2014 Employer Health Benefits Survey

Section Three: Employee Coverage, Eligibility, and Participation

Employers are the principal source of health insurance in the United States, providing health benefits for about 149 million non-elderly people in America.1 Most workers are offered health coverage at work, and the majority of workers who are offered coverage take it. Workers may not be covered by their own employer for several reasons: their employer may not offer coverage, they may be ineligible for benefits offered by their firm, they may elect to receive coverage through their spouse’s employer, or they may refuse coverage from their firm. In 2015, new coverage requirements will be implemented that may affect employers’ decisions about offering health care coverage going forward.

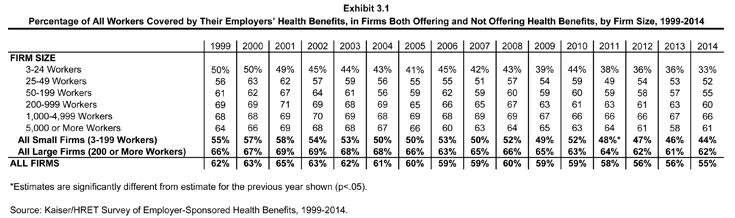

- Among firms offering health benefits, 62% percent of workers are covered by health benefits through their own employer (Exhibit 3.2).

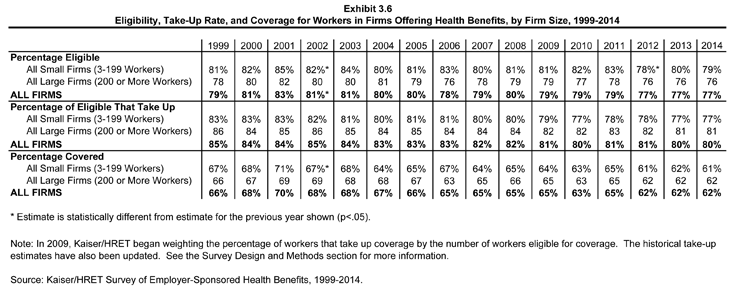

- When considering both firms that offer health benefits and those that don’t, 55% of workers are covered under their employer’s plan (Exhibit 3.1). This coverage rate has slowly decreased over time, down from 59% in 2009 and 61% in 2004.

Eligibility

- Not all employees are eligible for the health benefits offered by their firm, and not all eligible employees “take up” (i.e., elect to participate in) the offer of coverage. The share of workers covered in a firm is a product of both the percentage of workers who are eligible for the firm’s health insurance and the percentage who choose to take up the benefit.

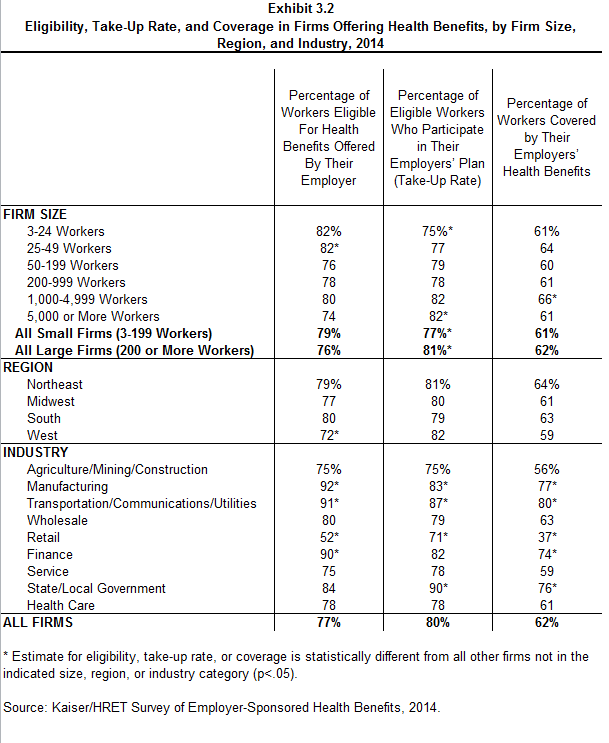

- Seventy-seven percent of workers in firms offering health benefits are eligible for the coverage offered by their employer (Exhibit 3.2).

