Strategies to Manage Unwinding Uncertainty for Medicaid Managed Care Plans: Medical Loss Ratios, Risk Corridors, and Rate Amendments

Introduction

Managed care is the dominant delivery system for Medicaid enrollees with 72% of Medicaid beneficiaries nationally enrolled in comprehensive managed care organizations (MCOs), accounting for 52% of total Medicaid spending (or more than $376 billion) in FY 2021. States pay MCOs on a capitated basis – that is, a fixed per member per month payment that must be “actuarially sound” when set. Capitation rates are typically established prospectively for a 12-month rating period, regardless of changes in health care costs or utilization.1 However, as pandemic-related enrollment increases, utilization decreases, and other cost and acuity changes began to emerge, the Centers for Medicare & Medicaid Services (CMS) allowed states to modify managed care contracts and many states implemented COVID-19 related “risk corridors” (where states and health plans agree to share profit or losses), allowing for the recoupment of funds.

States and plans are now facing another period of heightened fiscal uncertainty due to the expiration of the continuous enrollment period (introduced at the start of the pandemic) on March 31, 2023. While millions could lose coverage during the unwinding – with some current enrollees no longer eligible, and others falling through the cracks due to renewal procedures — Medicaid MCOs may see overall average member acuity increase, since people who need more health care may be more likely to stay enrolled. This would result in higher per member utilization and costs. As they developed their 2023 MCO capitation rates, some states may have built in enrollment and acuity change assumptions related to unwinding, but considerable uncertainty remains.

This brief draws on data from KFF’s 22nd annual Medicaid budget survey to provide a high-level snapshot of states with minimum medical loss ratio (MLR) and remittance requirements and risk corridors (defined in Table 1 below) in place as of July 1, 2022 that may provide financial protection and limits on financial risk for states and plans as the unwinding unfolds. This brief also discusses states’ ability to amend capitation rates (during the rating period and retroactively) as the unwinding plays out.

Background

As of July 2022, 41 states, including DC, contract with comprehensive, risk-based managed care plans to provide care to at least some of their Medicaid beneficiaries. Medicaid managed care organizations provide comprehensive acute care (i.e., most physician and hospital services) and in some cases long-term services and supports to Medicaid beneficiaries. MCOs accept a set per member per month payment for these services and are at financial risk for the Medicaid services specified in their contracts. Under federal law, payments to Medicaid MCOs must be actuarially sound.2 , 3 Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.”

Unlike fee-for-service (FFS), capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit. Plan rates are usually set for a 12-month rating period and must be reviewed and approved by CMS each year. States may use a variety of mechanisms to adjust plan risk, incentivize plan performance, and ensure payments are not too high or too low, including risk-sharing arrangements (including risk corridors), risk and acuity adjustments, medical loss ratios (MLRs, which reflect the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement), or incentive and withhold arrangements.

In response to unanticipated COVID-19 costs and conditions that led to decreased utilization, CMS permitted states to make pandemic-related adjustments to managed care contracts and capitation rates to provide financial protection and limits on financial risk for states and plans. In 2021, more than half of MCO states reported implementing COVID-19-related risk corridors in their 2020 or 2021 contracts, and many states reported the recoupment of funds as a result. Since the start of the pandemic, Medicaid enrollment overall has grown substantially, resulting in increased MCO enrollment as well. Enrollment growth has been primarily attributed to the Families First Coronavirus Response Act (FFCRA) provision that required states to ensure continuous enrollment for Medicaid enrollees in exchange for a temporary increase in the Medicaid match rate.

The Consolidated Appropriations Act, 2023 ends the continuous enrollment provision and allows states to resume disenrollments starting April 1, 2023. States must initiate all renewals and other outstanding eligibility actions within 12 months. CMS has issued specific guidance allowing states to permit MCOs to update enrollee contact information and facilitate continued enrollment. The share of individuals disenrolled (and the pace of disenrollment) across states will vary due to differences in how states prioritize and process renewals. When states begin disenrollments, Medicaid managed care plans may see the acuity of their membership increase with implications for per member utilization and costs. In a recent KFF survey of non-profit safety net managed care plans, plans reported they expect the risk profile (or acuity) of members to increase (as a result of the unwinding), as plans anticipate “stayers” will be sicker than “leavers.” Plans also reported they expect MLRs to increase.

