2020 Employer Health Benefits Survey

Section 2: Health Benefits Offer Rates

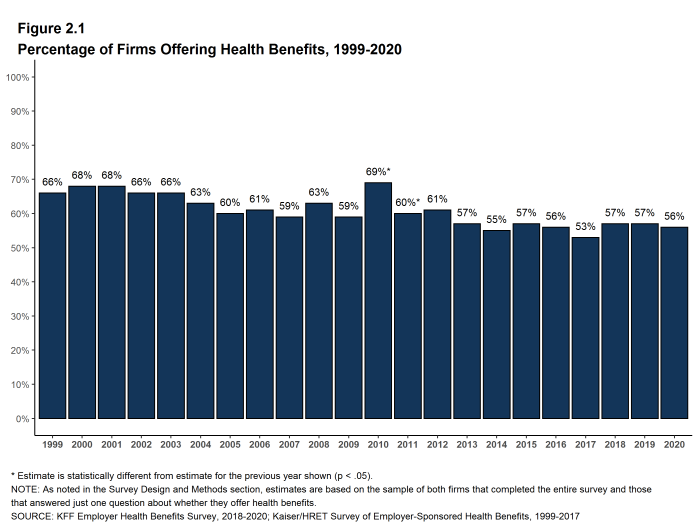

While nearly all large firms (200 or more workers) offer health benefits to at least some workers, small firms (3-199 workers) are significantly less likely to do so. The percentage of all firms offering health benefits in 2020 (56%) is similar to the percentages of firms offering health benefits last year (57%) and five years ago (57%).

Firms not offering health benefits continue to cite cost as the most important reason they do not do so. Almost all firms that offer coverage offer benefits to dependents such as children and the spouses of eligible employees.

FIRM OFFER RATES

- In 2020, 56% of firms offer health benefits, similar to the percentage last year [Figure 2.1].

- The overall percentage of firms offering health benefits in 2020 is similar to the percentages offering health benefits in 2015 (57%). The percentage of offering firms in 2010 was an aberration so we are not making a 10-year comparison [Figure 2.1].

