10 Things to Know About Medicaid Managed Care

Managed care is the dominant delivery system for people enrolled in Medicaid. The latest national Medicaid managed care enrollment data (from 2022) show 75% of Medicaid beneficiaries were enrolled in comprehensive managed care organizations (MCOs). While managed care is the dominant Medicaid delivery system, states decide which populations and services to include in managed care arrangements, which leads to considerable variation across states. Additionally, while state requirements for Medicaid managed care plans can be tracked, plans have flexibility in certain areas, including in setting provider payment rates, and plans may choose to offer additional benefits beyond those required by the state.

Early in 2025, there are many factors at play that could have implications for Medicaid managed care plans and the people they serve. At the state level, states and plans have faced considerable rate setting uncertainty after millions of people were disenrolled during the unwinding of the pandemic-era Medicaid continuous enrollment provision. Some firms report that current capitation rates do not align with higher member risk and utilization patterns. Many states have sought federal approval to adjust rates to address these changes amid shifts and uncertainty in state fiscal conditions. At the federal level, talks in Congress about cutting federal Medicaid spending could have implications for coverage as well as plans and providers. Finally, major Medicaid regulations designed to promote quality of care and advance access to care for Medicaid enrollees finalized under the Biden administration could be repealed by Congress or delayed or rewritten by the Trump administration. In this context, this brief describes 10 themes related to the use of comprehensive, risk-based managed care in the Medicaid program.

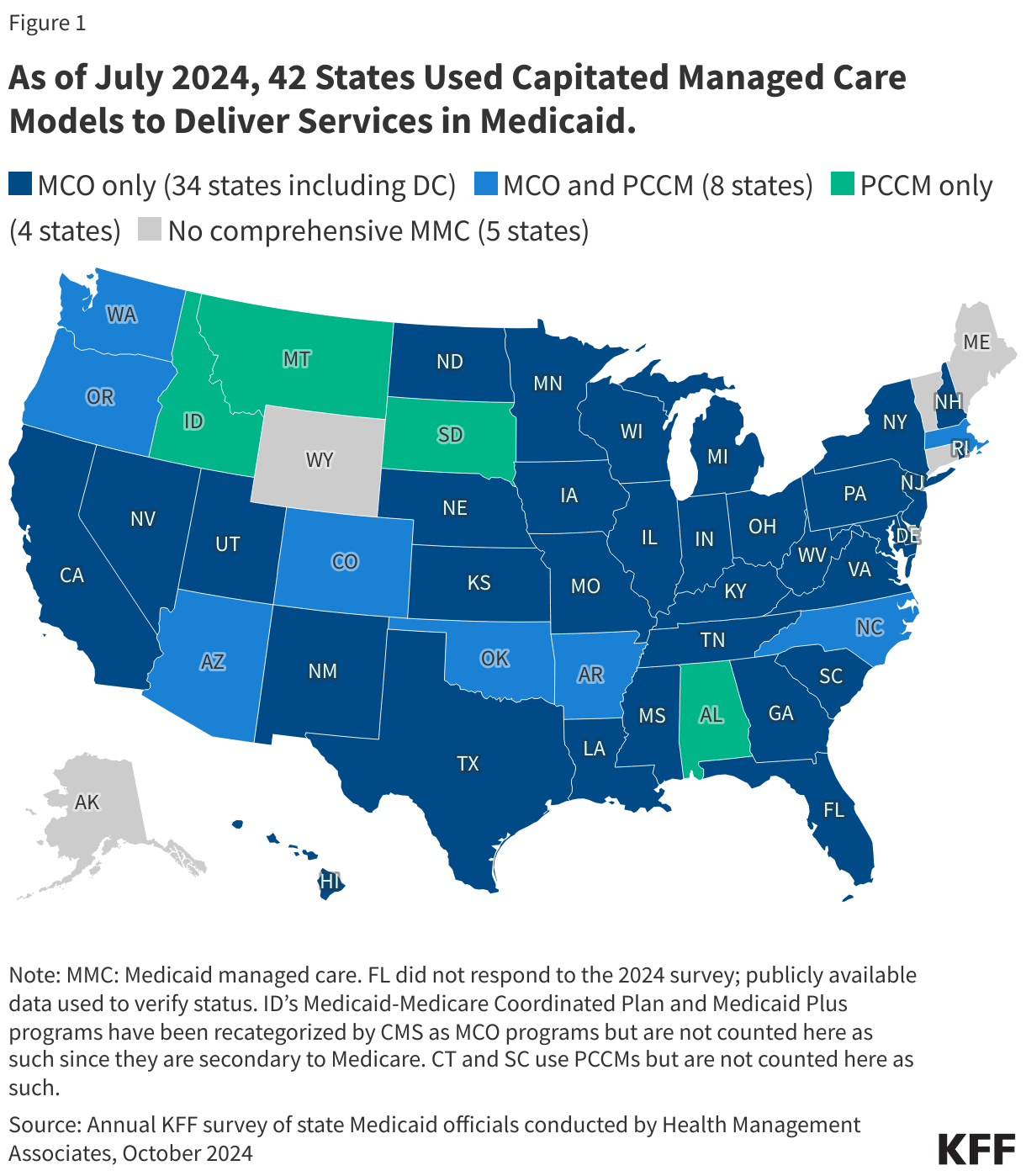

1. Today, capitated managed care is the dominant way in which states deliver services to Medicaid enrollees.

States design and administer their own Medicaid programs within federal rules. States determine how they will deliver and pay for care for Medicaid beneficiaries. Nearly all states have some form of managed care in place – comprehensive risk-based managed care and/or primary care case management (PCCM) programs.1,2 As of July 2024, 42 states (including DC) contract with comprehensive, risk-based managed care plans to provide care to at least some of their Medicaid beneficiaries (Figure 1). Oklahoma is the latest state to be included in this count, having implemented capitated, comprehensive Medicaid managed care (for most children and adults) on April 1, 2024. Medicaid MCOs provide comprehensive acute care (i.e., most physician and hospital services) and, in some cases, long-term care to Medicaid beneficiaries and are paid a set per member per month payment for these services. For more than three decades, states have increased their reliance on managed care delivery systems with the aim of improving access to certain services, enhancing care coordination and management, and making future costs more predictable. While the shift to MCOs has increased budget predictability for states, the evidence about the impact of managed care on access to care and costs is both limited and mixed.3,4,5

