Medicaid Eligibility and Enrollment Policies for Seniors and People with Disabilities (Non-MAGI) During the Unwinding

Medicaid is an important source of health and long-term care coverage for low-income people ages 65 and older and those with disabilities. Seniors and people with disabilities account for less than one in four Medicaid enrollees but over half of Medicaid spending. The Medicaid pathways in which eligibility is based on old age or disability are known as “non-MAGI” pathways because they do not use the Modified Adjusted Gross Income (MAGI) financial methodology that applies to children, pregnant individuals, parents, and other non-elderly adults with low incomes. In addition to considering income and age or disability status, non-MAGI eligibility pathways usually require people to demonstrate that they have limited savings and other financial resources (e.g., assets). Medicaid enrollees who use long-term services and supports (LTSS) must also meet requirements related to their functional needs which are generally measured in terms of the ability to perform activities of daily living such as eating and bathing. Because nearly all non-MAGI pathways are optional, eligibility levels vary substantially across states.

Between March 2020 and March 2023, there was a three-year pause on disenrollments, resulting in the largest ever number of enrollees in Medicaid and the lowest ever uninsured rate. Starting in April 2023, states began renewing eligibility for all enrollees as the COVID-related Medicaid continuous enrollment period ended (referred to as the “unwinding”), resulting in 23 million disenrollments as of June 2024. KFF’s recent survey of people who had lost coverage revealed that one quarter of those who were disenrolled remained uninsured, and many reported disruptions in their access to health care.

Even though seniors and people with disabilities often live on fixed incomes and are unlikely to experience eligibility changes, more cumbersome eligibility requirements relative to other groups could result in more people losing coverage. Loss of Medicaid coverage poses unique challenges for seniors and people with disabilities, people who are likely to have high health care spending and rely on Medicaid for coverage of LTSS. Civil rights complaints alleging discrimination against people with disabilities for failure to prioritize their special needs during unwinding have been filed in Colorado, Texas, and Washington D.C.

In this context, KFF’s Survey of Medicaid Financial Eligibility & Enrollment Policies for Seniors & People with Disabilities was conducted in March 2024 by KFF and Watts Health Policy Consulting. The survey sheds light on states’ eligibility, enrollment, and renewal policies for seniors and people with disabilities as of June 2024. Overall, 49 states and the District of Columbia (hereafter referred to as a state) responded to the survey, though response rates to specific questions varied (Florida was the only state that did not respond). Responses were supplemented with publicly available information and information from KFF’s 2022 survey when available. The Appendix tables contain detailed state-level data.

Key takeaways include:

Eligibility policies. The only mandatory eligibility pathway for seniors and people with disabilities is for people who receive Supplemental Security Income (SSI), which limits people to $943 per month in income and no more than $2,000 in savings and other financial assets.

- Unlike Medicaid enrollees who qualify through MAGI pathways, most non-MAGI enrollees must document limited assets. All non-MAGI enrollees under age 65 must also establish that they have a qualifying disability, high health care spending, or need for LTSS.

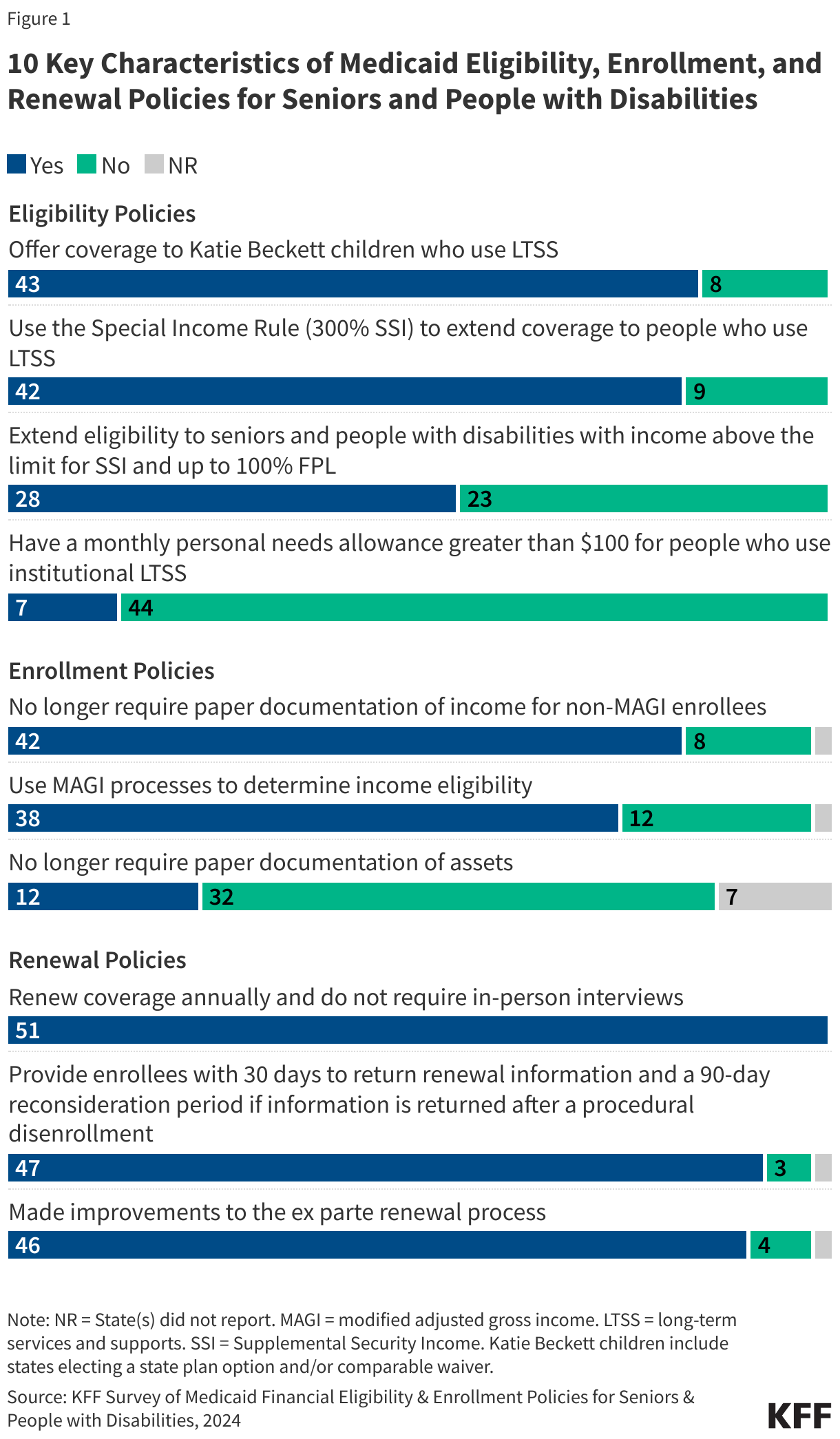

- Just over half of states offer coverage for seniors and people with disabilities to people with incomes above the SSI limit (Figure 1).

