Medicare Spending was 27% More for People who Disenrolled from Medicare Advantage than for Similar People in Traditional Medicare

Issue Brief

More than half (54%) of eligible Medicare beneficiaries are enrolled in a private Medicare Advantage plan in 2024. People are drawn to Medicare Advantage because most plans offer extra benefits and lower cost sharing compared to traditional Medicare without supplemental insurance, usually for no additional premium (other than the Part B premium). Medicare Advantage is also popular among lawmakers in Congress, both Republicans and Democrats, as well as President-elect Trump, whose previous administration generally supported policies that provided increased flexibilities to insurers when designing and administering these private plans.

Though Medicare Advantage is a popular choice for Medicare beneficiaries, there is some evidence that people who use relatively more health care services are less likely to choose a private plan and more likely to choose traditional Medicare. Previous analyses from KFF and the Medicare Payment Advisory Commission (MedPAC) found that people who enroll in Medicare Advantage have lower Medicare spending in the years before they enroll than similar people who remain in traditional Medicare, even after controlling for health status. This pattern may be partly attributable to concerns about the tools Medicare Advantage plans typically use to manage utilization and costs, such as prior authorization requirements and provider network restrictions.

This analysis looks at traditional Medicare spending among people who choose to disenroll from Medicare Advantage and obtain coverage under traditional Medicare during the annual Medicare open enrollment period. It compares their traditional Medicare spending (Parts A and B) in the year following disenrollment to similar people who were continuously covered by traditional Medicare (see Appendix for characteristics of each group), using data from the Medicare Master Beneficiary Summary File (MBSF) for 2021 and 2022 (see Methods).

Key Takeaways

- Medicare spent 27% more, on average, for people who were covered by traditional Medicare after disenrolling from Medicare Advantage than for people who were continuously covered by traditional Medicare, after adjusting for differences in health status and other characteristics. This is a difference of $2,585 in Medicare spending per person, on average, between the two groups in 2022.

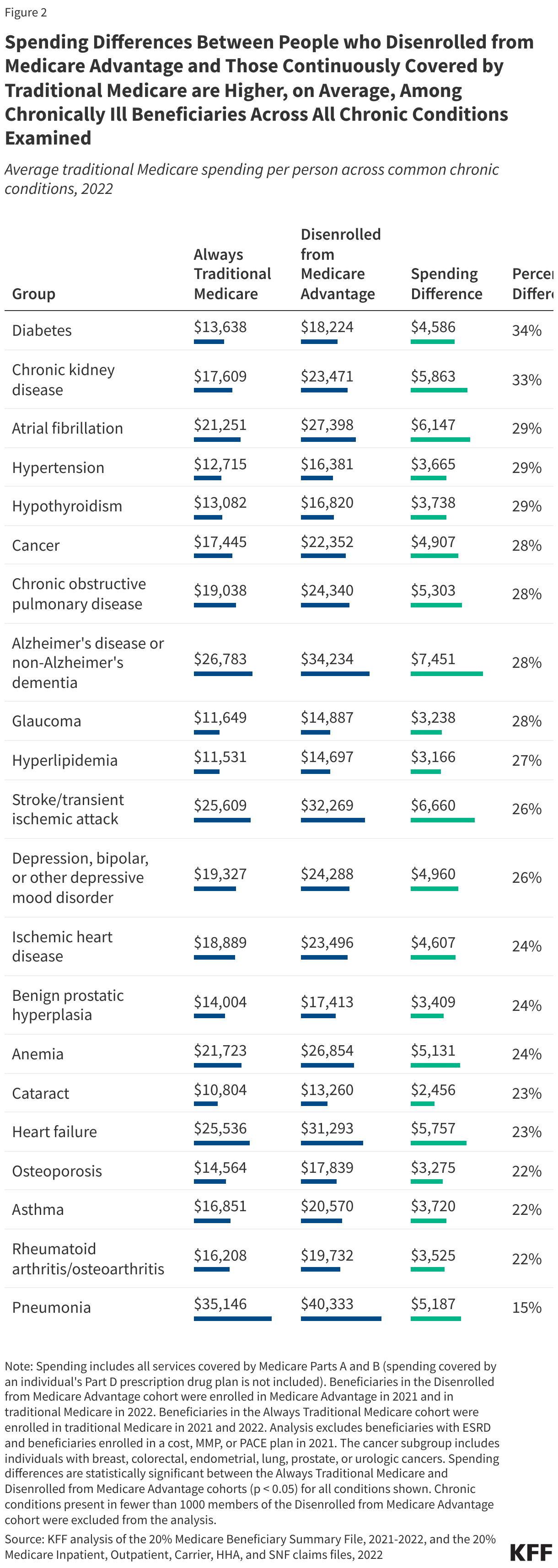

- Differences in Medicare spending between people who disenrolled from Medicare Advantage and beneficiaries continuously in traditional Medicare varied by health condition, ranging from 15% for people with pneumonia to 34% for people with diabetes. For example, among people with certain cancers, Medicare spending was 28% ($4,907) higher, on average, among those who disenrolled from Medicare Advantage than among people continuously covered by traditional Medicare.