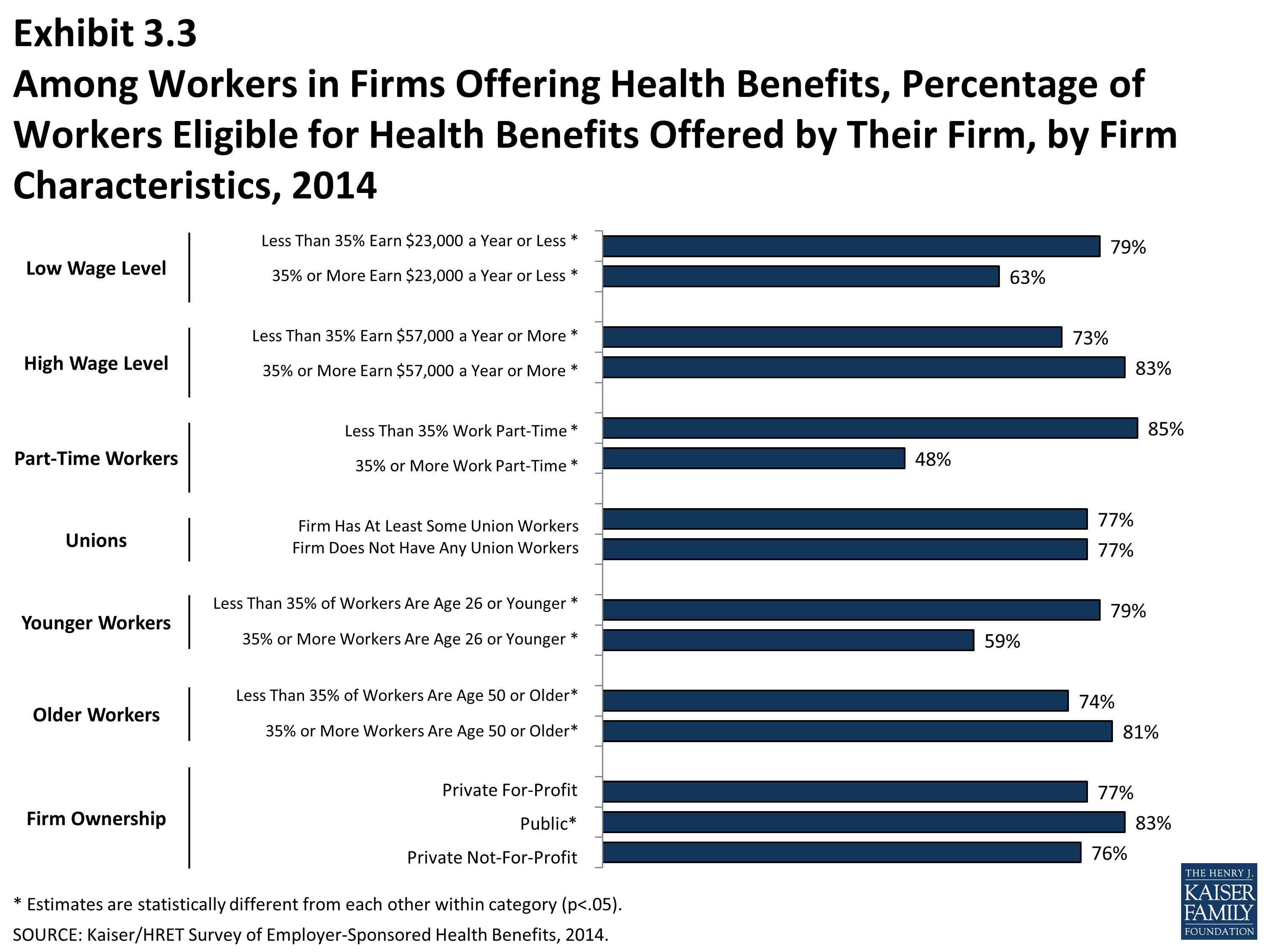

- Eligibility varies considerably by wage level. Employees in firms with a lower proportion of lower-wage workers (less than 35% of workers earn $23,000 or less annually) are more likely to be eligible for health benefits than employees in firms with a higher proportion of lower-wage workers (79% vs. 63%). We observe a similar pattern among firms with many higher-wage workers (35% or more of workers earn $57,000 or more annually) (83% vs. 73%) (Exhibit 3.3).

