What Are the Primary Medicaid Eligibility Pathways for Dual-Eligible Individuals?

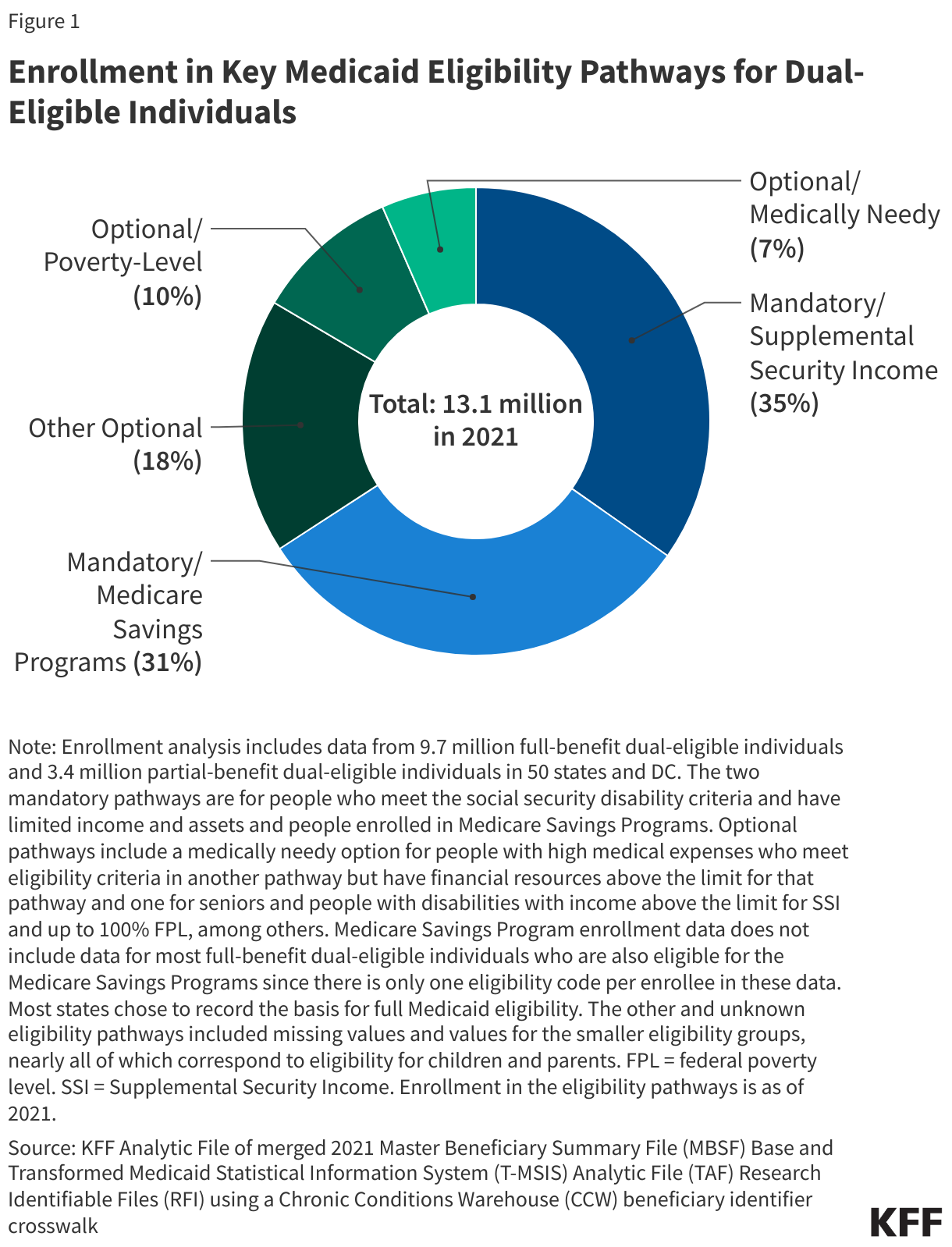

In 2021, 1 in 5 Medicare beneficiaries or 13.1 million people, known as “dual-eligible individuals,” had both Medicare and Medicaid coverage. Eligibility for Medicare, which is the primary source of coverage for dual-eligible individuals, is based on their age or disability status. For most dual-eligible individuals, there are two pathways to Medicaid eligibility: one is through Medicaid eligibility pathways for seniors and people with disabilities and the other is through the Medicare Savings Programs. These eligibility pathways confer different benefits. The Medicaid eligibility pathways provide coverage of Medicaid benefits that are not otherwise covered by Medicare including long-term services and supports (LTSS), vision, and dental care. The Medicare Savings Programs cover Medicare premiums and often, cost sharing, but not Medicaid benefits. Medicare beneficiaries who are only eligible for Medicaid through the Medicare Savings Programs are “partial-benefit” dual-eligible individuals because they only receive coverage of Medicare premiums and often, cost sharing. To be a “full-benefit” dual-eligible individual, Medicare beneficiaries must be enrolled in Medicaid through a Medicaid eligibility pathway beyond the Medicare Savings Programs. (Most full-benefit dual-eligible individuals are eligible for both.)