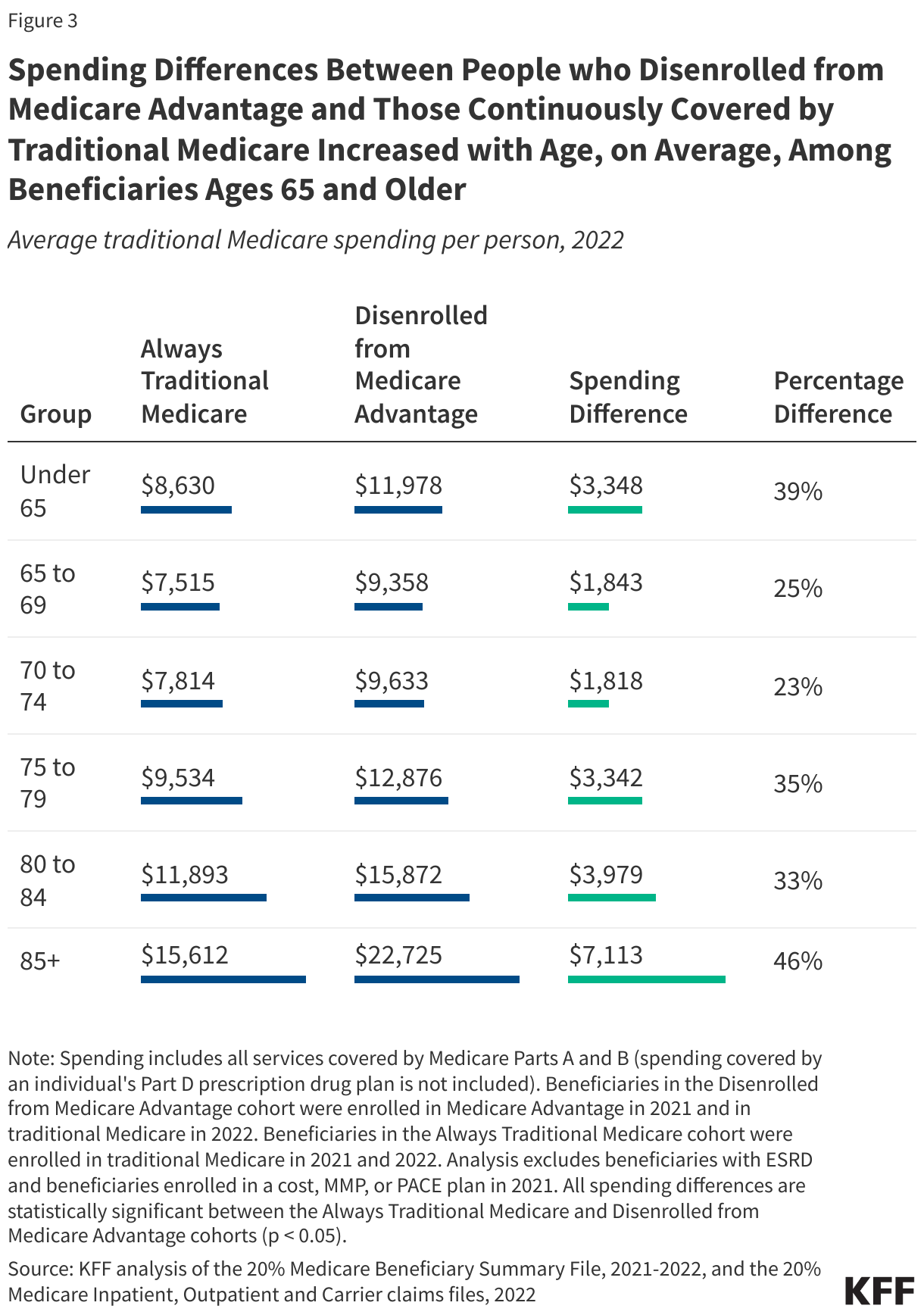

- Differences in Medicare spending between people who disenrolled from Medicare Advantage and those continuously in traditional Medicare increased with age for Medicare beneficiaries ages 65 and over. For example, among people ages 85 and over the difference was 46% ($7,113) compared to 25% among people ages 65 to 69 ($1,843).