This brief describes minimum MLR and remittance requirements and risk corridors arrangements in place as of July 2022 that may provide financial protection and limits on financial risk for states and plans as another period of heightened uncertainty approaches. The brief also discusses states’ ability to amend previously certified and approved capitation rates already in place, including retroactive rate changes under certain circumstances. CMS requires states to document risk-sharing mechanisms (including MLR requirements and risk corridor arrangements) in health plan contracts and rate certification documents prior to the start of the rating period. States may be using a variety of other risk mitigation strategies and profit-sharing approaches, including profit caps, experience rebates, risk pools, reinsurance, and stop loss requirements, which are not covered in this issue brief.

Minimum Medical Loss Ratios (MLRs) and Remittance Requirements

WHAT ARE MLR AND REMITTANCE REQUIREMENTS?

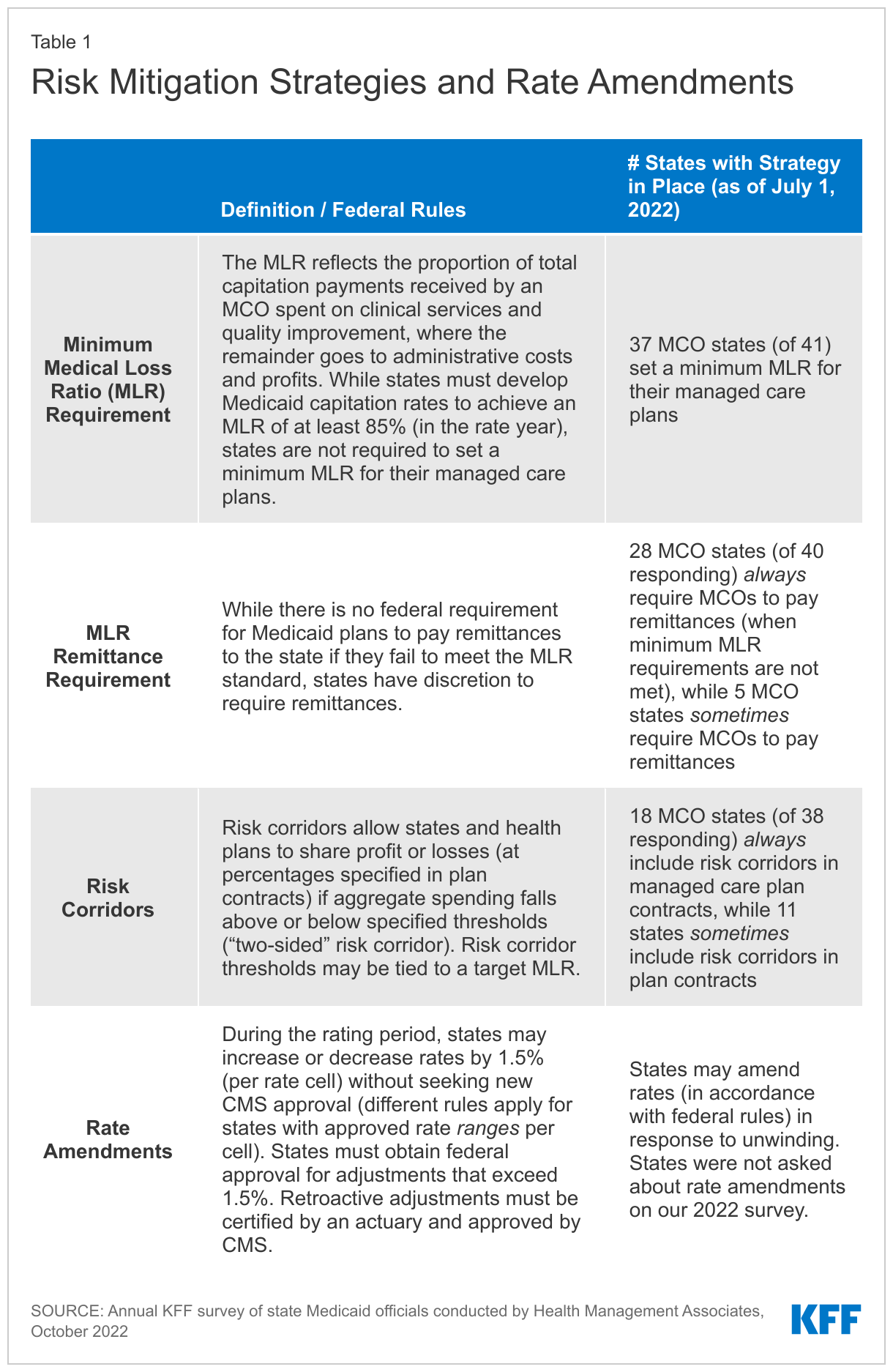

The Medical Loss Ratio reflects the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement, where the remainder goes to administrative costs and profits. To limit the amount that plans can spend on administration and keep as profit, CMS published a final rule in 2016 that requires states to develop capitation rates for Medicaid to achieve an MLR of at least 85% in the rate year.4 , 5 Plans must calculate and report an MLR and submit an annual MLR report to the state (within 12 months after the end of the contract year).6 A review conducted in 2020 by the HHS Office of Inspector General found that while most plans submitted required annual