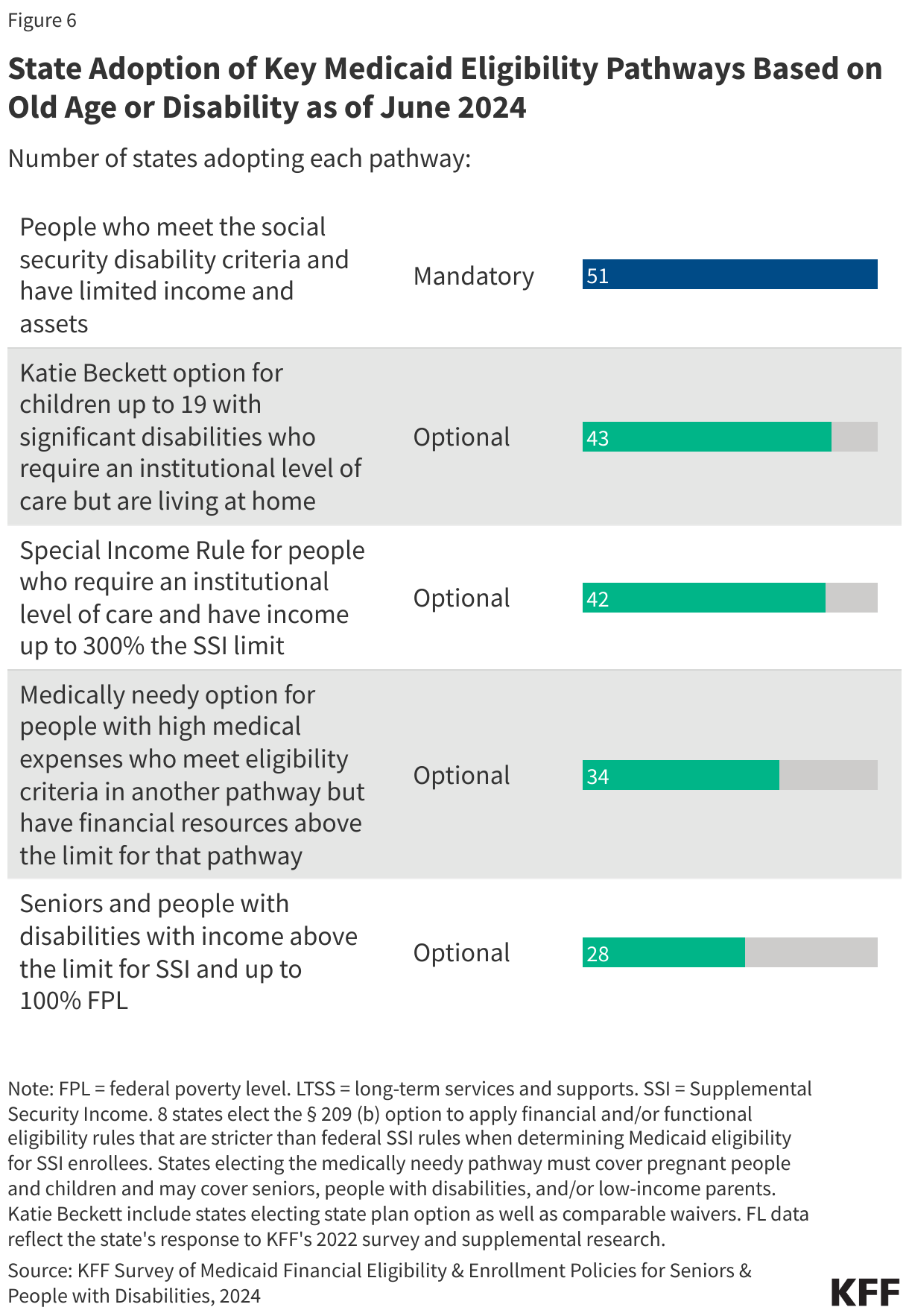

- States are more likely to expand eligibility for people who use long-term services and supports (LTSS). People who are eligible for Medicaid LTSS must also demonstrate that they meet functional requirements for eligibility, which generally require attestation from a medical provider about people’s ability to perform the activities of daily living. Most states offer coverage under the Katie Beckett pathway for children with significant disabilities (adopted by 43 states) and the Special Income Rule for people with LTSS needs with incomes up to 300% of SSI (adopted by 42 states).

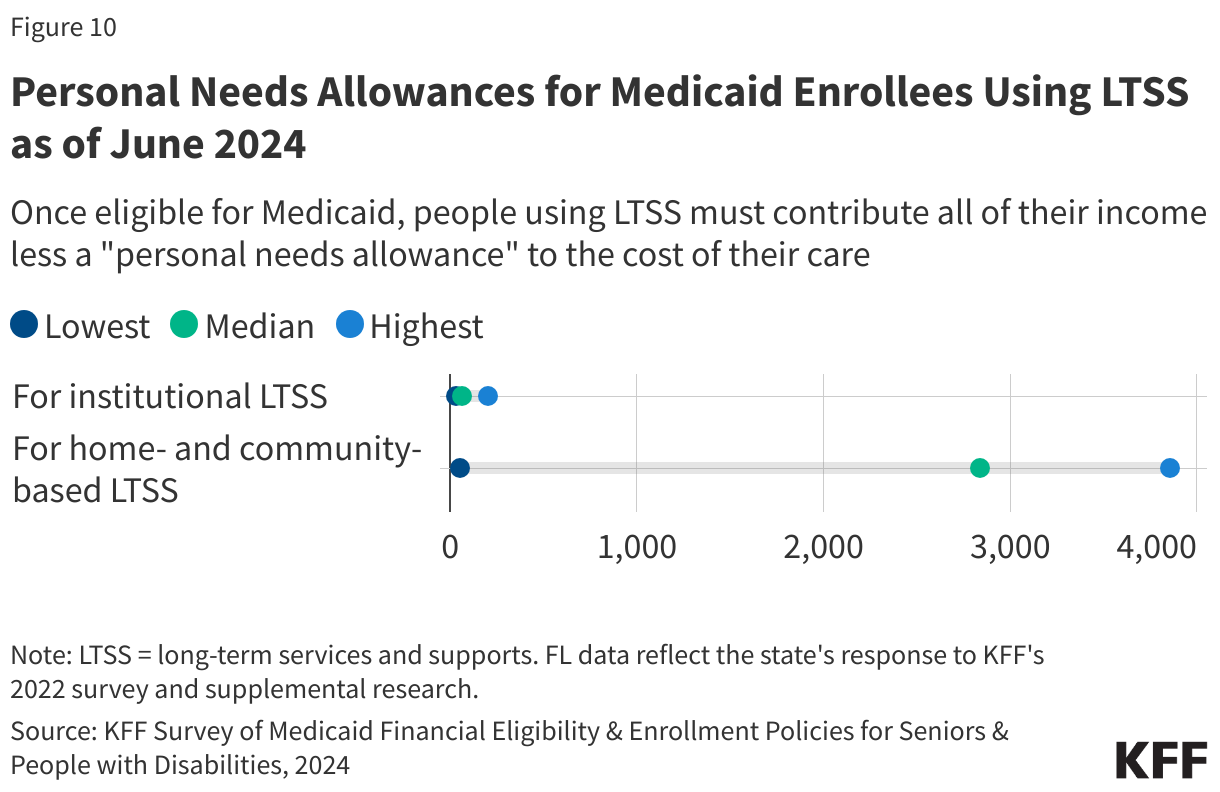

- Medicaid enrollees using institutional LTSS must generally contribute nearly all monthly income to the cost of their care, except for a small “personal needs allowance” to cover expenses such as soap, toothbrushes, clothing, and discretionary spending. There are 24 states with personal needs allowances up to $50, 20 states between $50 and $100, and only 7 states with personal needs allowances greater than $100.

