2016 Employer Health Benefits Survey

Section Four: Types of Plans Offered

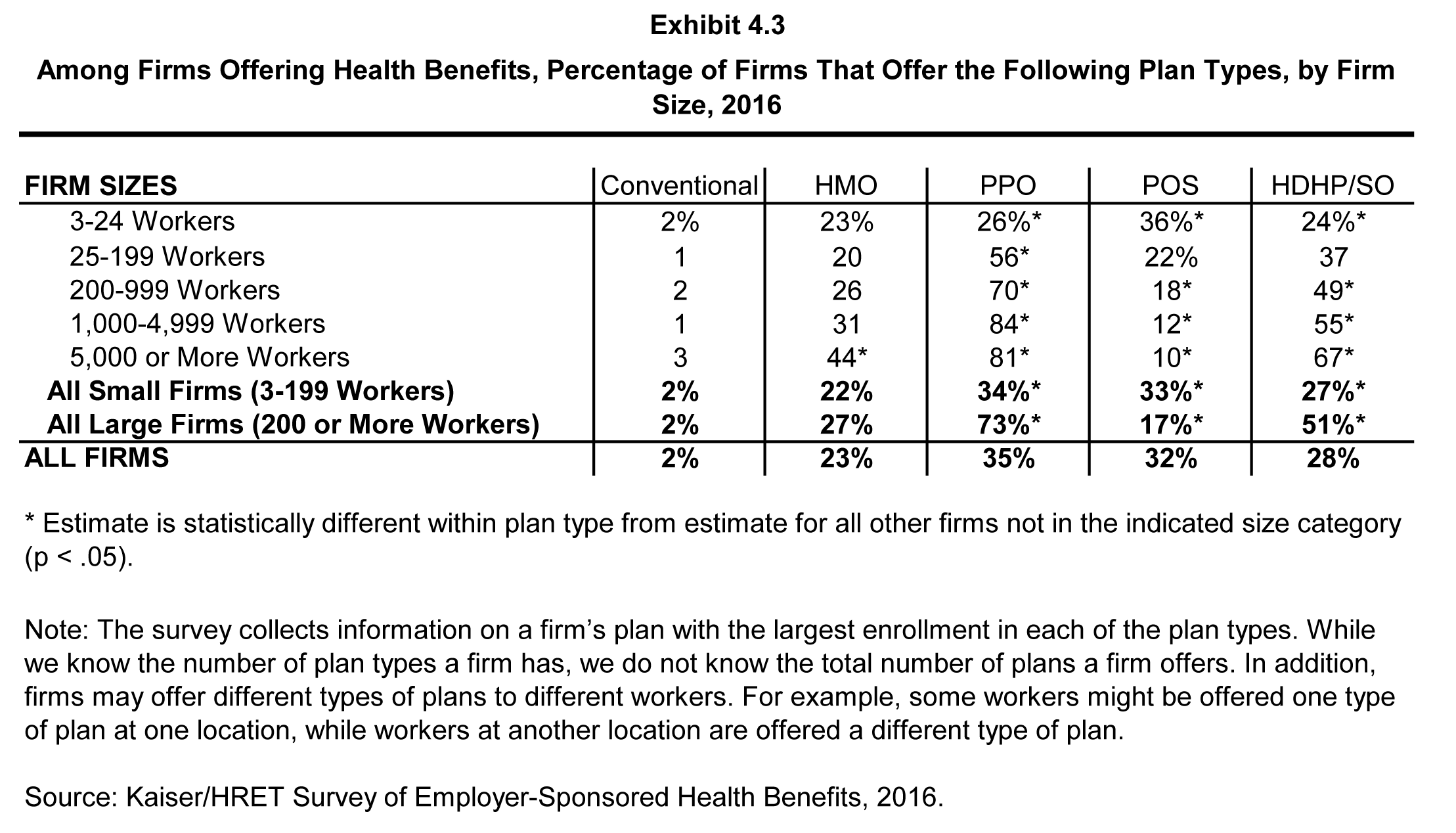

Most firms that offer health benefits offer only one type of health plan (83%) (see text box). Large firms (200 or more workers) are more likely to offer more than one type of health plan than small firms (3-199 workers). Employers are most likely to offer their workers a PPO plan and are least likely to offer a conventional plan (sometimes known as indemnity insurance).

