Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries

Health insurance through Medicare provides important financial protections for 67 million Americans. However, people with Medicare can face substantial cost-sharing requirements for Medicare-covered services, and unlike most health insurance policies, Medicare has no limit on out-of-pocket spending. Many Medicare beneficiaries have modest incomes and little savings to draw on to pay for expensive medical care, and medical debt is a concern for more than one in five (22%) older adults. In light of these facts, the Medicare supplement insurance market, also known as Medigap, plays a key role in helping beneficiaries afford medical care by limiting their exposure to catastrophic out-of-pocket medical costs.

This brief presents facts about Medigap, including the characteristics of Medicare beneficiaries with a Medigap policy, variation in Medigap enrollment by state, and Medigap premiums. This analysis is based on data from the National Association of Insurance Commissioners (NAIC) compiled by Mark Farrah Associates (MFA), through the end of 2023 (the most recent year of annual data) and the Centers for Medicare & Medicaid Services (CMS) Medicare Current Beneficiary Survey 2022 Survey File data. See methods for more information. A companion brief Medigap May Be Elusive for Medicare Beneficiaries with Pre-Existing Conditions analyzes federal and state guaranteed issue rules and how they impact beneficiaries’ access to Medigap.

Key Takeaways

- In 2022, 12.5 million, or four in 10 (42%) people in traditional Medicare had a Medigap policy. Compared to all traditional Medicare beneficiaries in 2022, traditional Medicare beneficiaries with a Medigap policy are more likely to be White, have higher incomes, and report better health. Among traditional Medicare beneficiaries, a smaller share of beneficiaries under age 65 with disabilities have a Medigap policy compared to beneficiaries ages 65 and older (7% vs 46%), due in part to a lack of Medigap guaranteed issue protections under federal law for those under age 65.

