A Look at Navigating the Health Care System: Medicaid Consumer Perspectives

This brief gauges Medicaid enrollees’ perspectives on their health insurance, based on findings from KFF’s Survey of Consumer Experiences with Health Insurance, fielded February 21 through March 14, 2023. Importantly, people covered by different types of insurance have different levels of income, education, and health status, which may affect their experiences and views. Adults with Medicaid are more likely to be younger, female and to have lower incomes. They are also more likely to describe their health as “fair” or “poor” than those with other coverage. Medicaid also has limited or negligible premiums and out-of-pocket costs, which may affect the types of problems enrollees face. This brief provides an overview of the survey findings, describes Medicaid enrollees’ views of their health and health coverage, explores problems those with Medicaid experience, compares how Medicaid performs relative to Medicare and private coverage, and reviews variation in Medicaid experiences. Key take-aways include the following:

- Medicaid enrollees report worse health status compared to those with other coverage, which could lead to greater need for health care and more opportunities to encounter problems with the system. Still, the large majority (83%) of Medicaid enrollees rate the overall performance of Medicaid positively. However, over half of Medicaid enrollees report having experienced a problem in the past year, and relative to Medicare and employer-sponsored insurance (ESI), Medicaid enrollees are more likely to report certain negative outcomes from insurance problems.

- Medicaid enrollees report fewer cost-related problems relative to those with Marketplace coverage and ESI; however, Medicaid enrollees report more problems with prior authorization and provider availability compared to people with other insurance types.

- Across racial and ethnic groups, most enrollees rate their Medicaid coverage positively, with White Medicaid enrollees the most likely to describe their insurance as “excellent.” Similar shares of enrollees among all racial and ethnic groups report experiencing problems with their coverage. Similar to the experiences of people with other coverage, Medicaid enrollees who utilize more health care services experience more problems with their insurance.

Proposed federal rules related to Medicaid access and prior authorization that are pending aim to address some of the problems faced by Medicaid enrollees.

How do Medicaid enrollees view their health and health coverage?

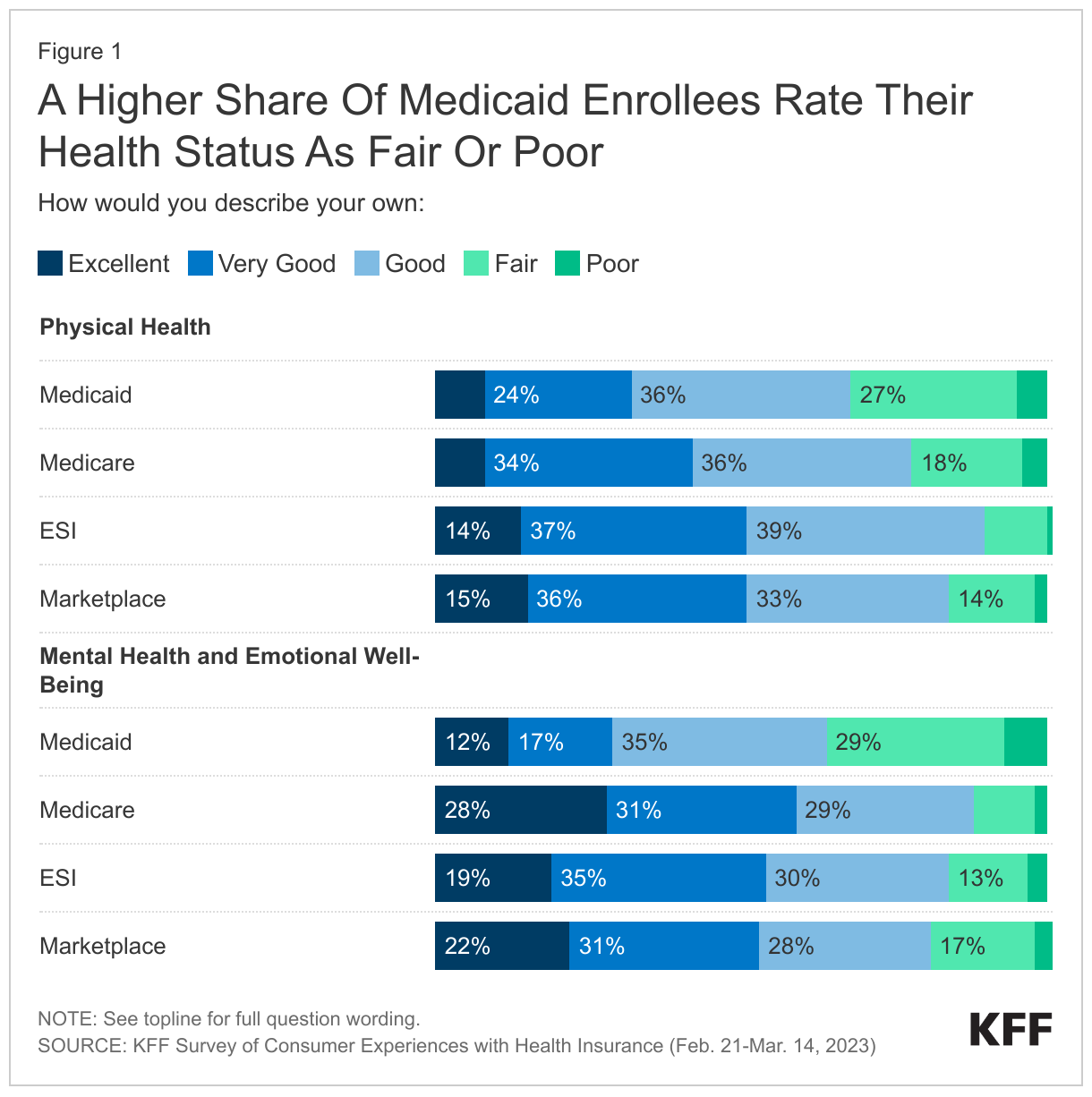

A higher share of Medicaid enrollees rate their health status as fair or poor relative to adults with other coverage. About one-third (32%) of those with Medicaid describe their physical health status as “fair” or “poor.” Over a third (36%) of Medicaid enrollees report “fair” or “poor” mental health, a rate much higher than Marketplace enrollees (20%) and over double the rate of those with Medicare or employer-sponsored insurance (ESI).