Federal statutes require states to enroll people who receive Supplemental Security Income (SSI) in Medicaid and to enroll eligible Medicare beneficiaries in the Medicare Savings Programs. Beyond these two “mandatory” eligibility pathways, there are optional Medicaid eligibility pathways that states may choose to offer for people who have disabilities or are ages 65 and older, including options to expand coverage beyond what is required under federal law to low-income seniors and people with disabilities; coverage for “medically needy” individuals who qualify for Medicaid after deducting incurred medical expenses from their income; and coverage for people who need LTSS.

States are currently implementing new rules designed to streamline the enrollment and renewal systems for the Medicare Savings Programs and for Medicaid. The rules are intended to help eligible individuals obtain and maintain Medicaid coverage by reducing administrative burdens on applicants and enrollees. As the new requirements start to take effect, this brief examines current Medicaid eligibility policies and enrollment patterns using data from KFF’s 2024 50-state survey of states’ eligibility and enrollment policies for seniors and people with disabilities, and 2021 Medicare and Medicaid claims data from the Centers for Medicare and Medicaid Services (CMS).

Key Takeaways

- Most of the 13.1 million dual-eligible individuals are enrolled in Medicaid through mandatory eligibility pathways: 4.6 million through SSI and 4.1 million through the Medicare Savings Programs. The remaining 4.5 million are enrolled through optional pathways (Figure 1).

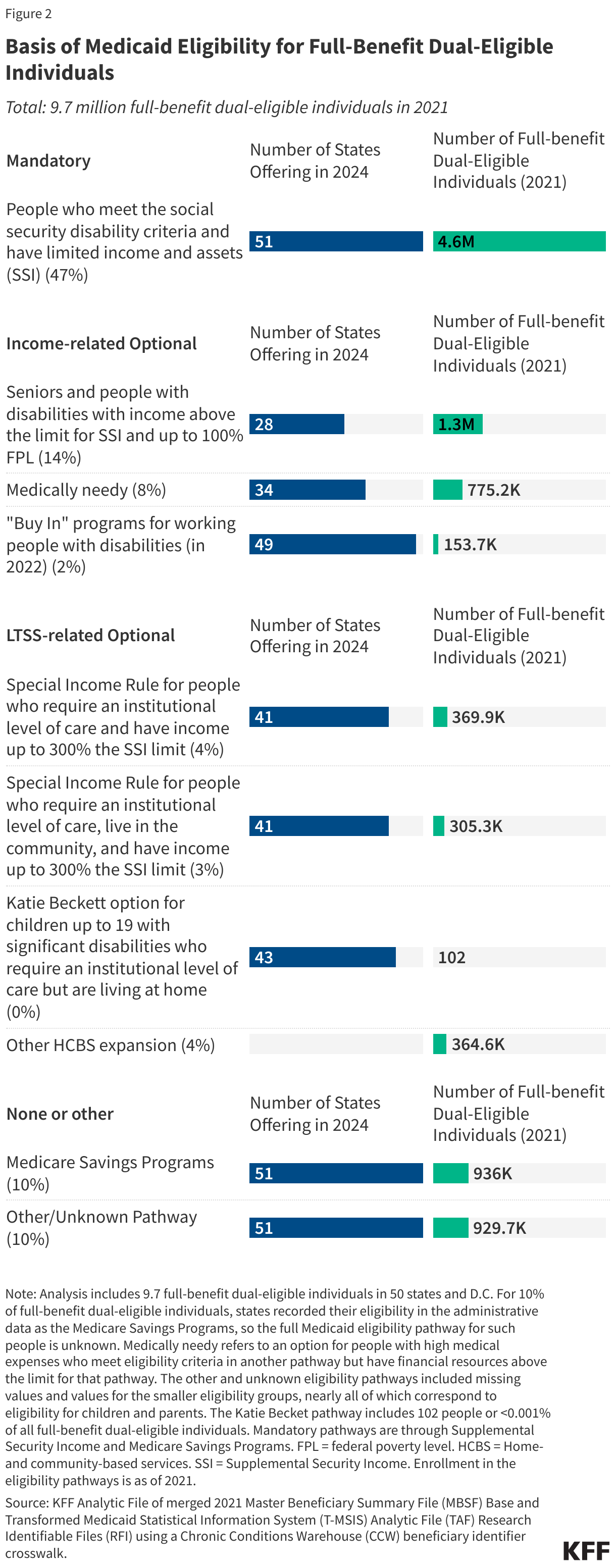

- Among the 9.7 million dual-eligible individuals with full Medicaid, nearly half (47%) are eligible through the only mandatory pathway to full Medicaid, which is SSI.