- Eligibility also varies by the age of the workforce. Those in firms with fewer younger workers (less than 35% of workers are age 26 or younger) are more likely to be eligible for health benefits than those in firms with many younger workers, at 79% versus 59% (Exhibit 3.3).

Take-up Rate

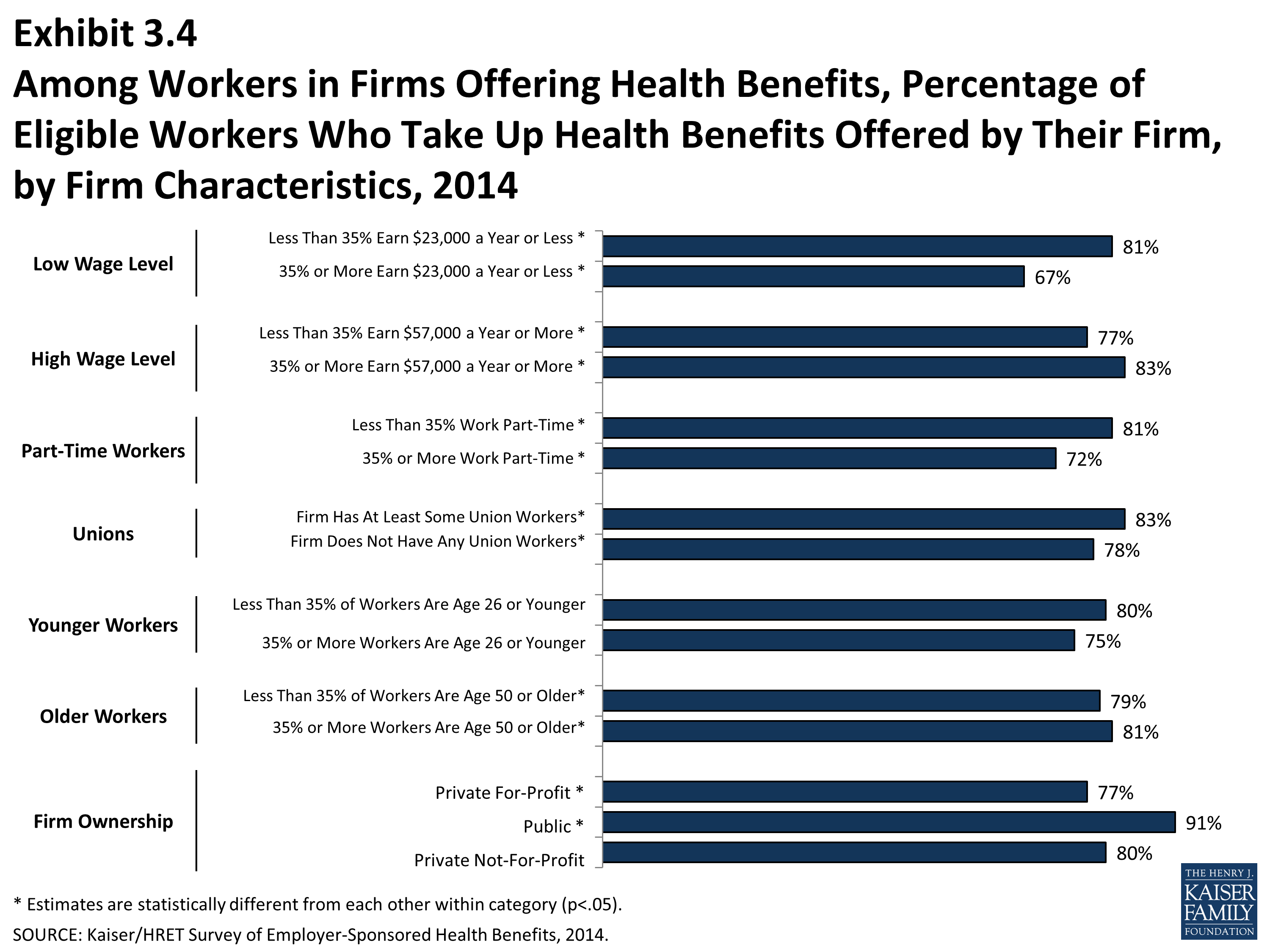

- Employees who are offered health benefits generally elect to take up the coverage. In 2014, 80% of eligible workers take up coverage when it was offered to them, the same rate as last year (Exhibit 3.2).2

- The likelihood of a worker accepting a firm’s offer of coverage also varies with the workforces’ wage level. Eligible employees in firms with a lower proportion of lower-wage workers are more likely to take up coverage (81%) than eligible employees in firms with a higher proportion of lower-wage workers (35% or more of workers earn $23,000 or less annually) (67%) (Exhibit 3.4). Similar patterns are seen in firms with a larger proportion of higher-wage workers, with workers in these firms being more likely to take up coverage than those in firms with a smaller share of higher wage workers (83% vs. 77%).

- Ninety-one percent of workers at public employers who offer health benefits take up coverage. Workers at private-for-profit employers are significantly less likely to do so – only 77% of these workers take up coverage (Exhibit 3.4).

Coverage

- There is significant variation by industry in the coverage rate among workers in firms offering health benefits. For example, only 37% of workers in retail firms offering health benefits are covered by the health benefits offered by their firm, compared to 74% of workers in finance, and 80% of workers in the transportation/communications/utilities industry category (Exhibit 3.2).