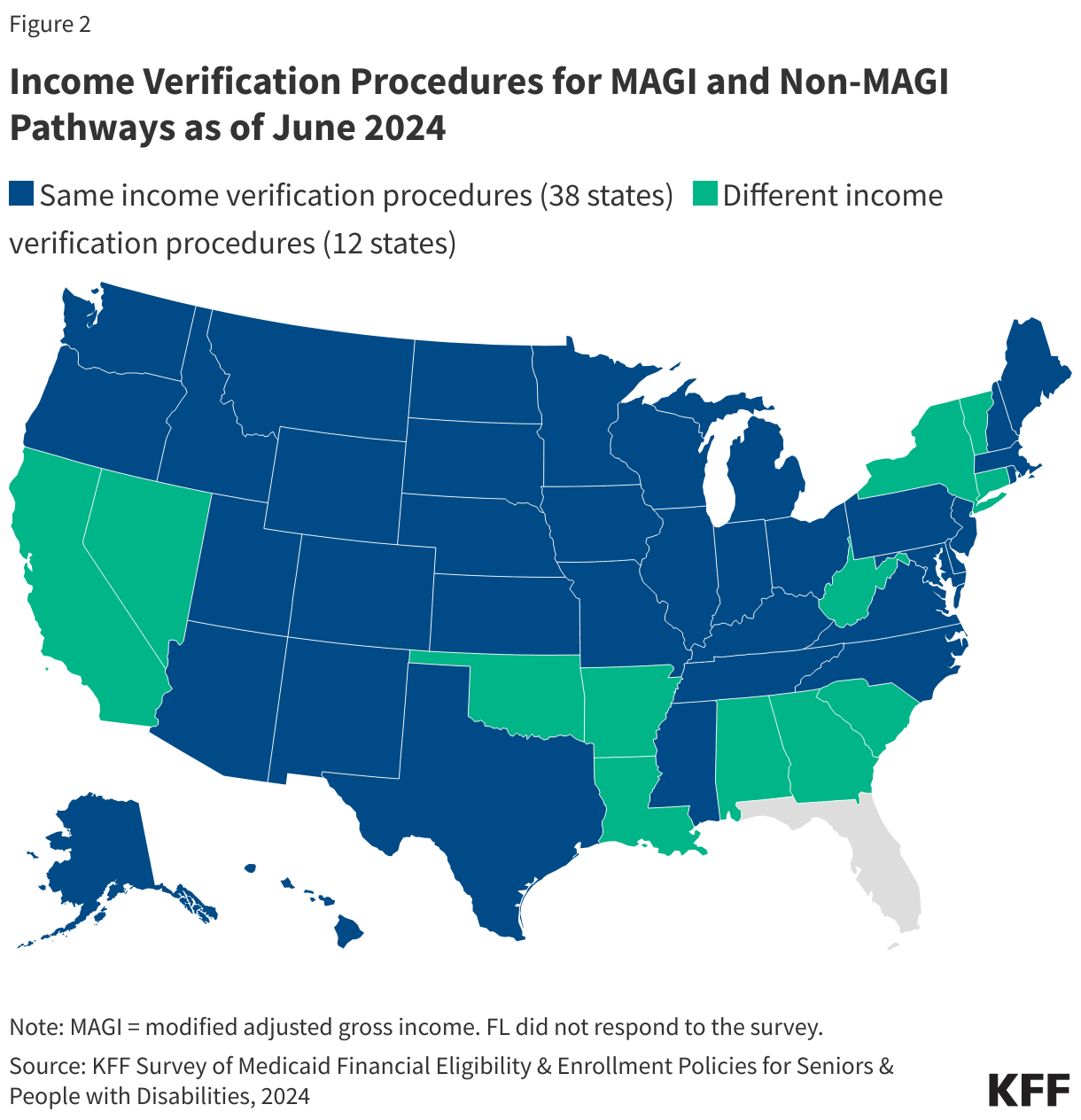

Enrollment policies. Most states (38) now use the same processes to determine income eligibility for all Medicaid enrollees regardless of what pathway they are applying through, but the need to document assets when applying for non-MAGI Medicaid may make non-MAGI applications more onerous (Figure 1).

- In states where income eligibility requirements for non-MAGI pathways differ from those of MAGI pathways, non-MAGI pathways tend to be more cumbersome.

- All states but California require many seniors and people with disabilities to demonstrate that their assets are below Medicaid eligibility limits, and asset eligibility processes are often more cumbersome. For example, when self-reported levels of income and assets differ from electronic sources, 25 states require paper documentation of income levels, and 32 states require paper documentation of assets. California eliminated the asset test beginning this year.

Renewal policies. To prepare for and simplify the unwinding process, states made wide-ranging changes to their renewal processes, many of which may be retained and may help states comply with requirements in the April 2024 final eligibility rule.

- All responding states reported that they only renew eligibility annually for non-MAGI populations and that in-person interviews are no-longer required (Figure 1).

- Nearly all states (47) provide enrollees with 30 days to return renewal information and a 90-day reconsideration period when information is returned following a procedural disenrollment; and 46 states have made changes to increase the rate of ex parte renewals for non-MAGI enrollees. (With ex parte renewals, states automatically renew eligibility using electronic data sources.)

Enrollment and Renewal Policies for Seniors and People with Disabilities

Within broad federal rules, states have discretion when establishing Medicaid application and enrollment policies, which tend to be more complicated for seniors and people with disabilities. Medicaid eligibility through the MAGI pathways is generally based only on income, age, and pregnancy/ family status, but seniors and people with disabilities applying for Medicaid through one of the “non-MAGI” pathways must usually also meet requirements related to financial assets, disability status, and often, their need for long-term services and supports (LTSS) or health care spending. Beyond setting the eligibility criteria, states make a host of other decisions about the application and enrollment process. For example, states decide whether to verify self-reported income and asset limits before enrollment or to issue conditional enrollment and then verify the income and asset amounts afterwards. States have discretion in how to respond when self-reported income and assets differ from the amounts shown in electronic data sources and in what type of documentation they require from applicants. After applicants are determined eligible, they must periodically renew their eligibility, and states have discretion in developing renewal policies.

States’ policies for enrolling people in Medicaid and renewing their coverage have been a focus of policymaker attention given pressures on eligibility workers stemming from the unwinding. The unwinding of continuous enrollment led to an unprecedented volume of eligibility work that came at a time when most states were experiencing workforce shortages and a lack of experience among newly hired staff. To support states encountering significant operational challenges and to protect eligible enrollees from inappropriate coverage losses, CMS provided states with technical assistance and a range of strategies aimed at streamlining the renewal process including allowing states to use section 1902(e)(14)(A) waiver authority. Some strategies are broad, but some are targeted specifically for non-MAGI populations. Beyond changes stemming from the unwinding, states are also updating enrollment and renewal processes to meet new requirements in a April 2024 final eligibility rule, many of which aim to streamline non-MAGI enrollment and renewal policies.

At enrollment, most states (38) use the same processes to determine income eligibility for Medicaid enrollees regardless of whether they are applying through MAGI or non-MAGI pathways (Figure 2). As part of the Medicaid application, all states require applicants to report their estimated income and then, applicants’ self-reported income is compared with income from electronic sources such as the Social Security Administration and Federal Data Services hub. Where state policies vary is in what happens when self-reported (or self-attested) income levels differ from the amounts returned from electronic data sources (Table 1). Federal rules specify that states must accept self-reported values if they are “reasonably compatible” with values from the data source (e.g., if reported income and the state’s electronic data source are both below, at, or above the income eligibility limit). With approval from CMS, states may elect an expanded “reasonable compatibility standard,” such as a percentage or dollar amount. For example, if a state elected a 10% reasonable compatibility standard, if an applicant’s self-reported income is below the eligibility threshold and the data source is above the threshold, but within 10% of the self-reported amount, the data are considered reasonably compatible, and the applicant is determined eligible for Medicaid.

Among the 12 states in which processes differ between MAGI and non-MAGI pathways, states generally have more cumbersome requirements for non-MAGI applicants. For example, 7 states reported that they have a “reasonable compatibility standard” between 10% and 50% for MAGI applicants but no similar standard for non-MAGI applicants; and 5 states reported that MAGI applicants may submit a reasonable explanation of differences, but non-MAGI applicants must submit paper documentation when the income estimates differ.