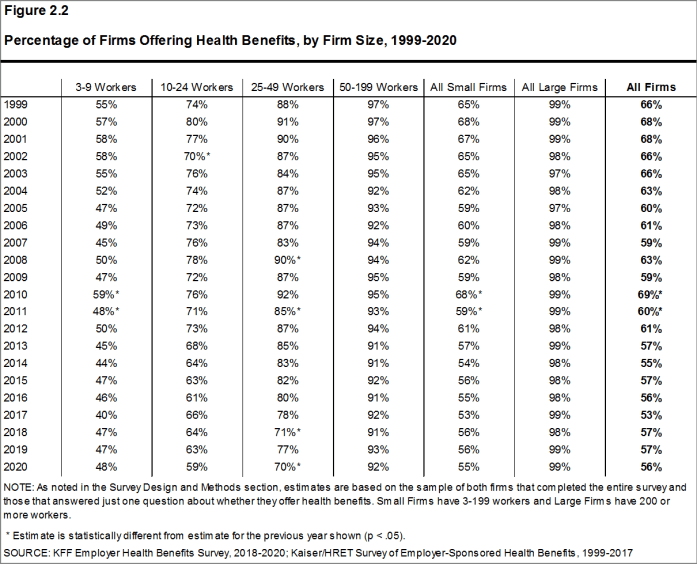

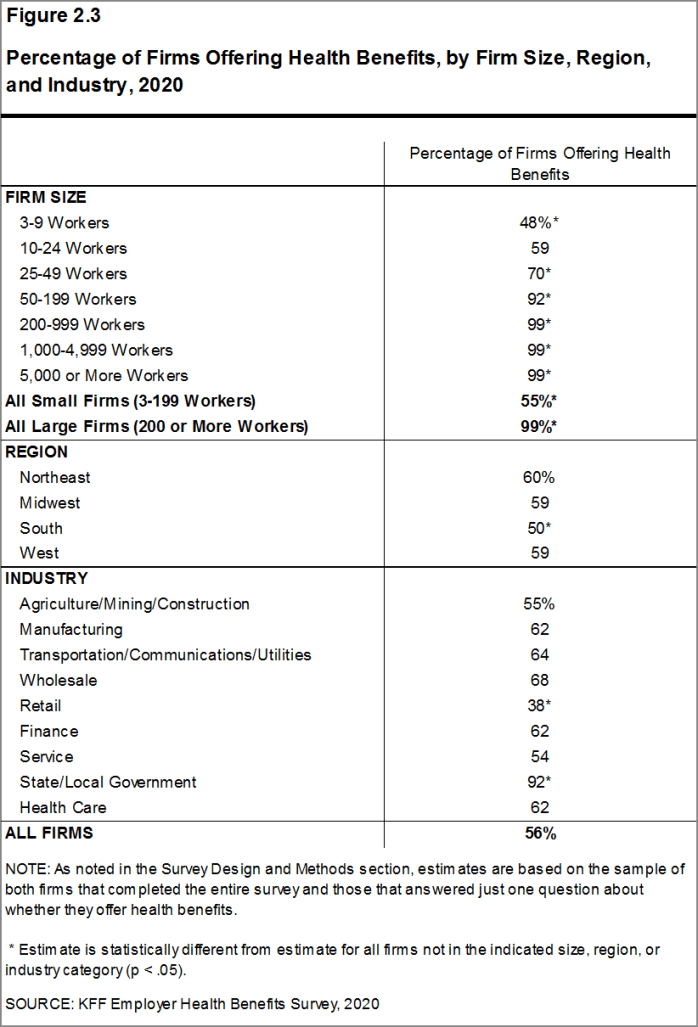

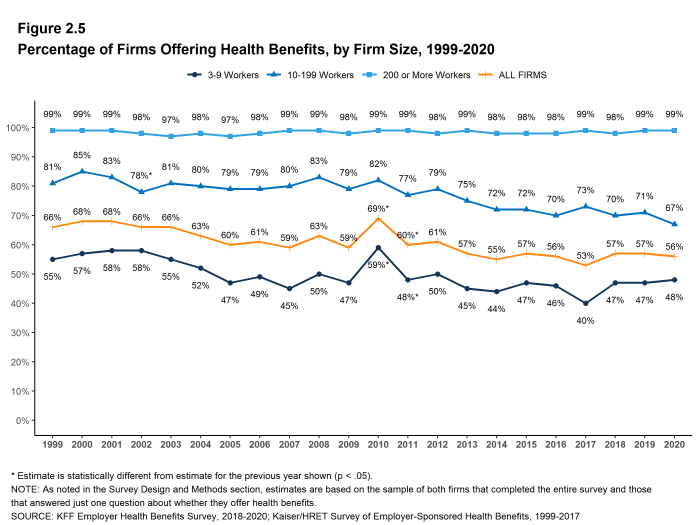

- Ninety-nine percent of large firms offer health benefits to at least some of their workers. In contrast, only 55% of small firms offer health benefits [Figure 2.2] and [Figure 2.3]. The percentages of both small and large firms offering health benefits to at least some of their workers in 2020 are similar to those last year [Figure 2.2].

- The smallest-sized firms are least likely to offer health insurance: 48% of firms with 3-9 workers offer coverage, compared to 59% of firms with 10-24 workers, 70% of firms with 25-49 workers, and 92% of firms with 50-199 workers [Figure 2.3]. Since most firms in the country are small, variation in the overall offer rate is driven largely by changes in the percentages of the smallest firms (3-9 workers) offering health benefits. For more information on the distribution of firms in the country, see the Survey Design and Methods Section and [Figure M.6].