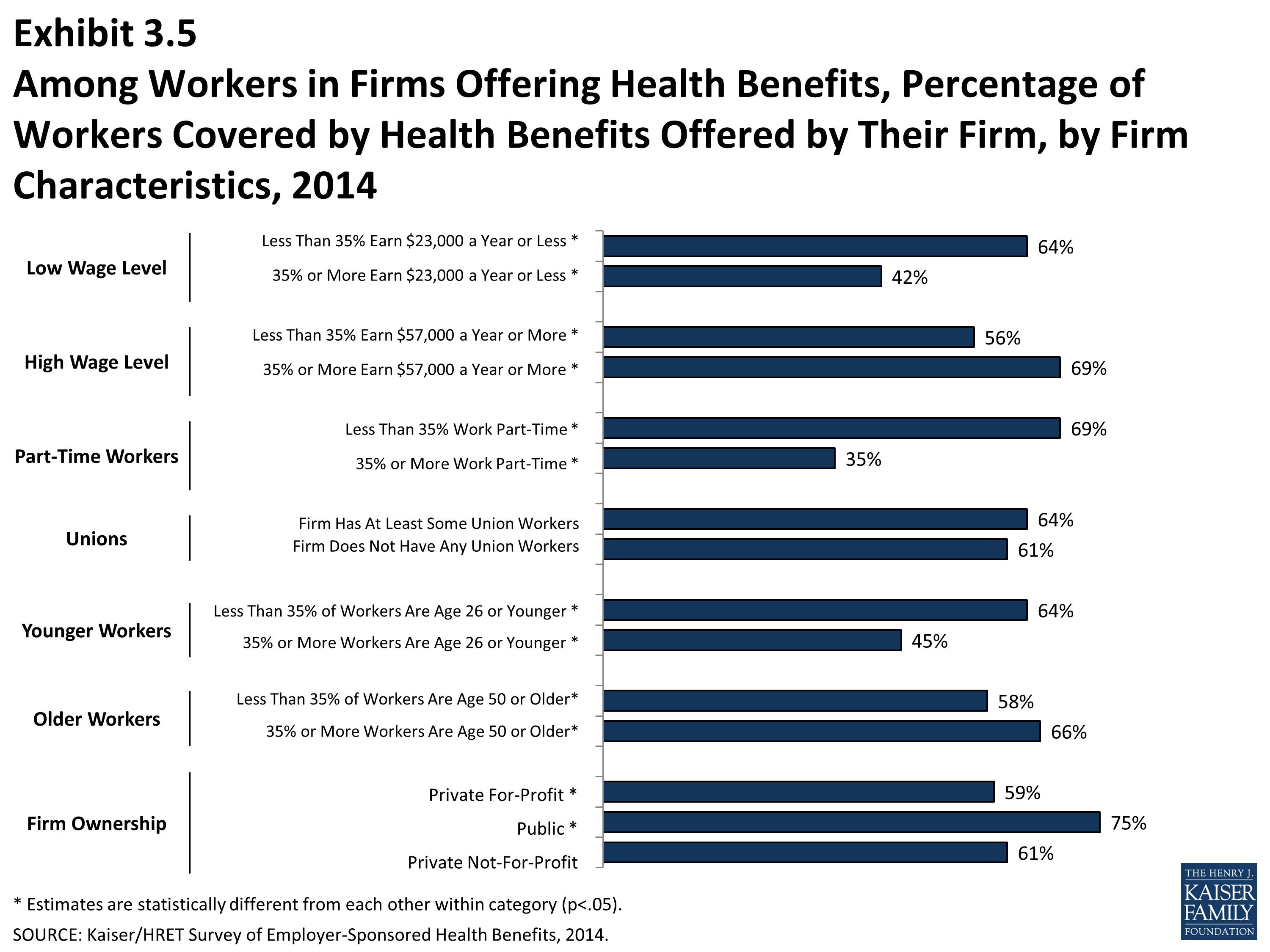

- Among workers in firms offering health benefits, those in firms with relatively few part-time workers (less than 35% of workers are part-time) are much more likely to be covered by their own firm than workers in firms with a greater percentage of part-time workers (69% vs. 35%) (Exhibit 3.5).

- Among workers in firms offering health benefits, those in firms with fewer lower-wage workers (less than 35% of workers earn $23,000 or less annually) are more likely to be covered by their own firm than workers in firms with many lower-wage workers (64% vs. 42%) (Exhibit 3.5). A comparable pattern exists in firms with a