MLR reports, almost half were incomplete, while over a third of states indicated that they did not review all MLR data for accuracy. States are required to submit a summary of plans’ MLR reports annually to CMS with their rate certification and, as of October 1, 2022, are required to use the standard reporting template released by CMS. States are also required to submit an Annual Managed Care Program report that must include financial performance information for each MCO, including MLR experience.

While there is no federal requirement for Medicaid plans to pay remittances to the state if they fail to meet the MLR standard, states have discretion to require remittances. (A state and the federal government share in any remittances in proportion to the state’s federal matching rate—if the state requires remittances). For a limited time (from federal fiscal years 2021 through 2023), The Substance Use Disorder Prevention that Promotes Opioid Recovery and Treatment for Patients and Communities (SUPPORT) Act permits states to keep their regular state share of any remittances paid by Medicaid plans for expansion adults rather than only 10%.7 President Biden’s FY 2024 Budget proposes to require Medicaid managed care plans to meet an 85% minimum MLR and to require states to collect remittances if plans fail to meet the minimum MLR, estimating $20 billion in Medicaid savings over 10 years. Analysis of National Association of Insurance Commissioners (NAIC) data for the Medicaid managed care market show that average loss ratios in 2021 (in aggregate across plans) remained lower by three percentage points from 2019 (implying increased profitability).

WHAT ARE STATES DOING?

