FY 2015. Six states indicated that they have plans to implement in FY 2016 and an additional four states plan to implement after FY 2016.

Early Elective Deliveries

States were asked about reimbursement policies designed to reduce the number of early elective deliveries. Twenty (20) states had a policy in place in FY 2015 and six additional states plan to adopt such a policy in FY 2016. Some of the states that do not have such a policy indicated that their managed care organizations can elect to have such a policy. The most common policy was reduced payment (paying for a Cesarean-Section at the rate of a vaginal delivery) for any Cesarean-Section before 39 weeks gestational age unless there was documentation of medical necessity. States are also implementing incentive programs that reward providers for reducing the rate of early elective deliveries.

Provider Taxes and Fees

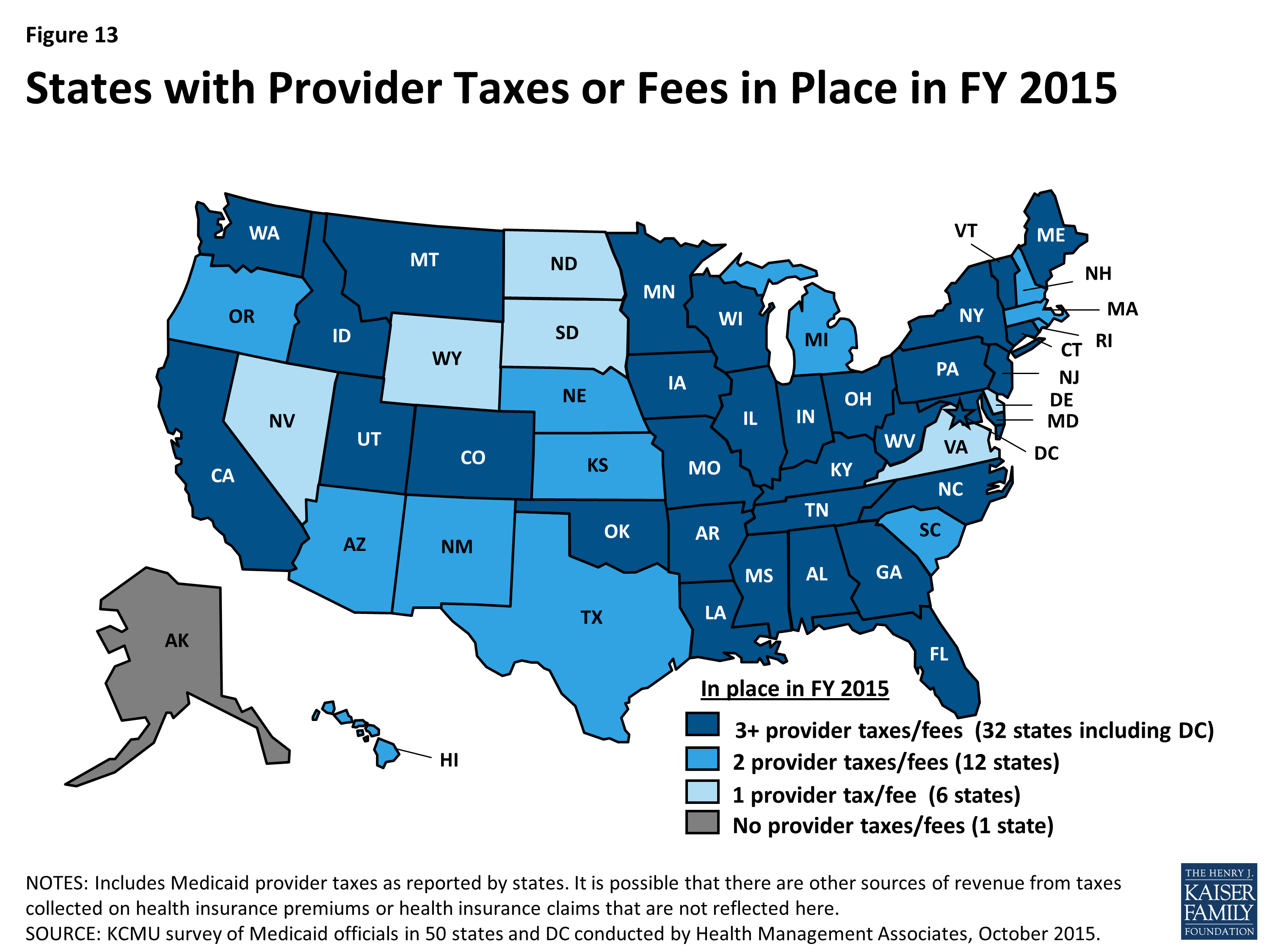

States continue to rely on provider taxes and fees to provide a portion of the non-federal share of the costs of Medicaid. At the beginning of FY 2003, a total of 21 states had at least one provider tax in place. Over the next decade, a majority of states imposed new taxes or fees and increased existing tax rates and fees to raise revenue to support Medicaid. By FY 2013, all but one state (Alaska) had at least one provider tax or fee in place.5 In FY 2015, 32 states had three or more provider taxes in place. (Figure 13)

Figure 13: States with Provider Taxes or Fees in Place in FY 2015

The most common provider taxes in place in FY 2015 were taxes on nursing facilities (44 states), followed by taxes on hospitals (39 states) and intermediate care facilities (37 states). In recent years, states have made very few changes to the number of provider taxes. Minor changes for FY 2015 and FY 2016 include the following:

- In FY 2015, two states eliminated provider taxes (a hospital tax in DC and a cosmetic surgery tax in New Jersey).

- For FY 2016, three states and DC reported plans to add provider taxes. DC has a new hospital tax. Connecticut is adding a tax on ambulatory surgery centers. Michigan and Utah are adding taxes on ambulance providers.

Several states reported changes to tax rates in FY 2015 and FY 2016. Most notable were increases to rates for hospital taxes and fees (ten states in FY 2015 and six states in FY 2016) as well as increases to rates for nursing home taxes and fees (six states in FY 2015 and eight states in FY 2016). Some states also reported reducing tax rates, again mostly for hospitals (one state in FY 2015 and four states in FY 2016) and nursing home taxes and fees (two states in FY 2015 and one state in FY 2016).

States were asked whether in the future they planned to use increased provider taxes or fees to fund all or part of the costs of the ACA Medicaid expansion that will occur in calendar year 2017 and beyond when the 100 percent federal match rate for expansion costs starts to decline. Seven of the expansion states (Arizona, California, Colorado, Indiana, Kentucky, Nevada and Ohio) responded that they had such plans. Other expansion states are studying provider taxes and fees.