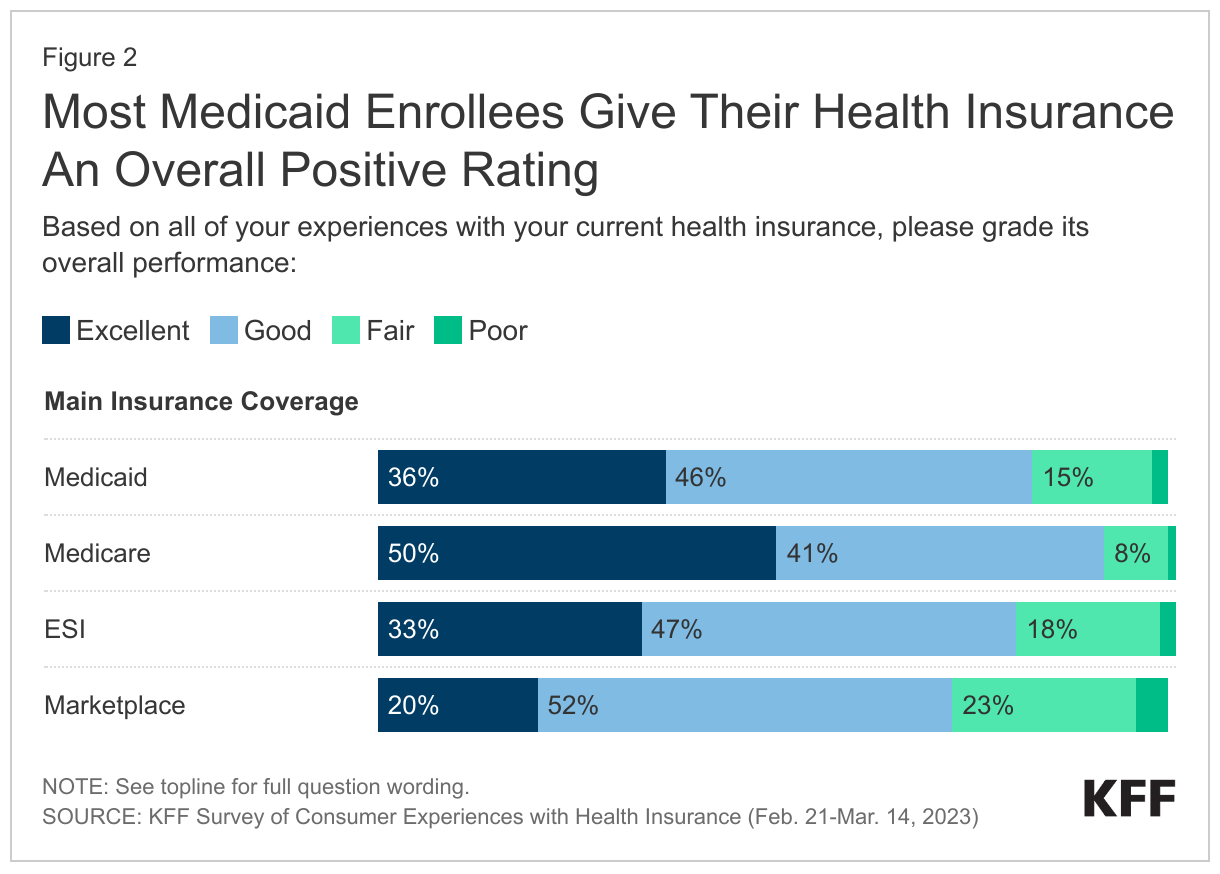

Despite worse health status – which could lead to greater need for health care and more opportunities to encounter problems with the system – the large majority (83%) of Medicaid enrollees rate the overall performance of their current health insurance as either “excellent” or “good.” This positive rating is similar to ratings among those with ESI (80%), lower than those with Medicare (91%) and higher than those with Marketplace coverage (73%).

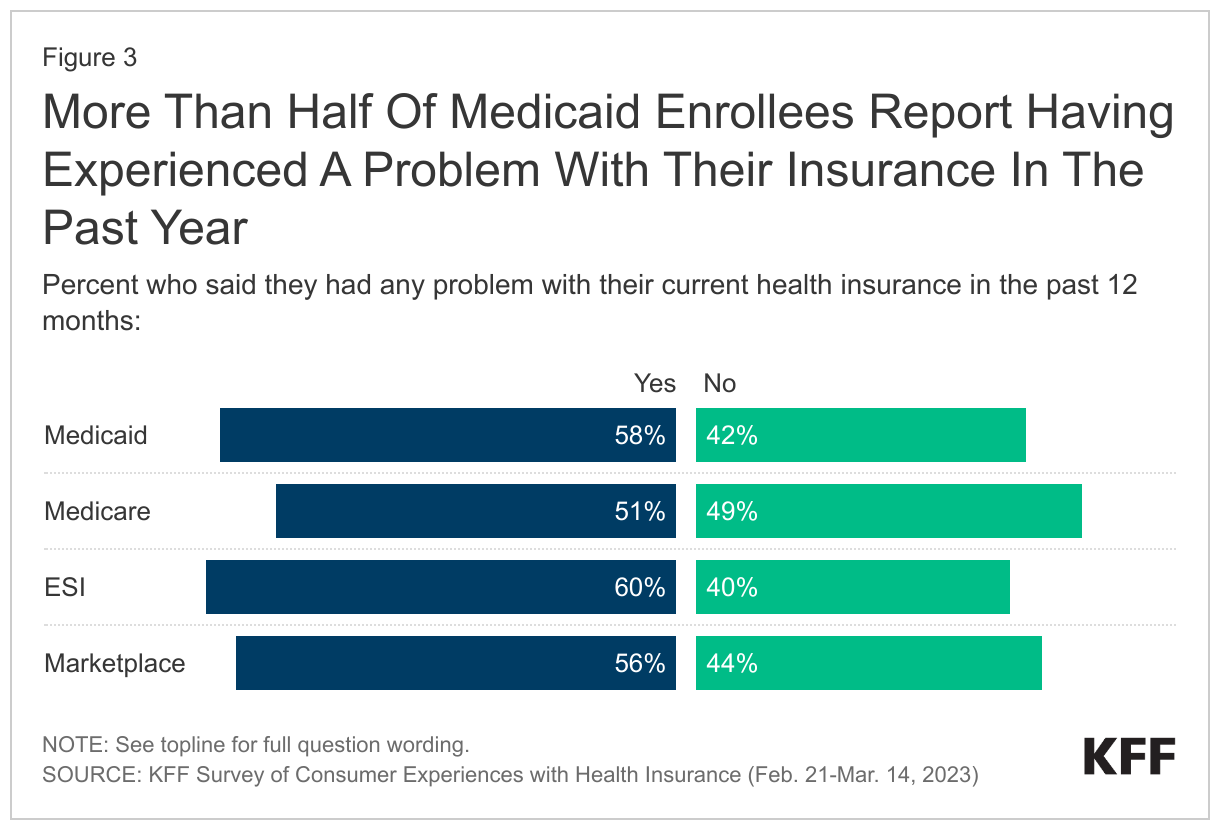

Even though most enrollees view their insurance positively, over half report having experienced a problem in the past year. The share of those with Medicaid reporting any problem with their insurance (58%) is similar to those with ESI (60%) and Marketplace coverage (56%), and higher than those with Medicare (51%). Though majorities across insurance types report at least some problem with their insurance, the nature of problems people experience differs across health coverage types. For example, those with private coverage are more likely to experience cost-related issues while those on Medicaid are more likely to report problems with prior authorization and provider availability.