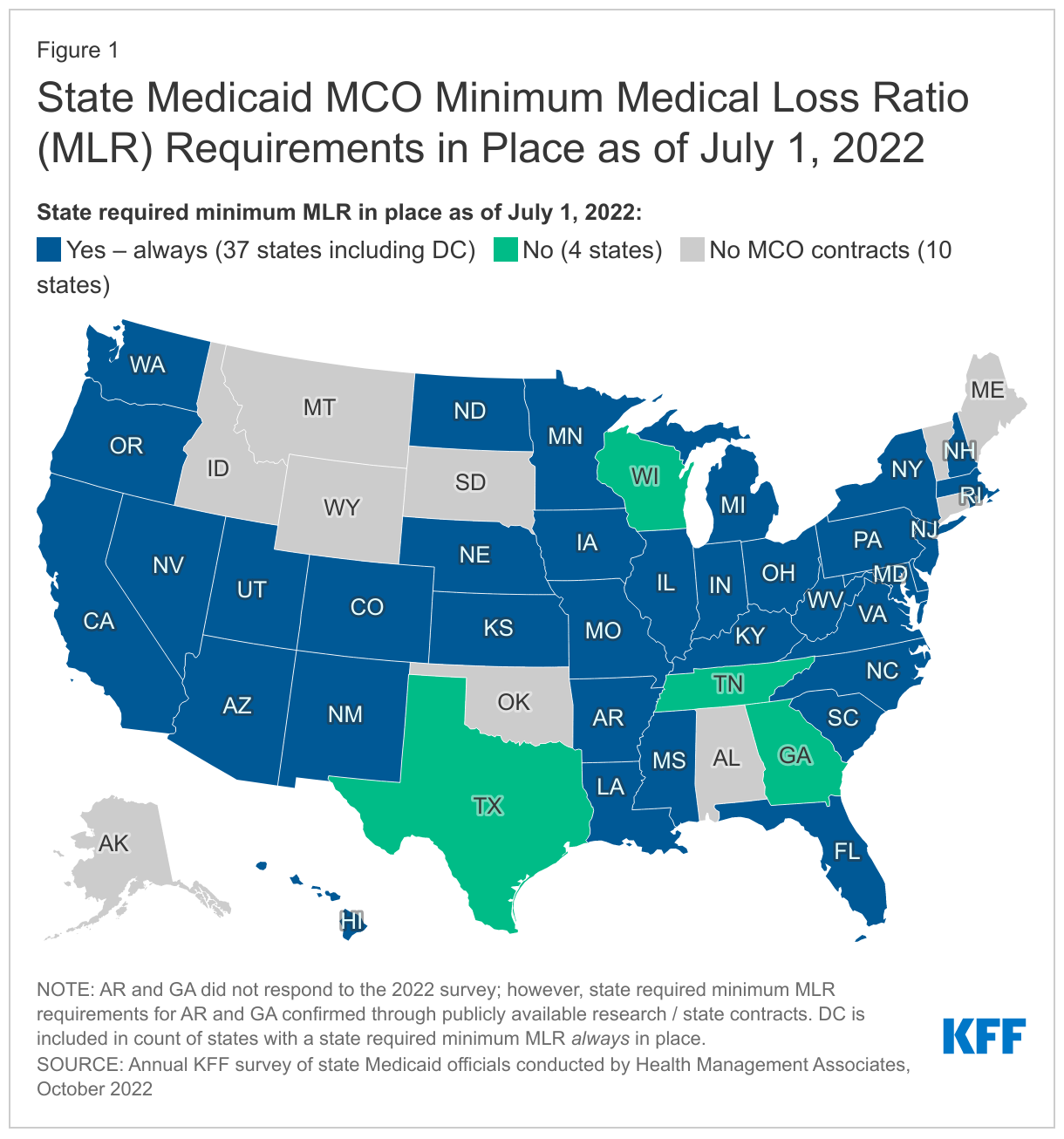

Nearly all MCO states reported a minimum MLR requirement is always in place for MCOs as of July 1, 2022 (Figure 1). While states must use plan reported MLR data to set future payment rates so that plans will “reasonably achieve” an MLR of at least 85%, states are not required to set a minimum MLR for their managed care plans. If states set a minimum MLR requirement, it must be at least 85%.8 Our findings represent a slight increase in the number of states that reported minimum MLR requirements compared to findings from OIG’s 2020 review. A few states noted that minimum MLRs may vary by program. Tennessee reported plans to implement a minimum MLR with remittance requirement in 2023 and Texas, a state with no state MLR requirement, reported an “experience rebate” requirement calculated on a graduated basis as a percentage of net income.