In all states but California, many seniors and people with disabilities must demonstrate that their assets are below Medicaid eligibility limits, and asset eligibility processes are sometimes administratively more cumbersome than income eligibility processes (Table 1). As of January 1, 2024, California eliminated asset tests for all Medicaid applicants, in part to reduce the administrative burden on applicants and the state. All states must verify income and asset eligibility, but they may do so either before or after enrollment. Most states verify income and asset eligibility before enrollment, but 9 states conditionally enroll applicants based on self-reported income prior to verification whereas only 5 states conditionally enroll applicants based on self-reported assets. Similarly, more states have expanded the reasonable compatibility standards for income purposes (32 states) than asset purposes (6 states). Regulations finalized in April 2024 clarify that reasonable compatibility standards apply to both income and assets, which may reduce those differences in future years. When self-reported data are not compatible with electronic data sources, 25 states require paper documentation of applicants’ income, but 32 states require paper documentation for applicants’ assets. Non-MAGI individuals can submit documents through the following modes: mail (49), local office (49), fax (48), online portal (44), email (37), and mobile devices (18), and 12 states allow individuals to submit documents through any of the six modes listed above.

Few states permit health care providers or other entities to determine non-MAGI eligibility prior to a formal application and approval, a practice known as “presumptive eligibility” (Table 1). Including Florida’s answer to the 2022 survey, there are 10 states that allow hospitals and 3 states allowing a different type of entity to do presumptive eligibility for non-MAGI populations, including the Department of Health in Tennessee, Division of Public Health in Delaware, and local health departments in Georgia. No states reported that providers such as pharmacies, nursing facilities, or home health care providers could do presumptive eligibility.

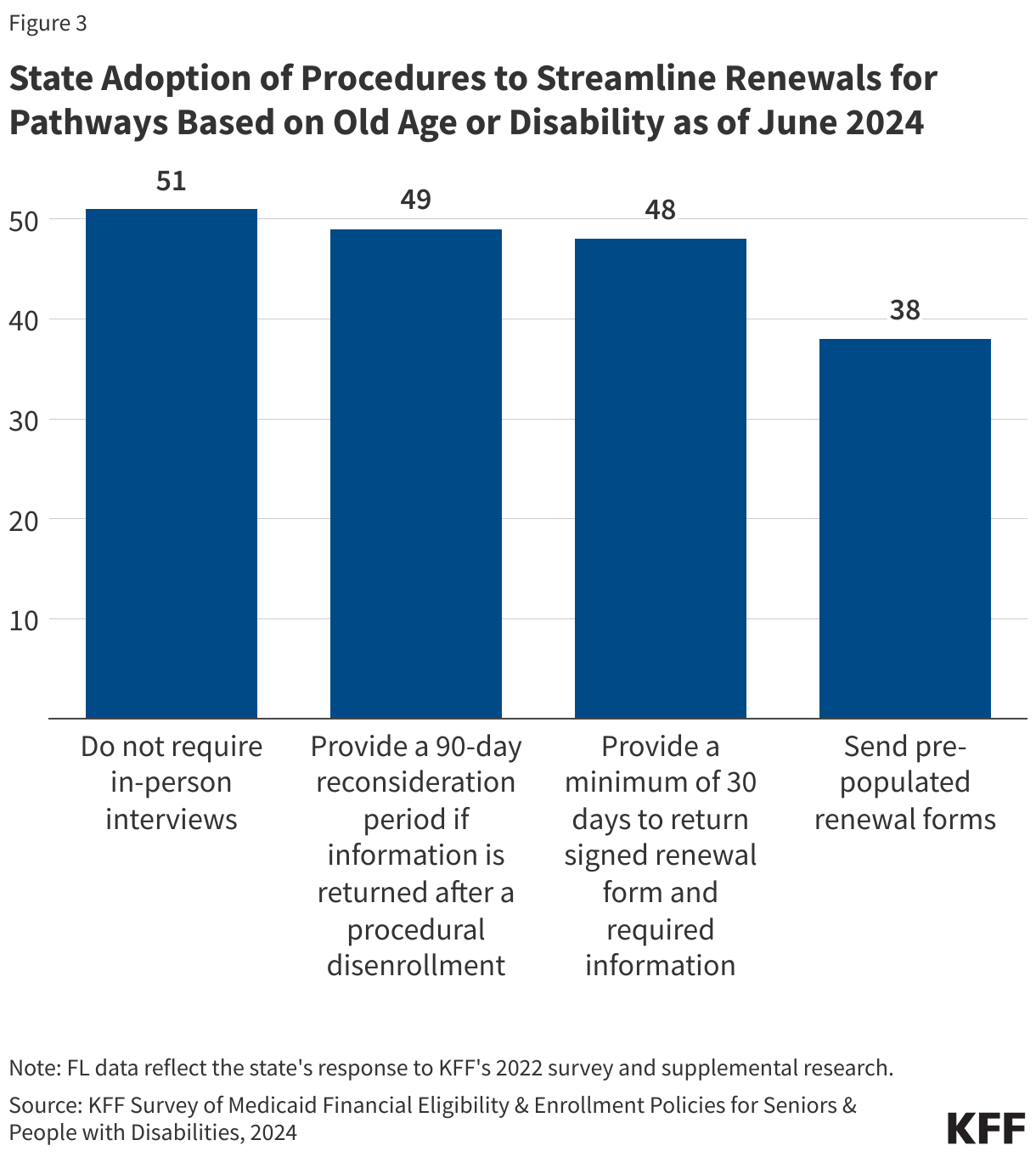

Many changes to streamline enrollment and renewals expedite the unwinding process and conform with new requirements in the April 2024 final eligibility rule (Figure 3, Table 2). The new rule prohibits states from requiring applicants or enrollees to do in-person interviews and from renewing coverage more frequently than once per year, two practices that had historically been applied to non-MAGI applicants and enrollees. All responding states now report that they do not require in-person interviews and that they only renew coverage for non-MAGI populations on an annual basis. All states also reported adopting one or more of the following practices that will be required under the new rule in 2027.

- 49 states provide a reconsideration period of 90-days or longer if information is returned after a procedural disenrollment.

- 48 states provide enrollees with at least 30 days to return signed forms and required information.

- 38 states send pre-populated renewal forms and Georgia sends pre-populated renewal forms when requested.