- Although it is only offered by 28 states, the next most common pathway for full Medicaid is an optional pathway that provides coverage for seniors and people with disabilities who have income below the federal poverty level, covering 14% of full-benefit dual-eligible individuals. Other optional pathways are offered by more states but only a small percentage of dual-eligible individuals enroll in each of those pathways (Figure 2).

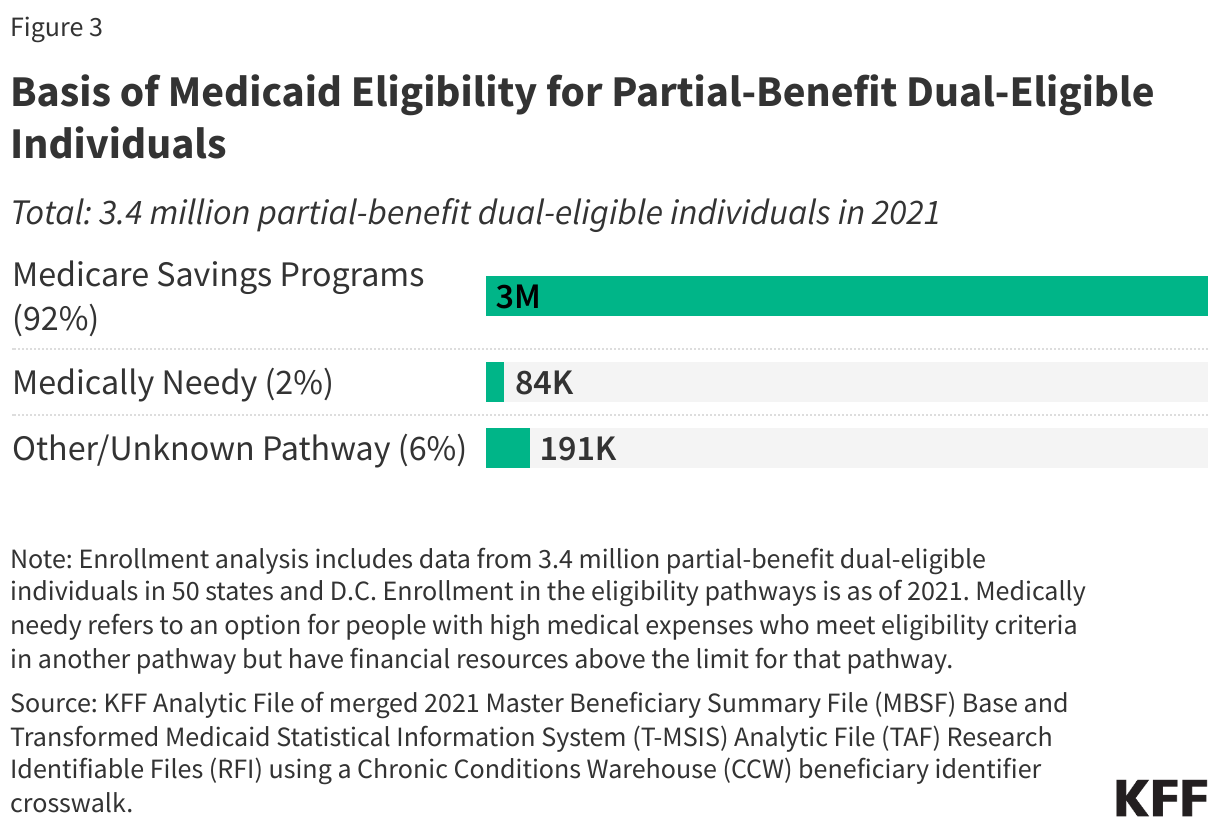

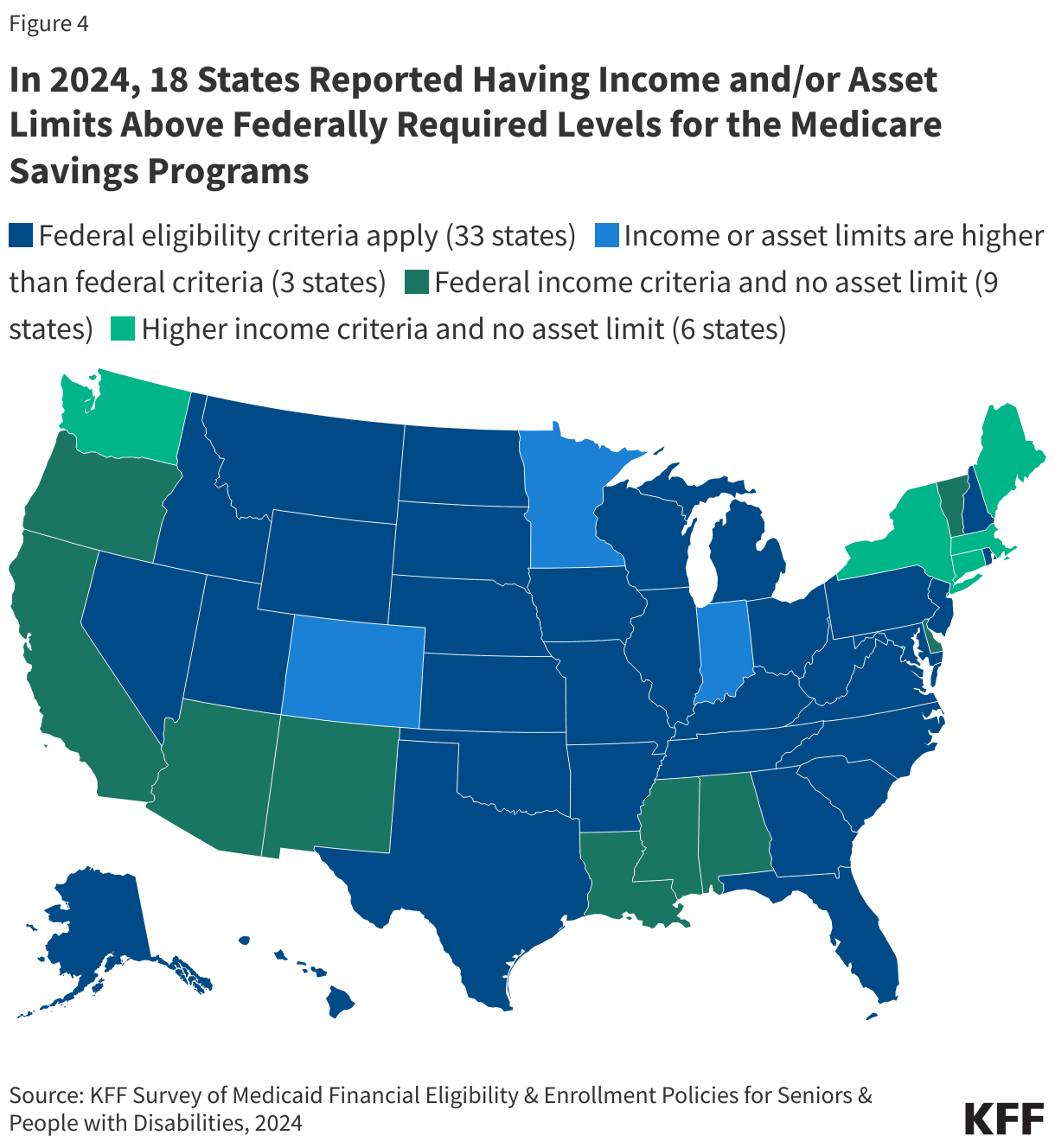

- Virtually all (92%) dual-eligible individuals with partial Medicaid (3.1 million) are eligible through the Medicare Savings Programs. Federal law defines minimum income and resource limits for each of the Medicare Savings Programs, but in 2024, 18 states reported having income and/or asset levels above the federally required limits for the Medicare Savings Programs. Those states are home to 1.1 million or a third (33%) of dual-eligible individuals with partial Medicaid.

- As new federal requirements for enrolling people in the Medicare Savings Programs take effect, most states report being in compliance with the requirements by October 2024.

KFF’s Survey of Medicaid Financial Eligibility & Enrollment Policies for Seniors & People with Disabilities, was conducted by KFF and Watts Health Policy Consulting, and describes states’ eligibility and enrollment policies for seniors and people with disabilities as of June 2024. Overall, 49 states and the District of Columbia (hereafter referred to as a state) responded to the survey, though response rates to specific questions varied (Florida was the only state that did not respond). Responses were supplemented with publicly available information and data from KFF’s 2022 survey when available.

The analysis also uses merged beneficiary-level Medicare and Medicaid data from 2021—the most recent full release of Medicaid data—to analyze how many dual-eligible beneficiaries enter Medicaid through each of the eligibility pathways. The enrollment analysis includes 13.1 million dual-eligible individuals in 2021 (see Methods).

How do full-benefit dual-eligible individuals become eligible for Medicaid?