larger proportion of higher wage workers (35% or more earn $57,000 or more annually) offering health benefits (69% vs. 56%).

- Among workers in firms offering health benefits, those in firms with fewer younger workers (less than 35% of workers are age 26 or younger) are more likely to be covered by their own firm than those in firms with many younger workers (64% vs. 45%) (Exhibit 3.5).

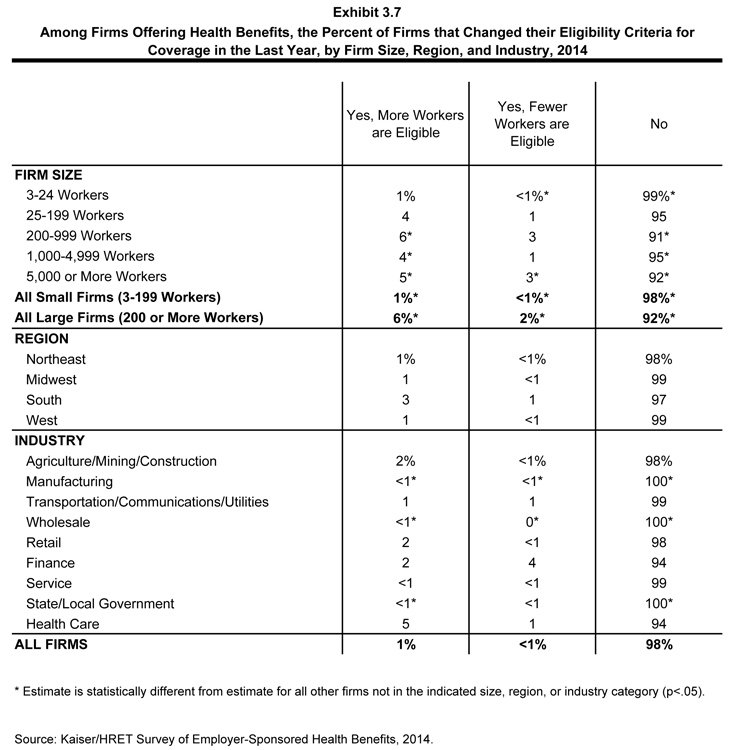

- Ninety-eight percent of firms offering health benefits reported that they did not change eligibility criteria by either increasing or decreasing the share of workers eligible for health benefits in the last year (Exhibit 3.7).