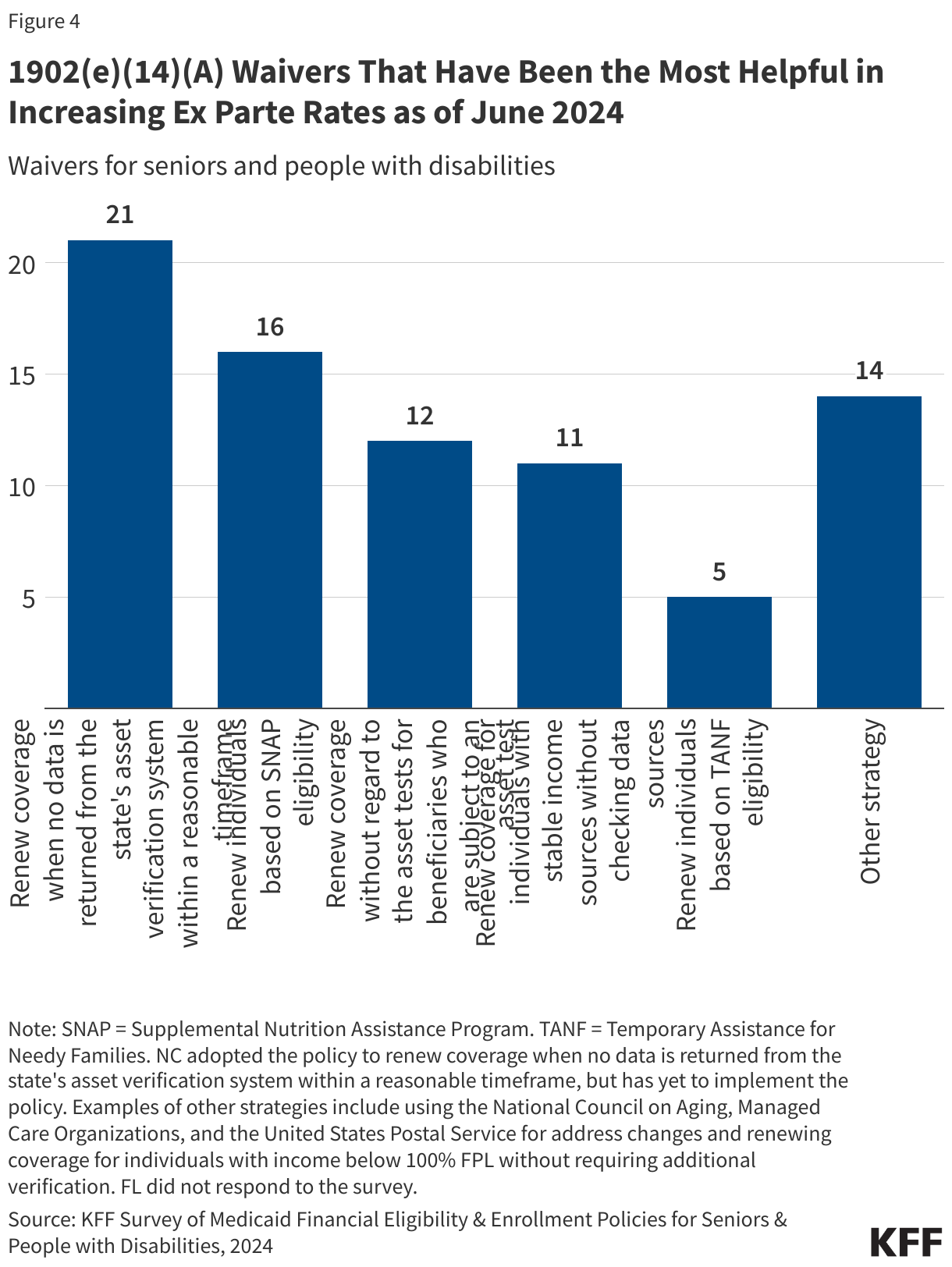

To streamline the unwinding process, 39 states reported that 1902(e)(14)(A) Medicaid waivers had helped increase the number of “ex parte” renewals for non-MAGI enrollees, in which states automatically renew eligibility using electronic data sources before requiring the enrollee to submit forms or documents (Figure 4, Table 3). Ex parte renewals reduce administrative burdens for enrollees and state agencies. Prior to the unwinding, most states reported a higher percentage of renewals being completed for MAGI enrollees than for non-MAGI enrollees, likely on account of the greater administrative requirements associated with non-MAGI eligibility. The 1902(e)(14)(A) waiver option allows states to waive various federal requirements for renewal processes. When asked which waivers had been the most helpful in increasing ex parte renewals, the highest number of states (21) reported waivers to renew eligibility when no information is available about enrollees’ assets from the state’s electronic system. (North Carolina reported adopting that waiver but has not yet implemented it.) Smaller numbers of states reported that the most helpful waivers allowed them to renew eligibility based on eligibility for the Supplemental Nutrition Assistance Program (16 states), renew coverage without regard to asset limits (12 states), and renew coverage for enrollees with stable incomes without checking data sources (11 states). A small number of states reported that the most helpful waivers permitted renewing coverage for people automatically if they had no income or assets in electronic data sources (Alaska and Indiana) or if their incomes were below the federal poverty level (FPL), which is $1,255 for an individual in 2024 (California and Minnesota).

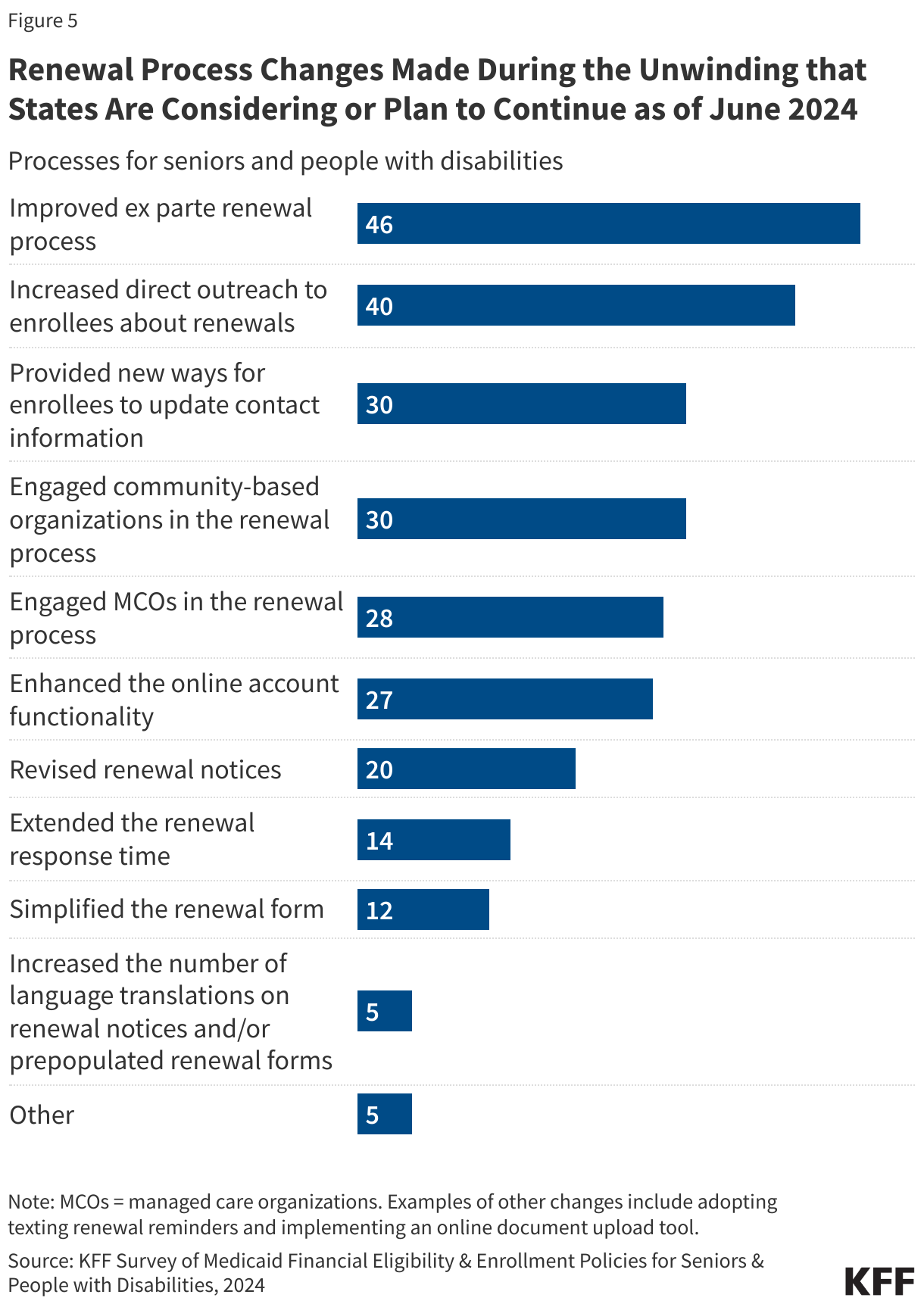

Nearly all states reported considering or planning to continue renewal policies that had been implemented to facilitate renewals during the unwinding and nearly half of states (24) reported planning to continue more than 5 changes (Figure 5, Table 4). The most common changes were efforts to increase ex parte renewals (46 states), followed by increased direct outreach (40 states), new ways for enrollees to update their contact information (30 states), and engagement with community-based organizations (30 states). Over half of states (28) engaged managed care organizations to help with the renewal process and 27 states enhanced online functionalities in their enrollment systems. Other changes states reported include engaging organizations other than managed care or community-based organizations (Connecticut), implementing strategies for returned mail (Minnesota), providing more information about what is required for renewals (Vermont), and sending text messages to remind enrollees of renewals (Washington and Wisconsin).