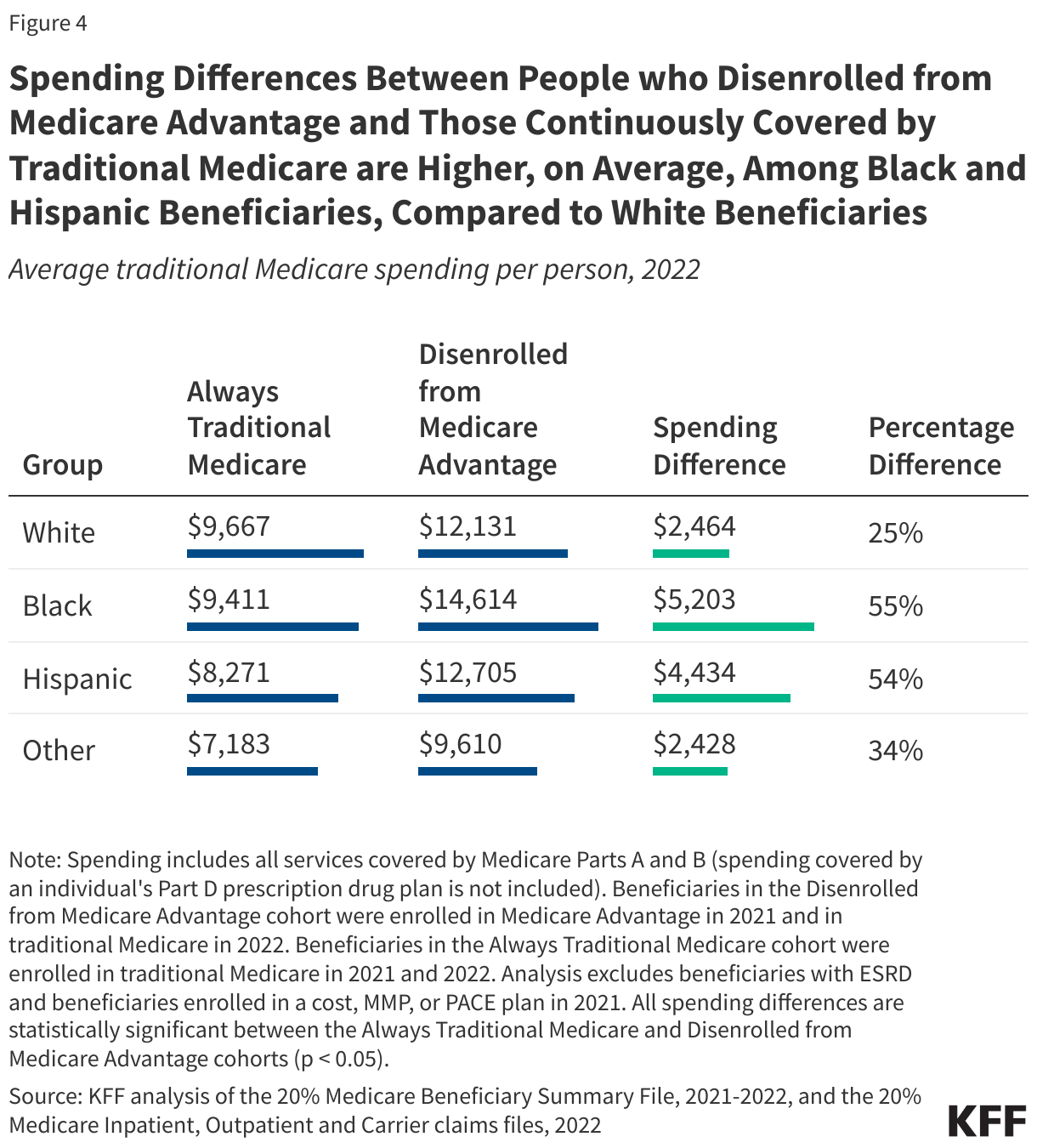

- Differences in Medicare spending between people who disenrolled from Medicare Advantage and beneficiaries continuously in traditional Medicare were larger among Black (55%, $5,203) and Hispanic (54%, $4,434) beneficiaries than White beneficiaries (25%, $2,464).

- People dually-eligible for Medicare and full Medicaid benefits who disenrolled from Medicare Advantage had spending that was 61% ($9,435) higher than their counterparts who were continuously in traditional Medicare, while the difference in spending for Medicare beneficiaries who do not receive Medicaid was 20% ($1,684).

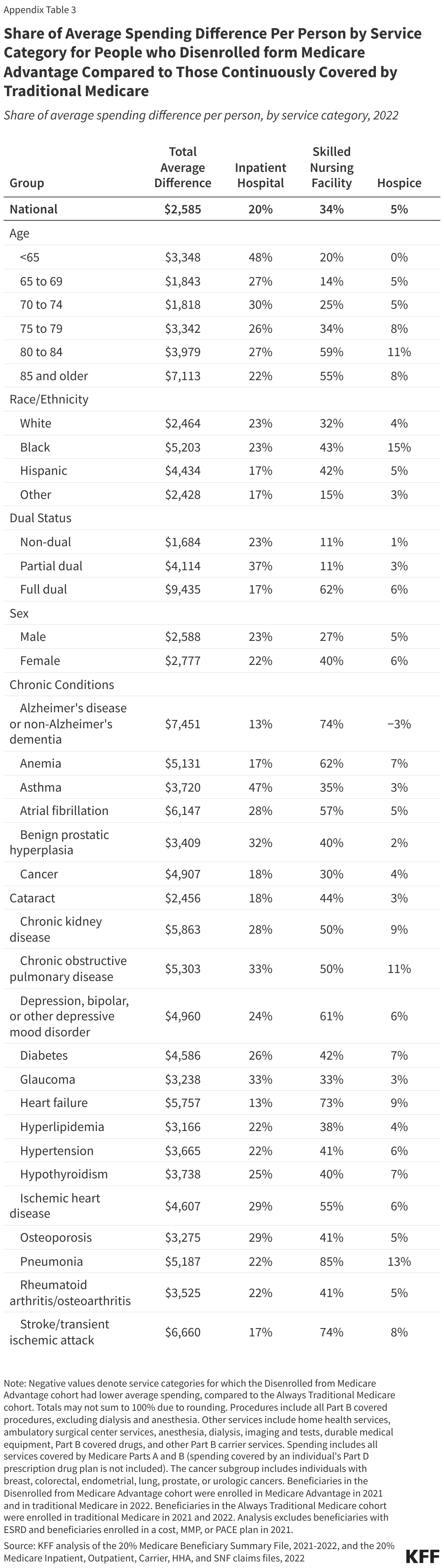

- Skilled nursing facility spending accounted for the largest share of the difference in average Medicare spending per person between people who disenrolled from Medicare Advantage and those continuously in traditional Medicare (34%), followed by outpatient hospital spending (23%), and inpatient hospital spending (20%), with some variation by chronic conditions and other beneficiary characteristics.

The substantially higher Medicare spending among people who disenrolled from Medicare Advantage, on average, compared to similar people who were continuously covered by traditional Medicare raises several questions. First, why are some Medicare Advantage enrollees choosing to disenroll from Medicare Advantage rather than get the medical care they need from their plan, and why are they receiving more medical care in the year following disenrollment than similar people who have been continuously covered by traditional Medicare?

Second, given how challenging it can be for people with pre-existing conditions to purchase Medicare supplemental insurance (Medigap) if they switch to traditional Medicare, and concerns about potentially high out-of-pocket costs under traditional Medicare without supplemental coverage, what share of Medicare Advantage enrollees would want to switch to traditional Medicare, but feel they cannot afford to do so?

Third, does the current payment system adequately account for adverse selection into traditional Medicare, which leads to higher Medicare Advantage benchmarks and higher payments to Medicare Advantage plans? Additionally, to what extent does the pattern of higher utilization and spending among people who disenroll from Medicare Advantage, reduce the costs incurred by insurers, increasing their profits and contributing to their ability to offer supplemental benefits? Finally, how does higher Medicare spending among people who disenroll from Medicare Advantage impact Medicare spending, and to what extent does it place added strain on the Medicare Hospital Insurance Trust Fund and increase beneficiary premiums?