Medicaid Eligibility Pathways for Seniors and People with Disabilities

To qualify for full Medicaid benefits, dual-eligible individuals must meet Medicaid eligibility criteria, typically through eligibility pathways specific to people ages 65 and older (seniors) and people with disabilities (see Appendix). The Medicaid pathways in which eligibility is based on old age or disability are known as “non-MAGI” pathways because they do not use the Modified Adjusted Gross Income (MAGI) financial methodology that applies to children, pregnant individuals, parents, and other non-elderly adults with low incomes. (Medicare beneficiaries who are eligible because of a disability may enroll in Medicaid through all MAGI pathways other than the pathway for adults eligible through the Affordable Care Act, but more often qualify through disability-related pathways. Medicare beneficiaries who are ages 65 and older are generally not eligible for Medicaid through the MAGI pathways.)

In addition to considering income, non-MAGI Medicaid applicants must meet other eligibility requirements that make the application more onerous than is the case for MAGI applicants. Non-MAGI applicants must meet eligibility requirements related to their age or disability status and unless living in a state that has eliminated asset limits, most applicants must demonstrate that they have limited savings and other financial resources (e.g., assets). Medicaid enrollees who use LTSS must also meet requirements related to their functional needs which are generally measured by their ability to perform activities of daily living such as eating and bathing. Beyond SSI (the only mandatory pathway), the main optional non-MAGI pathways to full Medicaid eligibility include state options to expand coverage to low-income seniors and people with disabilities, “medically needy individuals” who qualify for Medicaid by deducting incurred medical expenses from their income, and coverage for people who use LTSS. Each group has different rules about income and assets, making eligibility determinations complex.

Most full-benefit dual-eligible individuals are also eligible for the Medicare Savings Programs, but eligibility for the Medicare Savings Programs does not provide access to full Medicaid. To be a full-benefit dual-eligible individual, people enrolled in the Medicare Savings Programs must also meet the eligibility criteria for one of the other Medicaid eligibility pathways, in which case, they would be eligible for Medicaid through two mechanisms: whichever Medicaid pathway confers eligibility for full Medicaid and the Medicare Savings Programs (which cover Medicare premiums and often, cost sharing).

Mandatory eligibility through SSI

In 2021, 4.6 million full-benefit dual-eligible individuals were enrolled in Medicaid through the only pathway that states are required to cover, SSI (Figure 2). Those enrollees comprised 47% of all full-benefit dual-eligible individuals. To be eligible for SSI, beneficiaries must have low incomes, limited assets, and either be older than 64 or have a qualifying disability. Although there is a standard federal maximum benefit, some states supplement the federal benefit with additional payments. In those states, the SSI benefit levels—and applicable income limits for SSI recipients—are higher.

The proportion of full-benefit dual-eligible individuals enrolled in Medicaid through SSI varied across states—from less than 30% in nine states to over 85% in Maine, Texas, and Missouri (Appendix Table 2). Such variation reflects differences in the SSI income limit and the extent to which the states offer coverage through optional Medicaid eligibility pathways in addition to the mandatory SSI pathway, among other factors such as disability rates, demographic characteristics, eligibility determinations, and data quality/availability.

Optional Medicaid eligibility pathways related to income

A total of 2.2 million full-benefit dual eligible individuals are eligible for Medicaid through optional eligibility pathways for low-income seniors and people with disabilities. Some of the more prominent options include: “buy in” programs for working people with disabilities (available in 49 states), medically needy coverage (available in 34 states), and coverage for seniors and people with disabilities with incomes above the SSI eligibility thresholds (available in 28 states). The KFF survey did not include the buy in programs in 2024, so states’ policies come from the 2022 KFF survey.

The optional eligibility pathway that was offered by the fewest states enrolled the largest number of full-benefit dual-eligible individuals: low-income seniors and people with disabilities, which covered 14% of full-benefit dual-eligible individuals (1.3 million people). The pathway for low-income seniors and people with disabilities is the simplest pathway administratively because it only requires information about people’s income and in most cases, assets. Most other non-MAGI eligibility pathways also require information about people’s health status, functional status, or spending on health care. The share of full-benefit dual-eligible individuals eligible through the state option to expand coverage to low-income seniors and people with disabilities was 14% nationally and ranged from less than 1% in 33 states to over 40% in Hawaii, Massachusetts, and North Carolina (Appendix Table 2).

More than 775,000 or 8% of full-benefit dual-eligible individuals were enrolled in medically needy coverage in 2021 (Figure 2). This pathway is one of the most complex administratively because people are eligible if their income exceeds the limit of another pathway, but only if they “spend down” to the medically needy limit by deducting health care expenses from their income. The after-health care spending income limits tend to be low—below 50% of the federal poverty level in more than half of the states offering such coverage. There were only four states (Illinois, Maryland, New York, and North Dakota) in which more than 20% of full- benefit dual-eligible individuals were enrolled through medically needy pathways.