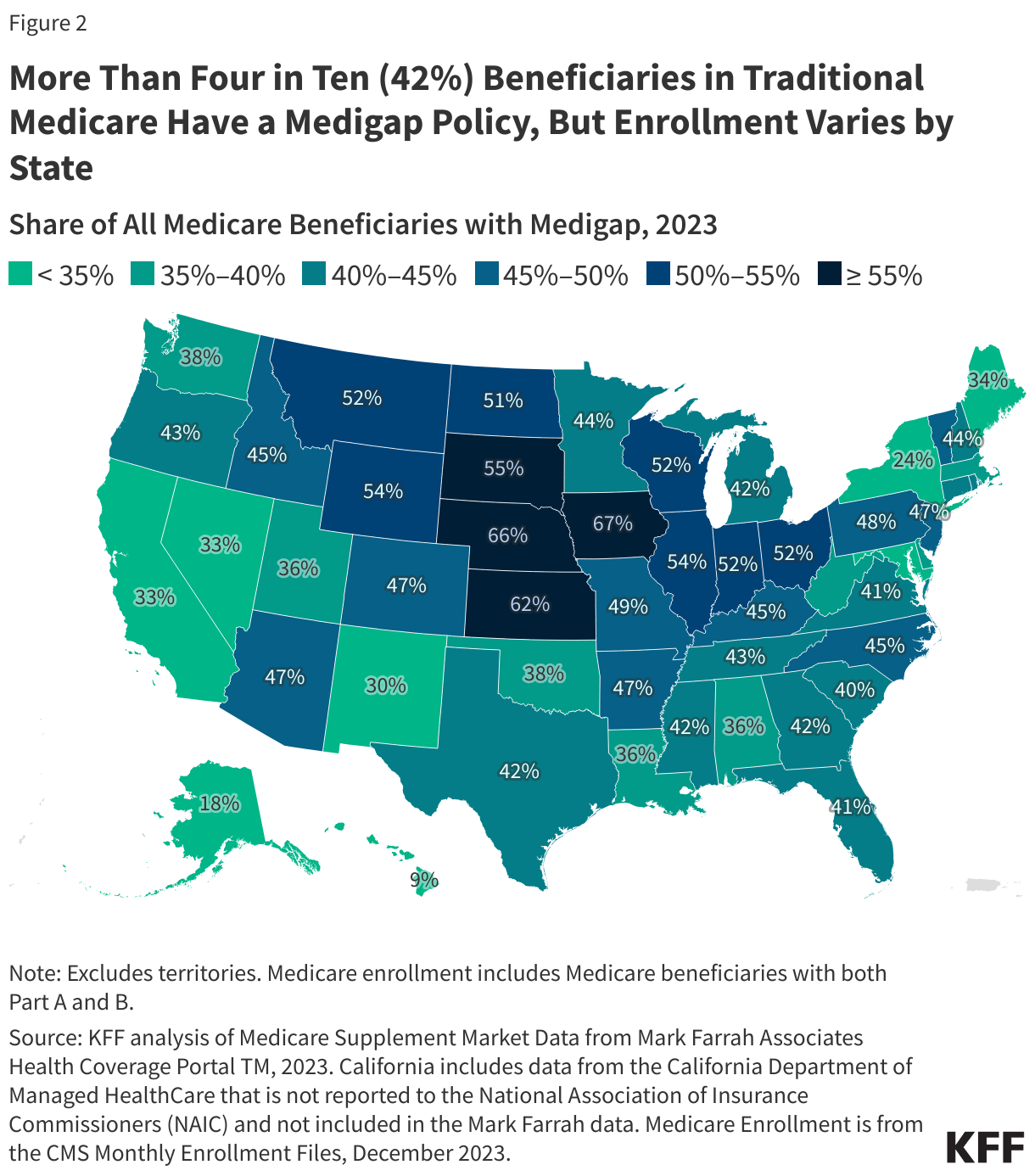

- The share of traditional Medicare beneficiaries with Medigap varies by state, ranging from 9% in Hawaii to 67% in Iowa. States with higher Medigap enrollment tend to be in the Midwest and plains states, where relatively fewer beneficiaries are enrolled in Medicare Advantage plans.