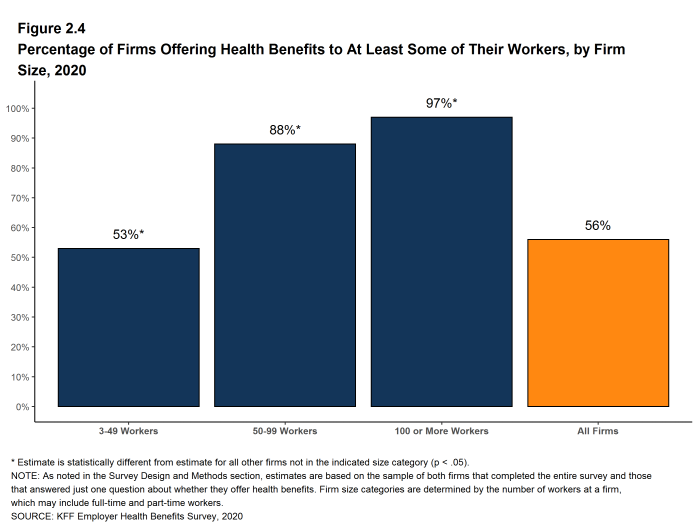

- Only 53% of firms with 3-49 workers offer health benefits to at least some of their workers, compared to 94% of firms with 50 or more workers [Figure 2.4].

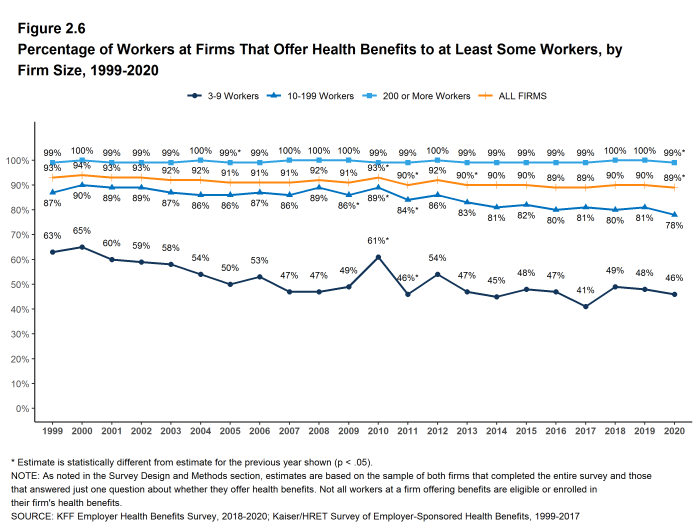

- Because most workers are employed by larger firms, most workers work at a firm that offers health benefits to at least some of its employees. Eighty-nine percent of all workers are employed by a firm that offers health benefits to at least some of its workers [Figure 2.6].

Figure 2.1: Percentage of Firms Offering Health Benefits, 1999-2020

Figure 2.2: Percentage of Firms Offering Health Benefits, by Firm Size, 1999-2020

Figure 2.3: Percentage of Firms Offering Health Benefits, by Firm Size, Region, and Industry, 2020

Figure 2.4: Percentage of Firms Offering Health Benefits to at Least Some of Their Workers, by Firm Size, 2020

Figure 2.5: Percentage of Firms Offering Health Benefits, by Firm Size, 1999-2020

Figure 2.6: Percentage of Workers at Firms That Offer Health Benefits to at Least Some Workers, by Firm Size, 1999-2020

PART-TIME WORKERS

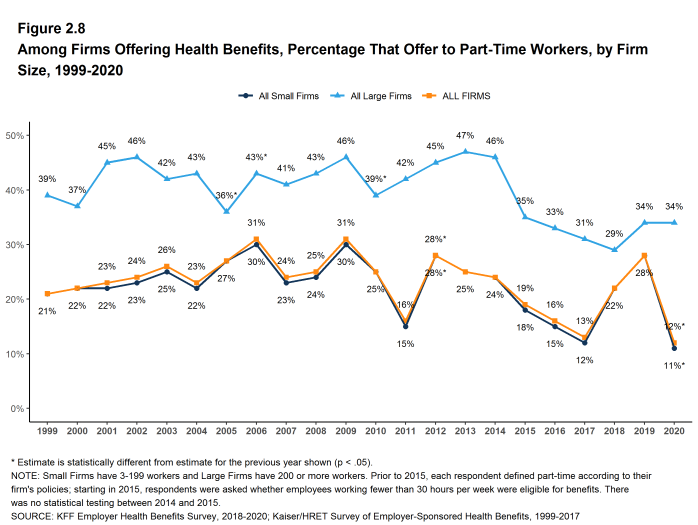

- Among firms offering health benefits, relatively few offer benefits to their part-time workers.