Primary Medicaid Eligibility Pathways for Seniors and People with Disabilities

The only non-MAGI pathway that states are required to cover is people receiving supplemental security income (SSI), but there is a wide array of additional groups that can be covered at state option (Box 1). Beyond SSI, the main non-MAGI pathways to full Medicaid eligibility include state options to expand coverage to low-income people with disabilities; medically needy individuals who “spend down” by deducting incurred medical expenses from their income; Katie Beckett children with significant disabilities living at home; and adults who use long-term services and supports (LTSS). Each group has different rules about income and assets, making eligibility complex.

| Box 1: Primary Medicaid eligibility pathways based on old age and disability |

| There are many eligibility pathways for people who are ages 65 and older or who have disabilities, but all of them other than SSI are optional for states. In this survey, KFF asked states about the five pathways that constitute the largest sources of Medicaid enrollment among seniors and people with disabilities.

Supplemental Security Income (SSI) Enrollees. States must generally provide Medicaid to people who receive federal SSI benefits. This is the only pathway where eligibility is based on old age or disability that states must include in their Medicaid programs. To be eligible for SSI, people must have low incomes, limited assets, and an impaired ability to work because of old age or significant disability. The maximum SSI federal benefit rate is $943 per month for an individual and $1,415 for a couple in 2024, which is 75 percent of the federal poverty level (FPL). The effective SSI income limit may be somewhat higher than 75% FPL in some states, due to state supplemental payments and/or additional income disregards. SSI enrollees also are subject to an asset limit of $2,000 for an individual and $3,000 for a couple. Katie Beckett Children with Disabilities. The “Katie Beckett” option allows states to extend coverage to children up to age 19 who meet the SSI medical disability criteria and qualify for an institutional level of care but are living at home. States may target different populations based on the type of institutional care that would be required (hospital, skilled nursing facility, or intermediate care facility for people with mental disease or intellectual/ developmental disabilities). Under the Katie Beckett pathway, only the child’s income and assets are considered for eligibility purposes. Special Income Rule. States can elect the “special income rule” pathway to cover people with incomes up to 300% of the SSI benefit rate ($2,829 in 2024) and functional needs qualifying them for an institutional level of care. Most states limit enrollees to $2,000 in assets for an individual or $3,000 for a couple and offer the pathway to people regardless of whether they are using LTSS in an institutional or community setting. Medically Needy Coverage. States use medically needy pathways to extend coverage to people who would be eligible through another pathway but have income or assets that exceed the limit for that pathway. People may qualify through a medically needy pathway if their income is higher than permitted under a different pathway but lower than the medically needy limit, or if they “spend down” to the medically needy limit by deducting health care expenses from their income. For people who spend down to eligibility, states select a budget period between one and six months during which the individual must incur enough expenses to decrease their income below the limit. Seniors and People with Disabilities up to 100% FPL. States can choose to extend Medicaid to seniors and people with disabilities whose income exceeds the SSI limit but is below the federal poverty level (FPL, $1,255 for an individual in 2024). States can also choose to apply an asset limit to this pathway, usually $2,000 for an individual. |

In 2024, the most common optional non-MAGI eligibility pathways were those for people who use LTSS and required an institutional level of care (Figure 6, Table 5). The two primary eligibility pathways for people who use LTSS include Katie Beckett coverage for children who have significant disabilities and require an institutional level of care but are living at home (43 states) and the special income rule, which covers other people who require an institutional level of care and have incomes up to 300% of the SSI benefit rate (42 states). There are 34 states offering medically needy coverage and 28 states that have extended eligibility for seniors and people with disabilities who have income above the SSI eligibility thresholds.

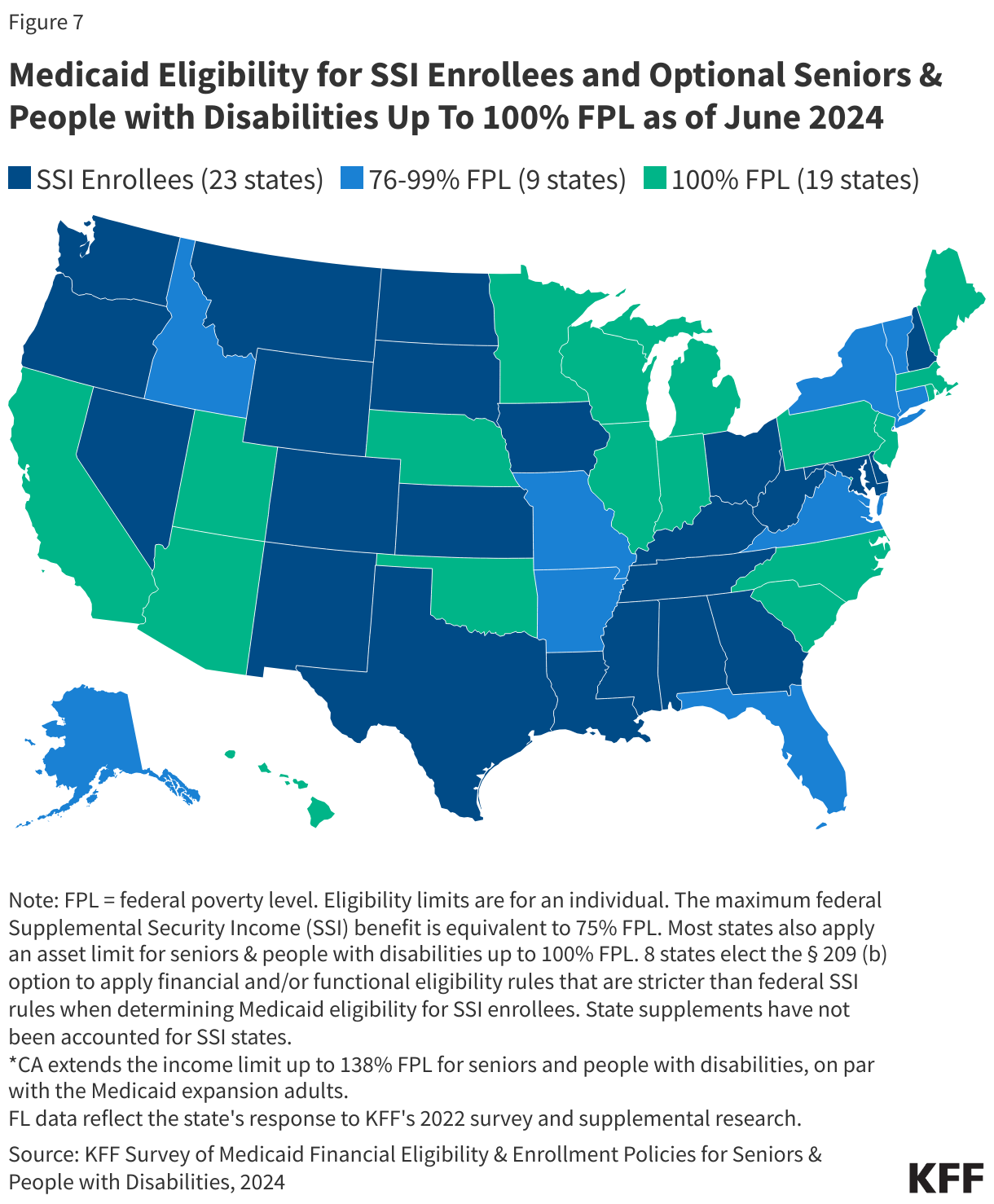

All states provide Medicaid to people with SSI, and just over half (28) of states expand coverage for people with income above SSI limits (Figure 7 and Table 6). The maximum SSI federal benefit amount is $943 per month for an individual and $1,415 for a couple in 2024, which is 75% of the federal poverty level (FPL), but over half of states now cover people with incomes greater than the SSI rate, including 18 states with coverage at the FPL and 9 states with coverage between 75% and 100% of the FPL. With eligibility at 138% FPL, California is the only state to offer coverage to people with incomes greater than the FPL ($1,732 for an individual). Most states set asset limits at $2,000 for an individual and $3,000 for a couple, although several states have established higher limits, and California and Arizona reported not having asset limits.