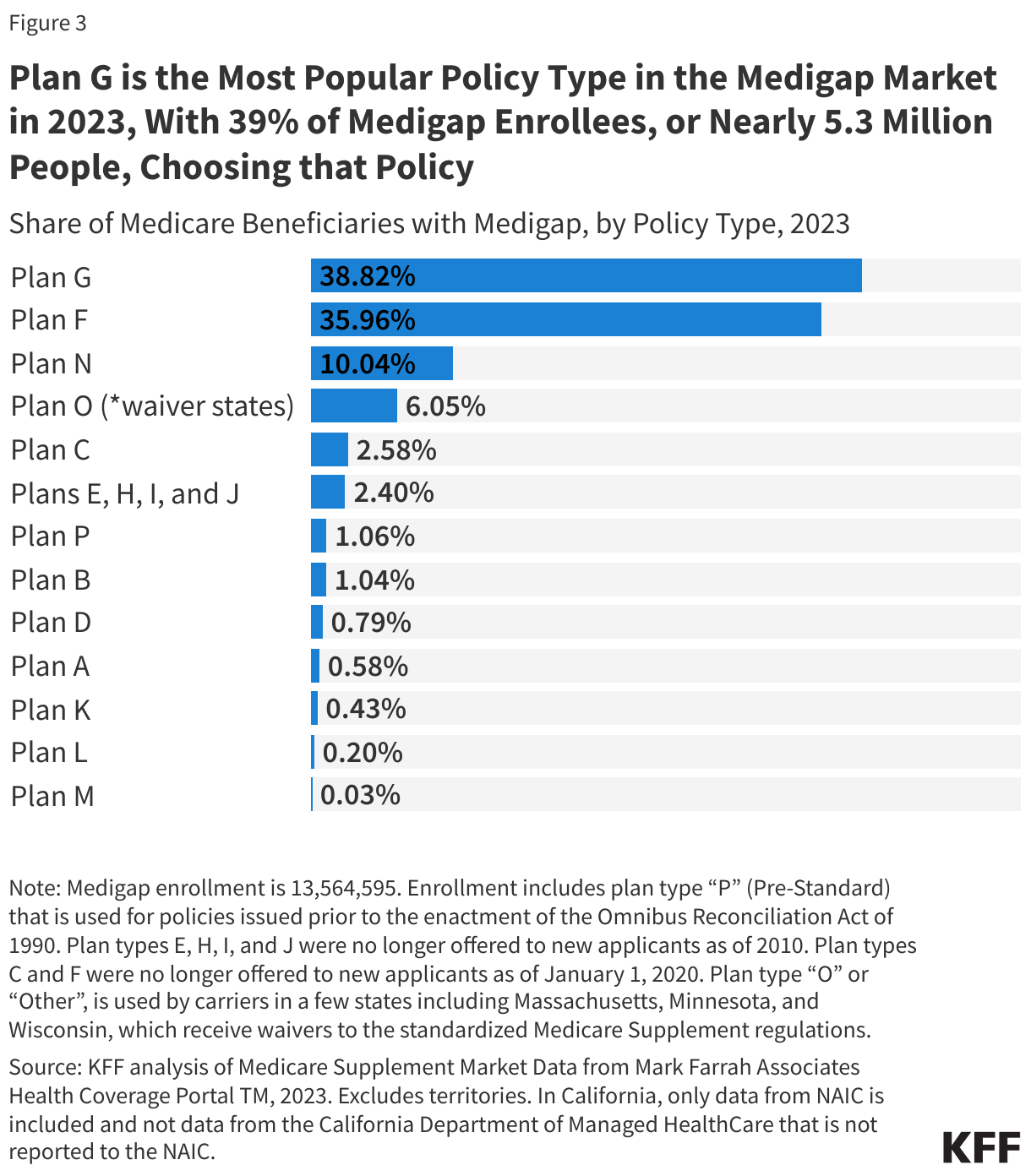

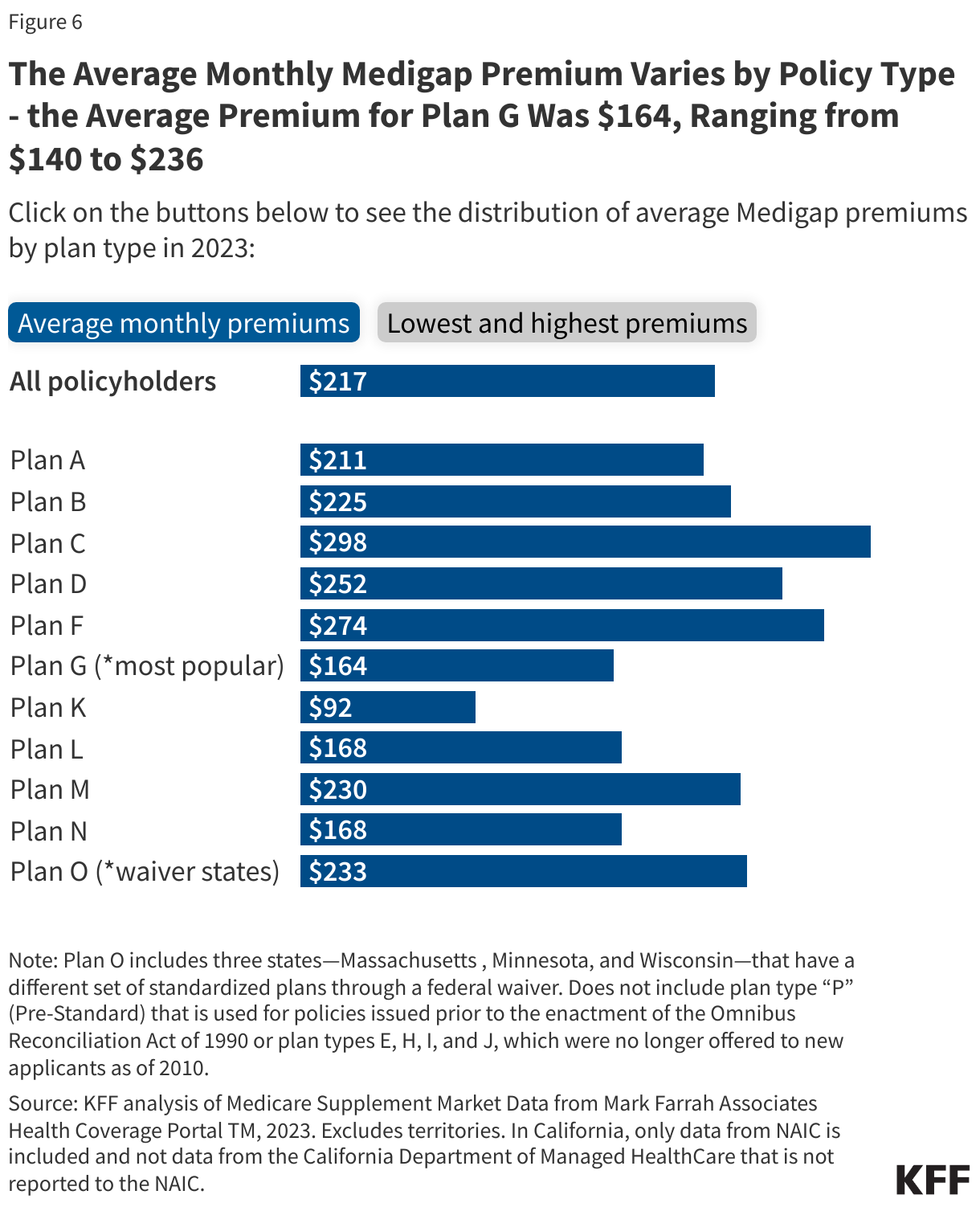

- Medigap Plan G, which is the most comprehensive Medigap policy available to new policyholders, was the most popular plan type in 2023, accounting for 39% of all policyholders, or nearly 5.3 million people. Part F, which has the same benefits as Plan G but also covers the Part B deductible, has the second largest share of Medigap policyholders in 2023 (36% or nearly 4.9 million people), although it has not been available to new beneficiaries since 2020.

- The average monthly premium among current Medigap policyholders was $217 in 2023, or $2,604 for a full year of coverage, according to KFF analysis of NAIC data from MFA.

- Medigap premiums vary by state and by policy type. For example, in 2023, the average monthly premium for people enrolled in Plan G was $164 ($1,968 for 12 months), but this varied from a low of around $140 in D.C., Hawaii, and New Mexico to $236 in New York.

Overview of Medigap

Medicare beneficiaries can choose to get their Medicare Part A and B benefits through the traditional Medicare program or a Medicare Advantage plan, such as a Medicare HMO or PPO. Among the nearly 60 million people enrolled in Medicare Part A and B in 2022, half (50%) of Medicare beneficiaries were in traditional Medicare. Most traditional Medicare beneficiaries had some form of additional coverage that helps to cover the cost-sharing requirements under the benefit design of traditional Medicare, such as Medigap, employer-sponsored retiree benefits, or Medicaid.

Medigap is private supplemental health insurance that helps cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. Medigap is a key source of supplemental insurance for people in traditional Medicare without employer-sponsored retiree benefits or Medicaid (Medigap does not work with Medicare Advantage). In 2022, 12.5 million Medicare beneficiaries, or 42% of all traditional Medicare beneficiaries, had a Medigap policy.