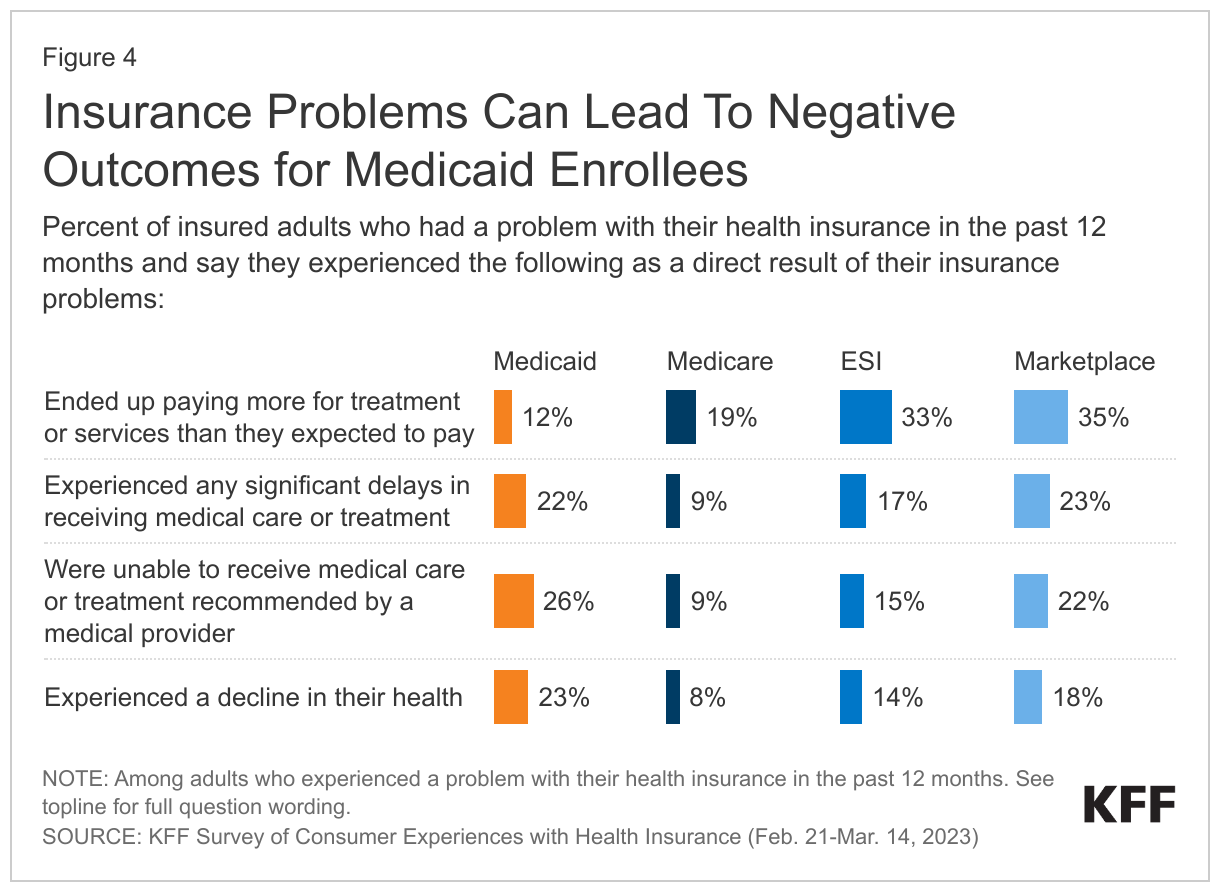

Relative to adults with Medicare and ESI, Medicaid enrollees are more likely to report certain negative outcomes from insurance problems. For example, Medicaid enrollees are more likely to report experiencing a decline in health (23%) and being unable to receive recommended treatment (26%) because of a problem they had with their insurance. Medicaid enrollees’ experiences on these measures are similar to those with Marketplace coverage. However, Medicaid enrollees are less likely than those with other insurance types to report having to pay more than expected for treatment or services (12%).

In what ways do Medicaid enrollees view their coverage more favorably compared to views of those with other coverage?

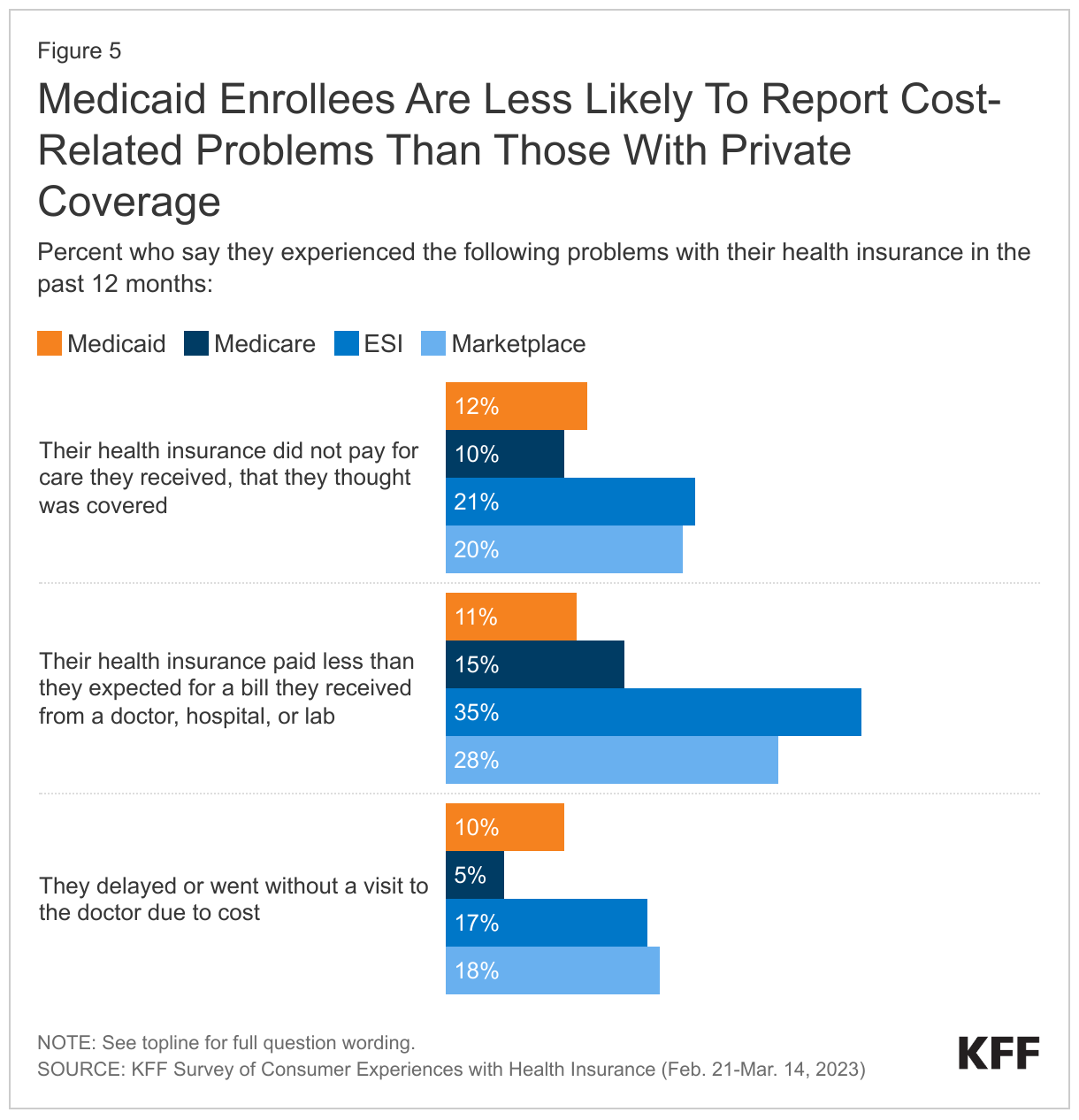

Medicaid enrollees are less likely to report cost-related problems than those with Marketplace coverage and ESI, but as likely to report these problems as those with Medicare. Smaller shares of adults with Medicaid (11%) say their insurance paid less than they expected for a medical bill, compared to those with private coverage (ESI 35%, Marketplace 28%). Similarly, Medicaid enrollees are less likely to report that insurance paid nothing at all for a service they thought was covered (12%) compared to those with private coverage (ESI 21%, Marketplace 20%). Smaller shares of adults with Medicaid report delaying a visit to the doctor’s office in the past year due to cost (10%) than those with ESI (17%) or Marketplace plans (18%). Enrollees with Marketplace and ESI plans can face significant cost sharing in the form of high deductibles, high out-of-pocket limits, and coinsurance or copay requirements. Given that Medicaid enrollees have low incomes, federal rules generally have protections to limit out-of-pocket costs that can help improve access.