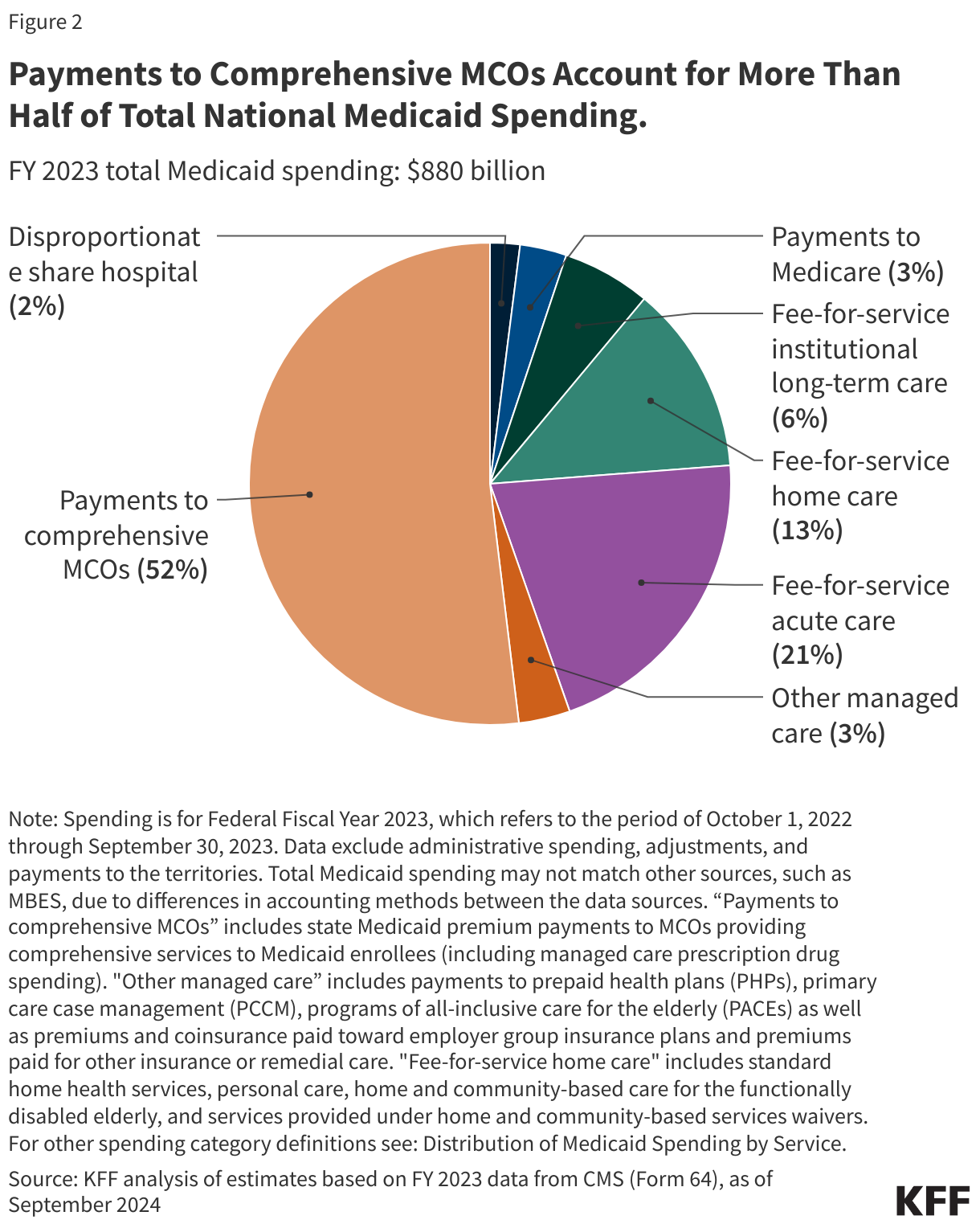

2. In FY 2023, payments to comprehensive risk-based MCOs accounted for over half of Medicaid spending.

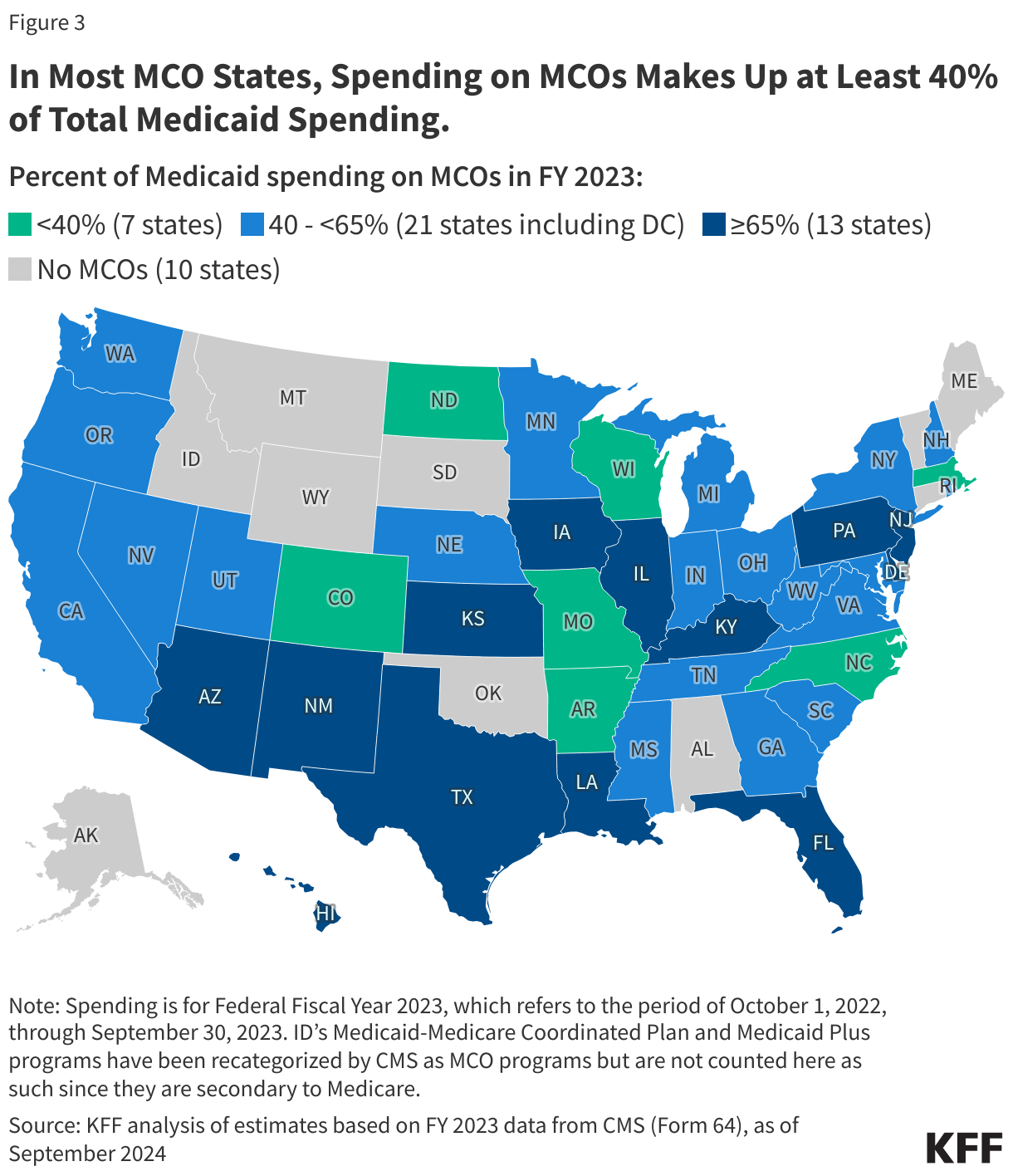

In FY 2023, state and federal spending on Medicaid services totaled over $880 billion. Payments made to MCOs accounted for about 52% of total Medicaid spending (Figure 2), unchanged from the previous fiscal year. The share of Medicaid spending on MCOs varies by state, but over three-quarters of MCO states directed at least 40% of total Medicaid dollars to payments to MCOs (Figure 3). State-to-state variation reflects many factors, including the proportion of the state Medicaid population enrolled in MCOs, the health profile of the Medicaid population, whether high-risk/high-cost beneficiaries (e.g., people with disabilities, dual eligible beneficiaries) are included in or excluded from MCO enrollment, and whether long-term care services are included in MCO contracts. As states expand Medicaid managed care to include higher-need, higher-cost beneficiaries, expensive long-term care, and adults newly eligible for Medicaid under the ACA, the share of Medicaid dollars going to MCOs could continue to increase.