- The Affordable Care Act (ACA) defines full-time workers as those who on average work at least 30 hours per week, and part-time workers as those who on average work fewer than 30 hours per week. The employer shared responsibility provision of the ACA requires that firms with at least 50 full-time equivalent employees offer most full-time employees coverage that meets minimum standards or be assessed a penalty.13

Beginning in 2015, we modified the survey to explicitly ask employers whether they offered benefits to employees working fewer than 30 hours. Our previous question did not include a definition of “part-time”. For this reason, historical data on part-time offer rates are shown, but we did not test whether the differences between 2014 and 2015 were significant. Many employers may work with multiple definitions of part-time; one for their compliance with legal requirements and another for internal policies and programs.

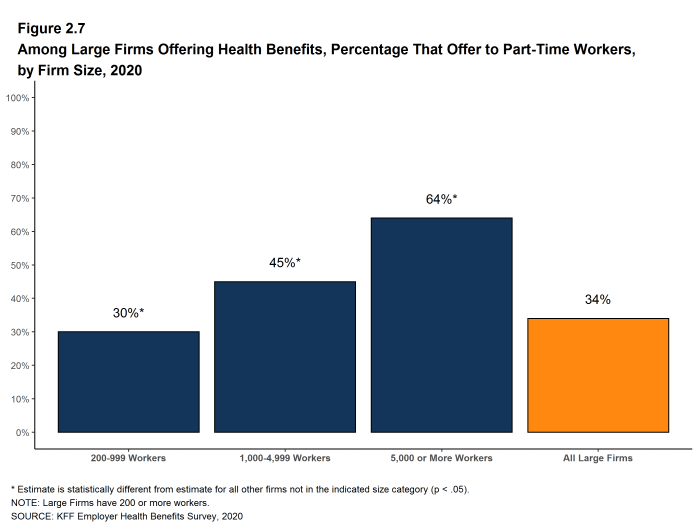

- Thirty-four percent of large firms offer health benefits in 2020 offer health benefits to part-time workers, similar to the percentage in 2019. The share of large firms offering health benefits to part-time workers increases with firm size [Figure 2.7].

Figure 2.7: Among Large Firms Offering Health Benefits, Percentage That Offer to Part-Time Workers, by Firm Size, 2020

Figure 2.8: Among Firms Offering Health Benefits, Percentage That Offer to Part-Time Workers, by Firm Size, 1999-2020

SPOUSES AND DEPENDENTS

- The vast majority of firms offering health benefits offer to spouses and dependents, such as children.

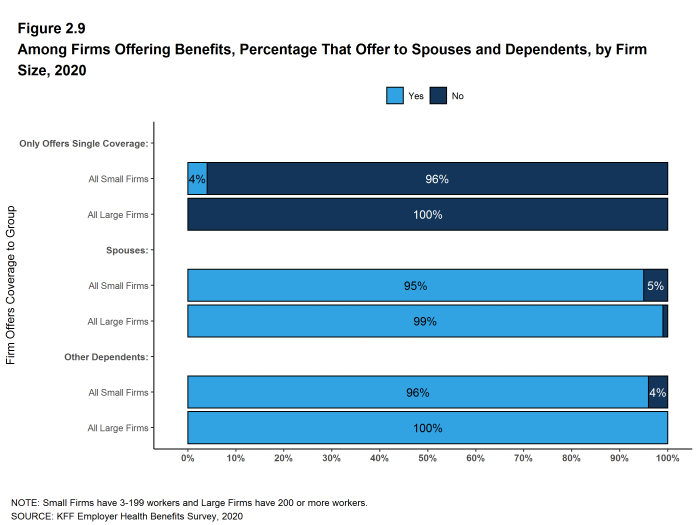

- In 2020, 95% of firms offering health benefits offer coverage to spouses, similar to the percentage last year [Figure 2.9].