The Medicaid buy in program refers to multiple Medicaid eligibility pathways that serve workers with disabilities who are earning income and for whom states may charge premiums as a condition of Medicaid eligibility, which combined enrolled only 2% of full-benefit dual-eligible individuals in 2021 (almost 154,000 people). Under the buy ins, states cover people with disabilities who are working, even if their income or assets exceed the limit for other eligibility pathways. This option enables people with disabilities to retain Medicaid’s coverage of medical care and LTSS as their income increases. Medicaid can fill in coverage gaps for working people with disabilities because private health insurance typically does not cover all the services and supports that they need to live independently and work. Iowa was the only state in which at least 20% of full-benefit dual-eligible individuals were enrolled through a buy in.

Optional Medicaid eligibility pathways related to LTSS

In 2024, 1.0 million people were eligible through several widely adopted Medicaid eligibility pathways specific to people using LTSS who require an institutional level of care (Figure 2, Appendix Table 1). The two primary eligibility pathways for people using LTSS include Katie Beckett coverage for children who have significant disabilities requiring an institutional level of care but living at home (43 states) and the special income rule, which covers other people requiring an institutional level of care with incomes up to 300% of the SSI benefit rate ($2,829 in 2024). Overall, 42 states offer coverage through a special income rule, with 41 states offering the option to people in institutions and 41 states offering the option to people living at home. Less is known about states’ other home- and community-based services (HCBS) expansions, which include state-specific demonstration programs and people who are eligible for Medicaid through the Program of All-Inclusive Care for the Elderly. (KFF’s eligibility surveys excluded other HCBS expansions.) LTSS-related pathways are administratively complex because applicants must demonstrate their need for an institutional level of care. As a result, people who may be eligible for Medicaid through LTSS-related pathways and through other pathways are more likely to be enrolled through those other pathways.

Although these optional Medicaid eligibility pathways related to LTSS are adopted by most states, they collectively enrolled only 11% of full-benefit dual-eligible individuals (1 million) in 2021 (Figure 2). Low enrollment in Katie Beckett reflects the fact that there are few dual-eligible individuals under the age of 19. For the other three LTSS-related pathways, dual-eligible individuals comprise three quarters of all Medicaid enrollees (see Appendix). Across the states, the percentage of dual-eligible individuals enrolled in Medicaid through each of the LTSS-related pathways varies, with some states having over 20% of dual-eligible individuals enrolled in other HCBS expansions or a special income rule program (Appendix Table 2).

Other or Unknown Medicaid eligibility pathways

Roughly 1.9 million full-benefit dual-eligible individuals were eligible for Medicaid through other or unknown Medicaid eligibility pathways, including 0.9 million individuals who were in states that recorded their eligibility in the administrative data as the Medicare Savings Programs. In the Medicaid administrative data, enrollees receive only one eligibility code each month; therefore among the full-benefit dual-eligible individuals in the Medicaid Savings Programs it is unknown how those full-benefit dual-eligible individuals became eligible for full Medicaid. The remaining 0.9 million full-benefit dual-eligible individuals were in an “other” or “unknown” Medicaid eligibility group. Those pathways included missing values and values for the smaller eligibility groups, nearly all of which correspond to eligibility for children and parents. (Totals do not add up to 1.9 million due to rounding.)

How do partial-benefit dual-eligible individuals become eligible for Medicaid?

The Medicare Savings Programs

Dual-eligible individuals with partial Medicaid benefits do not receive coverage of the full range of Medicaid benefits, such as long-term services and supports, but do receive payments of Medicare premiums and, in most cases, cost sharing through the Medicare Savings Programs. Medicare beneficiaries are responsible for payment of Medicare premiums, deductibles, and other cost sharing requirements unless they have supplemental coverage, a Medicare Advantage plan that covers some of the cost sharing, or have incomes and assets low enough to qualify for the Medicare Savings Programs (under which state Medicaid programs provide assistance with Medicare Part A and Part B premiums and/or cost sharing) and the Part D Low-Income Subsidy (LIS) (which helps with Medicare Part D drug plan premiums and cost sharing).