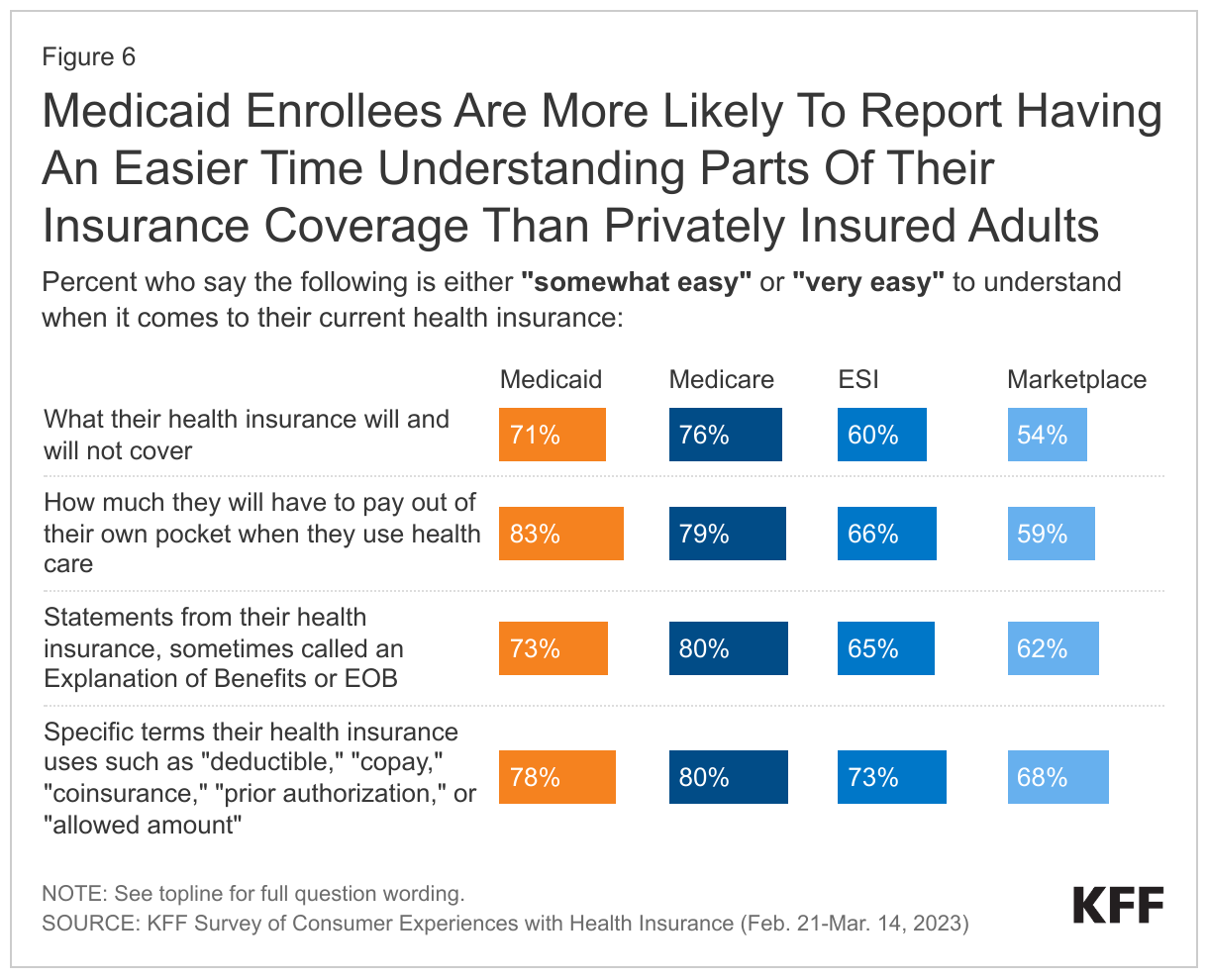

Medicaid enrollees are more likely to report having an easier time understanding parts of their insurance coverage than privately insured adults. Over seven in ten (73%) Medicaid enrollees compared to over six in ten (62%) of those with Marketplace plans and 65% of those with ESI say they find it easy to understand statements explaining whether or how much insurance will pay for care; these statements are called Explanation of Benefits, or EOBs. Additionally, more than eight in ten Medicaid enrollees describe understanding what they would owe out-of-pocket as easy, a much higher share than those with ESI (66%) or Marketplace coverage (59%). About seven in ten Medicaid enrollees easily understand what their insurance does and does not cover, while smaller shares of adults covered in Marketplace plans (54%) or ESI (60%) cite similar ease. Medicaid enrollees also report having an easier time understanding specific terms, such as “deductible,” “coinsurance,” “prior authorization,” or “allowed amount” than those with private insurance. This comparative ease in understanding by Medicaid enrollees may be a result of limited out-of-pocket costs for Medicaid plans leading to a simpler plan design.

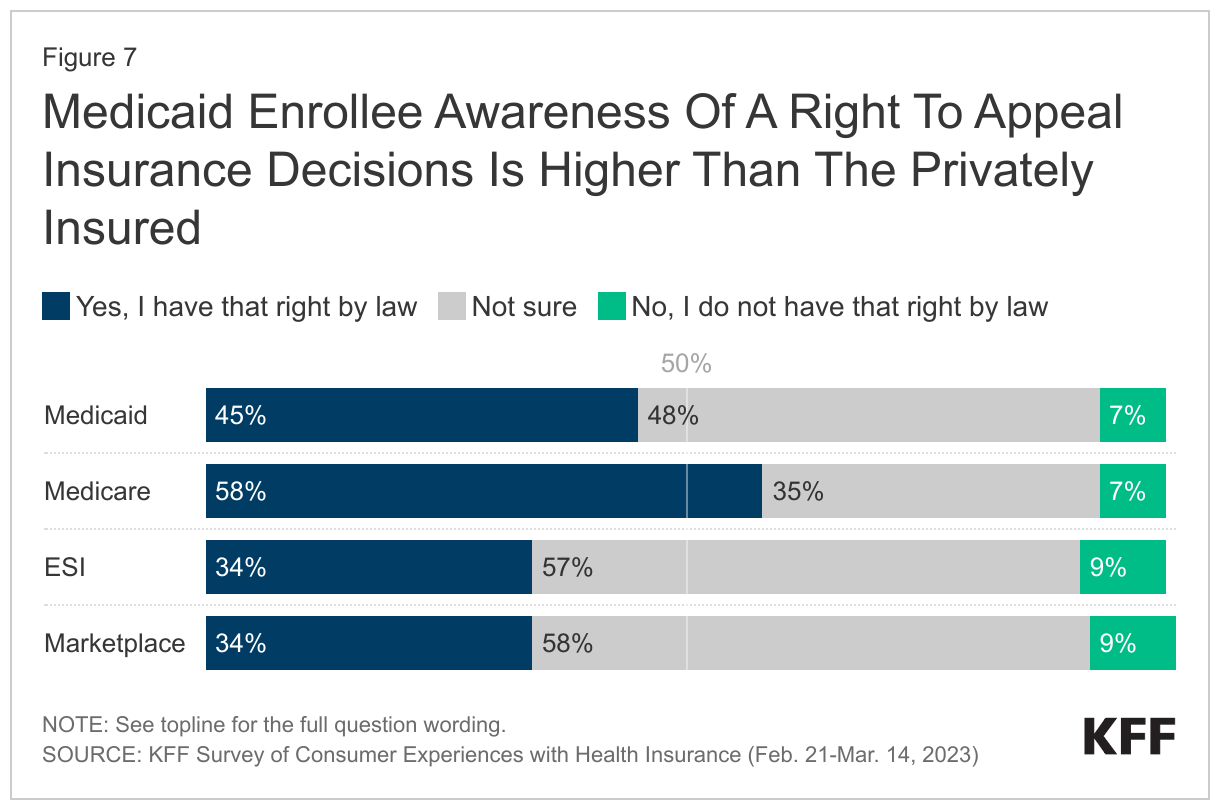

Although a majority of Medicaid enrollees are unaware they have a right to appeal insurance decisions, Medicaid enrollees are more likely to be aware of these appeal rights than those who are privately insured. Less than half of Medicaid enrollees (45%) report being aware of their legal right to appeal to a government agency or an independent medical expert if their health insurance refuses to cover medical services they think they need, with most either incorrectly saying they do not have appeal rights (7%) or saying they are not sure if this is a right they have (48%). However, Medicaid enrollees have a higher awareness of their right to an appeal than those who are privately insured, with 34% of those with ESI or Marketplace coverage reporting they are aware of their right to appeal insurance decisions.