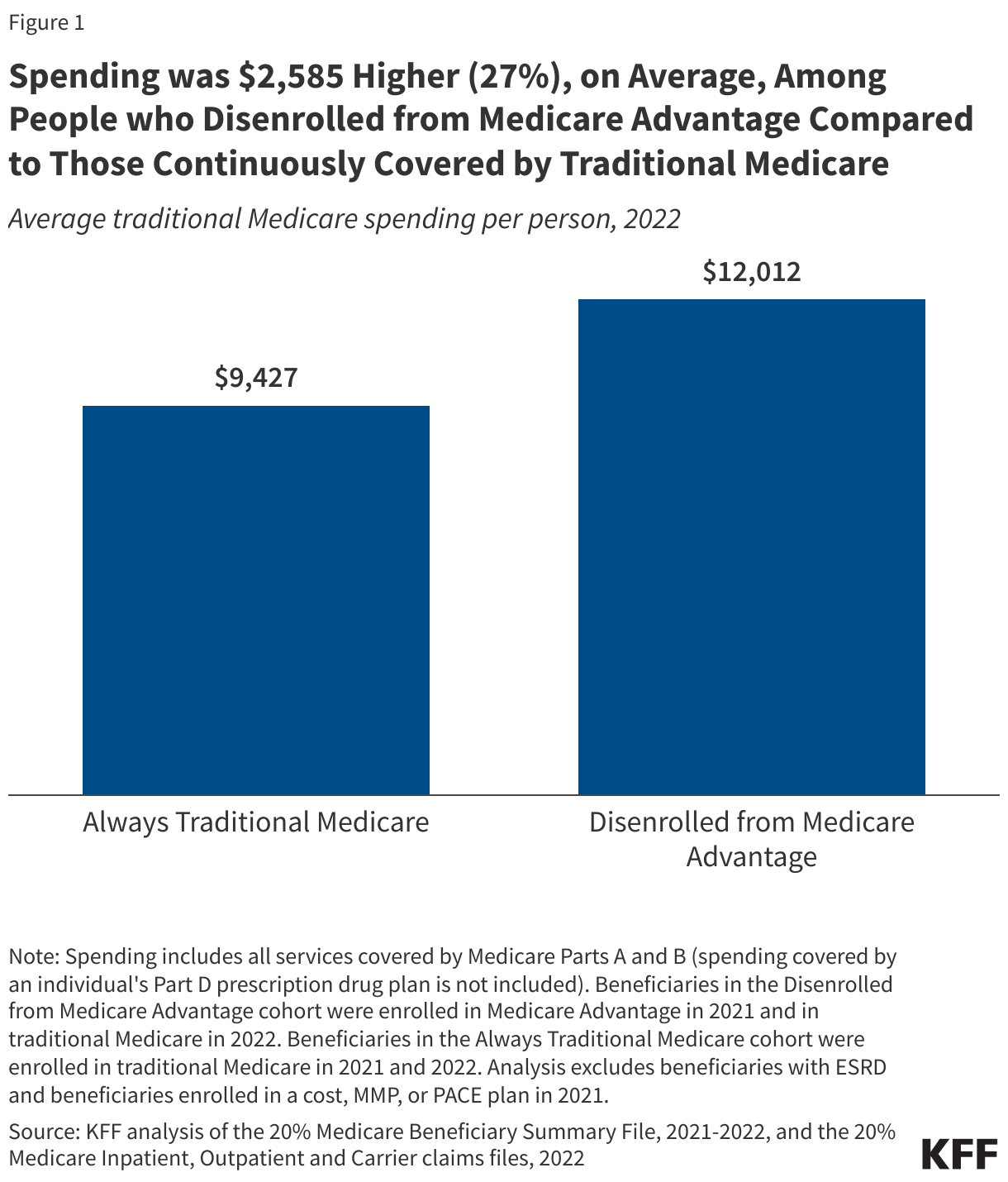

People who disenrolled from Medicare Advantage had Medicare spending that was 27% more, on average, than spending for similar people continuously covered by traditional Medicare