Table 15: Provider Rate Changes in all 50 States and DC, FY 2015

|

States |

Inpatient Hospital |

Outpatient Hospital |

Specialists |

Dentists |

Managed Care Organizations |

Nursing Facilities |

Total |

|||||||

|

Rate Change |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

|

Alabama |

X |

— |

— |

X |

X |

X |

||||||||

|

Alaska |

X |

X |

X |

— |

— |

X |

X |

|||||||

|

Arizona |

X |

X |

X |

X |

X |

|||||||||

|

Arkansas |

X |

— |

— |

X |

X |

X |

||||||||

|

California |

X |

X |

X |

X |

X |

|||||||||

|

Colorado |

X |

X |

X |

X |

X |

X |

||||||||

|

Connecticut |

X |

X |

— |

— |

X |

X |

||||||||

|

DC |

X |

X |

X |

X |

X |

X |

||||||||

|

Delaware |

X |

X |

X |

X |

X |

X |

X |

X |

||||||

|

Florida |

X |

X |

X |

X |

X |

X |

||||||||

|

Georgia |

X |

X |

X |

X |

X |

|||||||||

|

Hawaii |

X |

X |

X |

X |

X |

|||||||||

|

Idaho |

X |

X |

X |

— |

— |

X |

X |

X |

||||||

|

Illinois |

X |

X |

X |

X |

X |

X |

X |

X |

||||||

|

Indiana |

X |

X |

X |

X |

X |

|||||||||

|

Iowa |

X |

X |

X |

X |

X |

|||||||||

|

Kansas |

X |

X |

X |

X |

X |

|||||||||

|

Kentucky |

X |

X |

X |

|||||||||||

|

Louisiana |

X |

X |

X |

X |

X |

X |

||||||||

|

Maine |

X |

— |

— |

X |

X |

X |

||||||||

|

Maryland |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Massachusetts |

X |

X |

X |

X |

X |

|||||||||

|

Michigan |

X |

X |

X |

X |

X |

X |

||||||||

|

Minnesota |

X |

X |

X |

X |

||||||||||

|

Mississippi |

X |

X |

X |

X |

X |

X |

||||||||

|

Missouri |

X |

X |

X |

X |

X |

|||||||||

|

Montana |

X |

X |

X |

X |

— |

— |

X |

X |

X |

|||||

|

Nebraska |

X |

X |

X |

X |

X |

X |

||||||||

|

Nevada |

X |

X |

X |

X |

X |

|||||||||

|

New |

X |

X |

X |

X |

X |

|||||||||

|

New Jersey |

X |

X |

X |

X |

X |

|||||||||

|

New Mexico |

X |

X |

X |

X |

X |

|||||||||

|

New York |

X |

X |

X |

X |

X |

|||||||||

|

North Carolina |

X |

X |

X |

— |

— |

X |

|

X |

X |

|||||

|

North Dakota |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Ohio |

X |

X |

X |

X |

X |

|||||||||

|

Oklahoma |

X |

X |

X |

X |

— |

— |

X |

X |

||||||

|

Oregon |

X |

X |

X |

X |

||||||||||

|

Pennsylvania |

X |

X |

X |

X |

X |

|||||||||

|

Rhode Island |

X |

X |

X |

X |

X |

|||||||||

|

South Carolina |

X |

X |

X |

X |

X |

|||||||||

|

South Dakota |

X |

X |

X |

X |

— |

— |

X |

X |

||||||

|

Tennessee |

X |

X |

X |

X |

X |

|||||||||

|

Texas |

X |

X |

X |

X |

X |

|||||||||

|

Utah |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Vermont |

X |

X |

X |

X |

— |

— |

X |

X |

||||||

|

Virginia |

X |

X |

X |

X |

X |

X |

||||||||

|

Washington |

X |

X |

X |

X |

X |

|||||||||

|

West Virginia |

X |

X |

X |

X |

||||||||||

|

Wisconsin |

X |

X |

X |

X |

X |

|||||||||

|

Wyoming |

X |

— |

— |

X |

X |

|||||||||

|

Totals |

19 |

32 |

20 |

2 |

15 |

5 |

9 |

4 |

27 |

5 |

37 |

14 |

47 |

35 |

|

NOTES: For the purposes of this report, provider rate restrictions include cuts to rates for physicians, dentists, outpatient hospitals, and managed SOURCE: Kaiser Commission on Medicaid and the Uninsured Survey of Medicaid Officials in 50 states and DC conducted by Health Management |