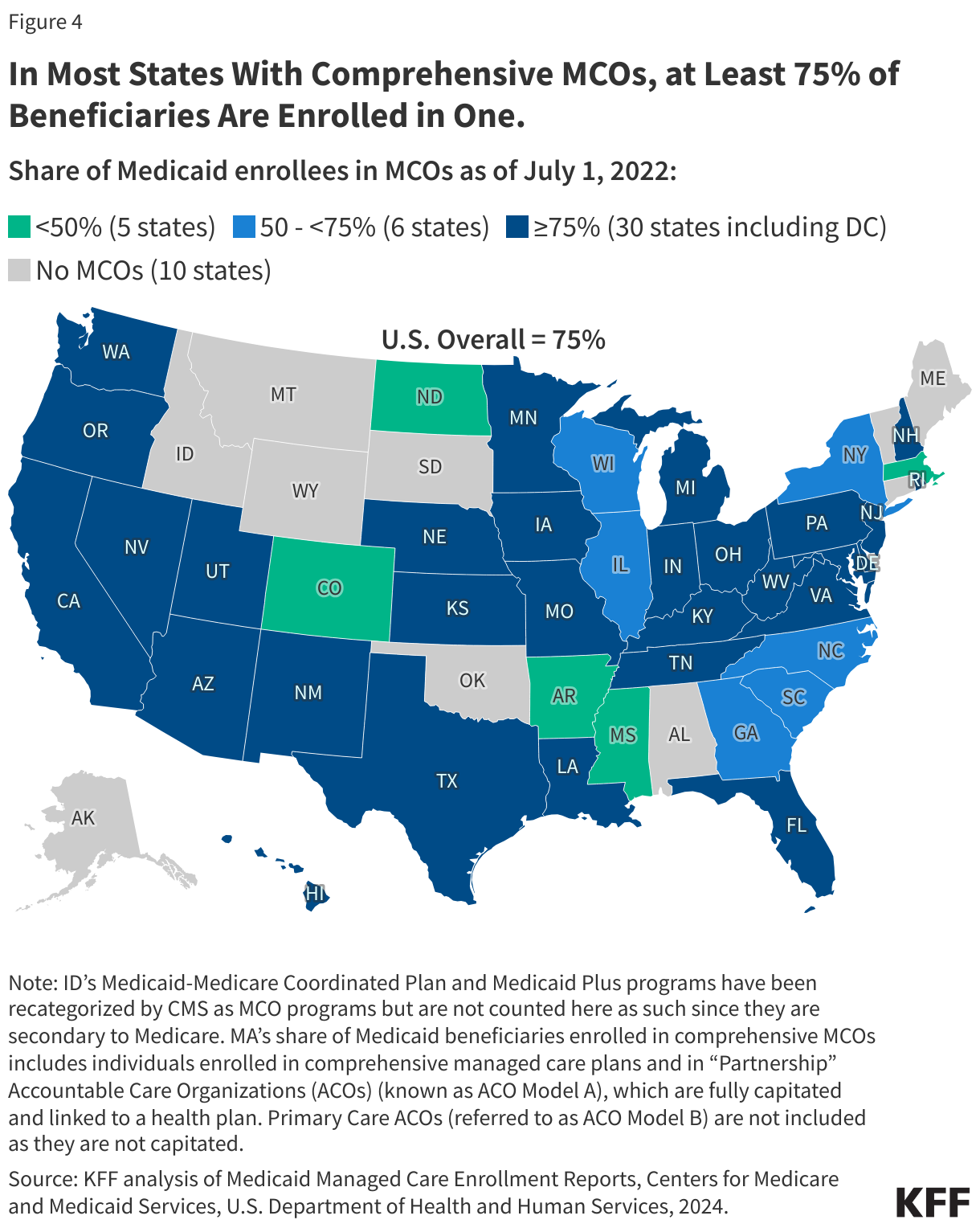

3. Three-quarters (75%) of all Medicaid beneficiaries received their care through comprehensive risk-based MCOs.

As of July 2022, nearly 72 million Medicaid enrollees received their care through risk-based MCOs. Thirty MCO states covered at least 75% of Medicaid beneficiaries in MCOs (Figure 4).

Although 2022 data are the most current national data available, enrollment in Medicaid overall grew substantially during the COVID public health emergency when states paused disenrollments, resulting in growth in MCO enrollment as well. At the start of the “unwinding” period, in April 2023, Medicaid enrollment (overall) peaked at 94.5 million, an increase of 23 million or 32% from before the pandemic. Despite millions of disenrollments during the unwinding, nationally, nearly 8 million more people were enrolled in Medicaid/CHIP in October 2024 than in February 2020 (pre-pandemic).