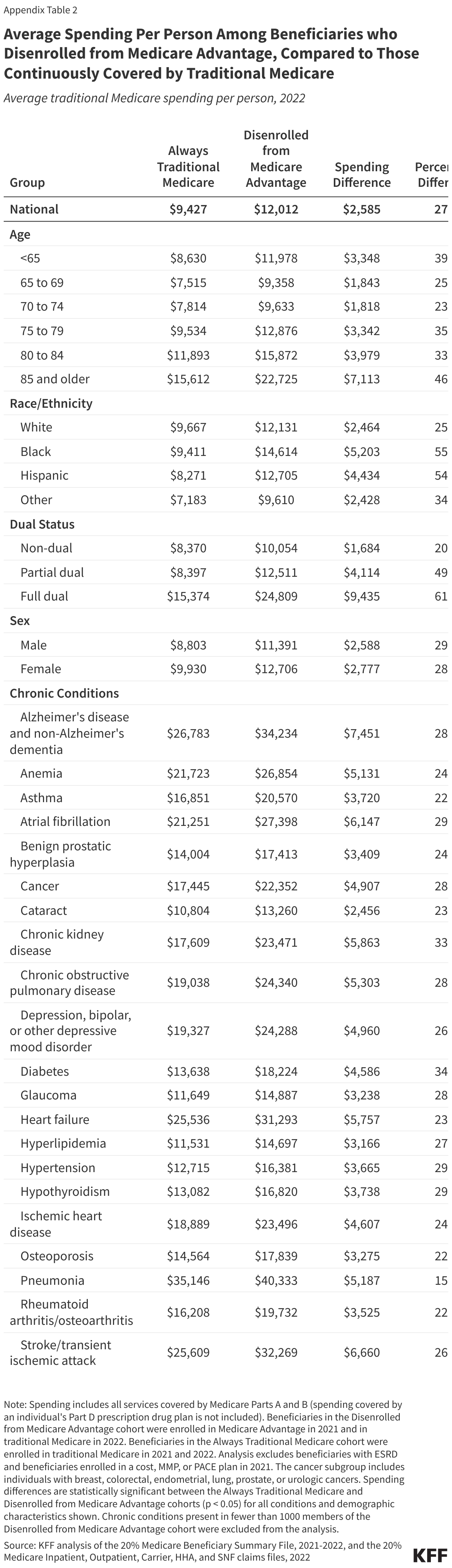

Overall, people who disenrolled from Medicare Advantage had Medicare spending that was 27% ($2,585) higher, on average, than those continuously covered by traditional Medicare, after adjusting for differences in health risk factors (Figure 1).

Several studies have found that certain groups of Medicare Advantage enrollees switch to traditional Medicare at higher rates, including beneficiaries in their last year of life, those with higher health needs, and those dually eligible for Medicare and Medicaid. Furthermore, some groups with high disenrollment rates, such as beneficiaries in their last year of life, have higher health care spending after they disenroll compared to similar beneficiaries who are long-time recipients of traditional Medicare.

This analysis shows that spending differences are not limited to those particularly high-need groups because the spending differences persist after controlling for health risk, though the magnitude of the difference is greater, on average, for high-cost beneficiaries. While prior research finds lower health care spending among people who enroll in Medicare Advantage, in the year prior to enrollment, this analysis shows that people who disenroll from Medicare Advantage use more services and incur higher Medicare costs in the year following disenrollment than similar beneficiaries who were continuously covered under traditional Medicare.

People who disenrolled from Medicare Advantage had higher spending, on average, than those continuously covered by traditional Medicare across all chronic health conditions examined

People who disenrolled from Medicare Advantage had higher Medicare spending, on average, across all chronic health conditions examined, after adjusting for other health risk factors, than those continuously covered by traditional Medicare (Figure 2, Appendix Table 2). Differences in average per person spending varied by condition, ranging from 15% ($5,187) for people with pneumonia to 34% ($4,586) for people with diabetes. The largest difference in Medicare spending per person in dollar terms between people who disenrolled from Medicare Advantage and those continuously in traditional Medicare was among people with Alzheimer’s disease or other dementias ($7,451), followed by stroke ($6,660), and atrial fibrillation ($6,147). Among people with certain cancers, including breast, colorectal, endometrial, lung, prostate, and urologic cancers, spending for people who disenrolled from Medicare Advantage was 28% ($4,907) higher than for people continuously covered by traditional Medicare.

People with greater health needs may see multiple health care providers and require numerous specialty services, resulting in a greater burden from the limited provider networks, prior authorization, and referral requirements Medicare Advantage plans often employ. Prior authorization is most often required for high-cost services, such as chemotherapy and other Part B drugs, inpatient hospital stays, and stays in skilled nursing facilities. In addition, narrow provider networks may limit available options for treatment of certain conditions. For instance, prior studies have found that Medicare Advantage enrollees are less likely than traditional Medicare beneficiaries to receive care from the highest rated hospitals for treatment of cancer or cancer-related surgical procedures.

Average differences in Medicare spending between people who disenrolled from Medicare Advantage and those continuously covered by traditional Medicare increased with age among beneficiaries ages 65 and older

Across all age groups, people who disenrolled form Medicare Advantage had higher Medicare spending, on average, than those continuously covered by traditional Medicare. Average differences in per person spending increased with age among older beneficiaries, from 25% ($1,843) among those ages 65-69 to 46% ($7,113) among those ages 85 and older. People under the age of 65, who qualify for Medicare due to long-term disability, have somewhat higher average spending per person than Medicare beneficiaries between the ages of 65 and 74, and the differences in spending among this group between those who disenrolled from Medicare Advantage and those continuously covered by traditional Medicare were also somewhat larger (39%, $3,348) (Figure 3).

Average differences in Medicare spending between people who disenrolled from Medicare Advantage and those continuously covered by traditional Medicare were higher among Black and Hispanic than White beneficiaries

Across all racial and ethnic groups examined, people who disenrolled from Medicare Advantage had higher Medicare spending, on average, than those continuously covered by traditional Medicare. Average differences in per person spending were approximately two times higher among Black (55%, $5,203) and Hispanic (54%, $4,434) beneficiaries than among White beneficiaries (25%, $2,464) (Figure 4).

