Data sources used for Key Facts About Hospitals are listed below. Some figures pull from other sources, including prior KFF analyses and KFF State Health Facts, which include additional information about the data and methodology. Numbers have been rounded.

American Hospital Association (AHA) Annual Survey. Data from an annual survey of all hospitals in the United States and its associated areas. Non-federal psychiatric hospitals were defined to include psychiatric hospitals as well as hospitals that identified their hospital type as “substance use disorder” or “intellectual disabilities.”

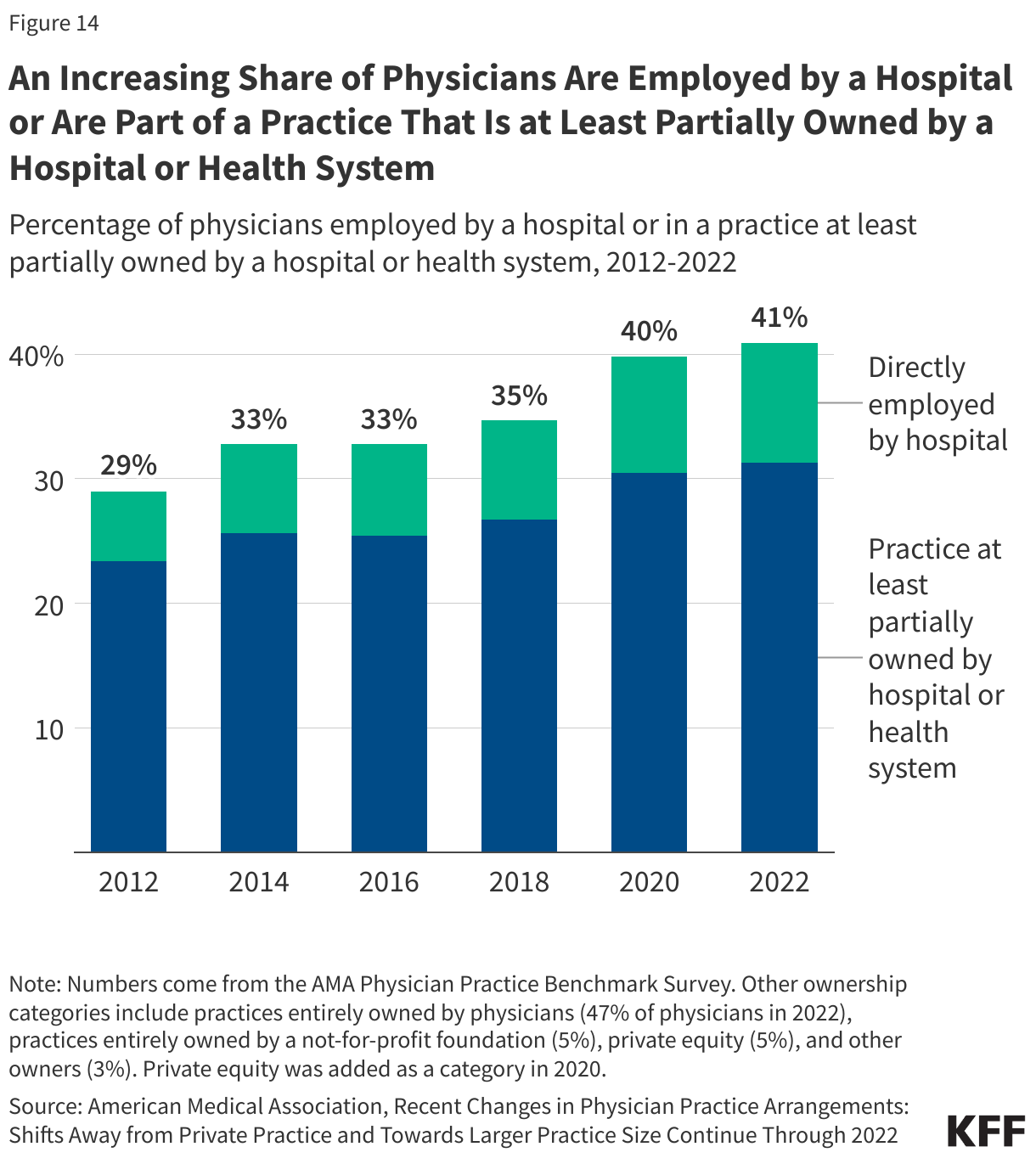

American Medical Association (AMA) Physician Practice Benchmark Survey. As described by the AMA, the Physician Practice Benchmark Survey is a nationally representative survey of “post-residency physicians who provide at least 20 hours of patient care per week, are not employed by the federal government, and practice in one of the 50 states or [DC].”