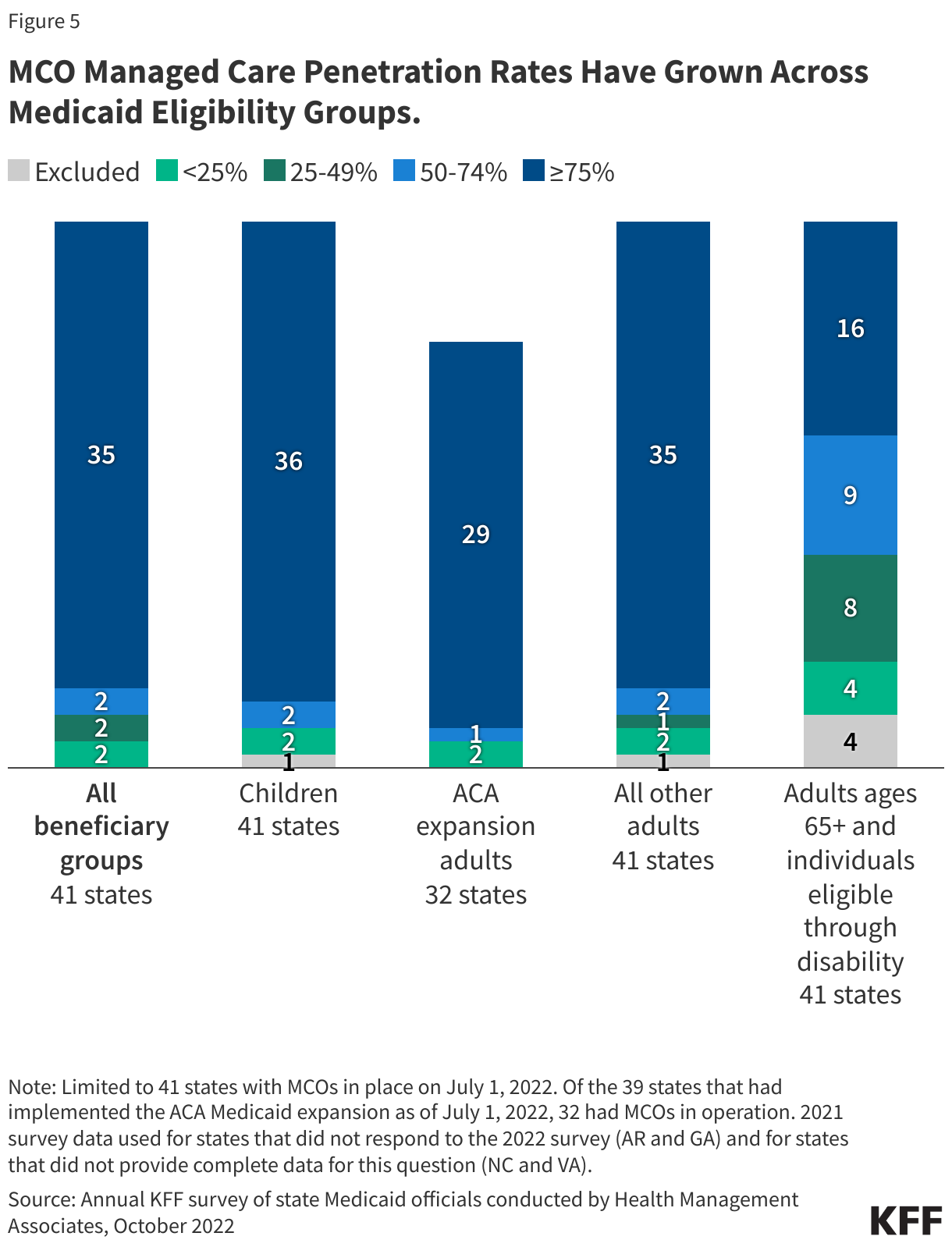

4. Children and adults are groups most likely to be enrolled in MCOs; however, states are increasingly including enrollees with complex needs in MCOs.

As of July 2022, 36 MCO states reported covering 75% or more of all children through MCOs (Figure 5). Of the 39 states that had implemented the ACA Medicaid expansion as of July 2022, 32 states were using MCOs to cover newly eligible adults and most covered more than 75% of beneficiaries in this group through MCOs. Thirty-five MCO states reported covering 75% or more of low-income adults in pre-ACA expansion groups (e.g., parents, pregnant women) through MCOs. Fewer MCO states reported covering 75% or more adults ages 65+ and people eligible through disability. Although this group is still less likely to be enrolled in MCOs than children and adults, over time, states have been moving to include adults ages 65+ and people eligible through disability in MCOs.

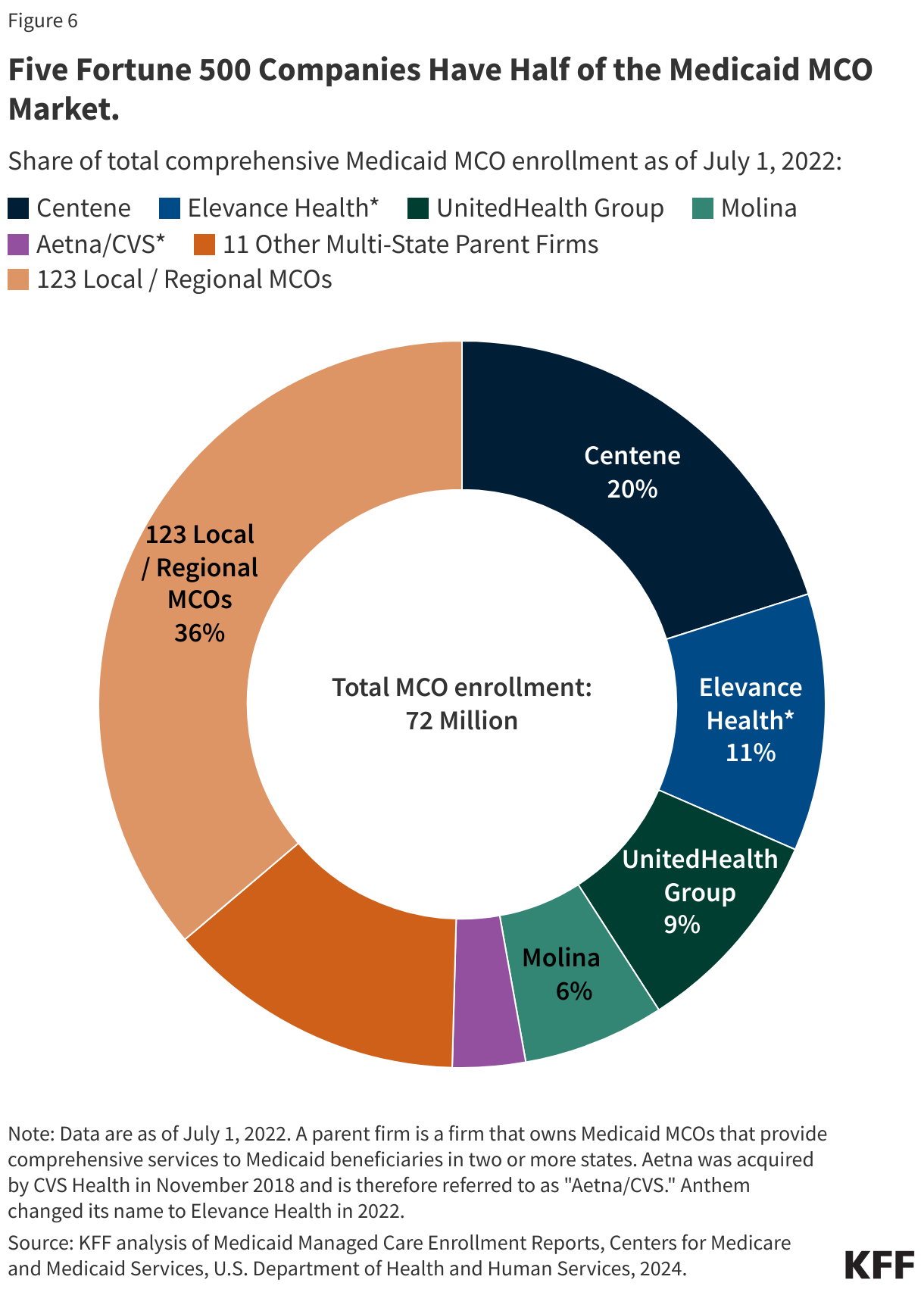

5. Five publicly traded firms account for half of MCO enrollment.

States contracted with a total of 282 Medicaid MCOs as of July 2022. MCOs represent a mix of private for-profit, private non-profit, and government plans. As of July 2022, a total of 16 firms operated Medicaid MCOs in two or more states (called “parent” firms), and these firms accounted for over 63% of enrollment in 2022 (Figure 6). Of the 16 parent firms, six are publicly traded, for-profit firms while the remaining ten are non-profit companies. Five firms – Centene, UnitedHealth Group, Elevance (formerly Anthem), Molina, and Aetna/CVS – account for 50% of all Medicaid MCO enrollment (Figure 6). All five are publicly traded companies ranked in the Fortune 500, and four are ranked in the top 100.