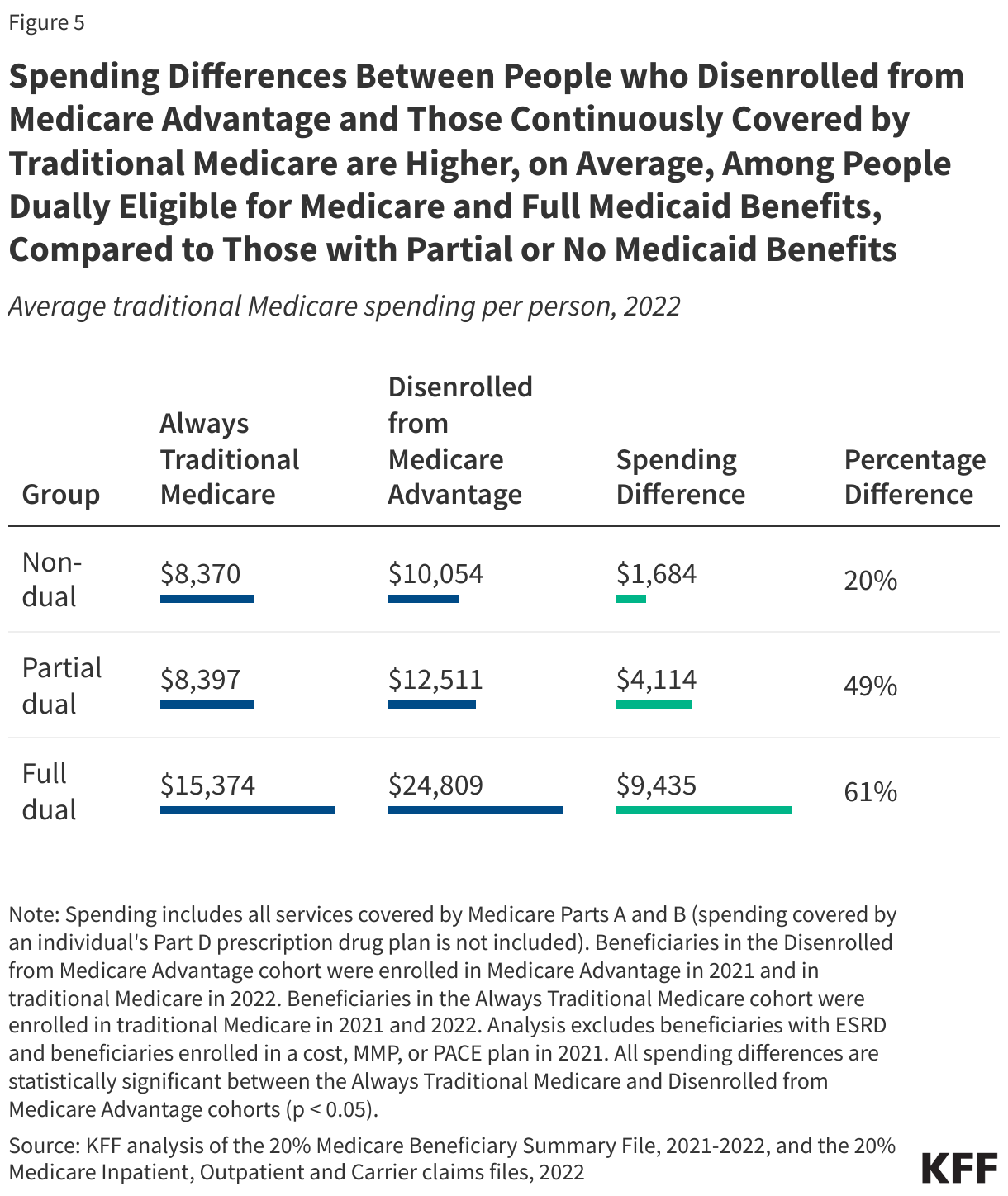

Average differences in Medicare spending between people who disenrolled from Medicare Advantage and those continuously covered by traditional Medicare were higher among people dually eligible for Medicare and full Medicaid benefits

Among dual-eligible beneficiaries who qualified for full Medicaid benefits, those who disenrolled from Medicare Advantage had spending that was 61% ($9,435) higher, on average, than those continuously covered by traditional Medicare. Average differences in per person spending were smaller among beneficiaries who were not dual-eligible (20%, $1,684) and among dual-eligible beneficiaries who qualified for assistance with Medicare premiums, and in some cases cost sharing, but not full Medicaid benefits (partial-benefit dual-eligible beneficiaries) (49%, $4,114) (Figure 5).