In what ways do Medicaid enrollees view their coverage less favorably compared to views of those with other coverage?

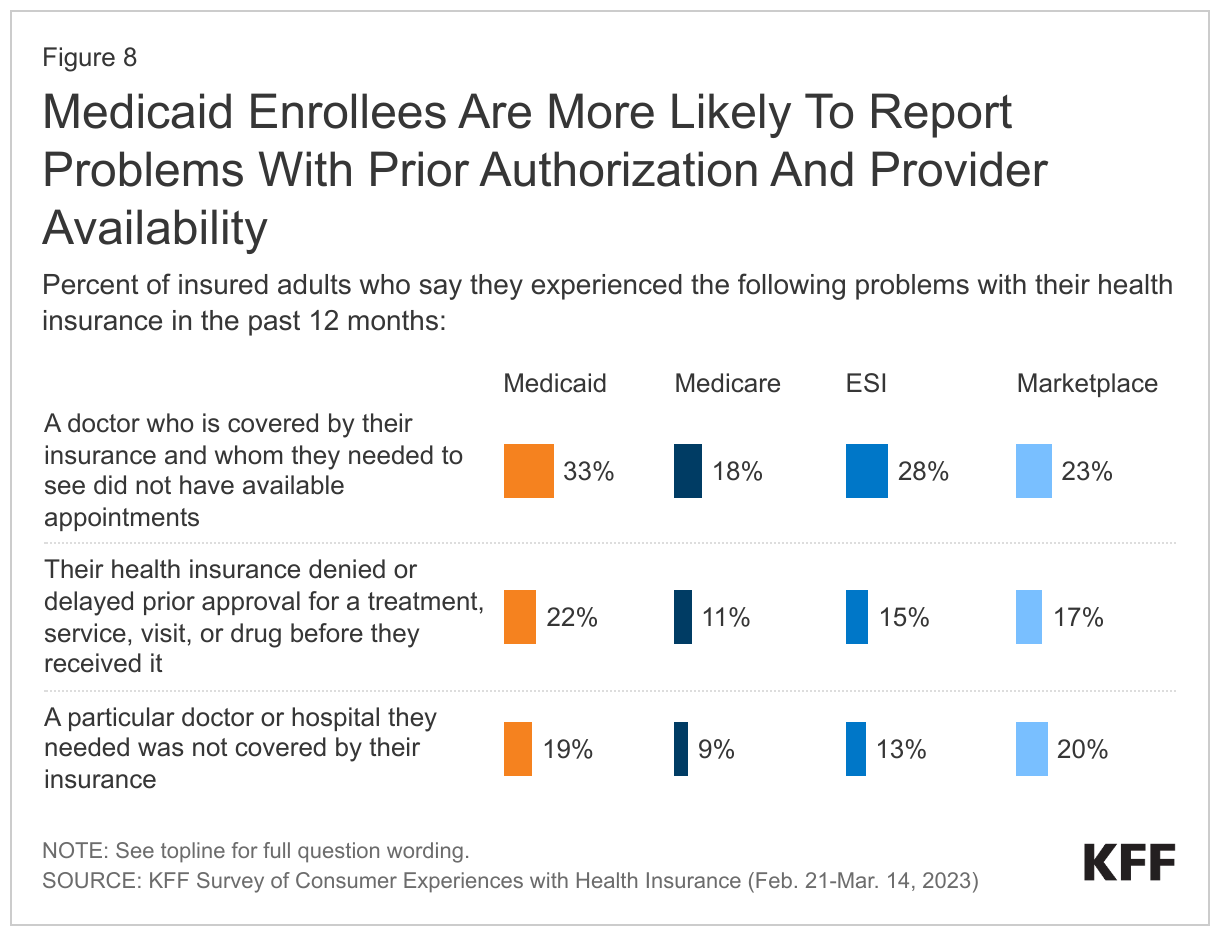

Medicaid enrollees are more likely to report problems with prior authorization. About one in five adults with Medicaid (22%) report that their health insurance denied or delayed prior approval for a treatment, service, visit, or drug before they received it, which is double the rate of adults with Medicare (11%). Consumers with prior authorization problems tend to face other insurance problems and are far more likely to experience serious health and financial consequences compared to people whose problems did not involve prior authorization.

Medicaid enrollees were also more likely to have problems finding providers available to care for them. One in three Medicaid enrollees report that a doctor covered by their insurance who they needed to see did not have available appointments, the highest share of any coverage group. Nearly one in five adults with Medicaid also report that a doctor or hospital they needed was not covered by their insurance, a higher share than adults with Medicare (9%) or ESI (13%) and a similar share to adults with Marketplace plans (20%). Overall, adults with Medicaid are more likely than adults with any other insurance type to report receiving care in the emergency room, with Medicaid enrollees twice as likely to report receiving care in the emergency room compared to those with ESI or Marketplace coverage. Higher emergency room utilization may be due to barriers in accessing providers as well as a number of other factors, including higher disease burden and minimal cost sharing requirements for emergency room care.

While a large body of research shows that Medicaid beneficiaries have substantially better access to care than people who are uninsured, lower provider payment and participation rates may contribute to findings that Medicaid enrollees experience more difficulty obtaining health care than those with private insurance. In 2021, MACPAC found physicians were less likely to accept new Medicaid patients compared to other payers, but rates may vary by state, provider type, and setting. Acceptance of new Medicaid patients was much higher where physicians practiced in community health centers, mental health centers, non-federal government clinics, and family clinics compared to the average for all settings.