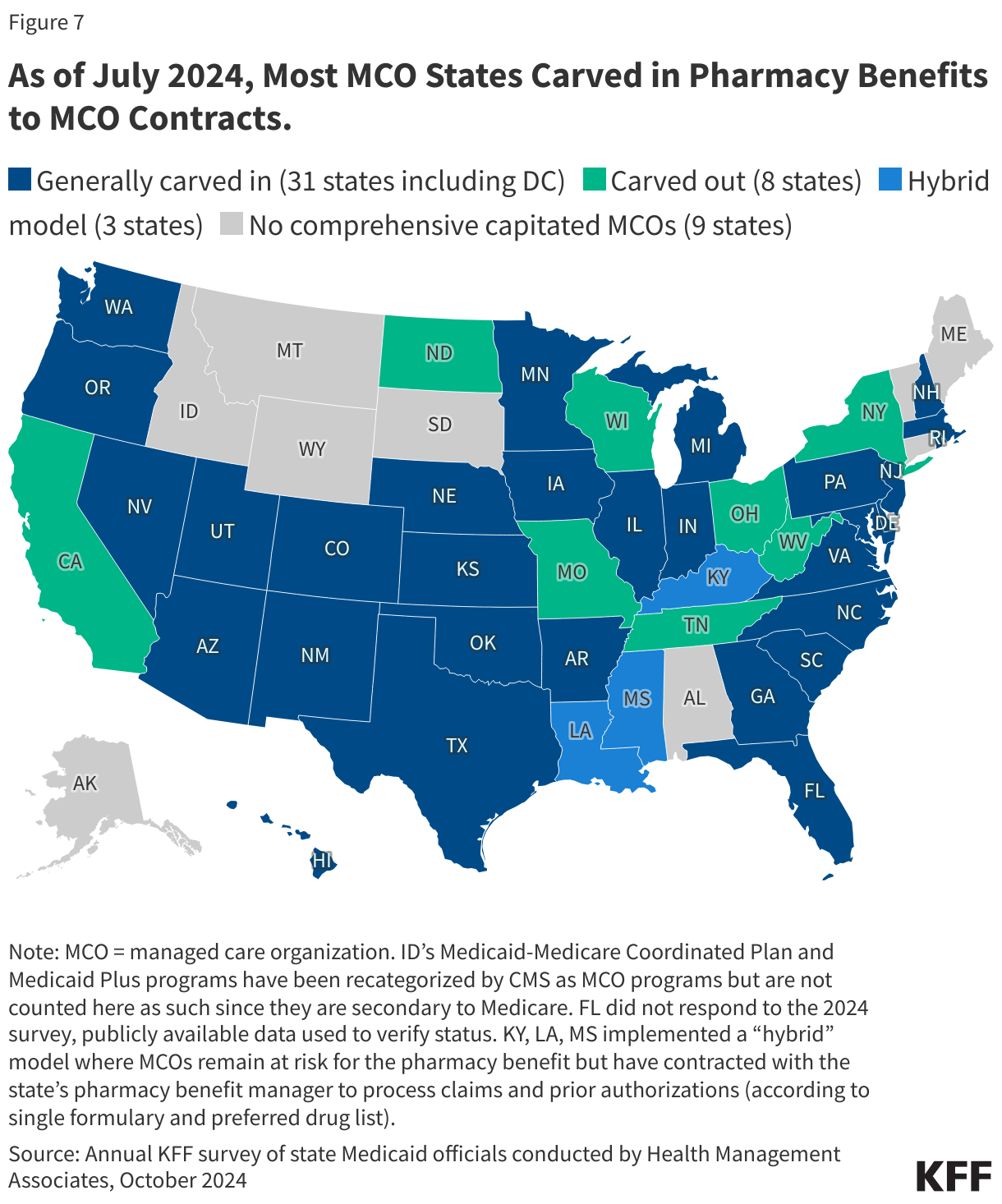

6. States make decisions about which services to carve in and out of MCO contracts.

Although MCOs provide comprehensive services to beneficiaries, states may carve specific services out of MCO contracts to fee-for-service systems or limited benefit plans. Services frequently carved out include behavioral health, pharmacy, dental, and long-term care services. However, there has been significant movement across states to carve these services into MCO contracts. While the vast majority of states that contract with MCOs report that the pharmacy benefit is carved into managed care (31 of 42), eight states report that pharmacy benefits are carved out of MCO contracts as of July 2024 (Figure 7). An additional three states (Kentucky, Louisiana, and Mississippi) now contract with a single PBM for the managed care population instead of implementing a traditional carve-out of pharmacy from managed care. (Under this “hybrid” model, MCOs remain at risk for the pharmacy benefit but must contract with the state’s pharmacy benefit manager to process pharmacy claims and pharmacy prior authorizations according to a single formulary and preferred drug list.)

7. Each year, states develop MCO capitation rates that must be actuarially sound and may include risk mitigation strategies.

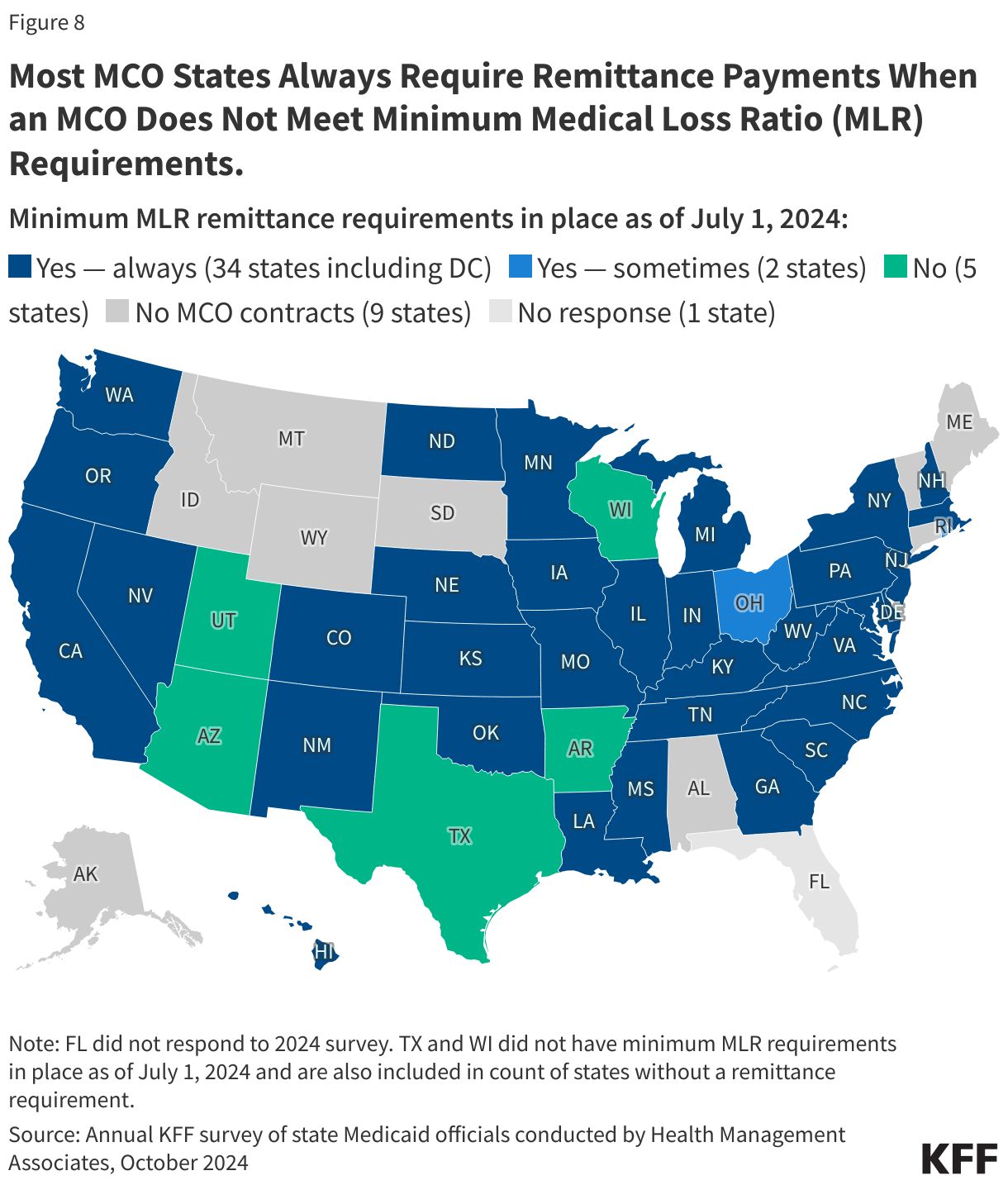

States pay Medicaid managed care organizations a set per member per month payment for the Medicaid services specified in their contracts. While plans set rates in the commercial and Medicare Advantage markets, Medicaid managed care rates are developed by states and their actuaries and reviewed and approved by CMS. Under federal law, payments to Medicaid MCOs must be actuarially sound. Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Unlike fee-for-service (FFS), capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit. Plan rates are usually set for a 12-month rating period. States may use a variety of mechanisms to adjust plan risk, incentivize plan performance, and ensure payments are not too high or too low, including risk sharing arrangements, risk and acuity adjustments, medical loss ratios (MLRs, which reflect the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement), or incentive and withhold arrangements.