There are two mechanisms states can use to increase eligibility levels for seniors and disabilities: First, some states supplement the federal SSI benefit with additional payments, which increases the total SSI benefit and results in higher income limits for Medicaid enrollees. Second, states may adopt the 100% FPL coverage group to cover people with incomes greater than the SSI limit but lower than the poverty level. Louisiana reported adopting the 100% FPL coverage pathway but sets eligibility for that pathway at SSI levels.

In terms of enrollment, there are three ways that states elect to enroll SSI recipients into Medicaid. In 35 states, the Social Security Administration determines eligibility for Medicaid when establishing SSI eligibility. There are 8 Section 209(b) states which use financial or functional eligibility criteria that are more restrictive than the federal SSI rules, but no more restrictive than the rules the state had in place in 1972 when SSI was established. The remaining 7 states use SSI criteria to determine eligibility but do not auto-enroll recipients into Medicaid. When asked why they did not use auto-enrollment, states reported that the process is too cumbersome to implement or they have requirements beyond SSI eligibility such as an application and/or interview.

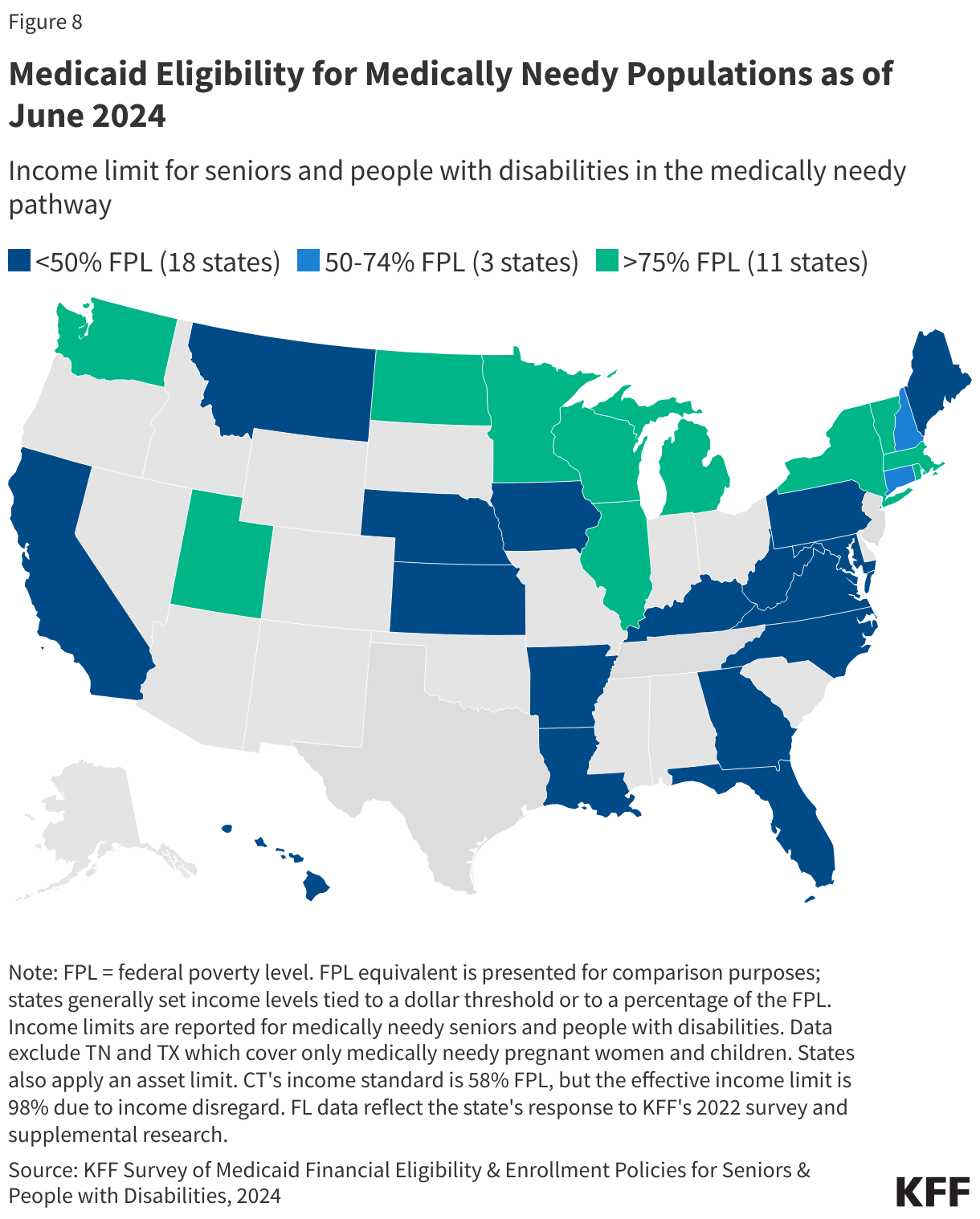

More than half (34) of states have medically needy pathways to Medicaid eligibility, but most income eligibility levels are low—usually below 50% of the FPL (Figure 8 and Table 7). If states offer medically needy coverage, they must offer it to pregnant women and children, so all 34 states offer medically needy coverage to pregnant women and children, 32 states offer it to seniors and people with disabilities, and 21 offer it to low-income parents. Income limits for medically needy coverage are low because the income limits often reflect income after payment of medical expenses and because when states created their medically needy programs, most states linked income eligibility to the income limits for cash assistance programs. Among states with medically needy programs, 15 states use a dollar threshold to determine income eligibility, 12 states use a percentage of the FPL, and 6 states use another basis. The median income limit is $504 or 40% of the FPL, and many states limit enrollees to $2,000 in assets.

Unlike other Medicaid eligibility pathways, states are not required to cover mandatory benefits in their medically needy programs, and they require enrollees to re-establish eligibility as frequently as once per month (Table 7). For most Medicaid eligibility groups, there are benefits that states are required to offer to all enrollees, but states may choose which benefits to cover in the medically needy programs. Among the 34 states that offer medically needy programs, 25 states reported covering nursing facility services. In other states, nursing facility services would not be covered and people’s spending on nursing facility care would not count as health care spending for the purposes of establishing eligibility. Given the high costs of nursing facility care, the exclusion of nursing facility coverage may have a significant impact on people’s ability to qualify through this pathway, but individuals that need nursing facility care may be eligible for Medicaid through another LTSS pathway. Medically needy coverage also requires individuals to periodically reestablish eligibility by incurring sufficient medical and LTSS expenses to reduce their countable income to the state’s medically needy income level. The timeframe for these “budget periods” ranges from 1 month (9 states) to 1 year (2 states). The most common budget period is 6 months (12 states).