||||||||||||||

Table 16: Provider Rate Changes in all 50 States and DC, FY 2016

|

States |

Inpatient Hospital |

Outpatient Hospital |

Specialists |

Dentists |

Managed Care Organizations |

Nursing Facilities |

Total |

|||||||

|

Rate Change |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

Increase |

Restrict |

|

Alabama |

X |

— |

— |

X |

X |

X |

||||||||

|

Alaska |

X |

X |

— |

— |

X |

X |

X |

|||||||

|

Arizona |

X |

X |

X |

X |

X |

|||||||||

|

Arkansas |

X |

— |

— |

X |

X |

X |

||||||||

|

California |

X |

X |

X |

X |

X |

X |

||||||||

|

Colorado |

X |

X |

X |

X |

X |

X |

||||||||

|

Connecticut |

X |

— |

— |

X |

X |

X |

||||||||

|

DC |

X |

X |

X |

X |

X |

X |

||||||||

|

Delaware |

X |

X |

X |

X |

X |

X |

X |

X |

||||||

|

Florida |

X |

X |

TBD |

X |

X |

X |

||||||||

|

Georgia |

X |

X |

X |

X |

X |

|||||||||

|

Hawaii |

X |

X |

X |

X |

X |

|||||||||

|

Idaho |

X |

X |

— |

— |

X |

X |

X |

|||||||

|

Illinois |

TBD |

TBD |

TBD |

TBD |

TBD |

TBD |

TBD |

|||||||

|

Indiana |

X |

X |

X |

X |

X |

|||||||||

|

Iowa |

X |

X |

X |

X |

X |

|||||||||

|

Kansas |

X |

X |

X |

X |

X |

|||||||||

|

Kentucky |

X |

X |

X |

|||||||||||

|

Louisiana |

X |

X |

X |

X |

X |

|||||||||

|

Maine |

X |

— |

— |

X |

X |

X |

||||||||

|

Maryland |

X |

X |

X |

X |

X |

X |

X |

X |

||||||

|

Massachusetts |

X |

X |

X |

X |

X |

|||||||||

|

Michigan |

X |

X |

X |

X |

X |

|||||||||

|

Minnesota |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Mississippi |

X |

X |

X |

X |

X |

X |

||||||||

|

Missouri |

X |

X |

X |

X |

X |

X |

X |

X |

||||||

|

Montana |

X |

X |

X |

X |

— |

— |

X |

X |

||||||

|

Nebraska |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Nevada |

X |

X |

X |

X |

X |

|||||||||

|

New Hampshire |

X |

X |

X |

|||||||||||

|

New Jersey |

X |

X |

X |

X |

X |

X |

||||||||

|

New Mexico |

X |

X |

X |

X |

X |

|||||||||

|

New York |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

North Carolina |

X |

— |

— |

X |

X |

|||||||||

|

North Dakota |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Ohio |

X |

X |

X |

X |

X |

X |

X |

X |

||||||

|

Oklahoma |

X |

— |

— |

X |

X |

|||||||||

|

Oregon |

X |

X |

X |

X |

||||||||||

|

Pennsylvania |

X |

X |

X |

X |

X |

|||||||||

|

Rhode Island |

X |

X |

X |

X |

X |

X |

||||||||

|

South Carolina |

X |

X |

X |

X |

X |

|||||||||

|

South Dakota |

X |

X |

X |

X |

— |

— |

X |

X |

||||||

|

Tennessee |

X |

X |

X |

|||||||||||

|

Texas |

X |

X |

X |

X |

X |

X |

||||||||

|

Utah |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Vermont |

X |

— |

— |

X |

X |

X |

||||||||

|

Virginia |

X |

X |

X |

X |

X |

X |

||||||||

|

Washington |

X |

X |

X |

X |

X |

|||||||||

|

West Virginia |

X |

X |

X |

X |

||||||||||

|

Wisconsin |

X |

X |

X |

X |

X |

X |

||||||||

|

Wyoming |

X |

— |

— |

X |

X |

X |

||||||||

|

Totals |

20 |

30 |

18 |

5 |

14 |

1 |

14 |

0 |

29 |

1 |

29 |

21 |

45 |

38 |

|

NOTES: For the purposes of this report, provider rate restrictions include cuts to rates for physicians, dentists, outpatient hospitals, and managed care organizations as well as both cuts or freezes in rates for inpatient hospitals and nursing facilities. Changes to primary care rates were asked about separately for FY 2016 and are not included in this table. There are 12 states that did not have Medicaid MCOs in operation in FY 2015; they are denoted as ‘–‘ in the MCO column. TBD – At the time of the survey, some rates for a few states were still being determined; these are denoted as TBD. SOURCE: Kaiser Commission on Medicaid and the Uninsured Survey of Medicaid Officials in 50 states and DC conducted by Health Management Associates, October 2015. |

||||||||||||||

Table 17: Provider Taxes in Place in the 50 States and DC, FY 2015 and 2016

|

States |

Hospitals |

Intermediate Care Facilities |

Nursing Facilities |

Other |

Any Provider Tax |

|||||

|

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

|

|

Alabama |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Alaska |

||||||||||

|

Arizona |

X |

X |

X |

X |

X |

X |

||||

|

Arkansas |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

California |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Colorado |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Connecticut |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

|

Delaware |

X |

X |

X |

X |

||||||

|

DC |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

|

Florida |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Georgia |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Hawaii |

X |

X |

X |

X |

X |

X |

||||

|

Idaho |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Illinois |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Indiana |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Iowa |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Kansas |

X |

X |

X |

X |

X |

X |

||||

|

Kentucky |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

Louisiana |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Maine |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Maryland |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Massachusetts |

X |

X |

X |

X |

X |

X |

||||

|

Michigan |

X |

X |

X |

X |

X |

X |

X |

|||

|

Minnesota |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Mississippi |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Missouri |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

Montana |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Nebraska |

X |

X |

X |

X |

X |

X |

||||

|

Nevada |

X |

X |

X |

X |

||||||

|

New Hampshire |

X |

X |

X |

X |

X |

X |

||||

|

New Jersey |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

New Mexico |

X* |

X* |

X |

X |

||||||

|

New York |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

North Carolina |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

North Dakota |

X |

X |

X |

X |

||||||

|

Ohio |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Oklahoma |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

Oregon |

X |

X |

X |

X |

X |

X |

||||

|

Pennsylvania |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

Rhode Island |

X |

X |

X |

X |

X |

X |

||||

|

South Carolina |

X |

X |

X |

X |

X |

X |

||||

|

South Dakota |

X |

X |

X |

X |

||||||

|

Tennessee |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Texas |

X |

X |

X |

X |

X |

X |

||||

|

Utah |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

|

Vermont |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

Virginia |

X |

X |

X |

X |

||||||

|

Washington |

X |

X |

X |

X |

X |

X |

X |

X |

||

|

West Virginia |

X |

X |

X |

X |

X |

X |

X* |

X* |

X |

X |

|

Wisconsin |

X |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|

Wyoming |

X |

X |

X |

X |

||||||

|

Totals |

39 |

40 |

37 |

37 |

44 |

44 |

19 |

22 |

50 |

50 |

|

NOTES: This table includes Medicaid provider taxes as reported by states. Some states also have premium or claims taxes that apply to managed care organizations and other insurers. Since this type of tax is not considered a provider tax by CMS, these taxes are not counted as provider taxes in this report. (*) has been used to denote states with multiple “other” provider taxes. SOURCE: Kaiser Commission on Medicaid and the Uninsured Survey of Medicaid Officials in 50 states and DC conducted by Health Management Associates, October 2015. |