- Ninety-six percent of firms offering health benefits cover dependents other than spouses, such as children, similar to the percentages last year [Figure 2.9].

- Four percent of small firms offering health benefits offer only single coverage to their workers, similar to the percentage last year [Figure 2.9].

Figure 2.9: Among Firms Offering Benefits, Percentage That Offer to Spouses and Dependents, by Firm Size, 2020

SPOUSAL SURCHARGES

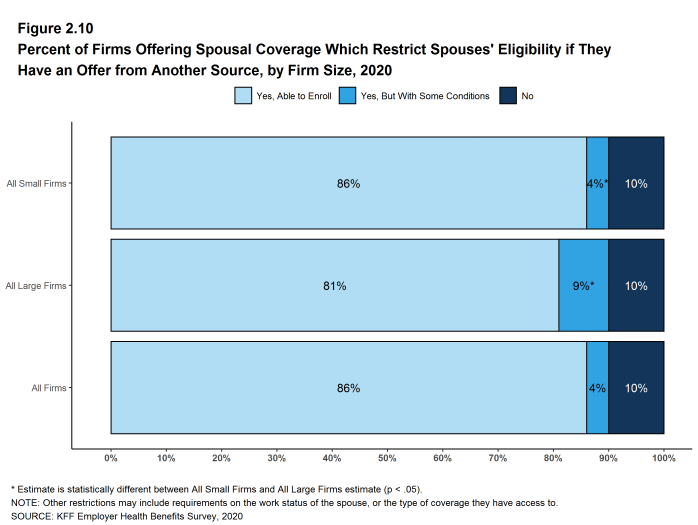

Some employers place conditions on the ability of dependent spouses to enroll in a health plan if the spouse is offered health insurance from another source, such as his or her own place of work.

- Among firms offering health benefits to spouses, 86% say that an employee’s spouse is able to enroll in the employee’s health plan even if the spouse is offered coverage from another source, 4% say the spouse can enroll subject to some conditions (for example, the type of coverage offered), and 10% say that the spouse is not eligible to enroll [Figure 2.10].

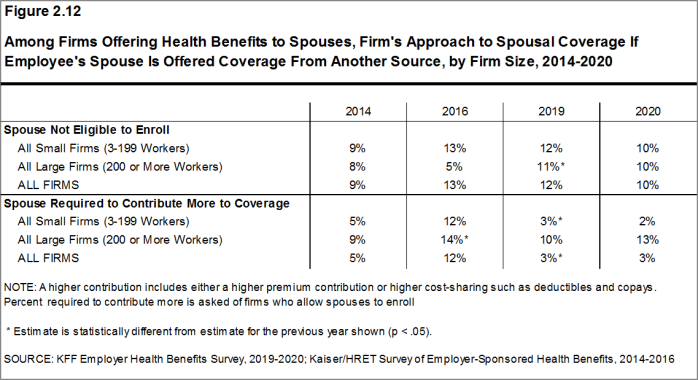

- Among large firms that say that spouses are eligible to enroll in an employee’s health plan even if the spouse has access to coverage from another source, 13% require the spouse to pay more to enroll than other spouses, such as a higher premium contribution or cost sharing [Figure 2.12].