By helping to cover Medicare’s cost-sharing requirements, Medigap insurance limits the financial exposure of Medicare beneficiaries and provides protection against catastrophic expenses for Medicare-covered services. Medigap policies also make health care costs more predictable by spreading costs over the course of the year through monthly premium payments and reduce the paperwork burden for beneficiaries associated with medical bills. According to KFF analysis, traditional Medicare beneficiaries with Medigap are less likely to report cost-related problems than similar Medicare Advantage enrollees or traditional Medicare beneficiaries without supplemental coverage.

Characteristics of People with Medigap

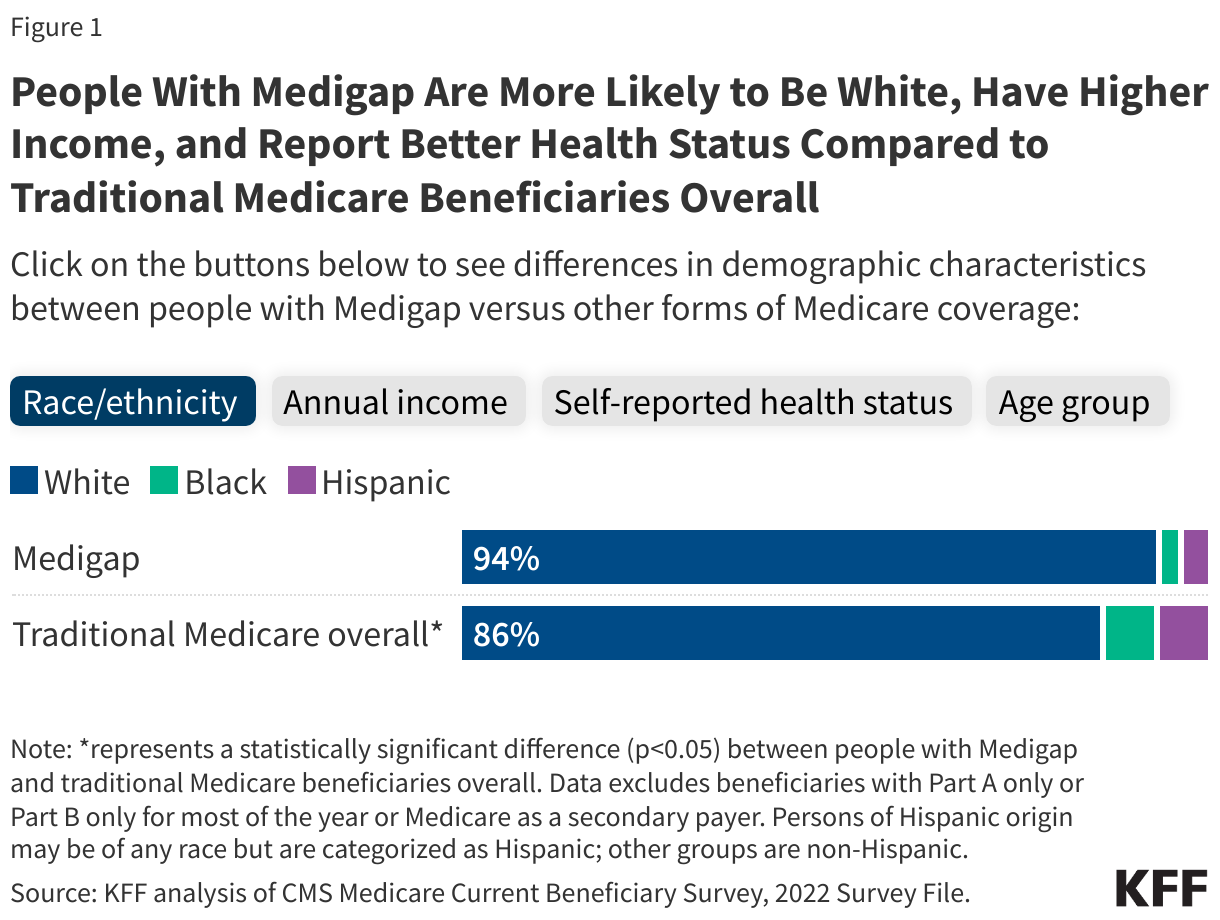

A larger share of traditional Medicare beneficiaries with Medigap than traditional Medicare beneficiaries overall are White (94% vs 86%), have incomes of $40,000 or above (54% versus 47%), and report their health as excellent, very good, or good (88% versus 82%) (Figure 1; See Appendix Table 1 for a comparison of Medigap enrollee characteristics to beneficiaries with other types of coverage).