||||||||||

Benefits Changes

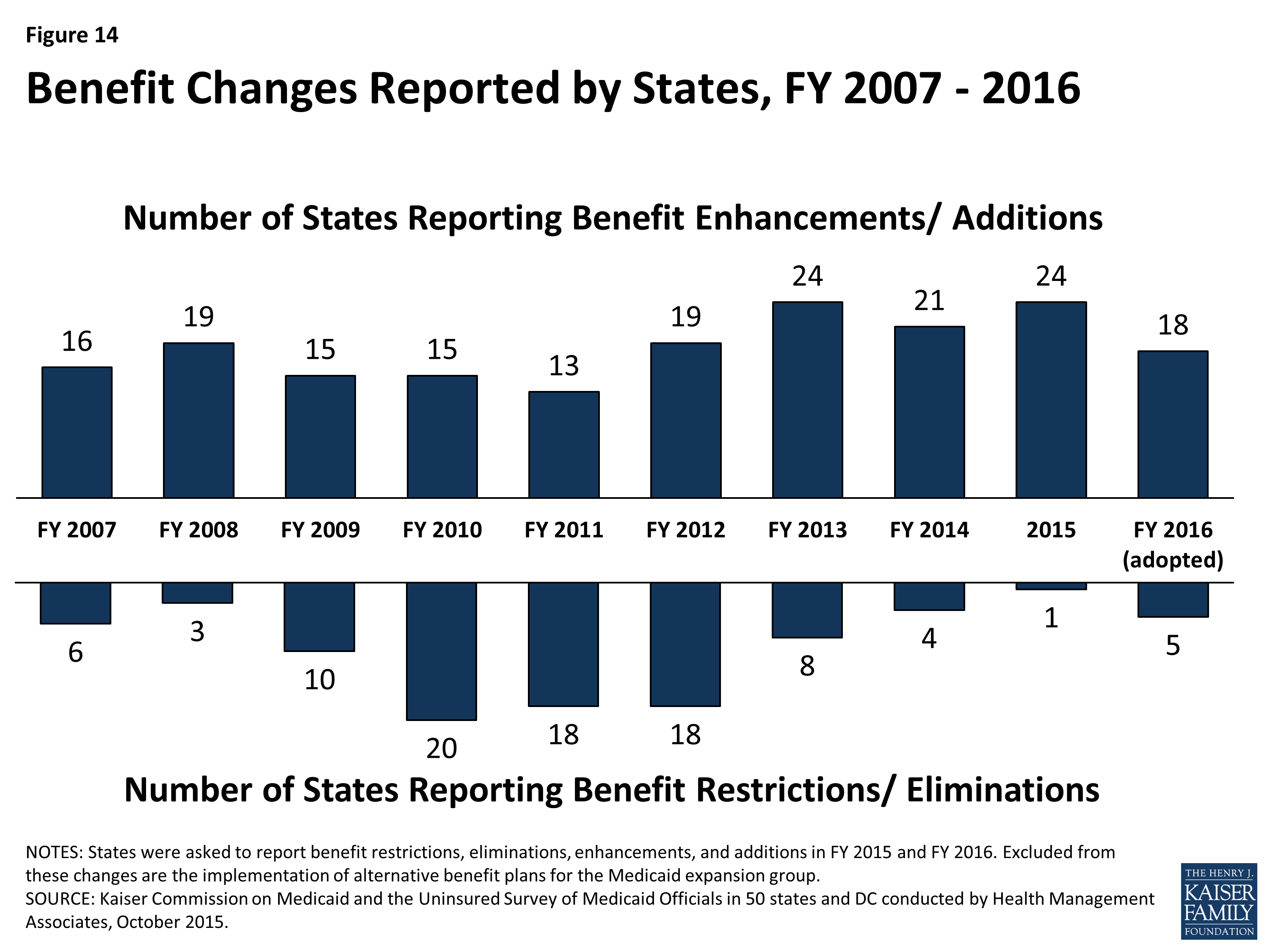

In this year’s survey, the number of states reporting benefit cuts or restrictions – one in FY 2015 and five in FY 2016 – remains far below the number seen during the economic downturn. (Figure 14) A far larger number of states, 24 states in FY 2015 and 18 in FY 2016, reported enhancing or adding new benefits.

Figure 14: Benefit Changes Reported by States, FY 2007 – 2016

One of the most common benefit enhancements or additions reported was for behavioral health and substance abuse services. For example, Ohio is redesigning its behavioral health benefits to include coverage of additional services such as Assertive Community Treatment and Intensive Home Based Treatment. Other common benefit enhancements reported include home and community-based services including changes to 1915(c) waivers, new 1915(i) HCBS State Plan Option implementations and implementation of the Community First Choice State Plan Option. Also common were enhancements to dental services and telemedicine and tele-monitoring. (Table 18)

| Table 18: Benefit Enhancements or Additions | ||

| Benefit | FY 2015 | FY 2016 |

| Behavioral Health | CT, DE, IN, MD, MO, NH, SC, VA, WY | DC, MD, NY, OH, SC, TX, VT, WY |

| HCBS | CA, CT, DC, DE, MA, ND, NJ, NY, TX, WI | CA, CT, DC, DE, GA, MS, WA |

| Dental Services | CO, IL, MA, SC, VA | MO, OR |

| Telemedicine / Tele-monitoring | MD, VT | NE, VT |

For its Medicaid expansion population, Pennsylvania reported replacing its Healthy PA waiver benefits plan (that included a number of physical and behavioral health service limits) with its traditional Medicaid benefit plan resulting in the elimination of those limits in FY 2015. Also, California is planning a notable benefit expansion for pregnant women in FY 2016; the state is planning to provide the full Medicaid benefit package to pregnant women up to 138 percent FPL in place of the current, more limited pregnancy-related benefit package.

Benefit restrictions reflect the elimination of a covered benefit or the application of utilization controls for existing benefits. In FY 2015, Arkansas imposed limits to non-emergency transportation for non-medically frail adults. For FY 2016, four states reported narrowly targeted benefit eliminations (Connecticut, New York, Oklahoma and Vermont) and one state (West Virginia) reported plans to apply a number of service limitations in its home and community-based services waiver serving persons with Intellectual and Developmental Disabilities to enable the waiver to operate within its budget while also serving more people on the waiting list.

| Autism Services |

| On July 7, 2014, CMS issued an Informational Bulletin6 describing approaches and Medicaid authorities available to cover Autism Spectrum Disorder (ASD) services. The bulletin also clarified state obligations under the Early and Periodic Screening, Diagnostic and Treatment (EPSDT) benefit to cover all medically necessary services for children, including ASD services. In this year’s survey, two states in FY 2015 and eight states in FY 2016 reported adding coverage for ASD services. These policy changes have not been counted as positive or negative as they were required changes. |

Table 19: Benefit Changes in the 50 States and DC, FY 2015 and 2016

|

Benefit Changes |

||||

|

STATES |

FY 2015 |

FY 2016 |

||

|

Enhancements/ Additions |

Restrictions/ Eliminations |

Enhancements/ Additions |

Restrictions/ Eliminations |

|

|

Alabama |

||||

|

Alaska |

||||

|

Arizona |

X |

X |

||

|

Arkansas |

X |

|||

|

California |

X |

X |

||

|

Colorado |

X |

|||

|

Connecticut |

X |

X |

X |

|

|

Delaware |

X |

X |

||

|

DC |

X |

X |

||

|

Florida |

||||

|

Georgia |

X |

|||

|

Hawaii |

||||

|

Idaho |

||||

|

Illinois |

X |

|||

|

Indiana |

X |

|||

|

Iowa |

||||

|

Kansas |

||||

|

Kentucky |

||||

|

Louisiana |

||||

|

Maine |

||||

|

Maryland |

X |

X |

||

|

Massachusetts |

X |

|||

|

Michigan |

||||

|

Minnesota |

X |

|||

|

Mississippi |

X |

X |

||

|

Missouri |

X |

X |

||

|

Montana |

||||

|

Nebraska |

X |

|||

|

Nevada |

||||

|

New Hampshire |

X |

|||

|

New Jersey |

X |

|||

|

New Mexico |

||||

|

New York |

X |

X |

X |

|

|

North Carolina |

||||

|

North Dakota |

X |

|||

|

Ohio |

X |

|||

|

Oklahoma |

X |

|||

|

Oregon |

X |

|||

|

Pennsylvania |

X |

|||

|

Rhode Island |

||||

|

South Carolina |

X |

X |

||

|

South Dakota |

||||

|

Tennessee |

||||

|

Texas |

X |

X |

||

|

Utah |

||||

|

Vermont |

X |

X |

X |

|

|

Virginia |

X |

|||

|

Washington |

X |

|||

|

West Virginia |

X |

|||

|

Wisconsin |

X |

|||

|

Wyoming |

X |

X |

||

|

Totals |

24 |

1 |

18 |

5 |

|

NOTES: States were asked to report benefit restrictions, eliminations, enhancements, and additions in FY 2015 and FY 2016. Excluded from these changes are the implementation of alternative benefit plans for the Medicaid expansion group. SOURCE: Kaiser Commission on Medicaid and the Uninsured Survey of Medicaid Officials in 50 states and DC conducted by Health Management Associates, October 2015. |

||||

Table 20: Benefit Actions Taken in all 50 States and DC, FY 2015 and 2016*

|

State |

Fiscal Year |

Benefit Changes |

|

Alabama |

2015 |

|

|

2016 |

||

|

Alaska |

2015 |

|

|

2016 |

||

|

Arizona |

2015 |

Adults (+) Eliminated 25-day inpatient hospital limit. (October 1, 2014) |

|

2016 |

Adults (+): Restoring coverage for orthotics. (August 1, 2015) |

|

|

Arkansas |

2015 |

Expansion Adults (-): Applied limits to non-emergency medical transportation benefits for non-medically frail expansion adults. (February 1, 2015) |