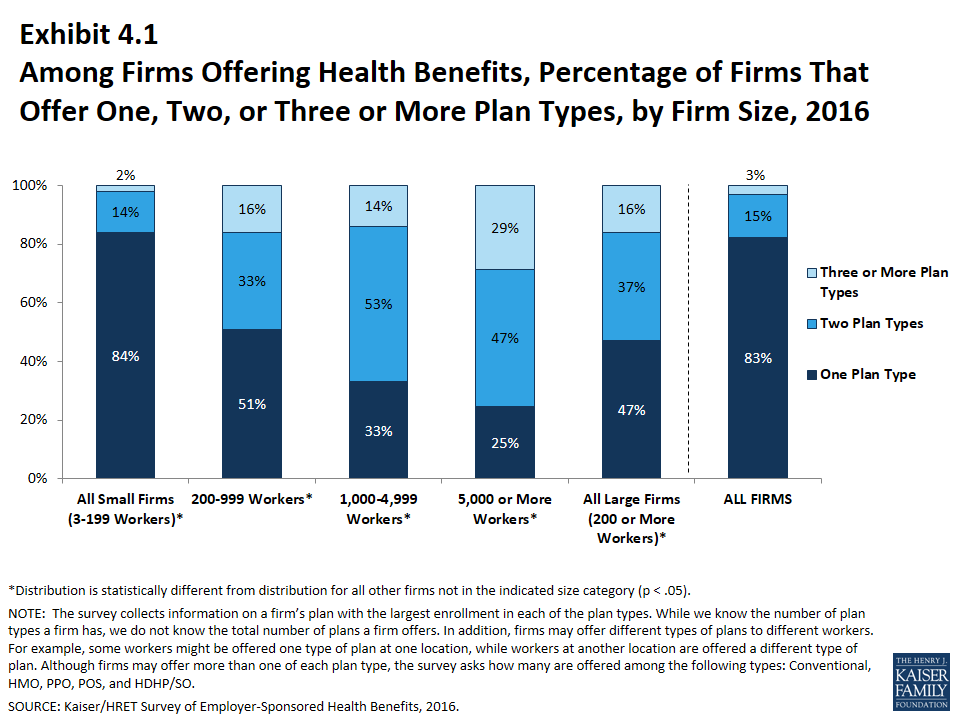

- Eighty-three percent of firms offering health benefits in 2016 offer only one type of health plan. Large firms are more likely to offer more than one plan type than small firms (53% vs. 16%) (Exhibit 4.1).