To limit the amount that plans can spend on administration and keep as profit, states are required to develop capitation rates for Medicaid to achieve an MLR of at least 85% in the rate year; 6 however, there is no federal requirement for Medicaid plans to pay remittances to the state if they fail to meet the MLR standard.7 As of July 2024, 34 MCO states reported they always require remittance payments when an MCO does not meet state minimum MLR requirements, while two states indicated they sometimes require MCOs to pay remittances (Figure 8).

8. In 2024, CMS finalized rules to strengthen access standards, but the future of the rules is uncertain.

The Biden administration finalized major Medicaid regulations designed to promote quality of care and advance access to care for Medicaid enrollees. The 2024 Managed Care rule addresses Medicaid managed care access, financing, and quality, including strengthening standards for timely access to care (e.g., through the establishment of national maximum wait time standards for certain “routine” appointments) and states’ monitoring and enforcement efforts. These rules are complex and are set to be implemented over several years. However, Congress may seek to overturn these rules, or the Trump administration could delay implementation or issue new regulations that would undo them. During the first Trump administration, CMS took action to change Medicaid managed care rules, including relaxing rules around network adequacy and beneficiary protections.

States are generally prohibited from contractually directing how a managed care plan pays its providers.8 Subject to CMS approval, however, states may implement certain “state directed payments” (SDPs) that require managed care plans to adopt minimum or maximum provider payment fee schedules, provide uniform dollar or percentage increases to providers (above base payment rates), or implement value-based provider (VBP) payment arrangements.9 In creating state directed payments (in 2016), CMS aimed to help states ensure access to adequate provider networks and to increase use of VBP arrangements. Many states that contract with MCOs use SDPs to make uniform rate increases that are like FFS supplemental payments. State directed payments must meet federal requirements (e.g., must be tied to utilization and delivery of services, be distributed equally to specified providers, and not be conditioned on participation in intergovernmental transfer (IGT) agreements).10 The managed care rules finalized in 2024 permit states to pay hospitals and nursing facilities at the average commercial payment rate (ACR) when using directed payments (higher than the Medicare payment ceiling used for other Medicaid FFS supplemental payments). The 2024 rules also tightened SDP requirements to improve oversight, evaluation, and transparency (e.g., states will be required to report provider level directed payment data) and to ensure state directed payments are tied to actual utilization. Recent reports indicate state directed payments have been a major driver of Medicaid expenditure growth in recent years, and CBO Medicaid projections for 2025-2034 attribute further increases in SDPs (partially tied to the changes in rule) as a factor increasing spending.

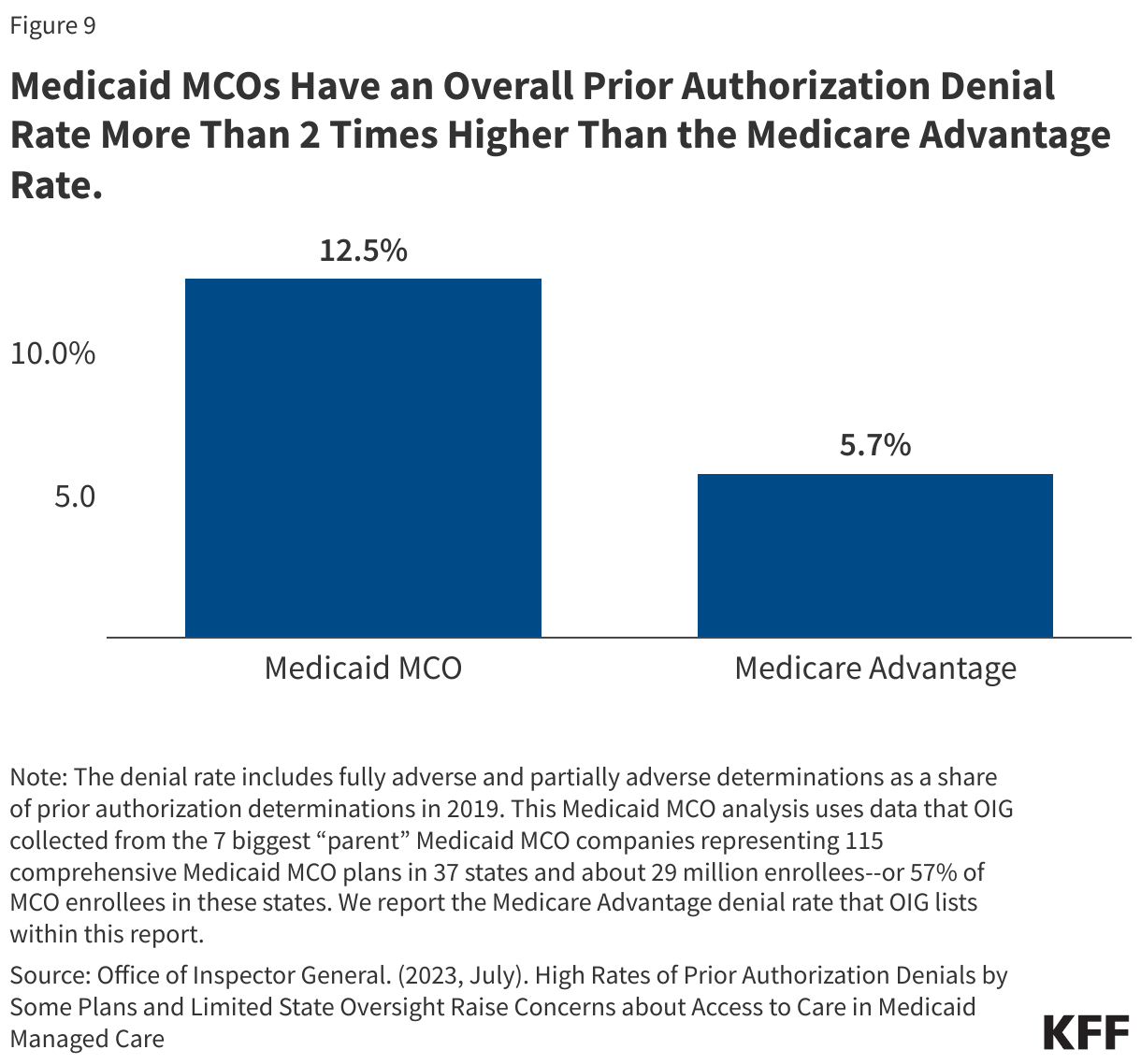

In 2024, CMS also finalized a rule focused on improving the prior authorization process including reducing approval wait times and improving transparency. A 2023 KFF survey of consumer experiences with health insurance found that about one in five Medicaid enrollees say they’ve had issues with prior authorization—higher than for most other types of insurance. A July 2023 OIG report found that Medicaid MCOs had an overall prior authorization denial rate of 12.5%–more than 2 times higher than the Medicare Advantage rate (Figure 9), raising concerns about prior authorization and access in Medicaid managed care. OIG recommendations (to CMS) include strengthening state monitoring of denials. Recent MACPAC analysis of denials and appeals in Medicaid managed care resulted in the inclusion of seven recommendations in the March 2024 Report to Congress focused on improving the appeals process and enhancing monitoring and oversight of MCOs.