Waiting Periods

- Waiting periods are a specified length of time after beginning employment before employees are eligible to enroll in health benefits. The ACA requires that waiting periods cannot exceed 90 days for non-grandfathered plans for plan years that begin on or after January 1, 2014. This survey is conducted from January to May annually, at which time many firms report information on their current plans. In some cases those plan years may have started in the previous calendar year (in this case, 2013). Some employers may have renewed their plan year in 2013 in order to delay implementing provisions of the ACA slated to take effect on January 1 2014. Also, many covered workers are enrolled in grandfathered health which are exempt from certain provisions of the ACA including the requirement to have a waiting period of less than 90 days (for more information see Section 13). If an employee is eligible to enroll on the 1st of the month, after two months this survey “rounds-up” and say the firm’s waiting period is three months. For these reasons some employers still have waiting periods exceed the 90 day maximum.

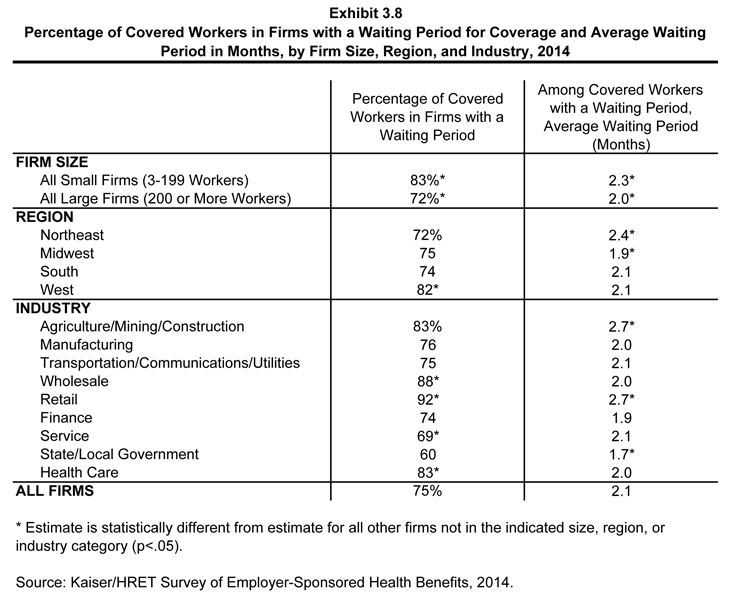

- Seventy-five percent of covered workers face a waiting period before coverage is available. Covered workers in small firms (3-199 workers) are more likely than those in large firms to have a waiting period, at 83% versus 72% (Exhibit 3.8). Workers in the West are more likely to face a wait for coverage than all other regions (82%).