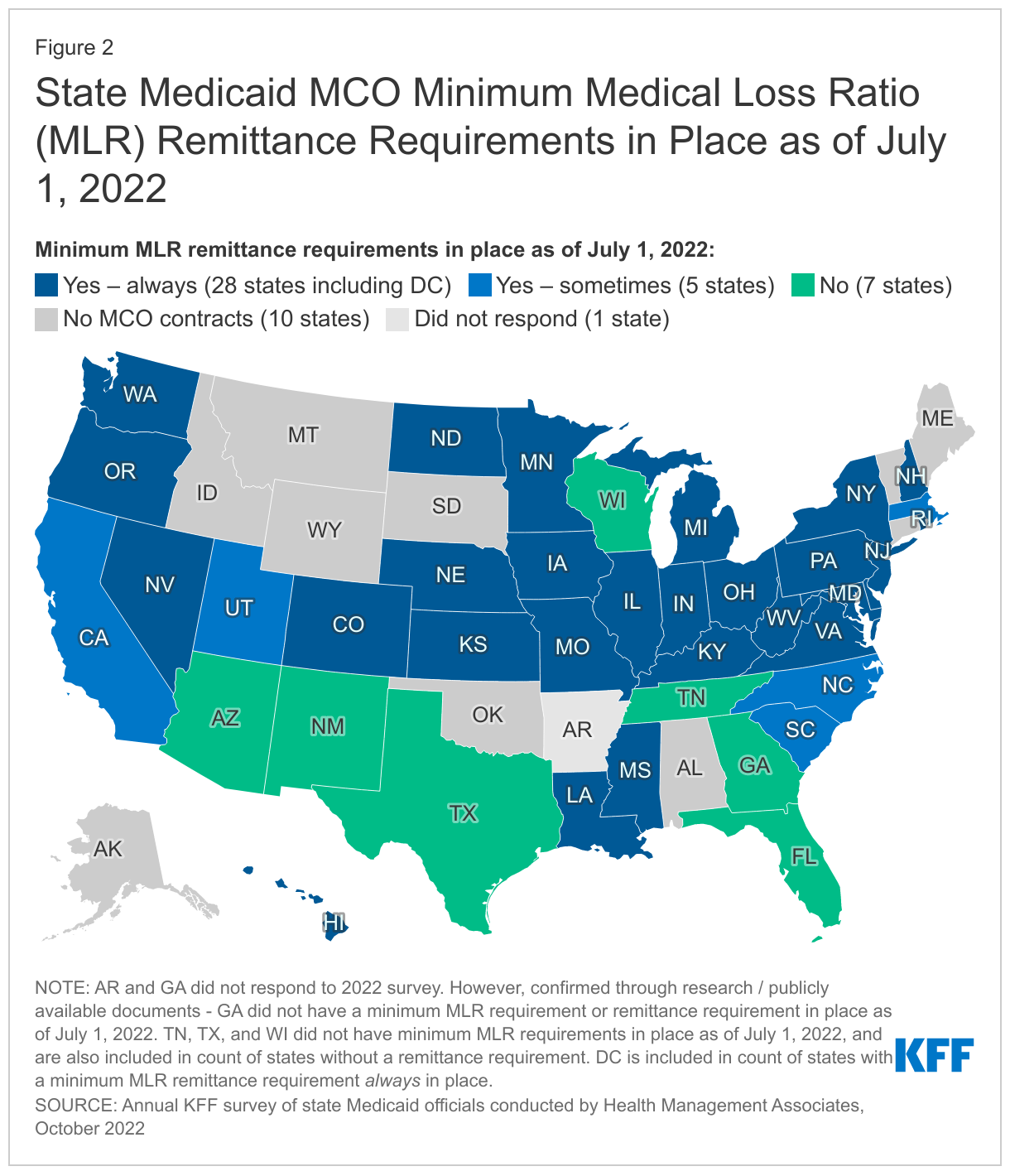

More than two-thirds of MCO states report they always require remittance payments when an MCO does not meet minimum MLR requirements (Figure 2). Twenty-eight states reported that they always require MCOs to pay remittances, while five states indicated they sometimes require MCOs to pay remittances (Figure 2). States reporting that they sometimes require remittances may limit this requirement to certain MCO contracts. For example, Utah limits its remittance requirements to MCO contracts for the adult expansion population. Seven states do not require remittances (including four states that do not set a minimum MLR requirement).9