Medicare beneficiaries with pre-existing medical conditions or who are under age 65 and qualify for Medicare based on having a long-term disability may have difficulty purchasing a Medigap policy. Federal law offers a one-time, six-month Medigap open enrollment period for beneficiaries ages 65 and older when they age on to Medicare, but federal and state laws place very limited restrictions on the practice of medical underwriting outside of this initial open enrollment period. Moreover, the guaranteed issue right under federal law does not extend to Medicare beneficiaries under age 65 who qualify for Medicare on the basis of having a long-term disability. This is one reason why a much smaller share of traditional Medicare beneficiaries under age 65 and older have a Medigap policy compared with people age 65 and older (7% versus 46%). In addition, people under age 65 are more likely to have no supplemental coverage compared to people 65 and older (17% vs. 10%) and more likely to qualify for Medicaid (65% vs. 10%). While most states (36 states) go beyond federal law and require Medigap insurers to offer at least one policy to people under age 65 during an initial open enrollment period, premiums in these states vary and may be higher for people under age 65 (see section below Premium Rules Vary Across States That Require Insurers to Offer at Least One Medigap Policy Type to People Under Age 65 for more details).

Additionally, Medigap premiums can be costly (as discussed in more detail below), making it more difficult for people with lower incomes to afford a Medigap policy. This, along with relatively high supplemental coverage under Medicaid, could be a factor in lower enrollment of Black and Hispanic Medicare beneficiaries in Medigap relative to Medicare Advantage, since Black and Hispanic beneficiaries have lower income and assets compared to White beneficiaries. Black and Hispanic beneficiaries are also more likely to report relatively poor health and have higher prevalence rates of certain chronic conditions that would be classified as pre-existing conditions by Medigap insurers, which could also make it difficult for individuals in these groups to obtain Medigap, particularly outside of guaranteed issue periods when medical underwriting is not allowed.

Medigap Enrollment Varies by State

Medigap enrollment varies widely by state: from 9% of traditional Medicare beneficiaries in Hawaii to 67% in Iowa, based on KFF analysis of 2023 NAIC data (Figure 2, Appendix Table 2). In eleven states, more than 50% of Medicare beneficiaries in traditional Medicare have a Medigap policy. States with higher Medigap enrollment tend to be in the Midwest and plains states, where relatively fewer beneficiaries are enrolled in Medicare Advantage plans.

What Are the Different Types of Medigap Policies and What Benefits Do They Cover?

There are 10 different types of Medigap policies (labeled A through N), each having a different, standardized set of benefits (Appendix Table 3).

Plan G is the most popular Medigap policy, accounting for 39% of all policyholders, or nearly 5.3 million people, in 2023 (Figure 3). Plan G is the most comprehensive policy available to new policyholders, covering the Part A deductible and all cost sharing for Part A and B covered services, but not the Part B deductible. Plan G has become the most popular plan since plan F, which covers all the same benefits as Plan G as well as the Part B deductible, can no longer be sold to new beneficiaries who turned 65 on or after January 1, 2020 due to a change in law (Plan C also is no longer available as of that date because it also covered the Part B deductible). Plan F has the second largest share of Medigap enrollment, covering 36% of Medigap policyholders or nearly 4.9 million people. Plan N has the third largest share of Medigap enrollment, covering 10% of policyholders or nearly 1.4 million people. Plan N is similar to Plan G, except that there are Part B copayments for some office visits and some emergency room visits, and it does not cover Part B excess charges.

Who Can Buy a Medigap Policy and When?

Federal law provides guaranteed issue protections for Medigap policies during a one-time, six-month Medigap open enrollment period for beneficiaries ages 65 and older, which begins the first month of Medicare Part B coverage, as well as for certain qualifying events. Some of these qualifying events may include instances when people involuntary lose certain types of supplemental coverage, such as when an employer cancels retiree coverage or when a Medicare Advantage plan discontinues coverage in their area. The federally guaranteed one-time, six-month Medigap open enrollment period does not extend to beneficiaries who qualify for Medicare under age 65.

Beneficiaries also have guaranteed issue rights during specified “trial” periods, such as the first year that adults ages 65 and older are in Medicare Advantage. During that time, older adults can try a Medicare Advantage plan, and if they disenroll within the first year, they have guaranteed issue rights to purchase any Medigap policy that is sold in their state.

During these defined periods, Medigap insurers cannot deny a Medigap policy to any qualifying applicant based on factors such as age, gender, or health status. Further, during these periods, Medigap insurers cannot vary premiums based on an applicant’s pre-existing medical conditions or exclude coverage for a pre-existing medical condition (i.e., medical underwriting).

However, under federal law, Medigap insurers may impose a waiting period of up to six months to cover services related to pre-existing conditions if the applicant did not have at least six months of prior continuous creditable coverage. For qualifying events that trigger guaranteed issue rights, people ages 65 and older in Medicare generally have 63 days to apply for a Medigap policy.

States can choose to establish Medigap consumer protections that go further than the minimum federal standards. Four states – Connecticut, Massachusetts, Maine, and New York – require Medigap insurers to offer policies either continuously throughout the year or once per year to Medicare beneficiaries age 65 and older without regard to their medical conditions. Other states have also expanded on the federal minimum standards to allow beneficiaries to purchase Medigap on a guaranteed issue basis after certain qualifying events or for beneficiaries under 65 with disabilities to purchase Medigap during an initial open enrollment period. (For more information on qualifying events and additional Medigap protections, see Medigap May Be Elusive for Medicare Beneficiaries with Pre-Existing Conditions for more details.)