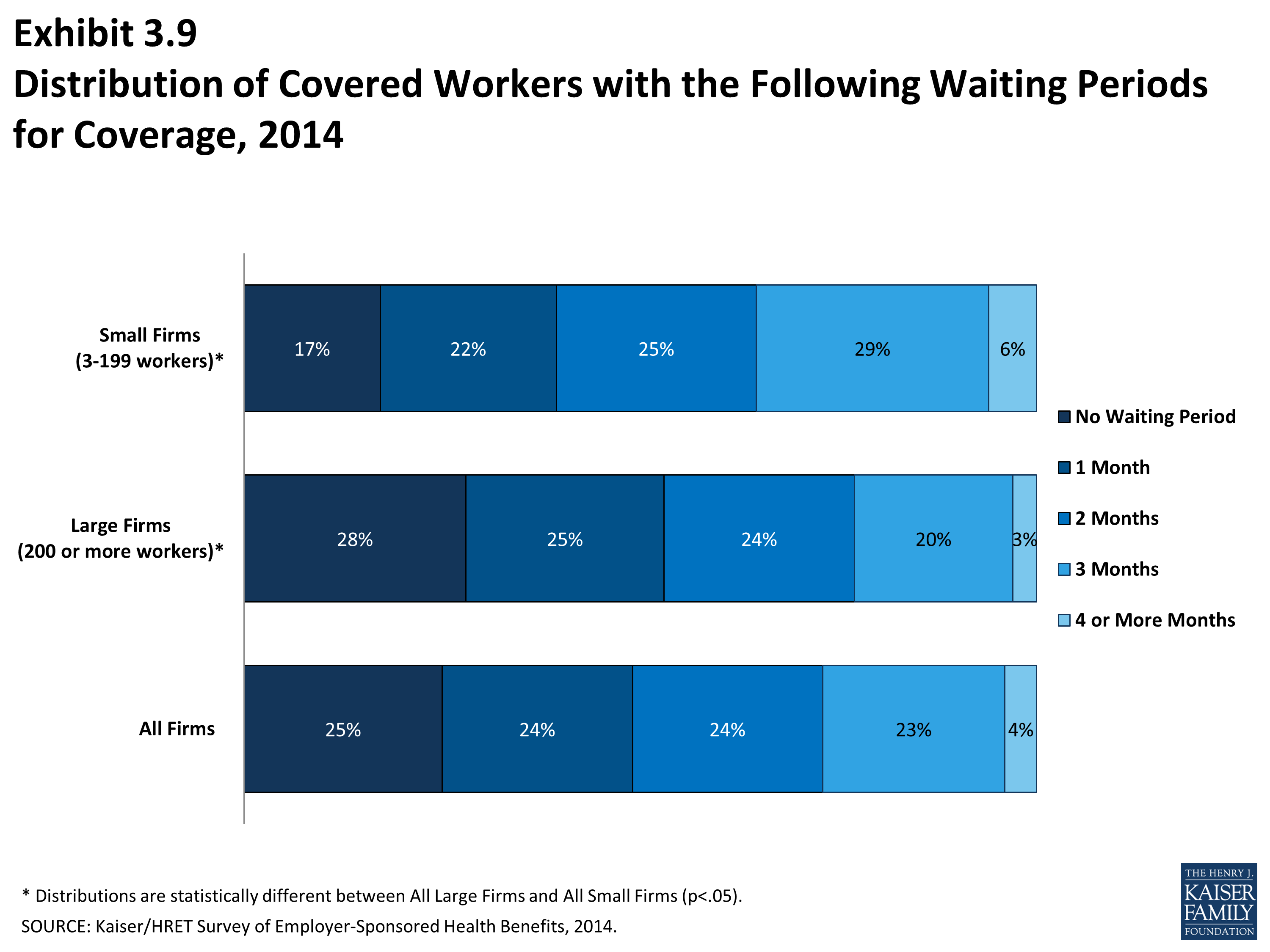

- The average waiting period among covered workers who face a waiting period is 2.1 months (Exhibit 3.8). While 27% of covered workers face a waiting period of 3 months or more, only 4% face a waiting period of 4 months or more. Workers in small firms (3-199 workers) generally have longer waiting periods than workers in larger firms (Exhibit 3.9).

