In 2024, A Majority of States Offer Medicare Advantage Plans to Their State Retirees, with 13 Offering Medicare Advantage Exclusively

This analysis, originally published on May 22, 2024, has been updated based on a review of Michigan’s retiree health benefits.

The share of large employers offering health benefits to retirees has been declining over time, dropping to 21 percent in 2023 according to KFF’s Employer Health Benefits Survey, though with substantially higher offer rates among public employers, such as state and municipal governments, than among private employers. In 2024, nearly all states and the District of Columbia (DC) provide some health benefits to their Medicare-age retirees.

Until fairly recently, employer-sponsored health benefits for Medicare-age retirees were typically designed to supplement, wrap around or coordinate with traditional Medicare. These plans often cover some or all of Medicare’s coinsurance and deductibles, and sometimes cover other benefits not covered by Medicare, such as dental and vision. Over the past few years, many states have shifted their approach and are now fulfilling their retiree health obligations by offering coverage through Medicare Advantage plans, mirroring a similar trend observed among large employers who have been shifting their retiree coverage to Medicare Advantage. Medicare Advantage plans are private plans – such as PPOs or HMOs – that provide all Medicare-covered benefits, typically include extra benefits such as dental, vision, hearing, and Part D drug coverage, and often provide all benefits for no additional premium (other than the Part B premium).

Under this approach, states typically contract with a Medicare Advantage private insurer to provide all Medicare-covered benefits as well as extra benefits for their Medicare-eligible retirees (and often spouses). The federal government (Medicare) provides a payment per retiree to cover all Medicare benefits, along with a package of extra benefits for retirees in the group. The extra benefits may also be subsidized by the employer or employee premiums. While some states offer their Medicare-age retirees a choice between a Medicare Advantage plan and a plan that supplements traditional Medicare, others exclusively offer Medicare Advantage. This shift to Medicare Advantage may help states reduce their retiree health liability and simplify administration, but presents tradeoffs for beneficiaries, particularly those who prefer coverage under traditional Medicare.

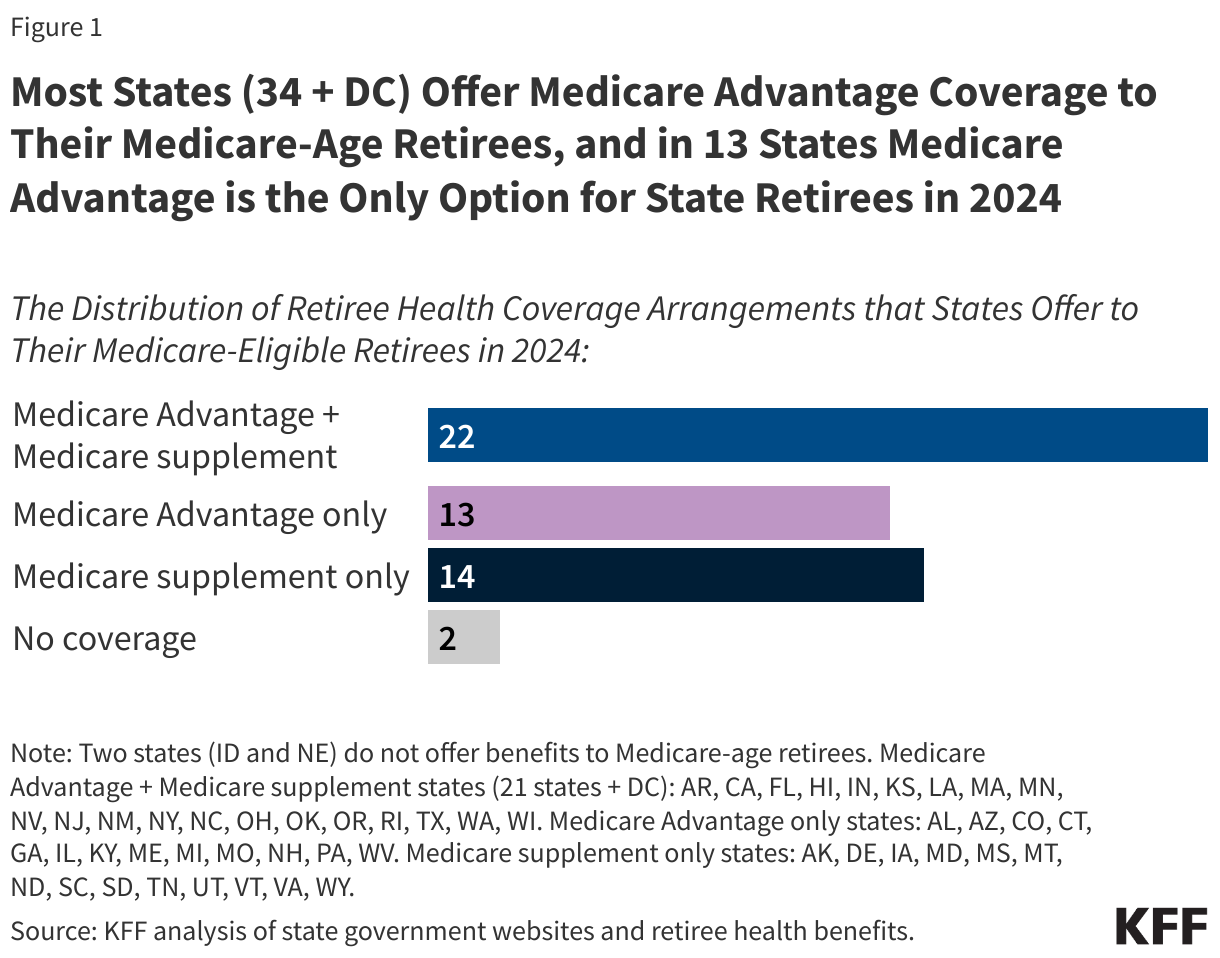

This data note examines the extent to which states are providing health benefits to their Medicare-eligible retirees through Medicare Advantage arrangements in 2024, based on KFF’s review of states’ employee retirement system websites (Figure 1, Table 1). This analysis does not focus on health benefits for pre-65 retirees, active employees, municipal- or county-granted retiree health benefits, groups of retirees that have separate retirement systems in some states, such as law enforcement or teachers, nor does it include Puerto Rico or the territories. Key findings for 2024 include:

- Almost all states, 48 states and DC, offer retiree health benefits to their Medicare-age retirees. Just two states, Idaho and Nebraska, offer no retiree health benefits to state retirees ages 65 or older.