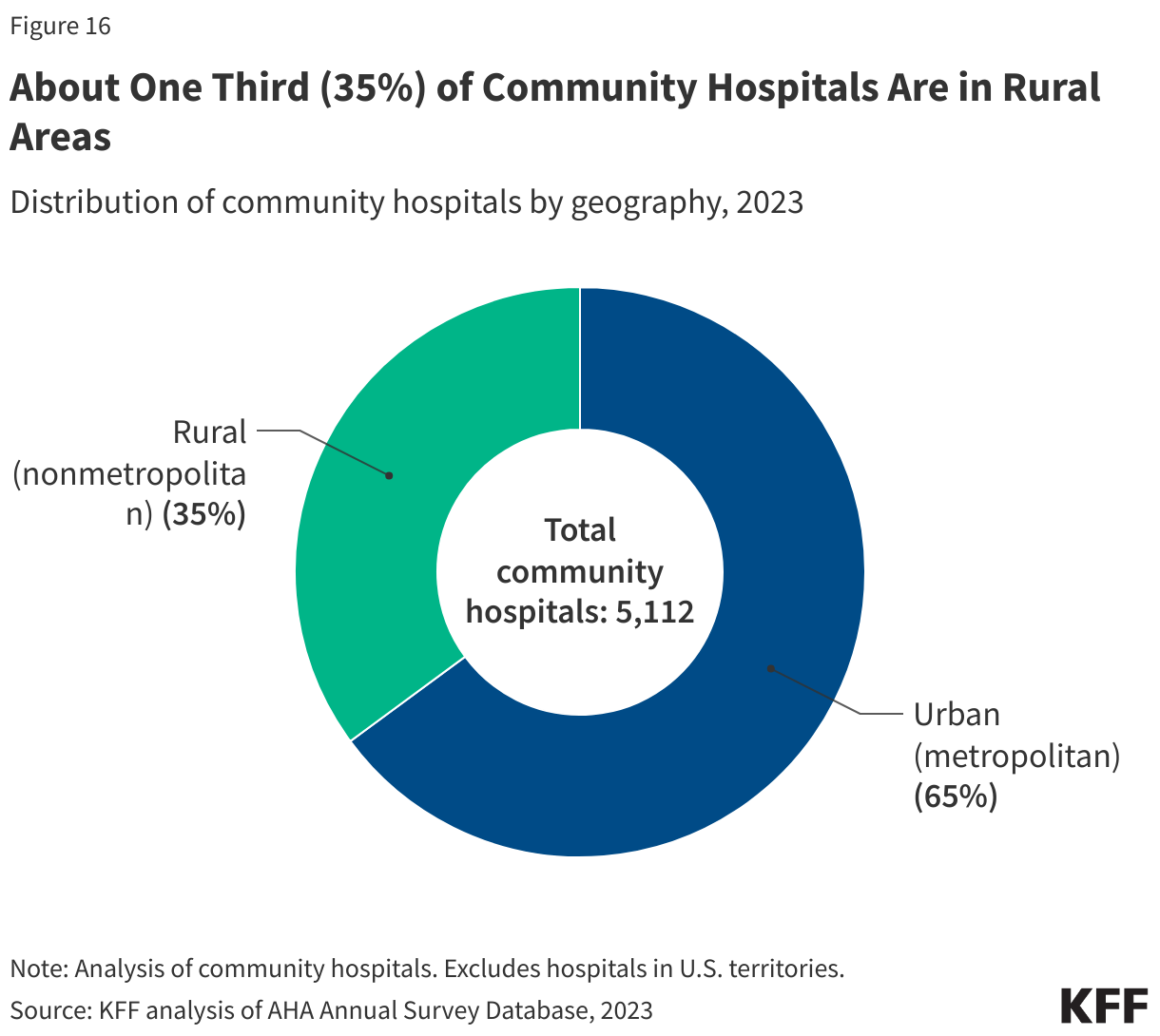

Census Bureau delineation files. The Census Bureau delineation files map counties and county equivalents to metropolitan areas, micropolitan areas, and other regions. These files were used to group hospitals into metropolitan, micropolitan, and other areas. A metropolitan area is a county or group of counties that contains at least one urban area with a population of 50,000 or more people. A micropolitan area is a county or group of counties that contains at least one urban area with a population of at least 10,000 but less than 50,000. Urban and rural regions were defined as metropolitan and nonmetropolitan areas, respectively.