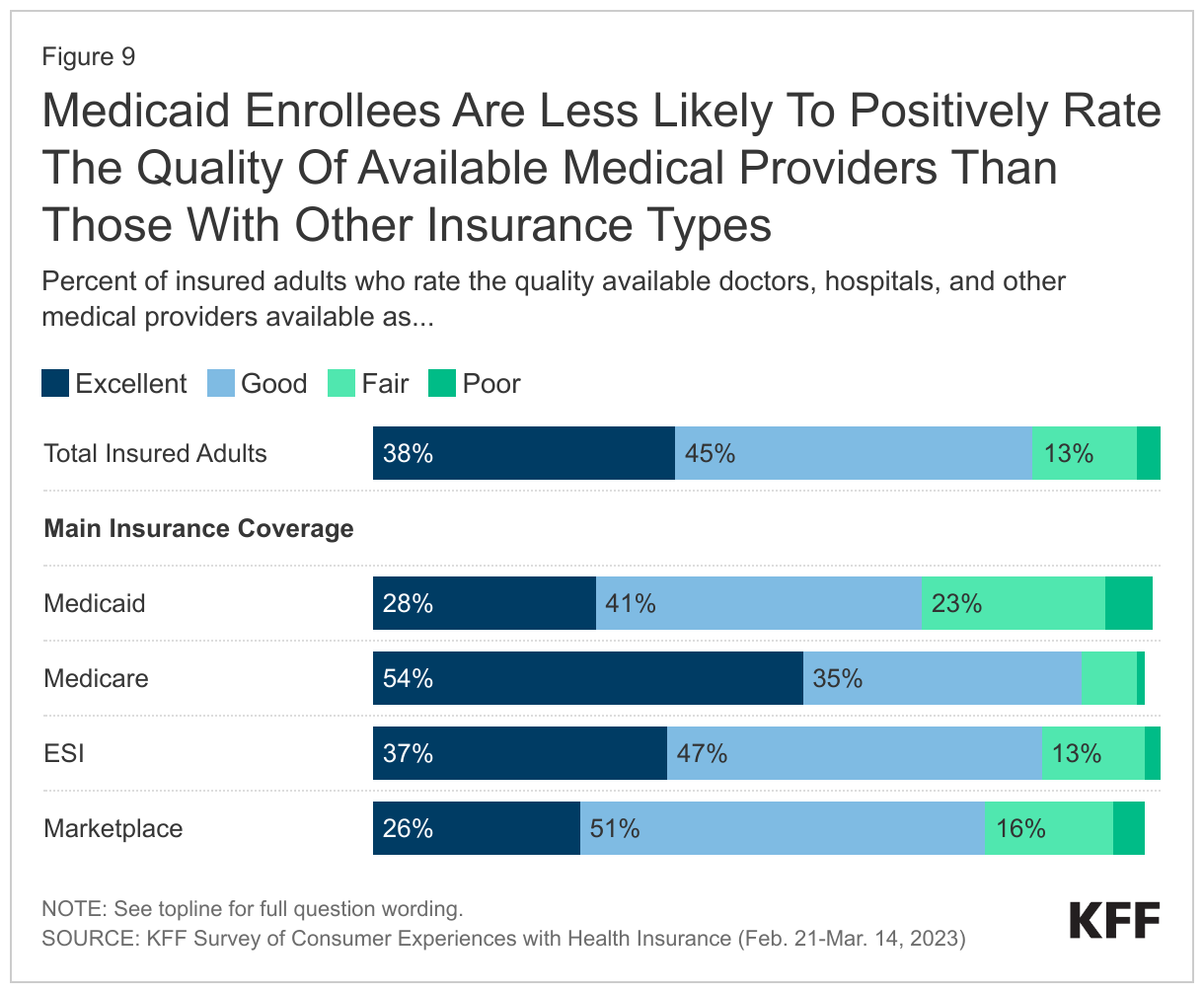

While the majority of Medicaid enrollees rate the quality of available providers positively, Medicaid enrollees are less likely to do so relative to individuals with other insurance types. Overall, more than two in three Medicaid enrollees (69%) report positive perceptions of provider quality. However, adults with Medicare, Marketplace, and ESI all exceed Medicaid enrollees in satisfaction provider quality satisfaction, with 90% of Medicare adults, 78% of Marketplace adults, and 84% of ESI adults rating the quality of providers as “good” or “excellent.”

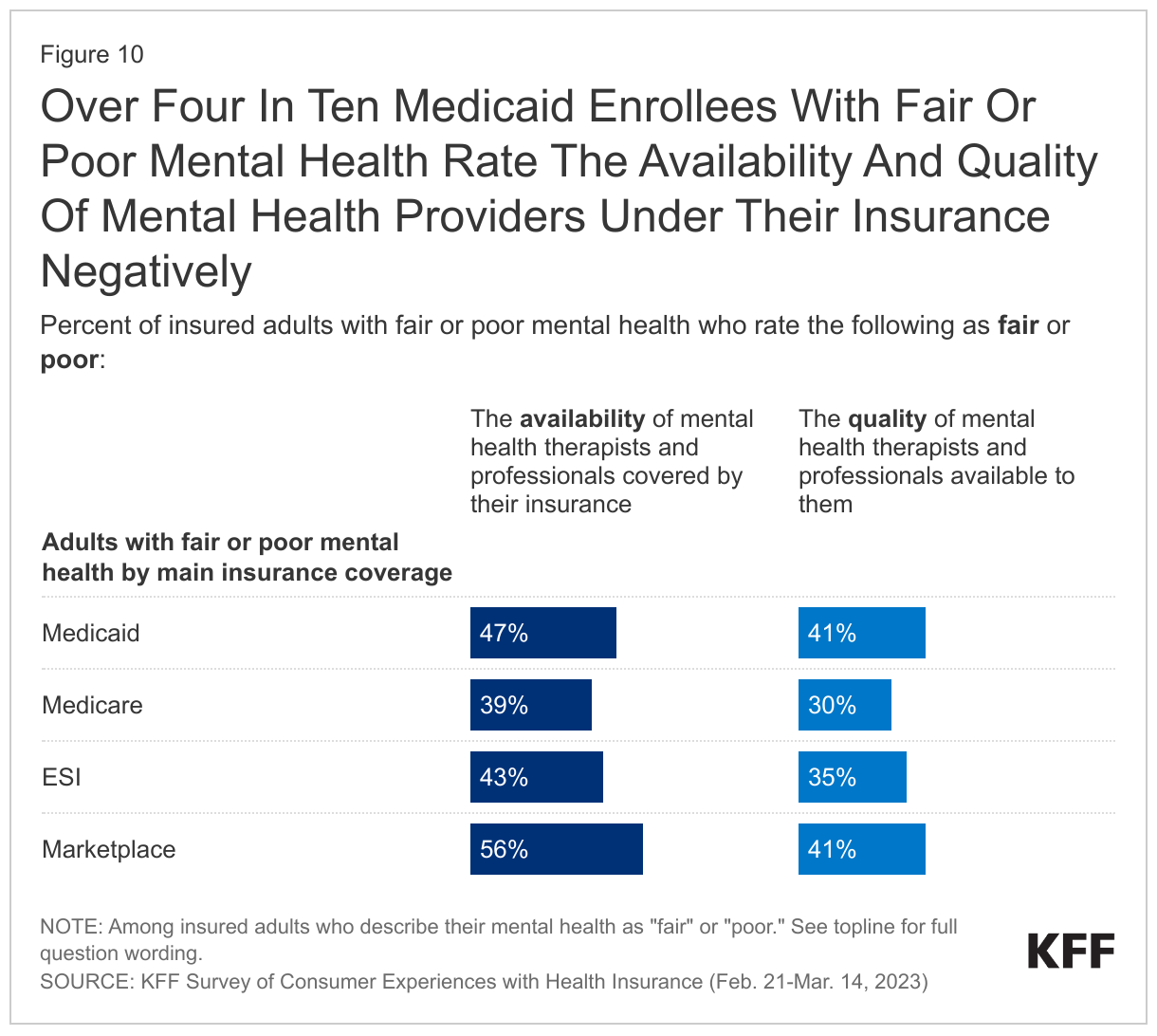

Medicaid enrollees report issues with availability and quality for mental health providers. Adults with Medicaid and Marketplace coverage are more likely than those with ESI or Medicare to negatively rate their insurance when it comes to the availability of mental health providers. Medicaid enrollees more frequently report “fair” or “poor” mental health and may, therefore, have a greater need for mental health providers than adults with other coverage. When looking specifically at adults with Medicaid who describe their own mental health as “fair” or “poor,” notable shares give their plan a negative rating for the availability (47%) and quality (41%) of mental health therapists and professionals.

Where is there significant variation within Medicaid?