Risk Corridors

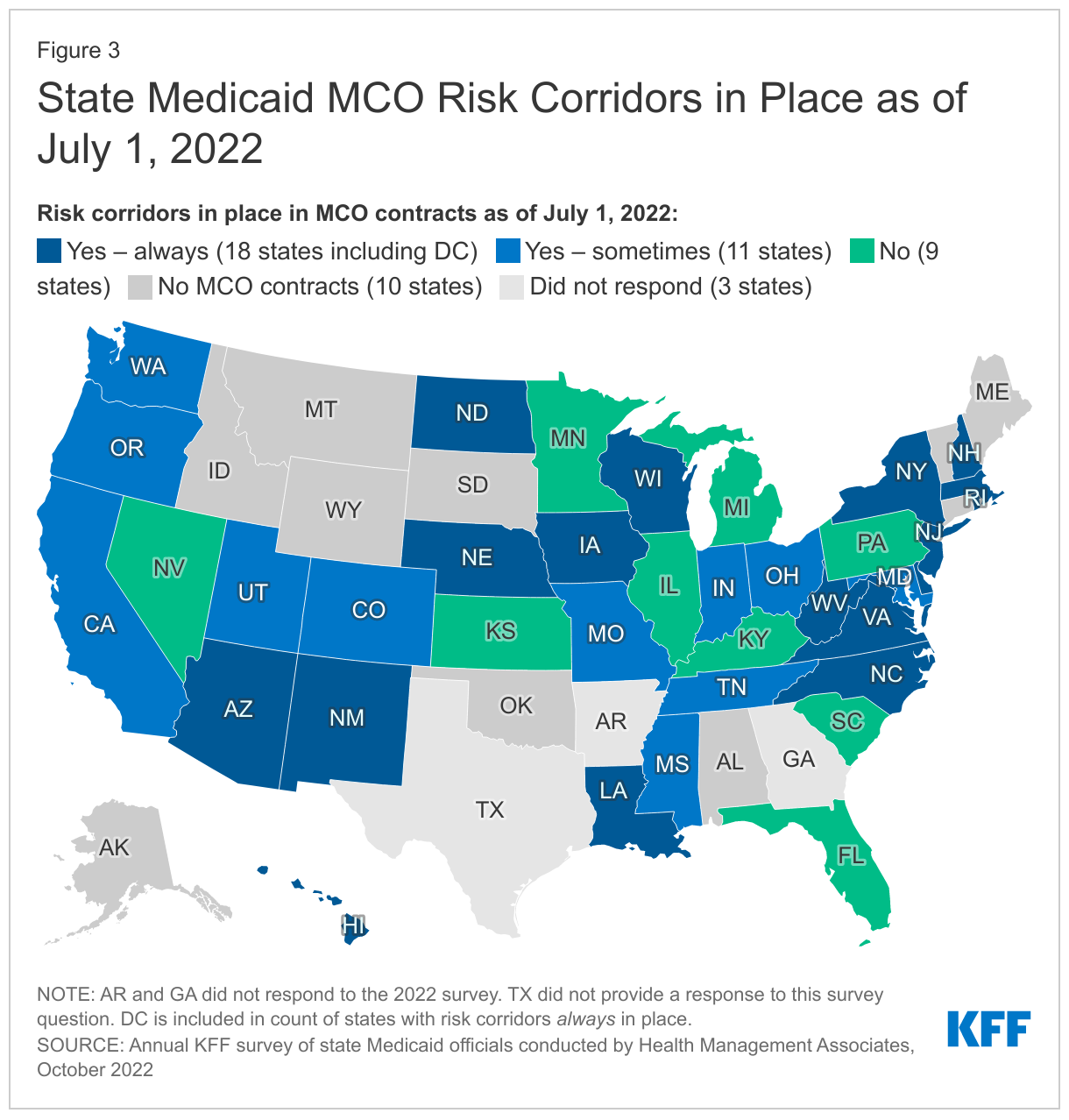

Nearly half of responding MCO states reported risk corridors were always in place in MCO contracts as of July 1, 2022 (Figure 3). Risk corridors provide financial protection to MCOs and limits on financial risk to states. Risk corridors allow states and health plans to share profit or losses (at percentages specified in plan contracts) if aggregate spending falls above or below specified thresholds (“two-sided” risk corridor). Risk corridor thresholds may be tied to a target MLR. Risk corridors may cover all/most medical services (and members) under a contract or may be more narrowly defined, covering a subset of services or members. States may introduce risk corridors on a time-limited basis – for example, following the expansion of coverage to new groups (e.g., ACA Medicaid expansion adults). Massachusetts reported an overall market risk corridor in addition to individual plan risk corridors. CMS allowed states to retroactively implement risk mitigation strategies, including risk corridors, in response to unanticipated costs and decreased utilization related to the COVID-19 pandemic.10 ,11 A few states reported implementing pandemic-related risk corridors beginning in 2020 but eliminated them in 2022 or 2023.