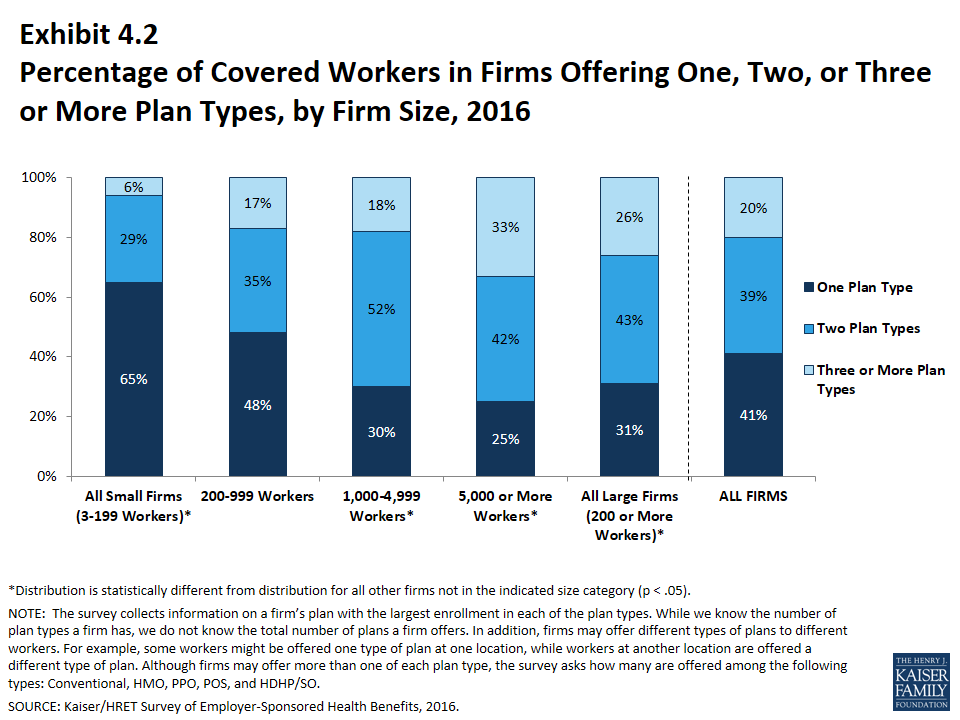

- In addition to looking at the percentage of firms that offer multiple plan types, the percentage of covered workers at firms that offer multiple plan types can also be analyzed. Fifty-nine percent of covered workers are employed in a firm that offers more than one health plan type. Sixty-nine percent of covered workers in large firms are employed by a firm that offers more than one plan type, compared to 35% in small firms (Exhibit 4.2).