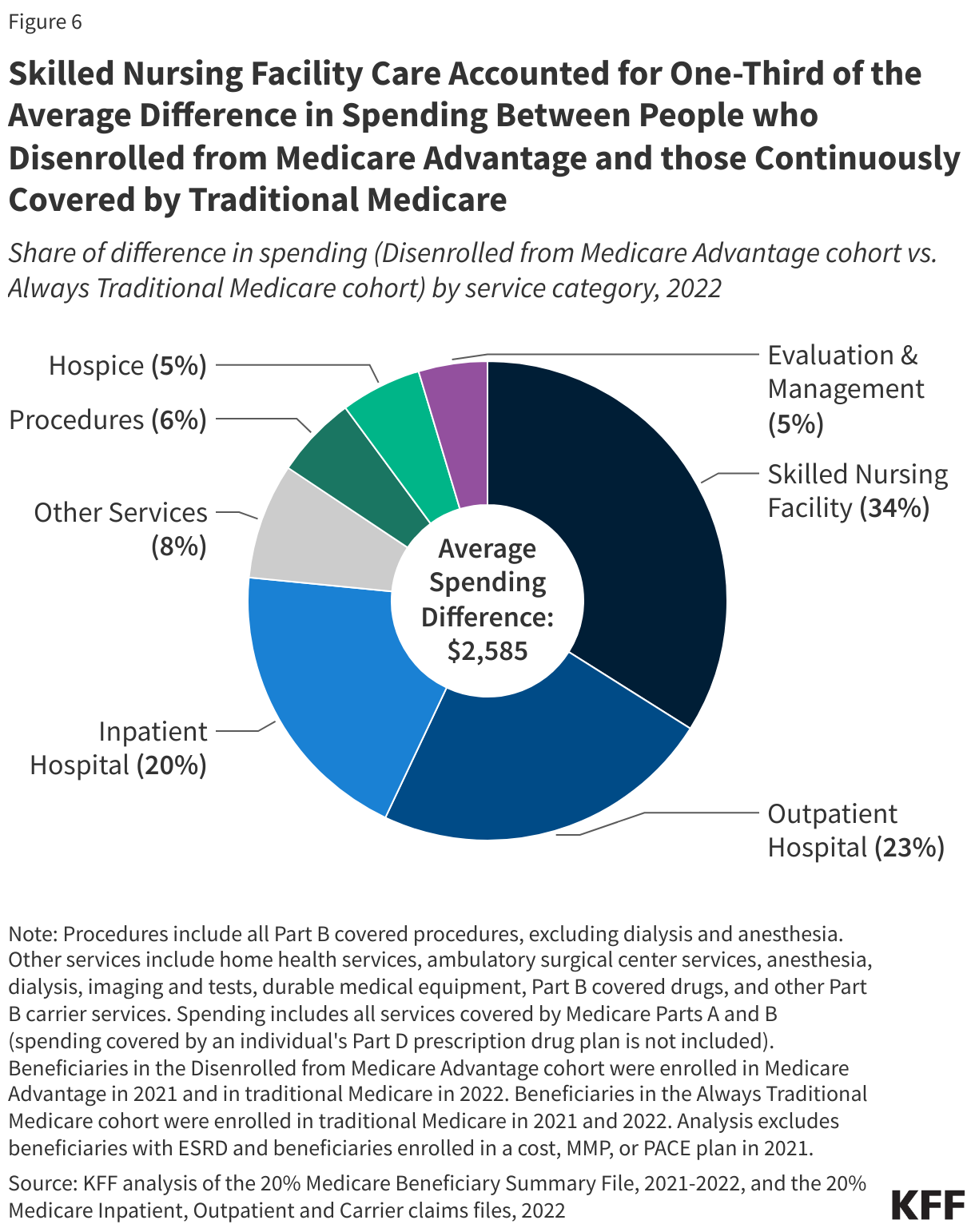

Skilled nursing facility and hospital care accounted for more than three-quarters of the average difference in Medicare spending between people who disenrolled from Medicare Advantage and those continuously covered by traditional Medicare

Skilled nursing facility services accounted for the largest share (34%, $877) of the average difference in per person spending between people who disenrolled from Medicare Advantage and those continuously covered by traditional Medicare, followed by outpatient hospital services (23%, $596) and inpatient hospital services (20%, $505) (Figure 6).

For certain groups, the total difference in average per person spending between people who disenrolled from Medicare Advantage and those continuously covered by Medicare Advantage was largely driven by skilled nursing facility services. These included dual-eligible beneficiaries with full Medicaid benefits (62%), beneficiaries ages 80 to 84 (59%) and ages 85 and older (55%), and beneficiaries with pneumonia (85%), Alzheimer’s disease or other dementias (74%), stroke (74%), and heart failure (73%) (Appendix Table 3). By contrast, skilled nursing facility services made up a smaller share of the total difference in average spending among people under age 65 (20%) and those ages 65 to 69 (14%).

Among other groups, inpatient hospital services made up a larger share of the difference in average spending, including among beneficiaries under age 65 with long-term disabilities (48%), as well as among beneficiaries with asthma (47%), glaucoma (33%), and chronic obstructive pulmonary disease (33%). Beneficiaries with certain cancers had among the highest share of the total difference in average spending attributed to outpatient hospital services (34%), a similar share attributed to skilled nursing facility services (30%) and a relatively modest share of the difference attributed to spending on inpatient hospital services (18%).

Consistent with this analysis, a recent report by the majority staff of the Senate Permanent Subcommittee on Investigations found that Medicare Advantage plans are more likely to deny prior authorization requests for coverage of post-acute care, such as skilled nursing facility stays, than for other types of services.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Appendix

Methods

This analysis uses data from the 20% Medicare Master Beneficiary Summary File (MBSF) and Medicare claims files to compare Medicare spending (across Parts A and B) for beneficiaries who were previously enrolled in Medicare Advantage (Disenrolled from Medicare Advantage) to beneficiaries who have been continuously covered by traditional Medicare (Always Traditional Medicare). The Disenrolled from Medicare Advantage cohort includes people who were enrolled in Medicare Advantage in 2021 and in traditional Medicare in 2022. The Always Traditional Medicare cohort of beneficiaries were enrolled in traditional Medicare in both 2021 and 2022.

To be included in either cohort, beneficiaries had to have 12 months of coverage under Medicare Part A and Part B in 2021, as well as coverage in Parts A and B in all months in 2022 they were enrolled in Medicare (i.e., not deceased). The analysis includes all 50 states and DC. People with ESRD are excluded because 2021 was the first year people with ESRD were broadly eligible to enroll in a Medicare Advantage plan. For the Disenrolled from Medicare Advantage cohort, the analysis excludes people who were enrolled in a cost plan, Medicare Medicaid plan, or PACE plan in 2021.