Under the Medicare Savings Programs, state Medicaid programs pay for premiums and/or cost sharing for Medicare beneficiaries who have monthly incomes up to 135% FPL under federal guidelines ($1,715 for individuals and $2,320 for couples in 2024) and assets up to 300% of the limit for Supplemental Security Income ($9,430 for individuals and $14,130 for couples in 2024; unlike SSI, asset limits for the Medicare Savings Programs are adjusted for inflation and increase each year). There are four eligibility categories within the Medicare Savings Programs (box 1), which confer different benefits based on different eligibility criteria. States must cover people who meet the federal eligibility requirements for the Medicare Savings Programs but may elect to increase income or asset eligibility limits beyond federal levels.

Box 1: The Medicare Savings Programs

There are four Medicare Savings Programs that help Medicare beneficiaries get help from Medicaid to pay their Medicare premiums and in many cases, cost sharing.

• The Qualified Medicare Beneficiary (QMB) program pays for Part A and B premiums, deductibles, coinsurance, and copayments. Medicare beneficiaries are eligible for the QMB program if their monthly income is below the FPL ($1,275 for individuals and $1,724 for couples in 2024) and if their assets are below the resource limit ($9,430 for individuals and $14,130 for couples in 2024).

• The Specified Low-Income Medicare Beneficiary (SLMB) program pays for Part B premiums only. Medicare beneficiaries are eligible for the SLMB program if their monthly income is below 120% of the FPL ($1,526 for individuals and $2,064 for couples in 2024) and if their assets are below the resource limit ($9,430 for individuals and $14,130 for couples in 2024).

• The Qualifying Individual (QI) program pays for Part B premiums only. Medicare beneficiaries are eligible for the QI program if their monthly income is below 135% of the FPL ($1,715 for individuals and $2,320 for couples in 2024) and if their assets are below the resource limit ($9,430 for individuals and $14,130 for couples in 2024).

• The Qualified Disabled and Working Individual (QDWI) program pays for Part A premiums only. Medicare beneficiaries are eligible for the QDWI program if they have a disability and lost their premium-free Medicare Part A because they returned to work. Their monthly income must be below 200% of the FPL ($5,105 for individuals and $6,899 for couples in 2024) and if their assets are below the resource limit ($4,000 for individuals and $6,000 for couples in 2024).

(Resource limits do not include $1,500 for burial expenses.)

In 2021, 92% of partial-benefit dual-eligible individuals were primarily eligible for Medicaid through the Medicare Savings Programs (Figure 3, Appendix Table 3). Among the 3.4 million people eligible for partial Medicaid benefits, more than nine in ten were eligible through the Medicare Savings Programs (3.1 million people). In all but six states, more than 80% of partial-benefit dual-eligible individuals were eligible through the Medicare Savings Programs. Among the remaining 8%, the largest eligibility category was through medically needy coverage (2% of partial benefit individuals, fewer than 0.1 million people). Dual-eligible individuals may have partial Medicaid benefits through medically needy programs because states may elect to only cover a subset of Medicaid benefits through their medically needy programs. The remaining 6% of partial-benefit dual-eligible individuals were eligible through other partial-benefit pathways such as those for family planning services, individuals needing treatment for breast or cervical cancer, and other eligibility pathways that may have occurred at some other point in the year.

Changes in eligibility and enrollment for the Medicare Savings Programs

In 2024, 18 states reported having income and/or asset levels above federally required levels for the Medicare Savings Programs. (Figure 4, Appendix Table 3). Overall, 33 states use the federal eligibility criteria, and the remaining 18 states—home to 1.1 million or a third (33%) of partial-benefit dual-eligible individuals—have more generous eligibility limits on income, assets or both:

- 3 states have either income or asset levels higher than the federally required levels (Colorado, Indiana, and Minnesota)

- 9 states use the federal income levels but have no asset test (Alabama, Arizona, California, Delaware, Louisiana, Mississippi, New Mexico, Oregon, and Vermont)

- 6 states have income levels higher than federally required and no asset test (Connecticut, District of Columbia, Maine, Massachusetts, New York, and Washington).

Many of the higher income and asset eligibility policies were new in 2024. Of the 7 states with higher income levels, 3 states reported raising the income eligibility criteria in 2024: Indiana increased the income limit for the Qualified Individuals program to 200% FPL, Massachusetts raised the income limits for all of the programs, and Washington increased the income limit for Qualified Medicare Beneficiary Program. (The remaining 4 states had higher income limits in earlier years but did not increase them in 2024.) Among the two states with asset limits higher than federally required levels, Colorado reported that change for the first time in 2024, but Minnesota had higher asset limits in earlier years. Among the 15 states with no limit on assets, that policy was new to California, Maine, and Massachusetts in 2024.