9. States link financial incentives to quality measures and use contract requirements to advance priorities, including addressing social determinants of health.

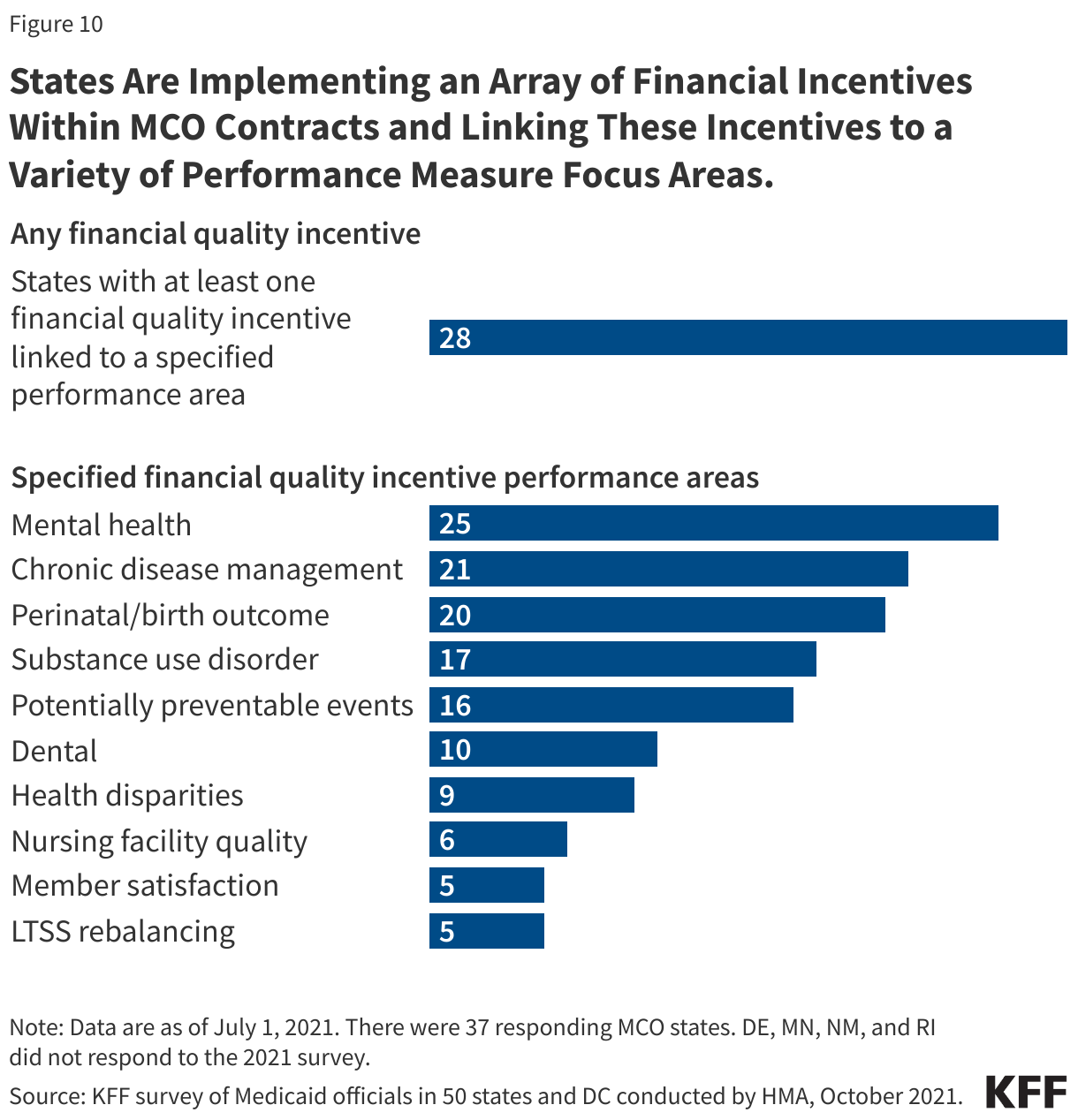

States incorporate quality metrics into the ongoing monitoring of their programs, including linking financial incentives like performance bonuses or penalties, capitation withholds, or value-based state directed payments to quality measures. Over three quarters of MCO states reported using at least one financial incentive to promote quality of care as of July 2021 (Figure 10). Financial incentive performance areas most frequently targeted by MCO states include behavioral health, chronic disease management, and perinatal/birth outcomes. Despite activity in this area, detailed performance information at the plan-level frequently has not been made publicly available by state Medicaid agencies, limiting transparency and the ability of Medicaid beneficiaries (and other stakeholders) to assess how plans are performing on key indicators related to access, quality, etc.