Premiums Vary Across Medigap Policies

States establish certain rules for Medigap insurers, including how to set premiums. Premiums may be based on factors such as a policyholder’s age, smoking status, gender, and residential area, even during open enrollment and guaranteed issue periods.

Premium costs are one of the primary concerns for people with Medigap. KFF focus groups indicate that while most beneficiaries with Medigap are satisfied with their coverage and like many of its elements, including coverage of most or all of Medicare’s cost-sharing requirements, comprehensiveness of their coverage, control over their health care, and ability to see any provider they want (by virtue of being in traditional Medicare rather than Medicare Advantage), some participants noted their premiums were expensive or cost more than they would like.

There are three different rating systems that can affect how Medigap insurers determine premiums: community rating, issue-age rating, or attained-age rating.

- Community rating: The same premium is generally charged to everyone, regardless of age or gender. Premiums may go up because of inflation and other factors, such as smoking status and residential area, but not due to age.

- Issue-age rating: The premium is based on the age of the beneficiary when they purchase the Medigap policy. Premiums are lower for people who buy at a younger age and will not change as they get older, but premiums may go up because of inflation and other factors, such as smoking status and residential area, but not due to age.

- Attained-age rating: The premium is based on a beneficiary’s current age, so the premium goes up as they get older. Premiums are lower for younger buyers but increase as they get older, which means that premiums may be the least expensive at first but can eventually become the most expensive. Premiums may also go up because of inflation and other factors, such as smoking status and residential area.

States can impose regulations on which of these rating systems are permitted or required for Medigap policies sold in their state. Currently, nine states (AR, CT, ID, MA, ME, MN, NY, VT, and WA) require premiums to be community rated among policyholders ages 65 and older (Appendix Table 4). Four states – Arizona, Florida, Georgia, and Missouri – permit issue-age rating but prohibit attained-age rating, while the majority of states (37 states and D.C.) allow any rating system.

Premium Rules Vary Across States That Require Insurers to Offer at Least One Medigap Policy Type to People Under Age 65