Some of the 2024 eligibility changes may be responses to a 2023 final rule on eligibility and enrollment in the Medicare Savings Programs. CMS expects the final rule to increase enrollment in the Medicare Savings Programs by nearly 1 million. New enrollments include people who enroll in the Medicare Savings Programs because of the rule, and gains in months of coverage among people who would have enrolled anyway but now face fewer administrative barriers, resulting in either gaining Medicaid earlier or experiencing less churn in and out of the program. Prior KFF research found that many low-income Medicare beneficiaries are not enrolled in the Medicare Savings Programs. The rule reduces barriers to coverage by improving alignment between the Medicare Savings Programs and applications for Medicare’s Part D Low-Income Subsidy, requiring states to automatically enroll Medicare beneficiaries with SSI into the Medicare Savings Programs, and making it easier for applicants to document their financial resources when applying for Medicaid.

In 2024, 31 states reported that they already automatically enroll Medicare beneficiaries who receive SSI into the Medicare Savings Programs, one of the key requirements of the new rule (Appendix Table 4). Of the remaining states, 15 reported plans to do so by October 2024, while 4 states reported needing additional time to comply. Among states not already in compliance, the most common reasons cited were related to modernizing or updating existing systems to implement the change.

Methods |

| Medicaid Financial Eligibility and Enrollment Policies Data: KFF’s 50-state survey and from administrative records from the Centers for Medicare and Medicaid Services (CMS). KFF’s Survey of Medicaid Financial Eligibility & Enrollment Policies for Seniors & People with Disabilities was conducted in March 2024 by KFF and Watts Health Policy Consulting.

Enrollment Data: Data are from a KFF analytic file that merged the Centers for Medicare & Medicaid Services Chronic Conditions Data Warehouse 2021 research-identifiable Master Beneficiary Summary File (MBSF) Base and the 2021 Transformed Medicaid Statistical Information System (T-MSIS) Analytic Files (TAF) Research Identifiable Files (RIF) file using a Chronic Conditions Warehouse (CCW) beneficiary identifier crosswalk. State inclusion criteria: Estimates include enrollees living in the 50 states and DC, excluding residents in the territories. Dual-eligible individual inclusion criteria: Dual-eligible individuals were included if (1) they were in both the MBSF and T-MSIS files using the CCW crosswalk, and (2) Dual-eligible individuals are assigned full-benefit status and partial benefit status using an “ever” approach and a hierarchy by giving priority to the full-benefit status. Individuals were a full-benefit dual-eligible individual in 2021 using the Medicare monthly DUAL_STUS_CD with values of 02,04,08 or the Medicaid monthly code DUAL_ELGBL_CD with values of 02,04,08 or the monthly code RSTRCTD_BNFTS_CD_03 values of 1,A,D,4,5,7.If not a full-benefit dual-eligible and the individual had DUAL_STUS_CD with values of 01,03,05,06 or the Medicaid monthly code DUAL_ELGBL_CD with values of 01,03,05,06 or the monthly code RSTRCTD_BNFTS_CD_03 values of 2,3,C,6,E,F they were assigned partial-benefit status. Assignment to Medicaid eligibility categories. Dual-eligible individuals were assigned to each eligibility category by using the ELGBLTY_GRP_CD_LTST in 2021. Eligibility groups for full-benefit dual-eligible individuals:

Eligibility groups for partial-benefit dual-eligible individuals:

Other and unknown eligibility groups. Among all dual-eligible individuals, 8% had “other” or “unknown” in the eligibility group variable. Those pathways included missing values and values for the smaller eligibility groups, nearly all of which correspond to eligibility for children and parents. Medicare beneficiaries may be eligible for Medicaid through those pathways, but in practice few are because to qualify for Medicare people must either be ages 65 and older or have disabilities that qualify them for Social Security Disability Insurance. There were a small number of dual-eligible individuals who were recorded has having coverage through the Affordable Care Act (ACA) Medicaid expansion, but people are not eligible for ACA coverage if they are enrolled in Medicare. The classification of dual-eligible individuals as having ACA coverage in the data may be partially due to the continuous enrollment provision, which could have carried over an eligibility status from before the person qualified for Medicare. One limitation to the analysis is that a significant minority (10%) of full-benefit dual-eligible individuals have the Medicare Savings Programs identified as their eligibility code in the Medicaid administrative data. Most full-benefit dual-eligible individuals are eligible for the Medicare Savings Programs, but that eligibility only qualifies them to receive Medicaid coverage of Medicare premiums and often, cost sharing. To receive full Medicaid benefits, they must also be eligible through one of the Medicaid eligibility pathways, but that pathway is unknown if the state recorded “Medicare Savings Programs” as their eligibility code in the administrative data. Related, this analysis does not include estimates of the total number of people enrolled in the Medicare Savings Programs—only the number of dual-eligible individuals for whom the Medicare Savings Programs are the only basis for their Medicaid eligibility. |

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.