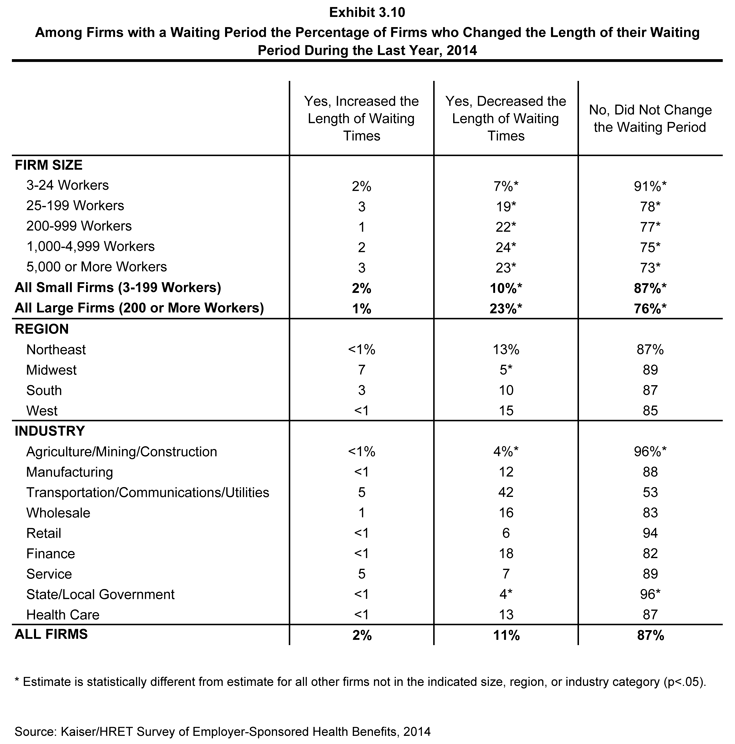

- In 2014, 11% of firms offering health benefits reported that they reduced the duration of the waiting period, significantly higher than the 2% that increased it (Exhibit 3.10).

- Ninety-one percent of covered workers at firms with many lower-wage workers (firms where 35% or more of the workforce makes $23,000 or less) face a waiting period before coverage is available compared to 76% at firms with few lower-wage workers.

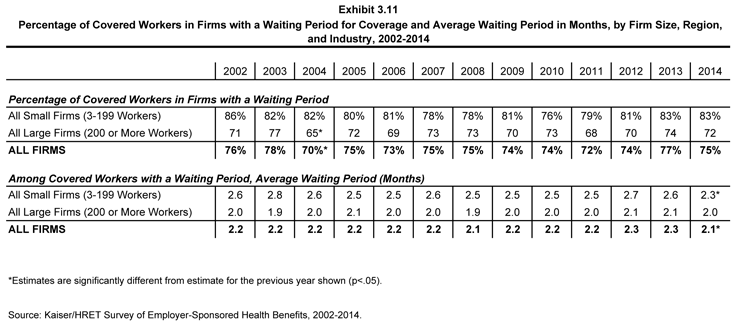

- The percentage of covered workers who face a waiting period is similar to last year. The average length of the waiting period for covered workers who face a waiting period decreased, however, from 2.3 months to 2.1 months (Exhibit 3.11).

Percentage of All Workers Covered by Their Employers’ Health Benefits, in Firms Both Offering and Not Offering Health Benefits, by Firm Size, 1999-2014

Eligibility, Take-Up Rate, and Coverage in Firms Offering Health Benefits, by Firm Size, Region, and Industry, 2014

Among Workers in Firms Offering Health Benefits, Percentage of Workers Eligible for Health Benefits Offered by Their Firm, by Firm Characteristics, 2014

Among Workers in Firms Offering Health Benefits, Percentage of Eligible Workers Who Take Up Health Benefits Offered by Their Firm, by Firm Characteristics, 2014

Among Workers in Firms Offering Health Benefits, Percentage of Workers Covered by Health Benefits Offered by Their Firm, by Firm Characteristics, 2014

Eligibility, Take-Up Rate, and Coverage for Workers in Firms Offering Health Benefits, by Firm Size, 1999-2014

Among Firms Offering Health Benefits, the Percent of Firms that Changed their Eligibility Criteria for Coverage in the Last Year, by Firm Size, Region, and Industry, 2014

Percentage of Covered Workers in Firms with a Waiting Period for Coverage and Average Waiting Period in Months, by Firm Size, Region, and Industry, 2014

Distribution of Covered Workers with the Following Waiting Periods for Coverage, 2014

Among Firms with a Waiting Period the Percentage of Firms who Changed the Length of their Waiting Period During the Last Year, 2014

Percentage of Covered Workers in Firms with a Waiting Period for Coverage and Average Waiting Period in Months, by Firm Size, Region, and Industry, 2002-2014

x

Exhibit 3.2

x

Exhibit 3.1

x

Exhibit 3.3

x

Exhibit 3.4

x

Exhibit 3.5

x

Exhibit 3.7

x

Exhibit 3.8

x

Exhibit 3.9

x

Exhibit 3.10

x