Rate Amendments

Even if the risk mitigation strategies described above are in place, states may determine rate amendments are necessary if their actual unwinding experience differs significantly from the assumptions used for the initial certified rates. During the rating period, states may increase or decrease rates by 1.5% per rate cell (which apply to population subgroups with one or more common characteristics such as age, gender, eligibility category, and geographic region) without seeking CMS approval for the change (different rules apply for states with approved rate ranges per cell).12 To make a larger change, the state must submit a rate amendment for federal approval that addresses and accounts for all differences from the most recently certified rates. A state may also determine that a retroactive adjustment to capitation rates (i.e., change to previously paid rates) is necessary. Retroactive adjustments are permissible under certain circumstances but must be certified by an actuary and approved by CMS. In the preamble to its 2020 final rule, CMS noted that states can adopt retroactive rate adjustments when substantial coverage changes occur mid-year or adjustments are necessary to address disease outbreaks, launches of high-cost prescription drugs, or other unforeseen circumstances that increase benefit costs.

Looking Ahead

In a dynamic environment where future MCO enrollment and utilization levels are uncertain, risk mitigation tools – like MLR and remittance requirements and risk corridors – can help states and MCOs plan for the unknown, ensuring greater fiscal certainty for both. With the Medicaid continuous coverage requirement ending this spring, another period of Medicaid enrollment and utilization uncertainty is beginning. While all states are now resuming Medicaid redeterminations or will soon, the pace and timing of those redeterminations will vary by state resulting in fiscal implications that are unique to each state. Risk mitigation strategies may provide financial protection and limits on financial risk for states and plans as the unwinding unfolds. In its 2022-2023 Medicaid Managed Care Rate Development Guide, released in April 2022, CMS recommended that all states “implement a 2-sided risk mitigation strategy for rating periods impacted by the public health emergency.”

As the process plays out in each state, more current data may help inform states whether mid-year rate amendments may be needed. State Medicaid programs use the most recent and accurate enrollment, cost, and utilization data available to ensure that MCO capitation rates are actuarially sound and that MCOs are not over-paid or under-paid for the services they deliver. In most states, Medicaid redeterminations will occur over 10-12 months that will cross more than one MCO contracting year (as most states contract on a state fiscal year or a calendar year basis) and while MCO membership losses will be immediately apparent, new utilization and acuity trends may take longer to discern. As they developed their 2023 MCO capitation rates, some states may have built in enrollment and acuity change assumptions related to unwinding (e.g., like in Arizona), but considerable uncertainty remains. Executives of publicly-traded companies that operate Medicaid MCOs (including Elevance13 and UnitedHealth Group14 ) have expressed confidence in states and their 2023 Medicaid rate-setting actions to date; however, MCOs will likely closely monitor utilization and acuity changes going forward. Sarah London, CEO of Centene, noted during the Q4 2022 earnings call: “We are focused on ensuring that state program rates reflect any shifting of the risk pool created by membership changes. We recognize the dynamics in each market are different, so we are leveraging our data to support early collaborative discussions with our state partners.”15

This brief draws on work done under contract with Health Management Associates (HMA) consultants Kathleen Gifford, Aimee Lashbrook, Mike Nardone, and Matt Wimmer.