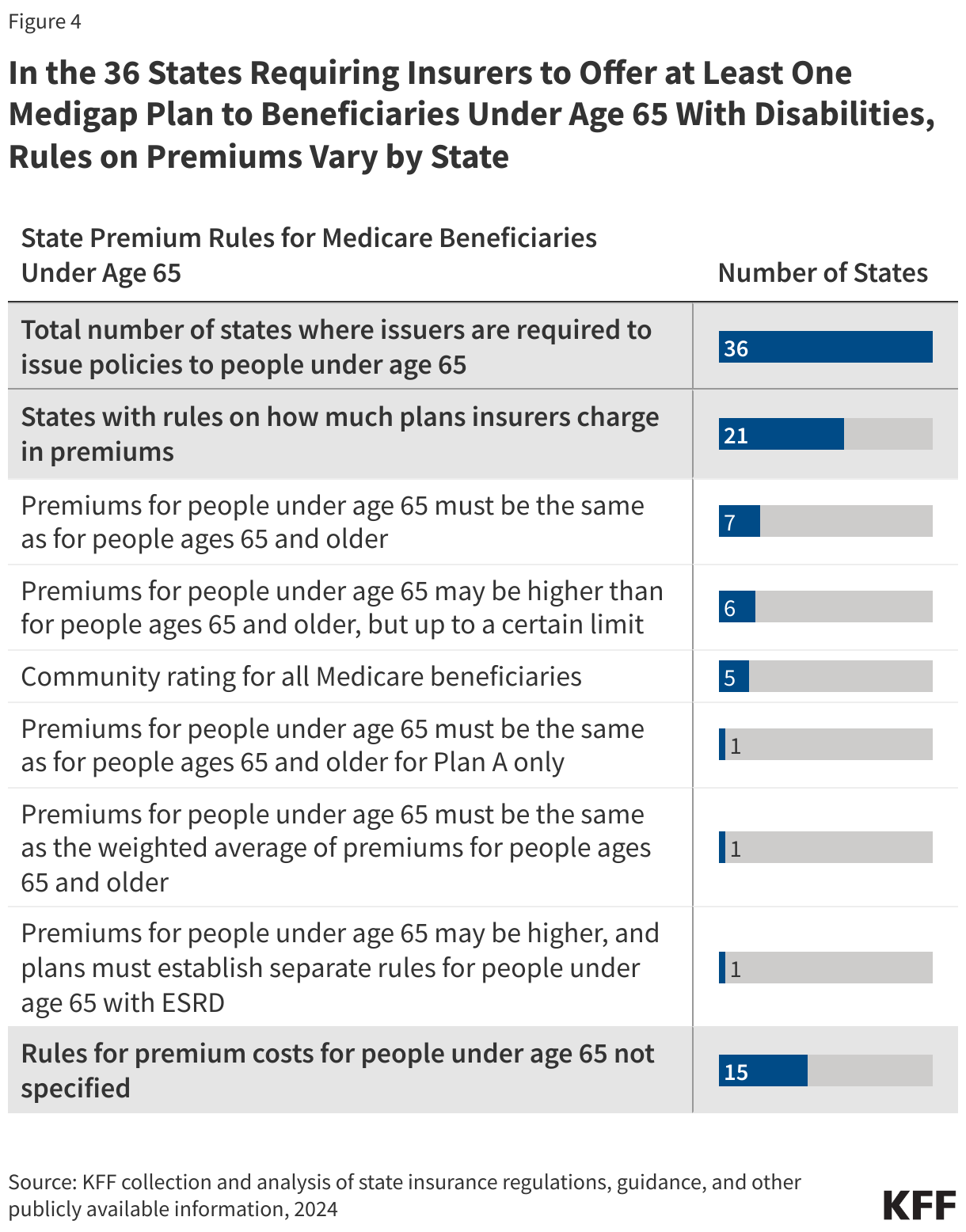

There are 36 states that require insurers to make at least one kind of Medigap policy guaranteed issue during an initial open enrollment period for beneficiaries under age 65, which is not a federal requirement. In these states, rules vary as to whether the same premiums are required for people under ages 65 and people ages 65 and older.

Among these 36 states, 21 states limit how much insurers can charge in premiums for beneficiaries under age 65. (Figure 4, Appendix Table 5). The remaining 15 states have no specified rules on premium costs.

Average Medigap Premiums Among Current Policyholders

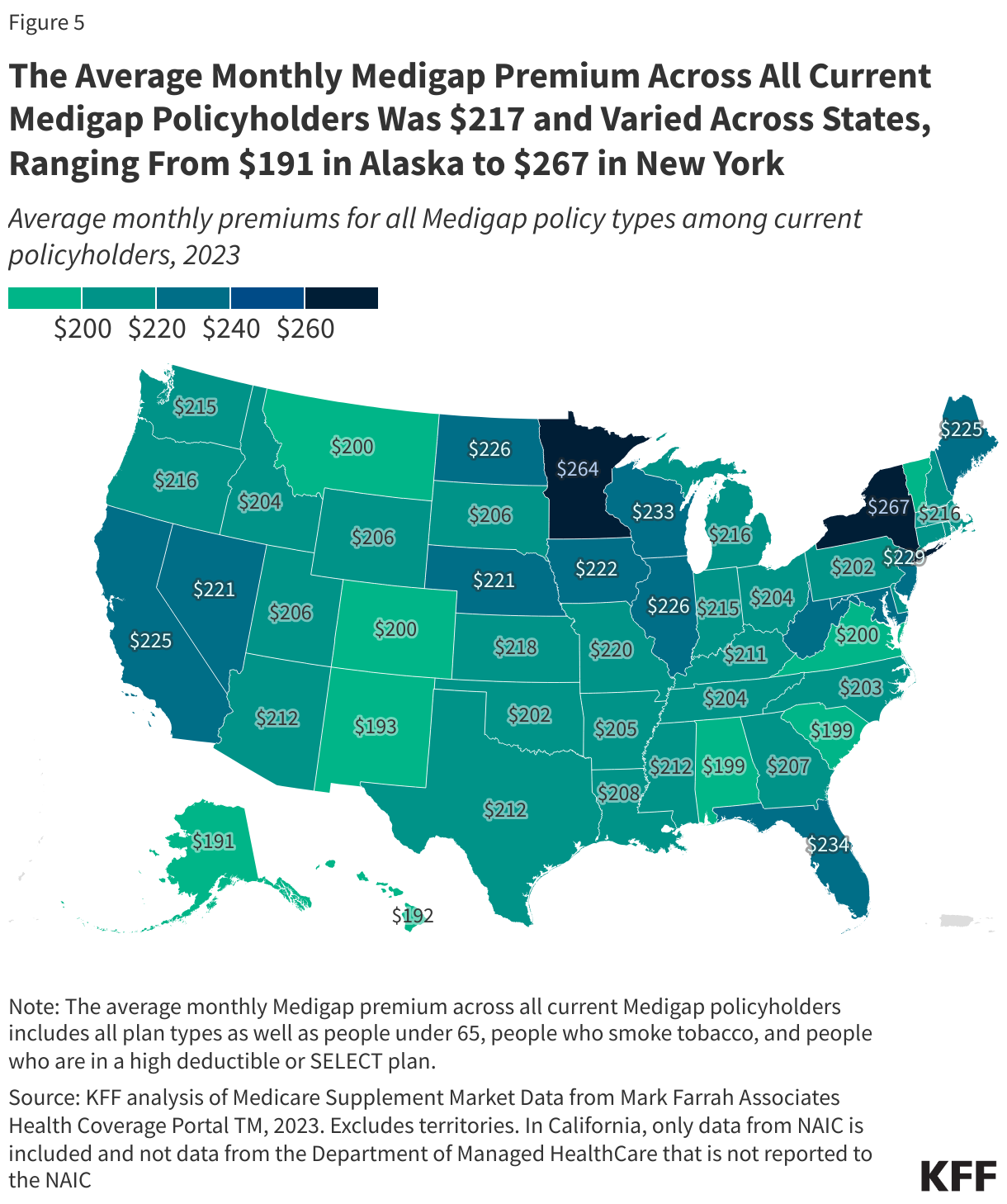

The average monthly Medigap premium across all current Medigap policyholders (including people under 65, people who smoke tobacco, and people who are in a high deductible or SELECT plan) was $217, ranging from $191 in Alaska to $267 in New York in 2023 (Figure 5, Appendix Table 4).

