2021 Employer Health Benefits Survey

Section 4: Types of Plans Offered

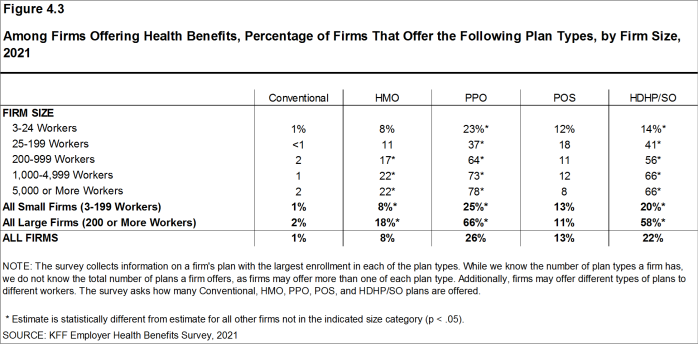

Most firms that offer health benefits offer only one type of health plan (75%). Large firms (200 or more workers) are more likely than small firms (3-199 workers) to offer more than one type of health plan. Firms are most likely to offer their workers a PPO plan and are least likely to offer a conventional plan (sometimes known as indemnity insurance).

NUMBER OF PLAN TYPES OFFERED

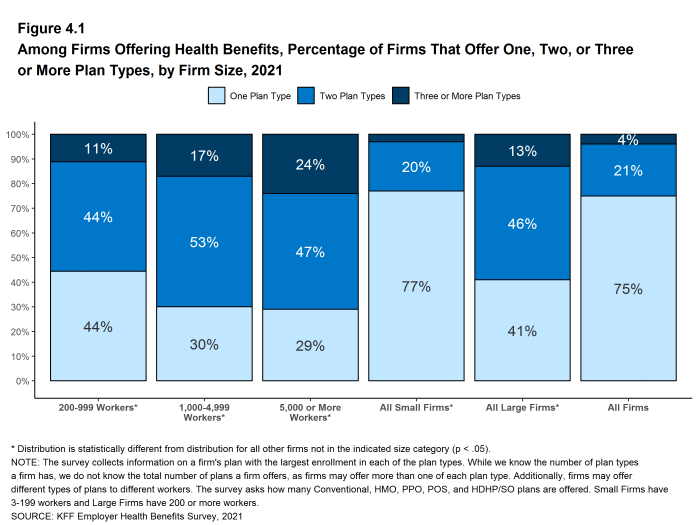

- In 2021, 75% of firms offering health benefits offer only one type of health plan. Large firms are more likely than small firms to offer more than one plan type (59% vs. 23%) [Figure 4.1].

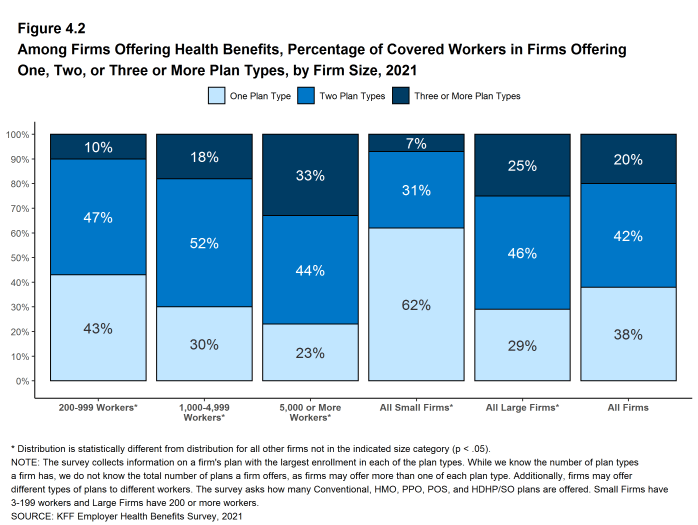

- Sixty-two percent of covered workers are employed in a firm that offers more than one type of health plan. Seventy-one percent of covered workers in large firms are employed by a firm that offers more than one plan type, compared to 38% in small firms [Figure 4.2].

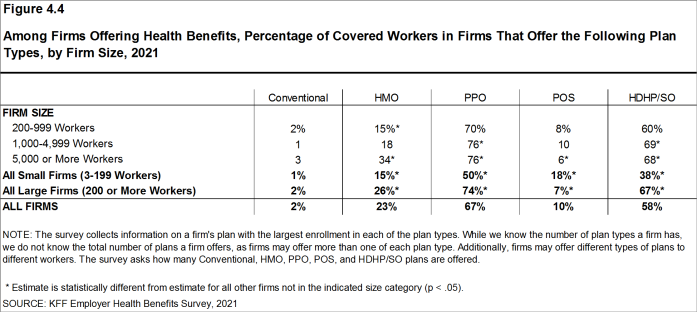

- Sixty-seven percent of covered workers in firms offering health benefits work in firms that offer one or more PPOs; 58% work in firms that offer one or more HDHP/SOs; 23% work in firms that offer one or more HMOs; 10% work in firms that offer one or more POS plans; and 2% work in firms that offer one or more conventional plans [Figure 4.4].

