Who Might Lose Eligibility for Affordable Care Act Marketplace Subsidies if Enhanced Tax Credits Are Not Extended?

Enhanced subsidies for Affordable Care Act (ACA) Marketplace plans are set to expire at the end of 2025, unless they are renewed by Congress. Since 2021, these enhanced subsidies have lowered monthly premium payments for the vast majority of Marketplace enrollees, across incomes. For example, instead of a lower-income person paying 2% of their income on their premium, they pay nothing. Higher income people currently pay no more than 8.5% of their income on their premium, whereas they were originally ineligible for financial assistance.

While virtually all subsidized ACA enrollees can expect to see their premium payments rise substantially without extension of these subsidies, most will still be eligible for some financial assistance (with the original ACA subsidies). However, those who earn more than four times the federal poverty level ($62,600 for an individual or $128,600 for a family of four with 2026 coverage) would lose eligibility for subsidies altogether and would therefore have to pay full price for their health plans. Based on 2025 premiums, for example, a 60-year-old couple earning $85,000 annually (416% of the federal poverty level in the contiguous 48 states), would see their monthly premium payment increase by $1,507 per month (an increase in payments of over $18,000 for the year), on average.

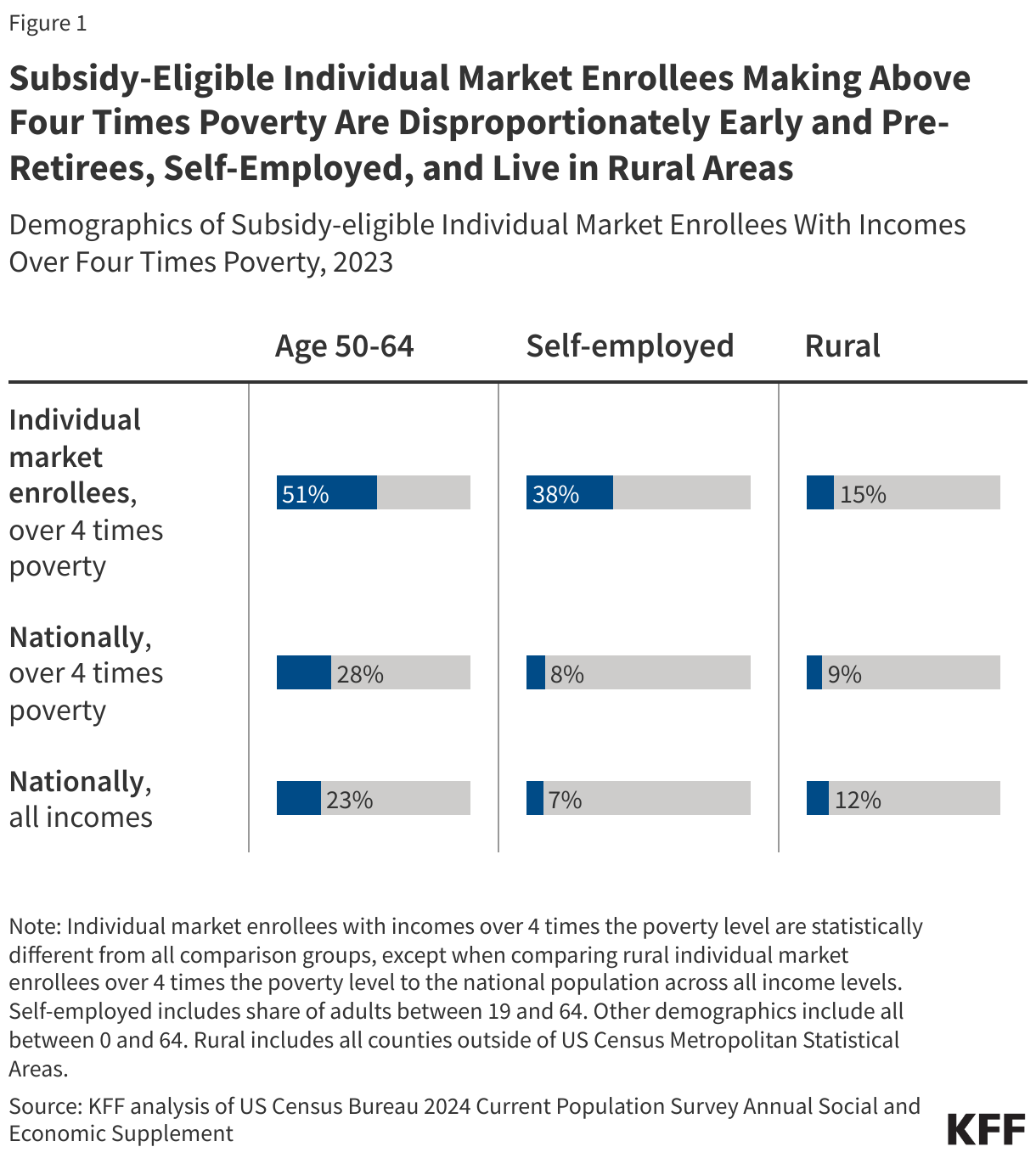

Relative to other Americans, subsidy-eligible individual market enrollees with incomes over four times poverty (who would lose subsidy eligibility if enhanced tax credits expire) are disproportionately:

- Early and pre-retirees: About half (51%) of enrollees with incomes over four times poverty who would lose subsidy eligibility are between the ages of 50 and 64, compared to 23% of the non-elderly U.S. population.

- Self-employed: Among non-elderly adults (ages 19 to 64) with incomes over four times poverty who would lose ACA subsidy eligibility, 38% are self-employed, compared to 7% of non-elderly adults (19-64) nationally. Small business owners often rely on the ACA Marketplaces because they do not have employer-sponsored insurance.

- Living in rural areas: 15% of people with individual market insurance who would lose subsidy eligibility live outside metropolitan areas, compared to 9% of Americans with incomes over four times poverty. (12% of all Americans live in rural area; this is not statistically different from the share of people who would lose subsidy eligibility living in rural areas.)

Relatively few Marketplace enrollees have incomes above four times poverty. According to administrative data, in 2024, 7% of Marketplace enrollees reported an income over four times poverty, with 3% having an income between four and five times poverty and another 4% with incomes over five times poverty (another 4% did not have a known income and may have also exceeded four times the poverty level, but most likely are not receiving an advanced premium tax credit). However, before the enhanced subsidies were introduced – and particularly in 2017 when there were large premium increases and debates about repealing the ACA – this group of people with incomes over four times poverty were the focus of a great deal of media attention because they were fully exposed to the underlying premiums. For those who were priced out of coverage before the enhanced subsidies, they often faced a choice of being uninsured, or – if they were healthy enough to qualify – buying a short-term (non-ACA-compliant) plan off of the Marketplace.

Note: The data above is based on KFF analysis of the 2024 Current Population Survey Annual Social and Economic Supplement. The analysis includes people under age 65 who buy individual market insurance, are subsidy eligible, and would receive a subsidy based on household income. Household offer units were imputed as described previously; enrollees were considered not subsidy eligible if a member of the unit reported being offered employer-sponsored insurance.