|

2016 |

Aged & Disabled (nc): Combining the ElderChoices 1915(c) and the Adults with Physical Disabilities 1915(c) waivers into a new 1915(c) waiver which ensures all benefits of both waivers to both groups. (January 1, 2016) |

|

|

California |

2015 |

Children (nc): Added coverage for Behavioral Health Treatment for children with autism spectrum disorder to meet federal requirements. (September 2014) Aged & Disabled (+): Partially restored FY 2014 in-home supportive services hour reduction. (July 1, 2014) |

|

2016 |

Aged & Disabled (+): Restored remaining FY 2014 in-home supportive services hour reduction. (July 1, 2015) Pregnant Women (+): Expansion to full-scope coverage to pregnant women 60-133% FPL. (Upon CMS approval) |

|

|

Colorado |

2015 |

Adults (+): Completed adding adult dental coverage. (July 1, 2014) |

|

2016 |

Children (nc): Increased expenditure cap as part of Autism Waiver expansion. (July 1, 2015) |

|

|

Connecticut |

2015 |

Adults (+): Expanded coverage for licensed behavioral health clinician services provided by independent practitioners (licensed psychologists, licensed clinical social workers, licensed marital and family therapists, licensed alcohol and drug counselors, and licensed professional counselors). (July 1, 2014) Aged & Disabled (+): Implemented new HCBS services under 1915(i) authority for Medicaid eligible elders who do not meet nursing home level of care. |

|

2016 |

Adults (+): Added coverage of select over the counter drugs. (July 1, 2015) Aged & Disabled (+): Implemented the Community First Choice Option. (July 2015) Pregnant Women (+): Added coverage of low dose aspirin. (July 1, 2015) Adults (-): Eliminated coverage of Part D copays for non-institutionalized dual eligible beneficiaries. (July 1, 2015) |

|

|

Delaware |

2015 |

Aged & Disabled (+): Added 1915(i) supported employment services for individuals with disabilities (Pathways Program). (January 1, 2015) |

|

Aged & Disabled (+): Enhancing behavioral health and substance use disorder services through the PROMISE Program. (January 1, 2015) |

||

|

2016 |

Aged & Disabled (+): Planning to implement the Community First Choice Option. |

|

|

District of Columbia |

2015 |

Children (+): Added coverage for school based health services when delivered in nonpublic school settings. (October 1, 2014) |

|

Children (nc): Personal care aide removed from coverage as school-based service. (Oct 2014) |

||

|

All (+): Expanding transplant services. (October 1, 2014) |

||

|

Aged & Disabled (+): Added adult day health services under 1915(i) authority for persons aged 55+ with a chronic medical condition. |

||

|

2016 |

Children (+): Adding reimbursement for adolescent substance abuse treatment. (Jan. 1, 2016) |

|

|

LTSS Adults (+): Amending the IDD and Elderly and Physically Disabled 1915(c) waivers to increase person-centered thinking, planning, and service coordination. Examples are the addition of Individualized Day Programs and Supported Living with Transportation to community activities for people with IDD. Key EPD Waiver amendments include the addition of a new provider type suitable to the delivery of Homemaker and Chore Services and revisions to the Environmental Accessibility Adaptation service that will make services more accessible. |

||

|

Florida |

2015 |

|

|

2016 |

||

|

Georgia |

2015 |

|

|

2016 |

Adults (+): Added coverage for medically necessary emergency transportation by rotary wing air ambulance. (July 1, 2015) LTSS Adults (+): Added hourly skilled nursing to Independent Care Waiver Program. (July 1, 2015) |

|

|

Hawaii |

2015 |

|

|

2016 |

||

|

Idaho |

2015 |

|

|

2016 |

||

|

Illinois |

2015 |

Adults (+): Restored coverage for adult dental services. (July 1, 2014) |

|

Adults (+): Restored coverage for adult podiatry services. (October 1, 2014) |

||

|

2016 |

||

|

Indiana |

2015 |

Aged & Disabled (+): Added habilitation services for adults with serious mental illness under 1915(i) authority. |

|

2016 |

Children (nc): Adding coverage for Applied Behavioral Analysis services for children with autism spectrum disorder to meet federal requirements. (October 1, 2015) |

|

|

Iowa |

2015 |

|

|

2016 |

||

|

Kansas |

2015 |

|

|

2016 |

||

|

Kentucky |

2015 |

|

|

2016 |

Aged & Disabled (nc): Modifying and adding new HCBS waiver services to better align beneficiary needs with services available and to comply with new HCBS federal requirements. |

|

|

Louisiana |

2015 |

|

|

2016 |

||

|

Maine |

2015 |

|

|

2016 |

||

|

Maryland |

2015 |

All (+): Expanded telemedicine services from rural to urban areas. (October 1, 2014) |

|

All (+): Added coverage for certain Substance Use Disorder services. (January 1, 2015) |

||

|

2016 |

All (+): Added Physician Assistants as a new provider type. (July 1, 2015) Children (+): Plan to implement services under 1915(i) authority for children and youth with serious emotional disturbances and serious and persistent mental illness. |

|

|

Massachusetts |

2015 |

Adults (+): Added coverage for treatment of gender dysphoria. Adults (+): Restored coverage for dentures. (May 15, 2015) Aged & Disabled (+): Added a shared living benefit to the TBI 1915(c) waiver. |

|

2016 |

||

|

Michigan |

2015 |

|

|

2016 |

||

|

Minnesota |

2015 |

Pregnant Women (+): Adding coverage for services provided by certified doulas. (July 1, 2014) |

|

2016 |

Children (nc): Added coverage for treatment of autism spectrum disorder to meet federal requirements. (July 1, 2015) Aged & Disabled (nc): Plan to convert the personal care assistance benefit to the Community First Choice Option under 1915(i) and Section 1115 waiver authority. (Upon CMS approval) |

|

|

Mississippi |

2015 |

Aged & Disabled Children (+): Added coverage for Prescribed Pediatric Extended Care Centers (a new provider type). (July 1, 2014) |

|

2016 |

Aged & Disabled (+): Plan to implement HCBS services under 1915(i) authority for persons with intellectual and developmental disabilities. |

|

|

Missouri |

2015 |

All (+): Added coverage for SBIRT (Screening, Brief Intervention, Referral and Treatment) and HBAI (Health Behavior Assessment and Intervention services). (January 2015) |

|

2016 |

Children (+): Adding coverage for asthma education and environmental assessment services. (Upon CMS approval) Adults (+): Restoring coverage for preventive dental services and fillings. (January 2016) |

|

|

Montana |

2015 |

|

|

2016 |

||

|

Nebraska |

2015 |

|

|

2016 |

All (+): Adding coverage for telehealth and tele-monitoring services. (January 2016). Children (nc): Adding coverage for intensive behavioral intervention services for treatment of autism spectrum disorder to meet federal requirements. |