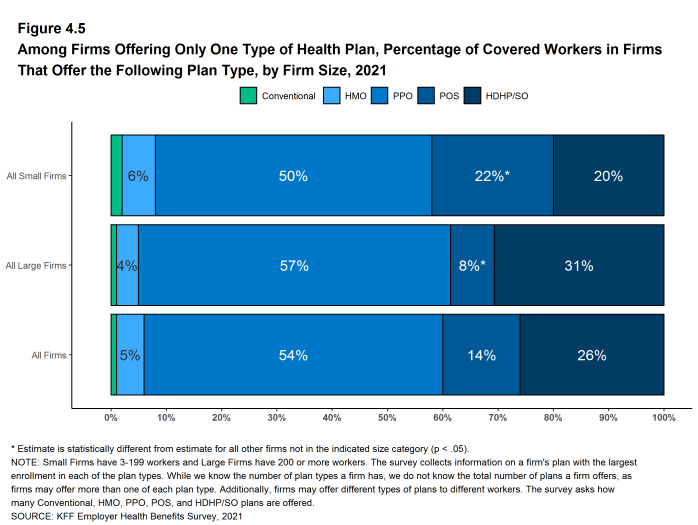

- Among covered workers in firms offering only one type of health plan, 54% are in firms that only offer one or more PPOs and 26% are in firms that only offer one or more HDHP/SOs [Figure 4.5].

Figure 4.1: Among Firms Offering Health Benefits, Percentage of Firms That Offer One, Two, or Three or More Plan Types, by Firm Size, 2021

Figure 4.2: Among Firms Offering Health Benefits, Percentage of Covered Workers in Firms Offering One, Two, or Three or More Plan Types, by Firm Size, 2021

Figure 4.3: Among Firms Offering Health Benefits, Percentage of Firms That Offer the Following Plan Types, by Firm Size, 2021

Figure 4.4: Among Firms Offering Health Benefits, Percentage of Covered Workers in Firms That Offer the Following Plan Types, by Firm Size, 2021

Figure 4.5: Among Firms Offering Only One Type of Health Plan, Percentage of Covered Workers in Firms That Offer the Following Plan Type, by Firm Size, 2021

CHOICE OF HDHP/SO PLANS

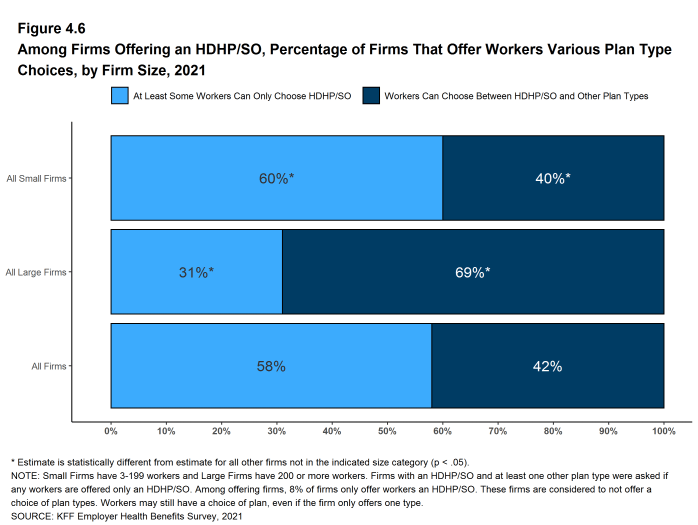

- Some firms only offer workers an HDHP/SO, or do not make other plan choices available to some workers. At 58% of firms that offer an HDHP/SO, at least some workers can only choose an HDHP/SO, while 42% of firms that offer an HDHP/SO allow workers also to choose between an HDHP/SO and other plan types [Figure 4.6].

Figure 4.6: Among Firms Offering an HDHP/SO, Percentage of Firms That Offer Workers Various Plan Type Choices, by Firm Size, 2021

The survey collects information on a firm’s plan with the largest enrollment in each of the plan types. While we know the number of plan types a firm has, we do not know the total number of plans a firm offers workers. In addition, firms may offer different types of plans to different workers. For example, some workers might be offered one type of plan at one location, while workers at another location are offered a different type of plan.

HMO is a health maintenance organization. The survey defines an HMO as a plan that does not cover non-emergency out-of-network services.

PPO is a preferred provider organization. The survey defines PPOs as plans that have lower cost sharing for in-network provider services, and do not require a primary care gatekeeper to screen for specialist and hospital visits.

POS is a point-of-service plan. The survey defines POS plans as those that have lower cost sharing for in-network provider services, but do require a primary care gatekeeper to screen for specialist and hospital visits.

HDHP/SO is a high-deductible health plan with a savings option such as an HRA or HSA. HDHP/SOs are treated as a distinct plan type even if the plan would otherwise be considered a PPO, HMO, POS plan, or indemnity plan. These plans have a deductible of at least $1,000 for single coverage and $2,000 for family coverage and are offered with an HRA, or are HSA-qualified. See Section 8 for more information on HDHP/SOs.

Conventional/Indemnity The survey defines conventional or indemnity plans as those that have no preferred provider networks and the same cost sharing regardless of physician or hospital.