Average premiums also vary considerably depending on the policy type. For Plan G, the most popular and comprehensive plan available to new enrollees, the average monthly premium among current policyholders in 2023 was $164, and ranged from $140 in Washington D.C. and $141 in Hawaii and New Mexico to $236 in New York (Figure 6, Appendix Table 4). For Plan F, the plan with the second highest enrollment (but no longer available to new enrollees as of 2020), the average premium among current policyholders is $274, ranging from $214 in Vermont to $313 in New York. The difference in premiums may be due in part to the fact that Plan F covers the Part B deductible, which Plan G does not cover, but may also be related to other factors, as described below.

In the five states with the most expensive monthly premiums on average in 2023 for Plan G, four states (NY, CT, ME, WA) require community rating, while the fifth (FL) only allows issue-age rating. Further, the three states with highest premiums – New York, Connecticut, and Maine – have continuous or annual guaranteed issue protections. For Plan F, however, while the state with the highest monthly premium is New York, the four states with the next highest premiums (IN, NE, MD, and WV) are not community rated and do not have guaranteed issue protections.

Overall, for average Medigap premiums across all current policyholders, there is not a clear relationship between states with community rating rules or guaranteed issue protections and having higher premiums. For example, New York has the highest average monthly premium, while Maine is slightly above the national average, and Connecticut and Massachusetts are about the national average. Differences in average premiums across states can be due to several factors, including Medigap rating requirements, guaranteed issue requirements, the number of Medicare beneficiaries, the characteristics of the Medicare population, Medicare Advantage penetration, urbanicity of the county, and health care cost and usage patterns. Due to limitations in the data, we are unable to evaluate differences in average premiums across gender, age, or smoking status.

“New or Innovative” Benefits in Medigap Policies

According to federal guidelines, Medigap insurers may offer policies that cover “new or innovative” benefits that are cost-effective, in addition to the standardized Medigap benefits provided in a given policy. These new or innovative benefits can include vision, dental, and hearing benefits, access to a 24/7 nurse phone line, access to Silver Sneaker fitness benefits, and other wellness benefits. Medigap policies that include these types of additional benefits often have slightly higher premiums than the standard version of the policy.

The scope of these benefits varies across policy types and insurers. For example, some policies include coverage of specific dental services, such as 100% coverage of dental diagnostic evaluations, preventive services, and diagnostic radiographs (x-rays), and 80% of some restorative services from in-network dentists, though they may not cover more comprehensive dental services. For other policies, rather than dental insurance, enrollees can receive discounts off of nationally contracted rates for a range of dental services that are not covered by traditional Medicare, including cleanings, exams, fillings and crowns, from in-network dentists.

These benefits, which are not available generally in traditional Medicare, may be offered to help Medigap insurers compete for business with Medicare Advantage plans, nearly all of which offer dental, vision, and hearing, as well as other extra benefits. KFF focus groups show that the availability of extra benefits in Medicare Advantage plans, such as dental and vision, is a major consideration when beneficiaries make their Medicare coverage choices. Moreover, KFF’s analysis of television ads from 2022 confirms that messaging about extra benefits is an important tool to attract enrollees, and were mentioned in more than 90% of ads promoting Medicare Advantage. Dental coverage was the most advertised extra benefit (included in 84% of ads), followed by coverage of vision (63%) and hearing (56%) services.

Methods |

| This analysis uses data from Health Coverage PortalTM, a market database maintained by Mark Farrah Associates, which includes information from the National Association of Insurance Commissioners (NAIC). We used the “Medicare Supplement Market Data” report (accessed June 14, 2024) for this analysis. For the analysis of Medigap enrollment and premiums, territories, including Puerto Rico, are excluded. For Medigap enrollment overall, data reported to the Department of Managed Health Care in California (536,659 beneficiaries in 2023) is included in overall California enrollment counts, but this data is not included for analysis of enrollment by policy type. For the analysis of average premiums among current Medigap policyholders, only data that is reported to the NAIC is included because data from the California Department of Managed Health Care does not include information about premiums or policy type. For that analysis, KFF excluded policies that have negative or zero dollars in premiums. Premiums for current policyholders include those who smoke tobacco and those with high deductible or SELECT policies.

For characteristics of Medicare beneficiaries with Medigap versus those with Medicare Advantage, KFF used the Centers for Medicare & Medicaid Services (CMS) Medicare Current Beneficiary Survey 2022 Survey File data. Data excludes beneficiaries with Part A only or Part B only for most of the year or Medicare as a Secondary Payer. Persons of Hispanic origin may be of any race but are categorized as Hispanic; other groups are non-Hispanic. |