|

|

Nevada |

2015 |

|

|

2016 |

||

|

New Hampshire |

2015 |

All (+): Removed service limits on psychotherapy, X-ray and outpatient hospital (to harmonize with Alternative Benefit Plan for the expansion population). Expansion Adults (+): Added coverage for chiropractic and Substance Use Disorder services. (August 15, 2014) |

|

2016 |

||

|

New Jersey |

2015 |

Aged & Disabled (+): Implemented managed long-term services and supports and consolidating 1915(c) waivers into state’s Section 1115 which provides LTSS beneficiaries with a greater array of LTSS services. (July 1, 2014) |

|

2016 |

||

|

New Mexico |

2015 |

Pregnant Women (nc): Added coverage for birthing centers to meet federal requirements. (December 1, 2014) Children (nc): Added coverage for treatment of autism spectrum disorder to meet federal requirements. (July 1, 2015) |

|

2016 |

||

|

New York |

2015 |

Aged & Disabled (+): Implemented the Community First Choice Option. (SPA still pending; plan to implement retroactively.7) |

|

2016 |

All (-): Discontinued coverage for viscosupplementation of the knee for an enrollee with a diagnosis of osteoarthritis of the knee. (April 1, 2015 for FFS and July 1, 2015 for managed care) All (+): Expanded smoking cessation counseling providers to include dental practitioners. (April 1, 2015 for FFS and July 1, 2015 for managed care) All (-): Limited coverage of DEXA Scans for Screening to one time every 2 years for Women Over Age 65 and Men Over Age 70. (April 1, 2015 for FFS and July 1, 2015 for managed care) Aged & Disabled (+):Plan to add services for adults with serious mental illness services under 1915(i) authority as part of the state’s Health and Recovery Plans (HARP) managed care program. |

|

|

North Carolina |

2015 |

|

|

2016 |

||

|

North Dakota |

2015 |

Aged & Disabled (+): Added personal care with supervision to the Home and Community Based waiver to allow individuals with a primary diagnosis of dementia or traumatic brain injury to receive 24 hour supervision with a daily rate. (January 2015) |

|

2016 |

||

|

Ohio |

2015 |

|

|

2016 |

Aged & Disabled (+): Planning to implement a redesign of behavioral health benefits to include coverage of additional services for persons with high intensity service and support needs (e.g., Assertive Community Treatment for SPMI adults, Intensive Home Based Treatment for SED children and residential treatment for substance use disorders). (January 1, 2016) |

|

|

Oklahoma |

2015 |

|

|

2016 |

Adults (-): Eliminated coverage for sleep studies. (July 1, 2015) |

|

|

Oregon |

2015 |

|

|

2016 |

Adults (+): Restoring previously cut adult restorative dental benefits (relaxed limitation criteria for dentures; coverage for crowns; scaling and planning). (January 1, 2016) |

|

|

Pennsylvania |

2015 |

Expansion Adults (+): Conformed Alternative Benefit Package (originally implemented on January 1, 2015) to the traditional Medicaid benefit package which resulted in an elimination of service limits on physical and behavioral health services. (April 27, 2015) |

|

2016 |

||

|

Rhode Island |

2015 |

|

|

2016 |

||

|

South Carolina |

2015 |

Dual Eligibles (+): Added inpatient psychiatric coverage. (July 1, 2014) Family Planning Adults (+): Added additional preventive services including diabetes screening, health and behavioral assessments, cholesterol abnormalities and HIV screening. (Aug 2014) Adults (+): Added a preventative adult dental benefit. (December 1, 2014) |

|

2016 |

Children (nc): Added autism spectrum disorder treatment to meet federal requirement. (Oct 2015) Children (+): Expanded coverage for treatment of eating disorders ages 0-21. (October 2015) |

|

|

South Dakota |

2015 |

|

|

2016 |

||

|

Tennessee |

2015 |

|

|

2016 |

||

|

Texas |

2015 |

LTSS Adults (+): Implemented Community First Choice Option (CFCO) services for eligible individuals meeting institutional level of care and delivered through both the FFS and managed care delivery systems. (September 1, 2014) MLTSS Adults (+): Added supported employment and employment assistance to the HCBS waiver service array in the STAR+PLUS program. (September 1, 2014) Aged & Disabled (nc): Allowed providers other than Local Mental Health Authorities (LMHAs) to provide Mental Health Targeted Case Management and Mental Health Rehabilitative services already available through STAR Health. (September 1, 2014) |

|

2016 |

Aged & Disabled (+): Implementing an array of HCBS designed to support long-term recovery from mental illness for SMI adults who are former long-term residents of inpatient facilities under a 1915(i) SPA. (Upon CMS approval) |

|

|

Utah |

2015 |

|

|

2016 |

Children (nc): Added autism spectrum disorder treatment to meet federal requirement. (July 2015) |

|

|

Vermont |

2015 |

All (+): Added a tele-monitoring benefit. (August 1, 2014) |

|

2016 |

Aged & Disabled (-): Eliminating Enhanced Residential Care and Adult Family Care Case Management. All (+): Adding coverage for Licensed Alcohol and Drug Counselors. (October 2015) All (+): Adding coverage for primary care telemedicine outside of a facility. (October 1, 2015) Children (nc): Added coverage for Applied Behavior Analysis for treatment of autism spectrum disorder to meet federal requirements. (July 1, 2015) |

|

|

Virginia |

2015 |

Aged & Disabled (+): Added nutrition counseling and inpatient substance abuse services for Medicaid Works (working disabled eligibility group). (July 1, 2014) |

|

Pregnant Women (+): Expanded comprehensive dental benefits to pregnant women. (March 2015) |

||

|

2016 |

||

|

Washington |

2015 |

|

|

2016 |

LTSS Adults (+): Adding skills acquisition training and assistive technology under Community First Choice (CFC) for persons meeting nursing facility level of care. (Upon CMS approval) All (+): Added coverage for gender reassignment surgery. (August 6, 2015) |

|

|

West Virginia |

2015 |

|

|

2016 |

Aged & Disabled (-): Amending IDD HCBS waiver (as part of five year renewal) to impose service limitations that will allow waiver to operate within its budget and serve more persons on the waiting list. Service limitations include reductions in respite hours, person centered support services, non-emergency transportation, and other reductions. (Upon CMS approval) |

|

|

Wisconsin |

2015 |

Aged & Disabled (+): Added the following HCBS waiver services for persons meeting nursing facility level of care: Consultative Clinical and Therapeutic Services for Caregivers and Training Services for Unpaid Caregivers. (January 1, 2015) |

|

2016 |

Children (nc): Added State Plan coverage (to replace HCBS waiver coverage) for behavioral health services for treatment of autism spectrum disorder to meet federal requirements. (January 1, 2016) |

|

|

Aged & Disabled (nc): A psychosocial rehabilitation program under 1915(i) along with two other such programs under other Medicaid authorities are being replaced with a single comprehensive psychosocial rehabilitation program under 1905 authority that will cover all the services provided by the prior programs. |