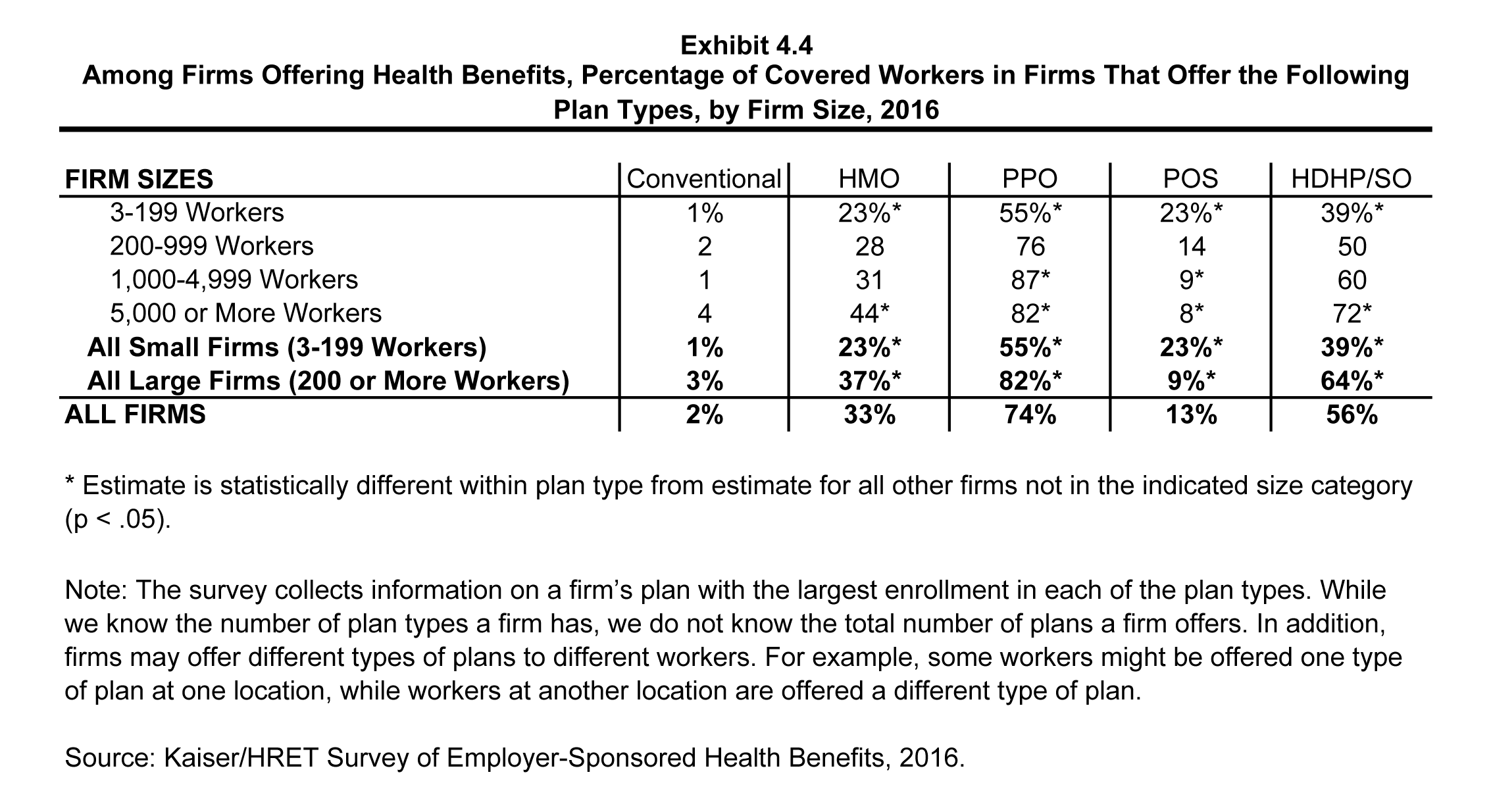

- Nearly three quarters (74%) of covered workers in firms offering health benefits work in firms that offer one or more PPO plans; 56% work in firms that offer one or more HDHP/SO plans; 33% work in firms that offer one or more HMO plans; 13% work in firms that offer one or more POS plans; and 2% work in firms that offer one or more conventional plans (Exhibit 4.4).1

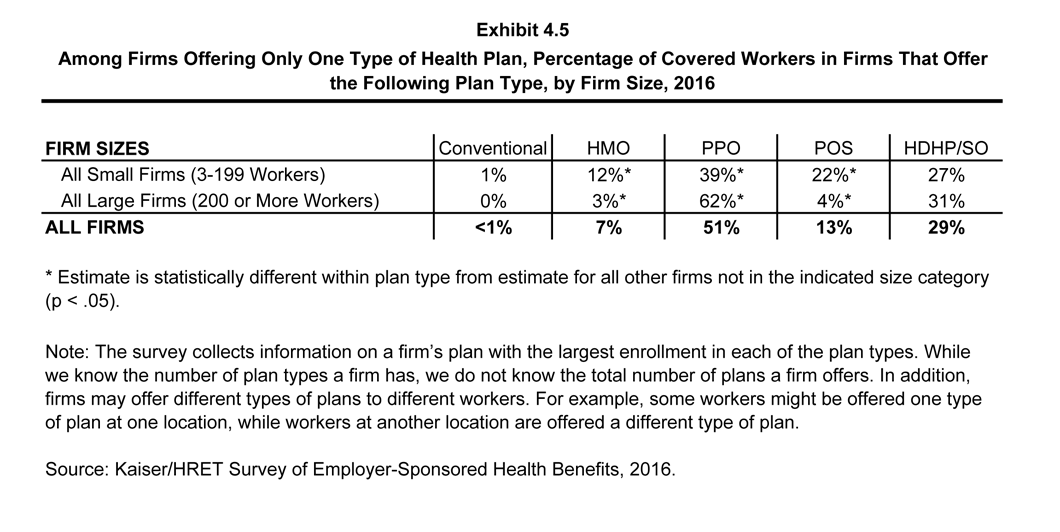

- Among firms offering only one type of health plan, covered workers in large firms are more likely to be offered PPO plans than covered workers in small firms (62% vs. 39%), while covered workers in small firms are more likely to be offered HMO (12%) and POS (22%) plans than covered workers in large firms (3% and 4%, respectively) (Exhibit 4.5).

- Among firms offering only one type of health plan, 29% of covered workers are in firms that only offer an HDHP/SO and 51% of covered workers are in firms that only offer a PPO (Exhibit 4.5).

The survey collects information on a firm’s plan with the largest enrollment in each of the plan types. While we know the number of plan types a firm has, we do not know the total number of plans a firm offers workers. In addition, firms may offer different types of plans to different workers. For example, some workers might be offered one type of plan at one location, while workers at another location are offered a different type of plan.

HMO is health maintenance organization.

PPO is preferred provider organization.

POS is point-of-service plan.

HDHP/SO is high-deductible health plan with a savings option such as an HRA or HSA.

Among Firms Offering Health Benefits, Percentage of Firms That Offer One, Two, or Three or More Plan Types, by Firm Size, 2016

Percentage of Covered Workers in Firms Offering One, Two, or Three or More Plan Types, by Firm Size, 2016

Among Firms Offering Health Benefits, Percentage of Firms That Offer the Following Plan Types, by Firm Size, 2016

Among Firms Offering Health Benefits, Percentage of Covered Workers in Firms That Offer the Following Plan Types, by Firm Size, 2016