- Medicaid and CHIP Payment And Access Commission, “Medicaid Managed Care Capitation Rate Setting,” March 2022; https://www.macpac.gov/wp-content/uploads/2022/03/Managed-care-capitation-issue-brief.pdf. ↩︎

- These requirements apply to comprehensive risk-based plans as well as limited-benefit plans (e.g., those providing only dental or behavioral health services). ↩︎

- The 2016 final rule on Medicaid managed care significantly strengthened the standards that states must meet in developing actuarially sound capitation rates and that CMS will apply in its review and approval of rates ↩︎

- Julia Paradise and MaryBeth Musumeci, CMS’s Final Rule on Medicaid Managed Care: A Summary of Major Provisions, (Washington, DC: KFF, June 9, 2016), https://modern.kff.org/medicaid/issue-brief/cmss-final-rule-on-medicaid-managed-care-a-summary-of-major-provisions/. ↩︎

- The 85% minimum MLR is the same standard that applies to Medicare Advantage and private large group plans. ↩︎

- Center for Medicare and Medicaid (CMS), “Medicaid Managed Care Regulations with July 1, 2017 Compliance Dates,” last updated June 30, 2017, https://www.medicaid.gov/federal-policy-guidance/downloads/cib063017.pdf. ↩︎

- Center for Medicare and Medicaid (CMS), “Medicaid Managed Care Frequently Asked Questions (FAQs) – Medical Loss Ratio,” June 5, 2020, https://www.medicaid.gov/sites/default/files/Federal-Policy-Guidance/Downloads/cib060520_new.pdf. ↩︎

- 42 CFR § 438.8(c). ↩︎

- Georgia House Bill 1013, signed into law by Governor Kemp on April 4, 2022, establishes an MLR remittance requirement for MCOs effective for contract rating periods beginning on and after July 1, 2023. According to a 2021 Report by the HHS Office of Inspector General, Georgia did not have a state minimum MLR or remittance requirement in place as of September 2020. Further, rate certification reports reviewed for FY 2022 indicate that no MLR requirements were in place for FY 2022. (See: Medicaid Rates for the Georgia Families and the Planning for Healthy Babies Program, July 1, 2021─June 30, 2022 Contract Period, Guidehouse for the State of Georgia Department of Community Health, April 1, 2021, and Medicaid Rates for the Georgia Families 360° Program, July 1, 2021─June 30, 2022 Contract Period, Guidehouse for the State of Georgia Department of Community Health, April 1, 2021, accessed at HMA Information Services.) ↩︎

- Center for Medicare and Medicaid (CMS), “Medicaid Managed Care Options in Responding to COVID-19,” May 14, 2020, https://www.medicaid.gov/sites/default/files/Federal-Policy-Guidance/Downloads/cib051420.pdf. ↩︎

- CMS, COVID-19 Frequently Asked Questions (FAQs) for State Medicaid and Children’s Health Insurance Program (CHIP) Agencies (last updated June 30, 2020), https://www.medicaid.gov/state-resource-center/downloads/covid-19-faqs.pdf (pgs. 83-84 V.C.6). ↩︎

- During the rating period, states may increase or decrease rates by a “de minimis amount” per rate cell. Federal regulations define the de minimis amount as 1.5% per rate cell (§438.7(c)(3)). If, however, the state initially elects to certify a rate range for a rate cell, the state is not permitted to use this de minimis change authority but may increase or decrease a capitation rate within a rate range by up to 1% during the rating period without submission of a new rate certification as long as the resulting rate does not fall outside of the 5 percent range limit allow by federal regulations (42 CFR §438.4(c)(2)(iii)). ↩︎

- John Gallina, Executive Vice President and Chief Financial Officer of Elevance Health Inc., stated: “We’ve been working very closely with our state partners on Medicaid and feel very good about the rating actions.” ↩︎

- Tim Spilker, CEO of UnitedHealthcare Community and State, indicated that states had taken redeterminations into account when setting rates for 2023 and further noted: “[R]evenue is in line with our expectations and consistent with the outlook that we shared in November. So, we’re appreciative of the balanced rational view that our states have taken as they’ve looked ahead, knowing that we’ve got many factors coming forward.” ↩︎

- Centene Corporation 4th Quarter 2022 Earnings Call Transcript, February 7, 2023. ↩︎