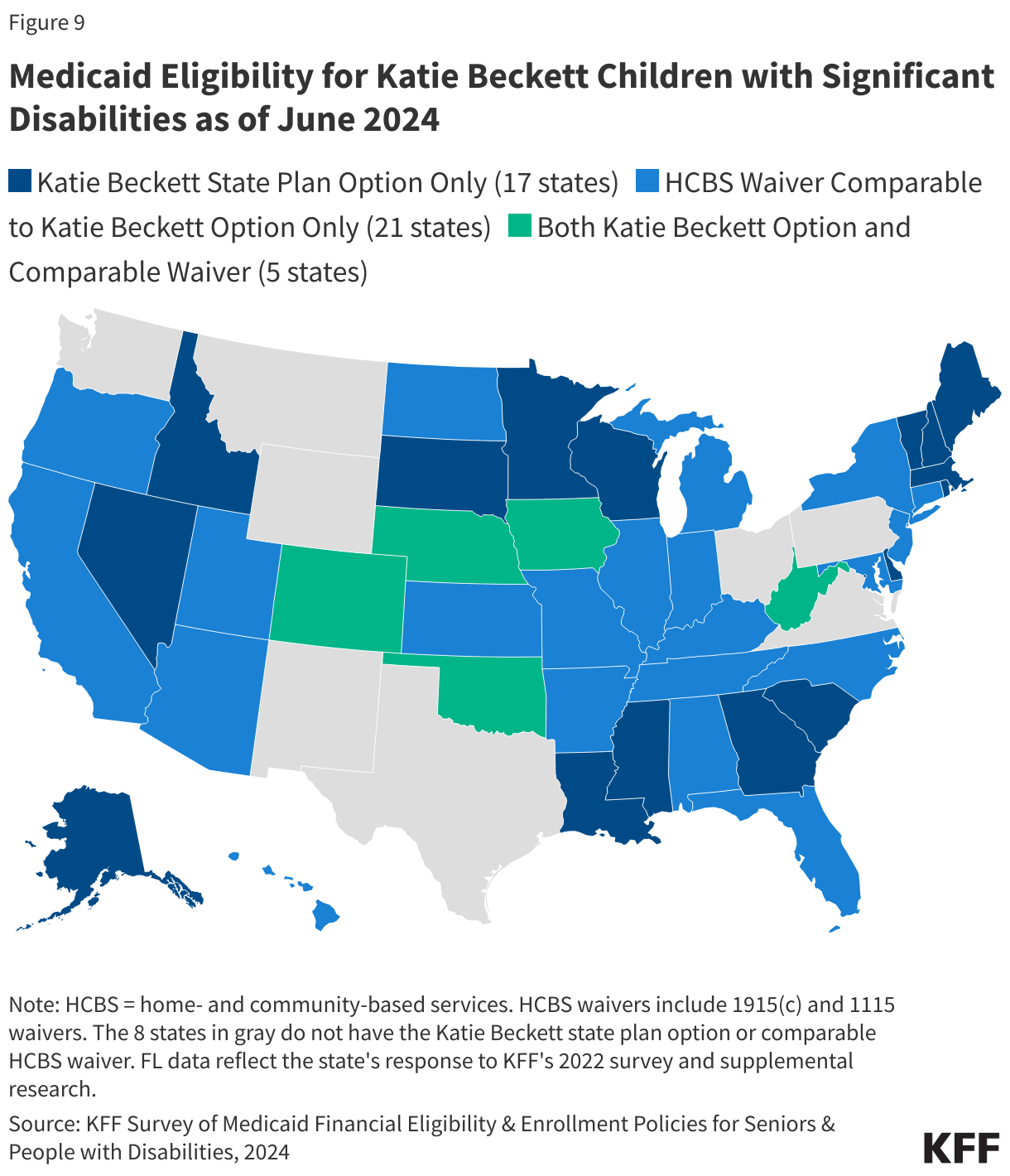

Most states adopt the Katie Beckett option to cover children with significant disabilities who live in the community or provide coverage through a comparable waiver program (Figure 9 and Table 8). In 2024, 43 states reported offering Katie Beckett coverage, with Washington currently pursuing coverage through an 1115 waiver, which will bring the total number of states with coverage back to 44 as was the case in 2022. Among those states, 17 states offer coverage through the state plan, 21 states offer coverage through a waiver, and 5 states have both waiver and state plan options. The most common income limit is $2,829 (used by 31 states), which equals 300% of the SSI benefit rate or 225% of the FPL. All states except for Massachusetts update income limits annually. Most states limit individuals to $2,000 in assets but 7 states have no limits (California, Hawaii, Illinois, Kansas, Minnesota, North Dakota, and Wisconsin).

Most states (42) adopt the special income rule and offer Medicaid coverage to people with incomes up to 300% of the SSI benefit rate ($2,829 per month for an individual in 2024) for people who need LTSS (Table 8). When adopting the special income rule, states may determine whether to adopt it for people using institutional LTSS, such as nursing facility care, and separately, whether to adopt it for people using home- and community-based services (HCBS), such as personal care. In 2021, KFF estimated that over 5.6 million people used Medicaid LTSS, and that most of them received HCBS. Among the 42 states that extend Medicaid to people who use LTSS, 41 states adopt the special income rule for institutional LTSS and 41 states adopt the rule for HCBS. As in 2022, Massachusetts was the only state to report adopting the special income rule for HCBS but not institutional care and New Hampshire was the only state to report adopting the rule for institutional care but not HCBS. Delaware is the only state that adopts the special income rule but sets income eligibility limits below 300% SSI, setting eligibility at 250% of the federal poverty level instead instead ($2,358 in 2024). (In all states, institutionalized individuals are treated as single-person households after eligibility has been established.)

For Medicaid enrollees who are eligible for Medicaid because they use LTSS, most states (37) limit the value of applicants’ homes to the federal minimum level ($713,000 in 2024), but all states disregard some home equity when calculating the home’s value (Table 9). In 2024, federal rules specified that if states place limits on applicants’ home values, those limits must be between $713,00 and $1,071,000. There are 11 states that set the home equity limit at the maximum level and 2 states that use a limit in between the federal minimum and maximum. Those amounts are updated annually based on changes in SSI benefit rates and the consumer price index. California has no home equity limit on principal residence. When estimating the value of the home, all states disregard some home equity for LTSS eligibility. When and how limits on home equity apply, is often complicated. For example, if the Medicaid enrollee has a spouse or child who is under 21, blind, or disabled living in the home, it is exempt from home equity limits and does not count towards the limit of people’s assets. In other circumstances—notably, when an enrollee is living in a nursing facility and does not intend to return home—the home may instead be counted as an asset for determining financial eligibility.

Once eligible for Medicaid, individuals using institutional care generally must contribute nearly all monthly income to the cost of their care, except for a small “personal needs allowance,” which was $55 in the typical state in 2024 (Figure 10, Table 9). Personal needs allowances are intended to cover costs that Medicaid does not pay for, ranging from personal hygiene supplies such as soap and toothbrushes to clothing to self-care such as haircuts. Any discretionary spending—such as purchasing gifts for loved ones or travel—would also come from the personal needs allowance. In 2024, the median monthly personal needs allowance for a Medicaid enrollee residing in an institution is $55, up from $50 in 2022. There are 24 states with personal needs allowances up to $50, 20 states between $50 and $100, and only 7 states with personal needs allowances greater than $100. Such limited personal needs allowances leave nursing facility residents with few resources for purchasing necessities, and generally, no income to cover discretionary expenses.

Personal needs allowances are generally higher for individuals receiving HCBS in recognition that enrollees living in their homes continue to incur costs such as rent, electricity, and food. The median monthly allowance for individuals receiving HCBS waiver services is $2,829 in 2024, which equals 300% of the SSI benefit rate and was reported by 20 states. There were 20 states that reported personal needs allowances below that rate and 2 states that reported allowances above that rate. (In some states, personal needs allowances differ across the HCBS waivers. KFF asked states to report the allowance associated with the waiver that had the highest enrollment.)