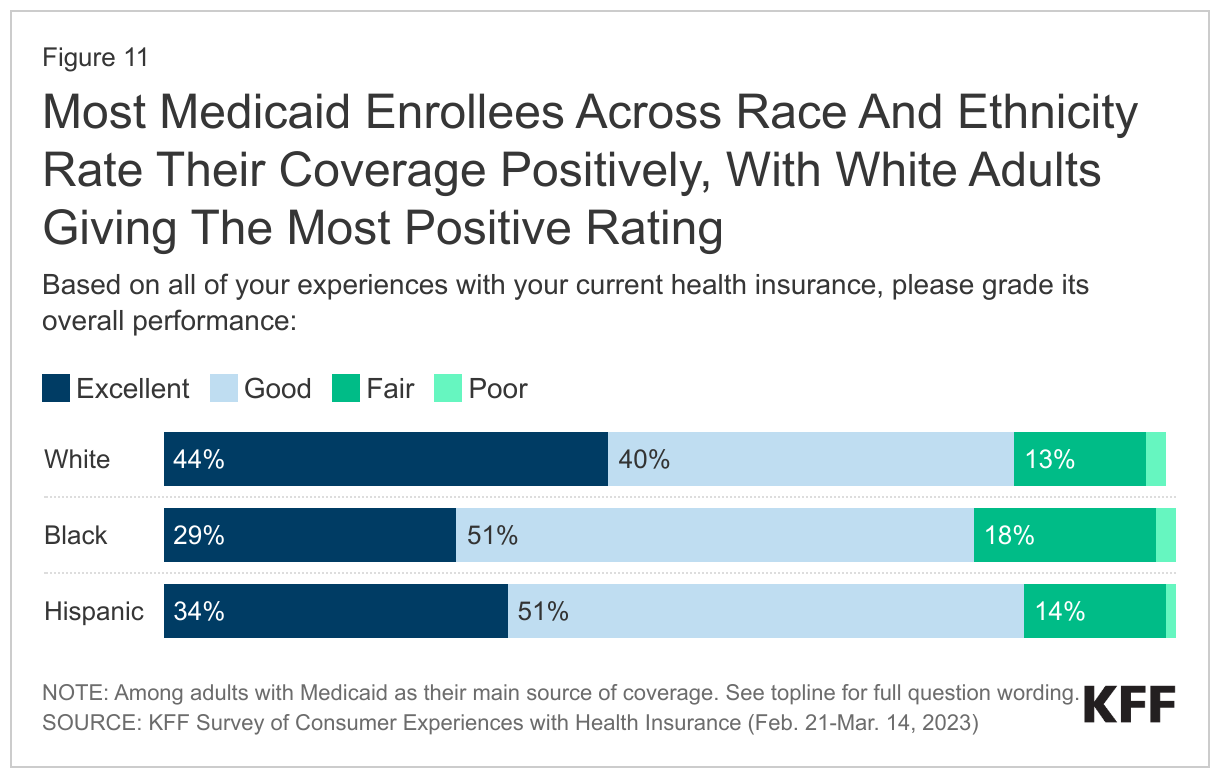

Few enrollees across racial and ethnic groups report their Medicaid coverage as fair or poor, with a large share of White Medicaid enrollees describing their insurance as excellent. Across all racial and ethnic groups, 80% or more of enrollees rate their Medicaid positively. White adults are the most likely to refer to their insurance as “excellent,” with more than 4 in 10 White adults (44%) describing their Medicaid coverage this way compared to 34% of Hispanic adults and 29% of Black adults. Larger shares of White Medicaid enrollees compared to Black or Hispanic enrollees also report the quality of doctors and hospitals available to them as “excellent.” Notably, for problems frequently faced by Medicaid enrollees, such as prior authorization or provider availability, similar shares of Black, White, and Hispanic adults report experiencing these issues.

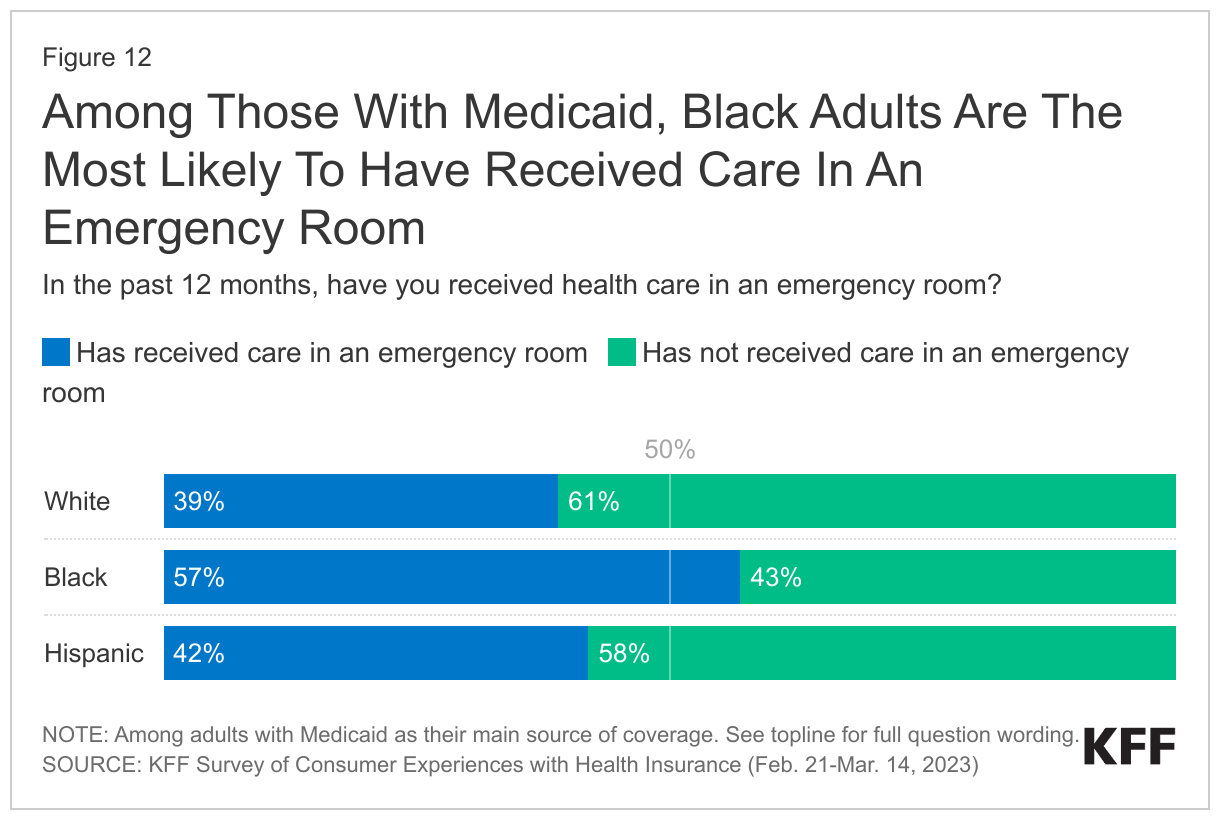

Among those with Medicaid, Black adults are the most likely to have received care in an emergency room at least once in the past year. Nearly six in ten Black Medicaid enrollees report receiving care in an emergency room in the past year, compared to about four in ten White and Hispanic Medicaid enrollees. As noted above, adults with Medicaid are more likely than adults with any other insurance type to report receiving care in the emergency room.