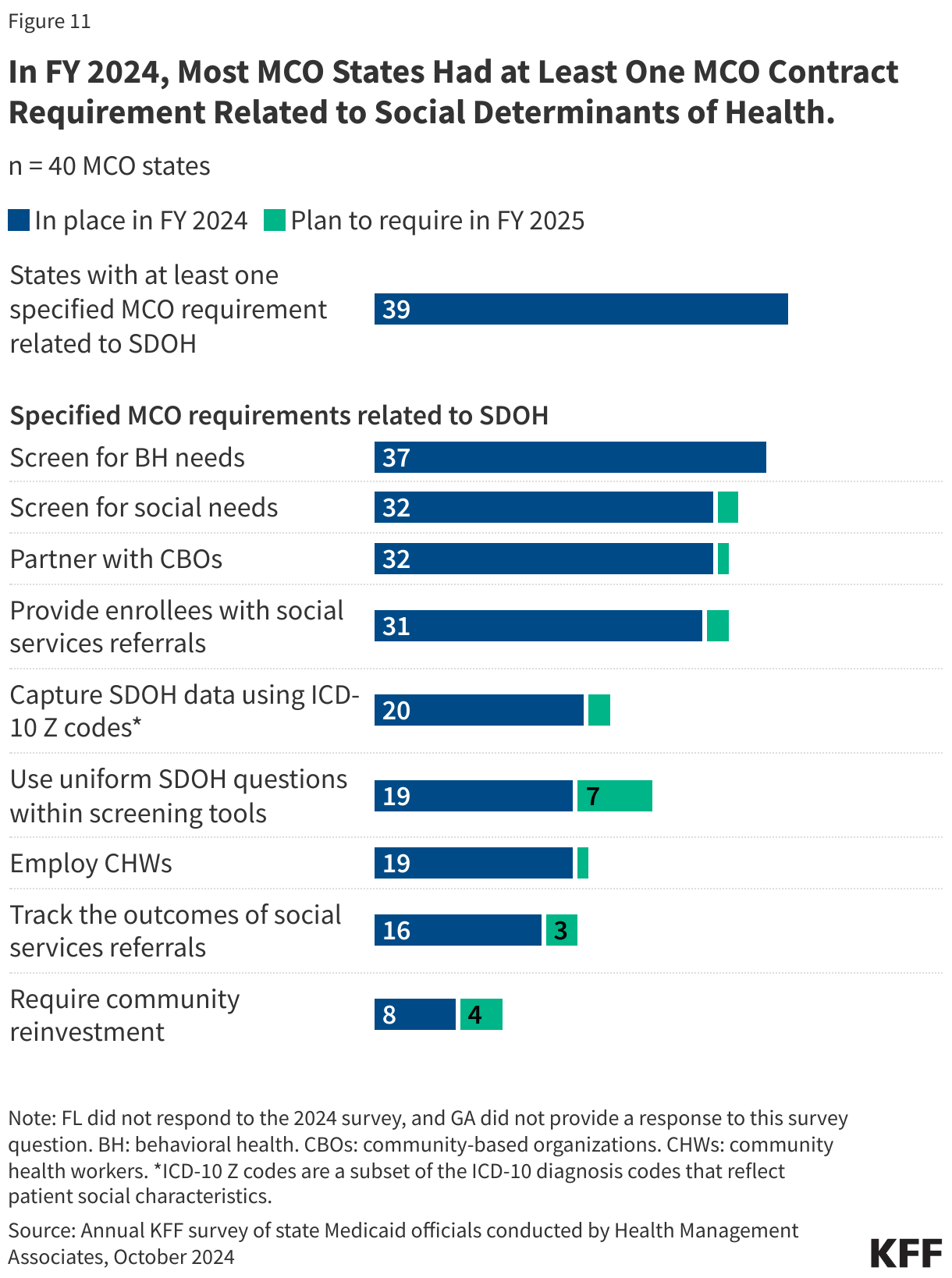

In FY 2024, most MCO states reported leveraging Medicaid MCO contracts to promote at least one specified strategy to address social determinants of health (Figure 11). States can also leverage managed care contracts to help reduce health disparities.

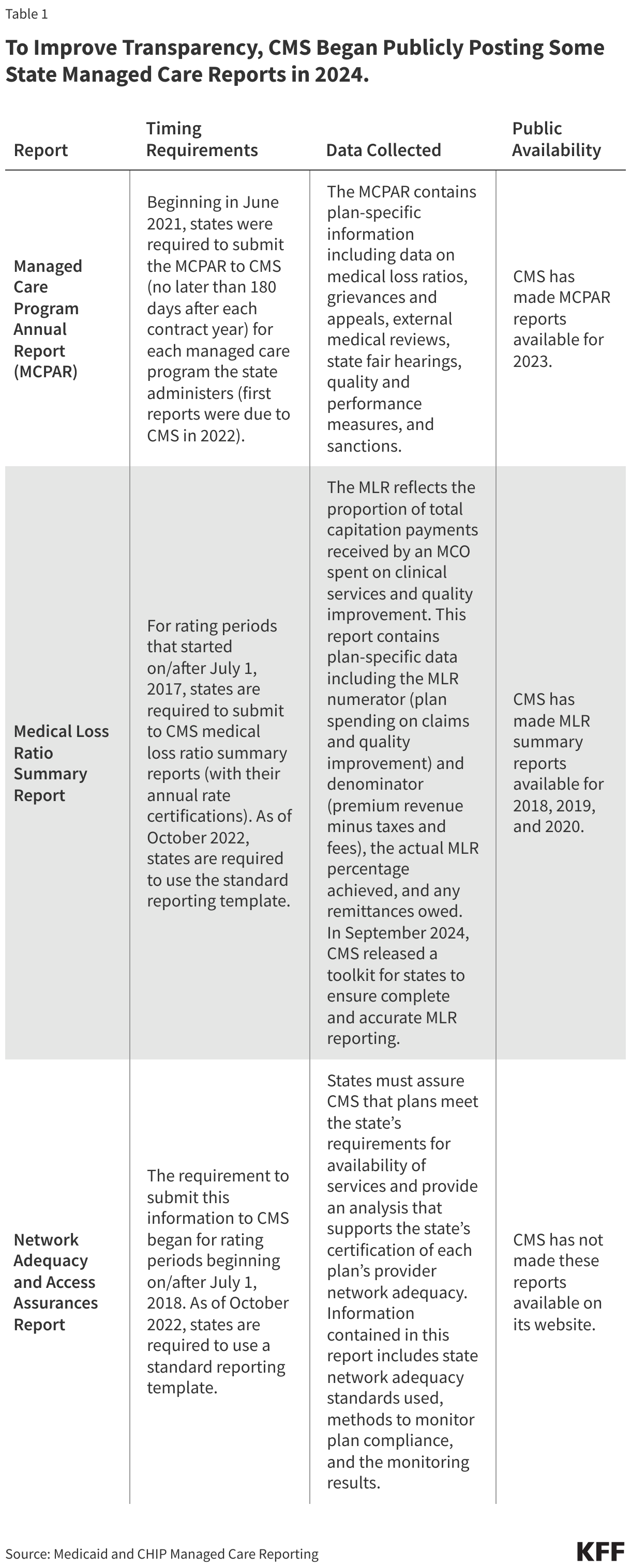

10. CMS has taken steps to improve managed care program monitoring and transparency.

The 2016 Medicaid managed care final rule created new managed care reporting requirements for states. CMS, under the Biden administration, developed standard reporting templates (Table 1) and a variety of toolkits and released a series of informational bulletins (2021, 2022, 2023, 2024) to help states improve their monitoring and oversight of managed care programs. Transparency has the potential to promote accountability. To improve transparency, CMS began publicly posting the Managed Care Program Annual Report (MCPAR) and the MLR Summary Reports on Medicaid.gov in 2024. Managed care rules finalized in 2024 include provisions aimed at further strengthening managed care transparency and monitoring, though the fate of these rules remains uncertain.

Posting data relating to the performance of individual MCOs may allow for comparison within and across states. However, limitations and challenges may exist including posting lags and incomplete data (e.g., GAO found 6 states had not submitted required MCPARs for 2022, OIG found MLR reports prepared by plans were missing required data). (States are required to post the MCPAR and Network Adequacy and Access Assurances Report on their websites but some states may not yet be in compliance with these requirements.) It is unclear whether the Trump administration will continue efforts to strengthen managed care oversight and transparency.

Endnotes

PCCM is a managed fee-for-service (FFS) based system in which beneficiaries are enrolled with a primary care provider who is paid a small monthly fee to provide case management services in addition to primary care.

While MCOs are the predominant form of Medicaid managed care, millions of other beneficiaries receive at least some Medicaid services, such as behavioral health or dental care, through limited-benefit risk-based plans, known as prepaid inpatient health plans (PIHPs) and prepaid ambulatory health plans (PAHPs).

Sparer M. 2012. Medicaid managed care: costs, access, and quality of care. Res. Synth. Rep. 23, Robert Wood Johnson Found., Princeton, NJ

Daniel Franco Montoya, Puneet Kaur Chehal, and E. Kathleen Adams, “Medicaid Managed Care’s Effects on Costs, Access, and Quality: An Update,” Annual Review of Public Health 41:1 (2020):537-549

Medicaid and CHIP Payment and Access Commission (MACPAC), “Managed care’s effect on outcomes,” (Washington, DC: MACPAC, 2018), https://www.macpac.gov/subtopic/managed-cares-effect-on-outcomes/

The 85% minimum MLR is the same standard that applies to Medicare Advantage and private large group plans.

The 2024 Consolidated Appropriations Act included a financial incentive to encourage certain states to collect remittances from Medicaid MCOs that do not meet minimum MLR requirements.

42 CFR Sections 438.6 and 438.60.

Permissible under 42 CFR Section 438.6(c).

42 CFR §438.6(c)