- In 13 states, Medicare Advantage is the only option for retiree health coverage for Medicare-age retirees. This is an increase from eight states in 2016, as noted in a prior Pew report. In some of these states, retirees forfeit their retiree health benefits in perpetuity if they choose coverage under traditional Medicare. Moreover, in all of these states except for Connecticut and Maine, which have continuous or annual guaranteed issue rights to purchase a Medigap policy (meaning they can purchase a Medigap policy without a review of their medical conditions), retirees in other states who switch to traditional Medicare may be denied a Medigap policy due to pre-existing conditions.

- In 21 states and DC, Medicare-age retirees are offered both Medicare Advantage plans and supplemental plans that wrap around traditional Medicare, an increase from 13 states in 2016. Among these states, 17 states and DC offer Medicare Advantage and supplemental plan options directly to their retirees while 3 of these states offer retiree health benefits through a private exchange, giving their retirees the option to purchase either a Medicare Advantage plan or a plan that supplements Medicare – typically Medigap. In Louisiana, Medicare-age retirees have the option of getting coverage through a private exchange or directly from the state, including both Medicare Advantage plans and supplements to traditional Medicare.

- In 14 states, Medicare-age retirees are offered coverage through plans that supplement traditional Medicare, but are not offered coverage through a Medicare Advantage plan, a decrease from 25 states in 2016.

For states, as with employers and unions that offer retiree health benefits, this shift towards Medicare Advantage may be an effective strategy to maintain benefits while reducing spending on retiree health costs. For example, in 2022, Connecticut estimated the state would save $400 million over the following three years by switching retirees to a different Medicare Advantage administrator, which would also reduce the state’s unfunded liability by about $7.5 billion. Similarly, in 2023, New York City estimated that it would save $600 million annually by switching its city retirees to Medicare Advantage.

Shifting retiree benefits to Medicare Advantage from other coverage arrangements may present tradeoffs for retirees. On the one hand, Medicare Advantage may offer lower premiums and more comprehensive benefits than other retiree coverage options. On the other hand, Medicare Advantage plans may have a more limited network of hospitals, physicians and other providers, which could require retirees to pay more out-of-pocket or pay the entire cost of their care if they go out-of-network. (Some states with Medicare Advantage contracts stipulate that retirees will not be required to pay more for out-of-network care; however, retirees in these states may need to cover the full cost of their out-of-network care upfront if the provider does not take their Medicare Advantage plan, and submit a claim for reimbursement to cover their costs.) Retirees with traditional Medicare and supplemental retiree benefits can see any provider who accepts Medicare, but supplemental plans vary on the extent to which they cover cost sharing.

In addition to often having a more limited network of providers, Medicare Advantage plans typically employ utilization management tools, such as prior authorization. These limitations are, in part, why public sector retirees in both Delaware and New York City sued to stop being moved into a Medicare Advantage plan. In New York City, a Manhattan Supreme Court Judge prohibited the implementation of this plan (though it is still possible that the mayoral Administration may try to appeal the ruling). In Delaware, the Supreme Court recently overruled the lower court’s decision, stating that it incorrectly halted the state’s move to a Medicare Advantage plan.

Of the 13 states that provide health benefits to Medicare-age retirees exclusively through Medicare Advantage plans, just four offer plans with $0 (or fully-subsidized) plan premiums. While many states offer premium subsidies or reductions based on individual factors such as household income, years of employment, or work in hazardous roles, premiums may still be costly. In Missouri, for instance, a retiree with no dependents receiving the maximum state contribution of 65% still pays a premium of $82 per month, raising questions about whether some retirees are paying more for their coverage than they would if they enrolled in another Medicare Advantage plan offered to enrollees in their area. Nearly all Medicare beneficiaries (99%) have access to a Medicare Advantage plan with drug coverage for no additional monthly premium in 2024 (other than the Part B premium), including 100% of beneficiaries in the state of Missouri.

It is possible that employer-sponsored Medicare Advantage plans charge additional premiums because they offer more generous benefits and broader provider networks than plans offered to other Medicare beneficiaries in the same area, but benefit, network, and cost-sharing information for employer plans are not required to be reported to the Centers for Medicare and Medicaid Services (CMS), making it difficult to compare the generosity of benefits in these state retiree plans to plans available to all Medicare beneficiaries.

For Medicare, the move to Medicare Advantage raises questions about whether states are shifting liabilities to the Medicare program. On average, Medicare pays more for enrollees in Medicare Advantage plans than for enrollees in traditional Medicare, including for group plans. In 2024, MedPAC estimates that the Medicare program will spend 22% more per Medicare Advantage enrollee ($83 billion) than for similar beneficiaries in traditional Medicare, including employer plans. In addition, employer plans (which include states) can also receive bonuses under the Medicare Advantage program. These bonus payments to employer and union-sponsored plans reached $2.5 billion in 2023, or nearly $10 billion over the last 5 years (2019-2023).

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.