Figure 2.10: Percent of Firms Offering Spousal Coverage Which Restrict Spouses’ Eligibility If They Have an Offer From Another Source, by Firm Size, 2020

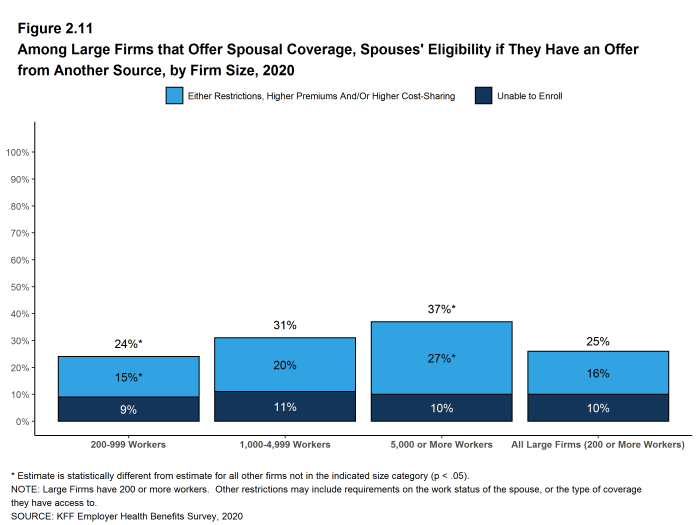

Figure 2.11: Among Large Firms That Offer Spousal Coverage, Spouses’ Eligibility If They Have an Offer From Another Source, by Firm Size, 2020

Figure 2.12: Among Firms Offering Health Benefits to Spouses, Firm’s Approach to Spousal Coverage If Employee’s Spouse Is Offered Coverage From Another Source, by Firm Size, 2014-2020

FIRMS NOT OFFERING HEALTH BENEFITS

- The survey asks firms that do not offer health benefits several questions, including whether they have offered insurance or shopped for insurance in the recent past, their most important reasons for not offering coverage, and their opinion on whether their employees would prefer an increase in wages or health insurance if additional funds were available to increase their compensation. Because such a small percentage of large firms report not offering health benefits, we present responses for small non-offering firms only.

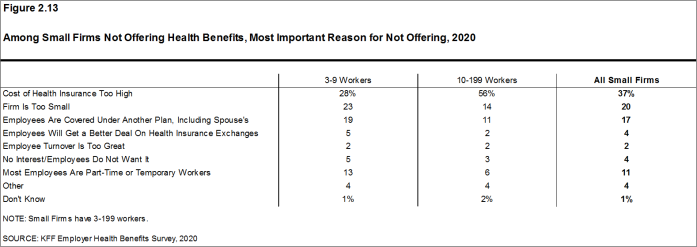

- The cost of health insurance remains the primary reason cited by firms for not offering health benefits. Among small firms not offering health benefits, 37% cite high cost as “the most important reason” for not doing so. Other factors include “the firm is too small” (20%), employees are covered by another health plan (including a spouse’s plan) (17%) and “most employees are part-time or temporary workers” (11%). Few small firms indicate that they do not offer because they believe employees will get a better deal on the health insurance exchanges (4%) [Figure 2.13].

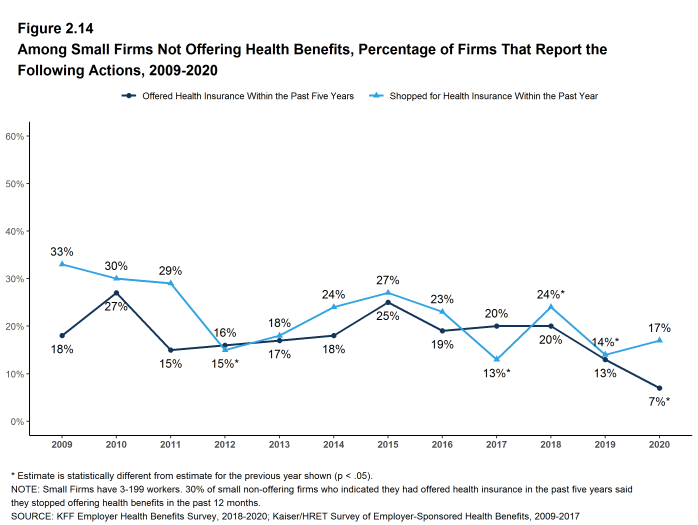

- Some small non-offering firms have either offered health insurance in the past five years or shopped for health insurance in the past year.