||

|

Wyoming |

2015 |

All (+): Added coverage for additional licensed MH provider types. (July 2014) |

|

2016 |

All (+): Added chiropractic benefit. (July 1, 2015) All (+): Adding coverage for additional provisionally licensed MH provider types. (July 1, 2015) |

|

|

* Benefit enhancements counted in this report are denoted with (+). Benefit restrictions or eliminations counted in this report are denoted with (-). Changes that were not counted as positive or negative in this report, but were mentioned by states in their responses, are denoted with (nc). |

||

Prescription Drug Utilization and Cost Control Initiatives

Just over a decade ago, between 2001 and 2005, the vast majority of states aggressively implemented policies designed to slow the growth in Medicaid spending for prescription drugs. In January 2006, the implementation of the Medicare prescription drug benefit reduced total state Medicaid drug expenditures by almost half, the rate of growth in the cost of prescription drugs abated, and the intense Medicaid focus on pharmacy cost containment began to diminish. Since 2014, however, a combination of rising drug prices and increasing enrollments (as a result of ACA coverage expansions) have refocused state attention on pharmacy reimbursement and coverage policies. In this year’s survey, over two-thirds of the states in FY 2015 and half in FY 2016 reported actions to refine and enhance their pharmacy programs and to react to new and emerging specialty and high-cost drug therapies.

This year’s survey asked states to comment on the most significant factors affecting the trend in total Medicaid pharmacy expenditures (federal and state) between FY 2014 and projected for FY 2016. Responding to this open-ended question, the vast majority of states identified specialty and other high-cost drugs as a significant cost driver including a number of states identifying specific drug classes: hepatitis C antivirals, oncology drugs, cystic fibrosis agents and hemophilia factor. A few states also identified recently approved cholesterol drugs called “PCSK9 inhibitors” as likely cost drivers for FY 2016. In addition to specialty and other high-cost drugs, a number of states identified generic drugs as a significant cost driver, referencing large price increases for existing generics and higher than expected prices for new generics entering the market in addition to inflation and general drug price increases. Increased enrollment was also identified as a factor (including both ACA Medicaid expansion states and non-expansion states). A few states also identified factors that helped to moderate or reduce expenditure growth trends including higher rebates, drugs coming off patent and increased prior authorization and step therapy requirements. A number of states also commented that because pharmacy benefits for many enrollees were delivered under a capitated MCO arrangement, the growth in pharmacy expenditures could not be isolated.

Pharmacy Management Policies in Place and New in FY 2015 and FY 2016

At the start of FY 2015, a total of 45 states indicated that they had already in place a Preferred Drug List (PDL) and were already obtaining supplemental rebates.8 Two states (Arizona and Massachusetts) reported collecting supplemental rebates for the first time during FY 2015; one state (North Dakota) reported plans to adopt a PDL and collect supplemental rebates in FY 2016. The number of states with limits on the number of prescriptions that Medicaid will pay for each month decreased to 14 states in FY 2015, down from 16 states in FY 2014 and 18 states in FY 2013. One state (Pennsylvania) reported eliminating their prescription cap for adults in FY 2015. (Kentucky reported eliminating their monthly prescription limit in January 2014.)

Summary of FY 2015 and FY 2016 Pharmacy Policy Changes and Cost Containment Efforts

Thirty-five states (35) in FY 2015 and 25 states in FY 2016 implemented cost-containment initiatives in the area of prescription drugs, comparable to the number of states taking such actions in FY 2014 (28), FY 2013 (24), and FY 2012 (33). As PDL and related supplemental rebate programs have matured in most states and as more states have carved the pharmacy benefit into capitated managed care arrangements, the number of states reporting PDL or supplemental rebate changes (e.g., adding new PDL drug classes or joining a multi-state rebate pool) has dropped significantly (three states planning changes to PDL and five states planning changes to supplemental rebates in FY 2016) compared to 24 and 28 states in FY 2009. A small number of states reported reductions in ingredient cost reimbursement (5 states in FY 2015 and 6 states in FY 2016) often associated with adopting an actual acquisition cost methodology (discussed below), and a small number reported dispensing fee reductions (4 states in FY 2015 and 1 state in FY 2016). No state reported imposing new limits on the number of monthly prescriptions in either FY 2015 or FY 2016. The most significant restriction reported related to applying clinical management protocols for specialty/high-cost drugs.

| Medicaid Covered Outpatient Drug Rule |

| State Medicaid programs reimburse pharmacies for the “ingredient cost” of each prescription using an Estimated Acquisition Cost (EAC), plus a dispensing fee.9 A proposed rule released in February 2012,10 replaces the term EAC with the term “Actual Acquisition Cost” (AAC) and also requires states to align their dispensing fees to be consistent with their ingredient cost reimbursement. States can define their own AAC prices or use the pricing files published and updated weekly by CMS – the “National Average Drug Acquisition Costs” (NADACs) – which are derived from outpatient drug acquisition cost surveys of retail community pharmacies.11 Some states have already transitioned to an AAC methodology. In this year’s survey, one state in FY 2015 (Alaska) and five states in FY 2016 (Maryland, Nevada, North Carolina, Texas and Virginia) reported adopting, or plans to adopt, an AAC (e.g., NADAC) ingredient cost methodology. A number of other states reported that they were holding off making any changes to their pharmacy reimbursement methodologies until the proposed rule is finalized which is expected to occur in late CY 2015.12 |

High-Cost Specialty Drugs

While there is no universally accepted definition of specialty drugs and Medicaid programs use varying definitions, products designated as specialty drugs tend to require either difficult or unusual medication delivery, or complex treatment maintenance. Price is also frequently considered an indicator of specialty drugs.13 According to pharmacy benefit manager, Express Scripts, overall U.S. drug spending increased by 13.1 percent in 2014 driven by a 30.9 percent increase in spending on specialty drugs, the highest specialty drug trend ever reported.14 Specialty drugs also grew as a share of total drug spending from 27.7 percent in 2013 to 31.8 percent in 2014 and are expected to reach 44 percent in the next three years with annual increases of 21 – 22 percent.15 Much of the 2014 growth was driven by the launch of three new hepatitis C treatments – Sovaldi, Olysio and Harvoni. As noted above, however, other new and emerging specialty drugs for cancer, cystic fibrosis, cholesterol management and other conditions are, or are expected to become, significant cost drivers.

In this year’s survey, states were asked to comment on whether their state had adopted or planned to adopt coverage, reimbursement or managed care policies targeting specialty or high-cost drugs in FYs 2015 or 2016.

- Nineteen (19) states reported implementing new clinical prior authorization requirements and 11 states indicated that they were standardizing clinical criteria across both fee-for-service and managed care;

- Four states (Connecticut, DC, Idaho and South Carolina) reported negotiating lower prices for certain drugs or more aggressive supplemental rebates;

- Two states (Tennessee, Texas) reported reimbursement changes that effectively lower specialty drug prices;

- One state (New York) reported plans to implement a specialty pharmacy program, and

- One state (Wyoming) reported adding case managements with high drug costs and plans to implement a medication therapy program.