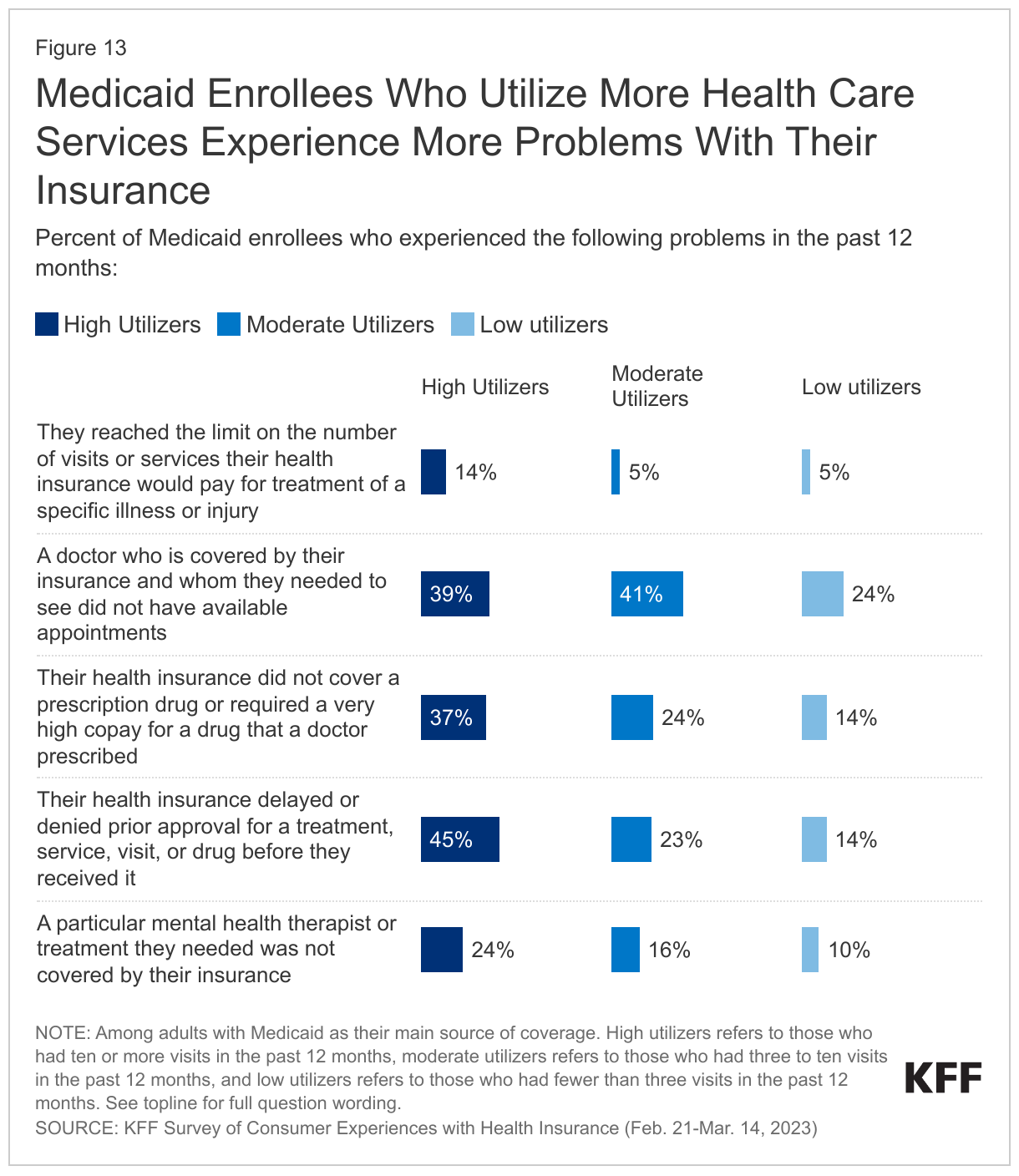

Not surprisingly, Medicaid enrollees who utilize more health care services experience more problems with their insurance. Across all insurance types, adults with fair or poor health status – who have greater need for health care – are more likely to face problems such as lack of appointment availability and high prescription drug costs. In addition to health status, those who have more frequent interactions with their health insurance are also more likely to report problems. When comparing Medicaid enrollees who had over ten visits in the past 12 months to enrollees who had two or fewer visits, high health care utilizers are much more likely to have experienced a problem with their health insurance than lower users. Higher shares of moderate health care utilizers (those who had seen a provider between three to ten times in the past 12 months) also tended to face problems with their insurance compared to low utilizers. These high and moderate health care utilizers are more likely to report that a doctor they needed to see did not have available appointments, that a mental health therapist, treatment, or prescription was not covered by their insurance, or that their health insurance did not cover or required a very high copay for a prescription drug. Compared to both moderate and low health care utilizers, high utilizers are more likely to report running into prior authorization issues or reaching the limit on the number of visits or services their insurance would pay for a specific illness or injury.

What to Watch

Recent federal proposed rules attempt to address some issues related to availability of providers and access in Medicaid. On April 27, 2023, the Biden Administration released two notices of proposed rulemaking (NPRMs) to help ensure access to quality health care in Medicaid and the Children’s Health Insurance Program (CHIP). The proposed rules include changes to Medical Care Advisory Committees (to allow for more meaningful engagement from Medicaid enrollees), increase transparency for fee-for-service (FFS) and managed care payments, establish national maximum appointment wait time standards for managed care enrollees, and require state monitoring related to access and network adequacy for managed care plans. Currently, federal law requires Medicaid managed care plans to assure that they have capacity to serve expected enrollment in their service area and maintain a sufficient number, mix, and geographic distribution of providers but there are no uniform standards.

Centers for Medicare and Medicaid Services (CMS) proposed rules, Office of the Inspector General (OIG) recommendations, and state legislation could help to address Medicaid prior authorization issues. Prior authorization is a tool long used to control spending and promote cost effective care, but it can also delay care and result in negative clinical outcomes. A recent review by the U.S. Department of Health and Human Services OIG found that in 2019, Medicaid MCOs had an overall prior authorization denial rate of 12.5% – more than double the Medicare Advantage rate. The OIG recommended stronger state monitoring of denials and a requirement for automatic external medical reviews following MCO appeal denials. In December of 2022, the Biden Administration also proposed prior authorization regulations that would apply to Medicaid and other coverage types, but these rules focus mostly on streamlining processes, improving transparency, and reducing approval wait times. While CMS has not yet finalized these proposed prior authorization rules, a final rule may be published soon.

A range of state regulatory actions have also focused on prior authorization practices. New state laws or updates to existing ones affecting prior authorization for Medicaid enrollees have passed in states such as Georgia, Illinois, and Washington state. State requirements include: new reporting on prior authorization standards and claims denials, shortened time frames for decision-making, allowing certain providers to bypass prior authorization to limit delays (e.g. “gold carding”), and restrictions on the use of clinical criteria developed by insurers to make coverage decisions. California has also recently began relaxing prior authorization requirements for diabetes care for Medi-Cal members.

Conclusion

Overall, most adults rate their insurance coverage favorably but the complex nature of health care and differences in insurance design and out-of-pocket costs lead to variations in beneficiary experiences. Compared to adults with private coverage or Medicare, Medicaid enrollees are more likely to face problems with provider availability and prior authorization and are at greater risk of experiencing negative outcomes as a result of problems with their insurance, including a decline in their health. However, because of federal rules that limit out-of-pocket costs, Medicaid enrollees are less likely to report cost-related problems or difficulty understanding what they would owe out of pocket. Pending federal rules addressing provider availability for Medicaid managed care enrollees may improve access to care for these enrollees. Proposed regulations from the Biden administration may streamline prior authorization processes and impact wait times but fall short of OIG recommendations for stronger state monitoring of denials and required automatic external medical reviews.

This work was supported in part by the Robert Wood Johnson Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

| Methodology |

| This KFF Survey of Consumer Experiences with Health Insurance was designed and analyzed by researchers at KFF. The survey was designed to reach a representative sample of insured adults in the U.S. The survey was conducted February 21–March 14, 2023, online and by telephone among a nationally representative sample of 3,605 U.S. adults who have employer sponsored insurance plans (978), Medicaid (815), Medicare (885), Marketplace plans (880), or a Military plan (47). The margin of sampling error is plus or minus 2 percentage points for the full sample and plus or minus 5 percentage points for adults with Medicaid as their main source of health coverage.

The sample includes 2,595 insured adults reached through the SSRS Opinion Panel either online or over the phone (n=75 in Spanish). Another 504 respondents were reached online through the Ipsos Knowledge Panel. Another 289 (n=10 in Spanish) interviews were conducted from a random digit dial (RDD) of prepaid cell phone numbers (n=190) and landline telephone numbers (n=99). An additional 217 respondents were reached by calling back respondents who said they were insured in previous KFF probability-based polls. Respondents were weighted separately to match each group’s demographics using data from the 2021 American Community Survey (ACS). Weighting parameters included gender, age, education, race/ethnicity, and region. For full details on the survey methodology, see the Methodology tab of the KFF Survey of Consumer Experiences with Health Insurance. |