- Seven percent of small non-offering firms have offered health benefits in the past five years, lower than the percentage reported last year or in recent years [Figure 2.14]. We will monitor this percentage to determine if this is a single-year change or a new and different level.

- Seventeen percent of small non-offering firms have shopped for coverage in the past year, similar to the percentage last year (14%) [Figure 2.14].

- Among small non-offering firms that report they stopped offering coverage within the past five years, 30% stopped offering coverage within the past year.

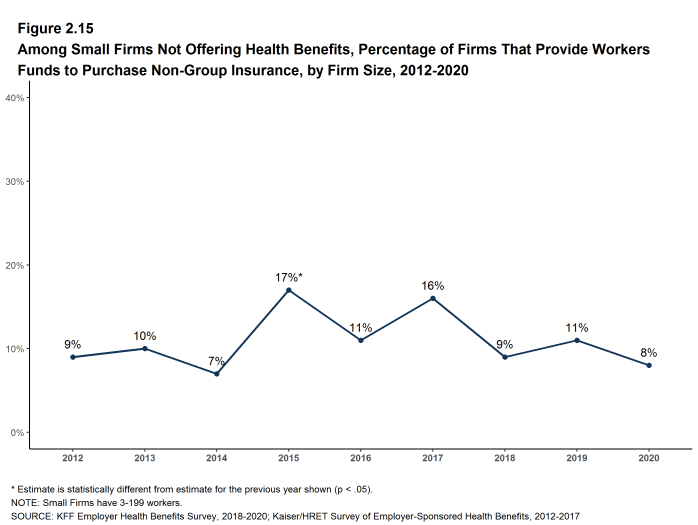

- Eight percent of small firms not offering health benefits report that they provide funds for employees to purchase insurance on their own in the individual market or through a health insurance exchange, similar to the percentage in 2019 [Figure 2.15].

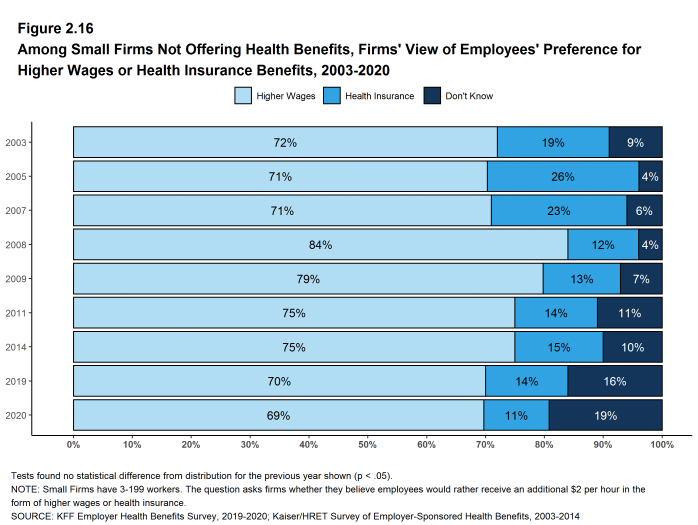

- Sixty-nine percent of small firms not offering health benefits believed that their employees would prefer a two dollar per hour increase in wages rather than health insurance. [Figure 2.16].

Figure 2.13: Among Small Firms Not Offering Health Benefits, Most Important Reason for Not Offering, 2020

Figure 2.14: Among Small Firms Not Offering Health Benefits, Percentage of Firms That Report the Following Actions, 2009-2020

Figure 2.15: Among Small Firms Not Offering Health Benefits, Percentage of Firms That Provide Workers Funds to Purchase Non-Group Insurance, by Firm Size, 2012-2020

Figure 2.16: Among Small Firms Not Offering Health Benefits, Firms’ View of Employees’ Preference for Higher Wages or Health Insurance Benefits, 2003-2020

- Internal Revenue Code. 26 U.S. Code § 4980H – Shared responsibility for employers regarding health coverage. 2011. https://www.gpo.gov/fdsys/pkg/USCODE-2011-title26/pdf/USCODE-2011-title26-subtitleD-chap43-sec4980H.pdf↩︎