In contrast, in FY 2016, two states (California and Connecticut) reported plans to liberalize their previously more restrictive prior authorization polices for hepatitis C drugs, making them more widely available.

Several states also reported other managed care policies specifically related to reimbursement of hepatitis C drugs in FY 2015: California and Florida pay “kick” payments to MCOs, Kansas pays a “case rate,” and Maryland makes supplemental payments to MCOs that follow the state’s hepatitis C clinical guidelines. New Mexico reported using risk corridors and Rhode Island reported stop-loss payments, and five states (DC, New Hampshire, South Carolina, Texas and Washington) reported carving these drugs out of the capitation payment. In some cases, these policies were reported as “temporary” to allow the state time to collect enough utilization data so that the cost of these drugs could be included in future capitation rates. Oregon also expressed the concern that the coverage of specialty and high-cost drugs could put its Section 1115 Demonstration Waiver budget neutrality ceiling at risk.

Other Pharmacy Policy Changes

Other pharmacy actions counted as cost containment measures for FY 2015 and FY 2016 included: Medication Therapy Management programs including efforts to better manage opiates and behavioral health drugs (Indiana, Massachusetts, North Carolina, North Dakota, Washington and Wyoming), new or expanded 340B programs (Arizona and Oklahoma), a common formulary across FFS and MCOs (Michigan and Mississippi), hemophilia management program (Arkansas), restructured physician administered drug program (Kentucky), expanded step therapy or prior authorization programs (Louisiana), new enrollee lock-in program (North Carolina), reductions in over-the-counter (OTC) coverage for cough and cold medications for children (New Mexico), management of compound prescriptions and limits on Buprenorphine – a medication used to treat opioid addiction (Tennessee).

In addition, several states reported other pharmacy-related actions that were not included in the count of cost containment actions. Connecticut is allowing non-controlled prescriptions to remain valid for a full year (rather than six months) and is also implementing select OTC coverage for adults. DC, New York, Ohio and Vermont are awarding new administrative contracts for pharmacy benefit management and related services. Delaware, Indiana and Iowa are transitioning the pharmacy benefit to MCOs and Kansas is moving select vaccines to the pharmacy benefit under managed care. New York plans to carve in hemophilia factor products and injectable antipsychotic drugs into managed care contracts in FY 2016. Maryland carved-out substance use disorder drugs from managed care. Michigan is allowing behavioral health and other select physician injectables to be billed under the pharmacy benefit. Nebraska implemented Indian Health Service pharmacy reimbursement at an encounter rate. Texas is requiring MCO prior authorization policies to be reviewed and approved by its Drug Utilization Review Board.

Finally, a few states reported pharmacy-related expansions or reversals of previous pharmacy cost containment actions. Three states increased dispensing fees in FY 2015 (Alaska, Iowa and Montana) and six states planned to increase dispensing fees in FY 2016 (Maryland, Montana, Nevada, North Carolina, Texas and Virginia). In six of these states (Alaska, Maryland, Nevada, North Carolina, Texas and Virginia), dispensing fee increases were expected to partially offset reimbursement decreases resulting from the adoption of the AAC/NADAC ingredient cost reimbursement methodology. In addition to expansions or reversals of cost containment noted previously (Pennsylvania eliminated its monthly prescription cap for adults; California and Connecticut reported plans to liberalize their prior authorization policies for hepatitis C drugs) Illinois reported exempting antipsychotic medications from its monthly prescription cap, as well as exempting children with complex medical needs enrolled in a care coordination entity from its monthly prescription cap requirements.

Table 21: Pharmacy Cost Containment Actions Taken in all 50 States and DC, FY 2015 and 2016

|

States |

Reduce Dispensing Fee |

Reduce Ingredient Costs |

Preferred Drug List Changes |

Supplemental Rebate Changes |

Specialty Rx Actions |

Other Pharmacy Actions |

Total Pharmacy Actions Taken |

|||||||

|

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

2015 |

2016 |

|

|

Alabama |

||||||||||||||

|

Alaska |

X |

X |

||||||||||||

|

Arizona |

X |

X |

X |

X |

X |

|||||||||

|

Arkansas |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

California |

X |

X |

||||||||||||

|

Colorado |

||||||||||||||

|

Connecticut |

X |

X |

X |

X |

X |

X |

X |

X |

X |

|||||

|

Delaware |

||||||||||||||

|

DC |

X |

X |

X |

X |

||||||||||

|

Florida |

X |

X |

||||||||||||

|

Georgia |

||||||||||||||

|

Hawaii |

X |

X |

||||||||||||

|

Idaho |

X |

X |

X |

|||||||||||

|

Illinois |

X |

X |

X |

X |

X |

|||||||||

|

Indiana |

X |

X |

X |

X |

X |

X |

||||||||

|

Iowa |

||||||||||||||

|

Kansas |

||||||||||||||

|

Kentucky |

X |

X |

||||||||||||

|

Louisiana |

X |

X |

X |

X |

X |

X |

||||||||

|

Maine |

X |

X |

||||||||||||

|

Maryland |

X |

X |

X |

X |

||||||||||

|

Massachusetts |

X |

X |

X |

X |

X |

|||||||||

|

Michigan |

X |

X |

||||||||||||

|

Minnesota |

||||||||||||||

|

Mississippi |

X |

X |

X |

X |

X |

|||||||||

|

Missouri |

||||||||||||||

|

Montana |

X |

X |

X |

|||||||||||

|

Nebraska |

X |

X |

X |

X |

||||||||||

|

Nevada |

X |

X |

X |

X |

X |

|||||||||

|

New Hampshire |

X |

X |

||||||||||||

|

New Jersey |

||||||||||||||

|

New Mexico |

X |

X |

X |

X |

||||||||||

|

New York |

X |

X |

X |

X |

X |

|||||||||

|

North Carolina |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

North Dakota |

X |

X |

X |

X |

X |

|||||||||

|

Ohio |

||||||||||||||

|

Oklahoma |

X |

X |

X |

|||||||||||

|

Oregon |

X |

X |

X |

X |

X |

|||||||||

|

Pennsylvania |

X |

X |

||||||||||||

|

Rhode Island |

X |

X |

X |

X |

||||||||||

|

South Carolina |

X |

X |

||||||||||||

|

South Dakota |

||||||||||||||

|

Tennessee |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Texas |

X |

X |

X |

X |

X |

X |

X |

|||||||

|

Utah |

||||||||||||||

|

Vermont |

||||||||||||||

|

Virginia |

X |

X |

X |

X |

||||||||||

|

Washington |

X |

X |

X |

X |

||||||||||

|

West Virginia |

||||||||||||||

|

Wisconsin |

X |

X |

||||||||||||

|

Wyoming |

X |

X |

X |

X |

||||||||||

|

Totals |

4 |

1 |

5 |

6 |

6 |

3 |

6 |

5 |

26 |

13 |

6 |

11 |

35 |

25 |

|

SOURCE: Kaiser Commission on Medicaid and the Uninsured Survey of Medicaid Officials in 50 states and DC conducted by Health Management Associates, October 2015. |

||||||||||||||