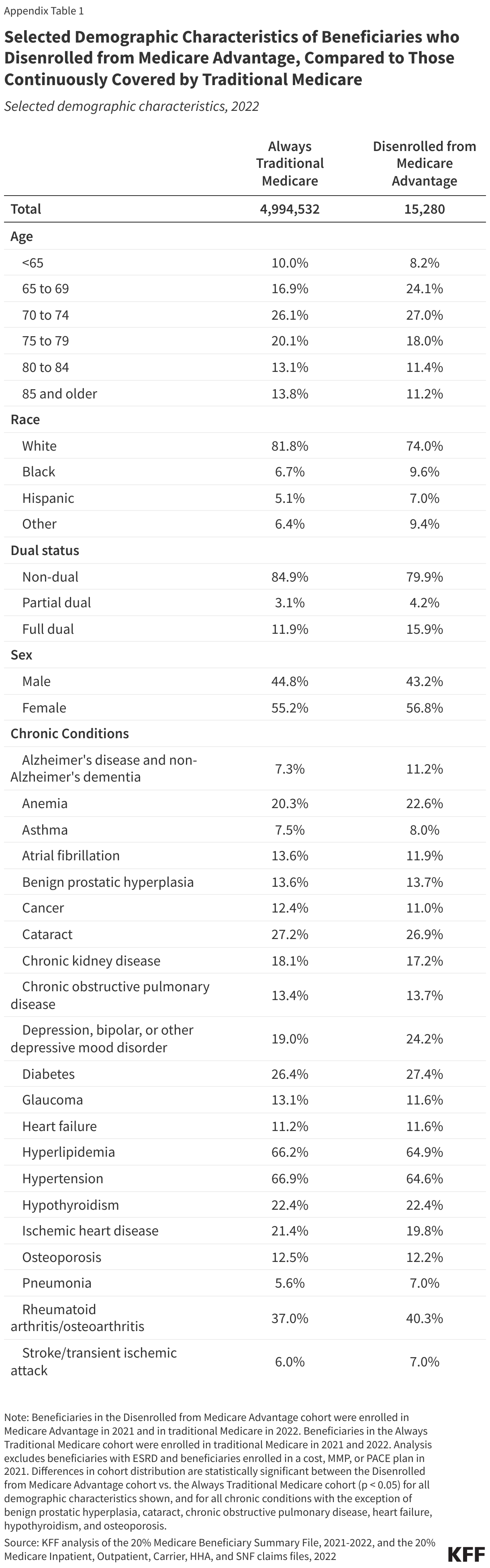

Compared to the Always Traditional Medicare cohort, a somewhat larger share of the Disenrolled from Medicare Advantage cohort were ages 65 to 69 (24% vs. 17%), Black (10% vs. 7%) or Hispanic (7% vs. 5%), or dually eligible for Medicare and full Medicaid benefits (16% vs. 12%). There were also differences in the share of beneficiaries with certain health conditions (Appendix Table 1). To account for differences in age, dual eligibility, and health status, the risk score for each person was calculated using the CMS-HCC Risk Adjustment model based on diagnoses present in 2022. Note that the risk model is used to adjust payments to Medicare Advantage plans and does not account for race. Thus our approach also does not control for race and ethnicity.

Compared to all people enrolled in Medicare Advantage in 2021, those who disenrolled were more likely to have been covered by traditional Medicare in 2020 than those who stayed enrolled in Medicare Advantage. Specifically, among people who disenrolled from Medicare Advantage, 31% were covered by traditional Medicare in 2020; among people who stayed in Medicare Advantage, 11% were in traditional Medicare in 2020. These differences may be driven by the ability for people to return to the same Medigap policy within 12-months after switching to Medicare Advantage for the first time (note, Medicare beneficiaries are limited to a single “trial period”), relieving concerns about Medigap underwriting or cost sharing without a supplemental policy for some subset of people who disenrolled. We are unable to determine what share of the people who disenrolled from Medicare Advantage were in their “trial period” because it was the first time they had tried Medicare Advantage.

Our approach to analyzing spending follows the approach used by MedPAC in calculating average spending for people who switch from traditional Medicare to Medicare Advantage compared to those who remain in traditional Medicare. First, all Medicare payments, beneficiary liability, and other primary payer payments for all Part A and Part B services were summed for each person in the sample for Calendar Year 2022. Next, each person’s total spending is divided by their risk score (calculated using the CMS-HCC Risk Adjustment model and 2022 diagnoses) to derive risk-standardized spending, which allows for comparisons on an apple-to-apple basis for people with differences in health risk (such as differences in diagnosed health conditions). Within each county, the risk-standardized spending for each cohort is then averaged. To estimate spending given the health risk of the population of people who disenrolled from Medicare Advantage, the risk-standardized spending is then multiplied by the average risk score of people who disenrolled from Medicare Advantage. The national average spending for each cohort is then calculated as a weighted average of each county spending, using the number of people who disenrolled from Medicare Advantage as the weight. Counties in which no beneficiaries disenrolled from Medicare Advantage are excluded from the analysis. For each subgroup analysis a similar approach is followed, limiting the sample to people with the specific characteristic.

The Medicare Chronic Conditions Warehouse definitions for chronic conditions were used as a basis for identifying people with specific chronic conditions. To maintain consistency across the cohorts, only the 2022 claims were used. At least 1,000 members of the Disenrolled from Medicare Advantage cohort had to have a chronic condition for it to be included in the list.

Additionally, to test the sensitivity of the analysis, spending was modeled using a regression that controlled for risk score and county. The regression was specified using both a general linear model with a log link and a probit model. The average difference in each case was similar to those presented in this brief.

Overview of Medicare Advantage Payments

Medicare pays Medicare Advantage plans, in part, based on county-level spending for similar people in traditional Medicare, though payments may be higher or lower depending on a range of factors, such as a plan’s quality star rating, the county in which it operates, and the amount requested annually by the plan (referred to as a plan’s “bid”).

Plans that bid above traditional Medicare spending must charge enrollees an additional premium to make up the difference in cost. A growing number of plans choose to bid below traditional Medicare spending, which allows them to recoup a portion of the savings as a “rebate.” Rebates must be put towards certain plan features, such as lower cost-sharing, reductions to enrollees’ Part B or Part D premiums, or extra benefits (such as dental, vision, and hearing) not included in traditional Medicare. Payments are further adjusted to reflect the health status of enrollees, as well as certain other characteristics, such as age, sex, and Medicaid enrollment. Plans whose enrollees are expected to incur larger health costs receive larger payments (a process referred to as “risk adjustment”).

The Medicare Payment Advisory Commission estimates that payment to Medicare Advantage insurers is 122% of Medicare spending for similar beneficiaries covered by traditional Medicare. The higher payments are driven by favorable selection into Medicare Advantage and more intense coding of diagnoses among these plans. Those higher payments allow Medicare Advantage insurers to offer additional benefits and lower out-of-pocket spending, but place pressure on the hospital insurance trust fund and raise Medicare Part B premiums for all beneficiaries, including those in traditional Medicare.