Census Bureau population estimates. We relied on annual population estimates for the 50 states and DC as of July 1 of a given year from the Census Bureau’s Population Estimates Program.

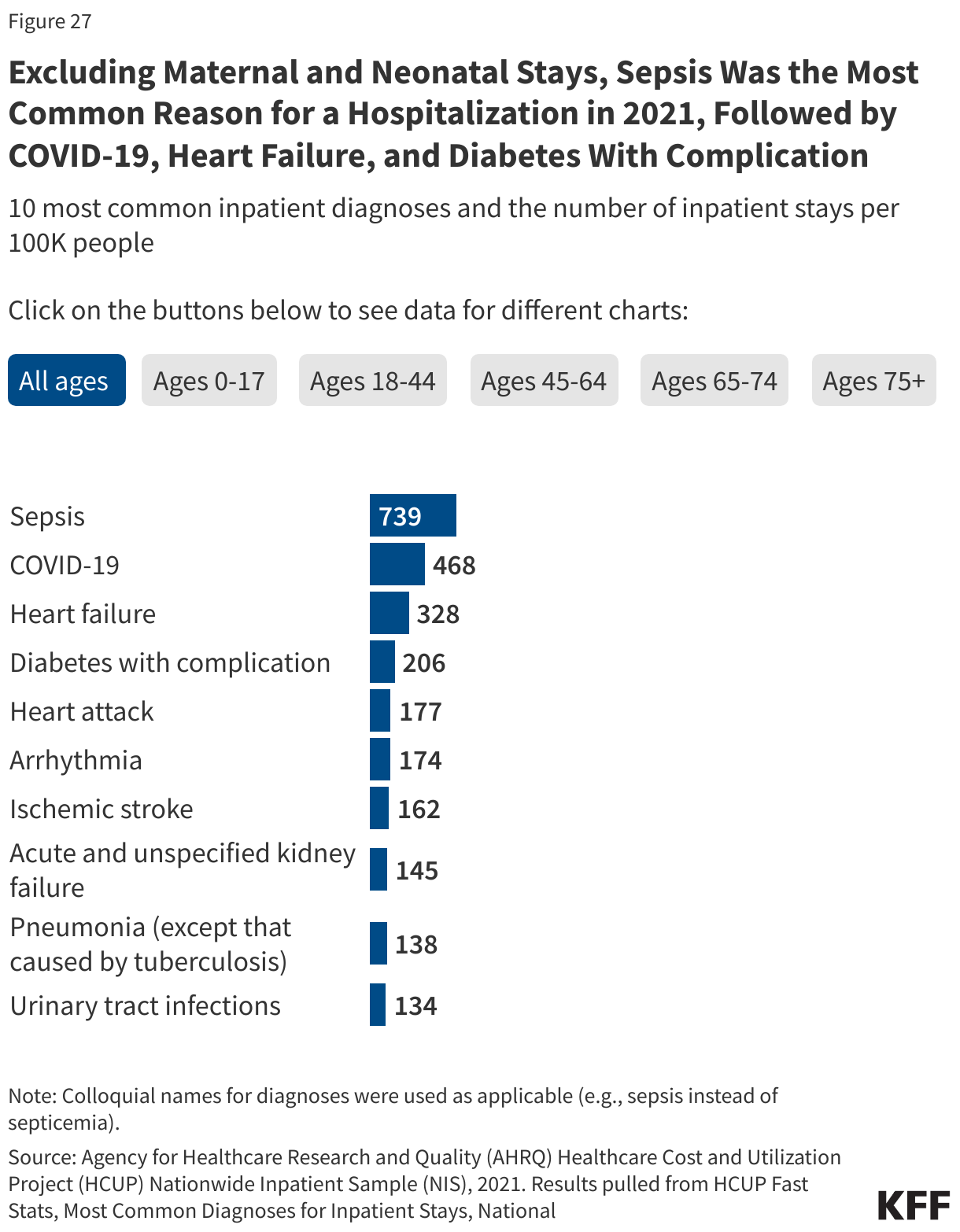

Healthcare Cost and Utilization Project (HCUP) National Inpatient Sample (NIS). The NIS is a sample that includes about 20% of all inpatient discharges from U.S. community hospitals (aside from rehabilitation and long-term care hospitals). It is nationally representative of non-federal short-term hospitals in the U.S. and is sponsored by the Agency for Healthcare Research and Quality. Primary diagnoses are grouped into clinical categories based on Clinical Classifications Software Refined (CCSR). The categories used for rankings are mutually exclusive; when a diagnosis falls under multiple clinical categories, the stay is assigned to a single category based on hierarchical guidelines.

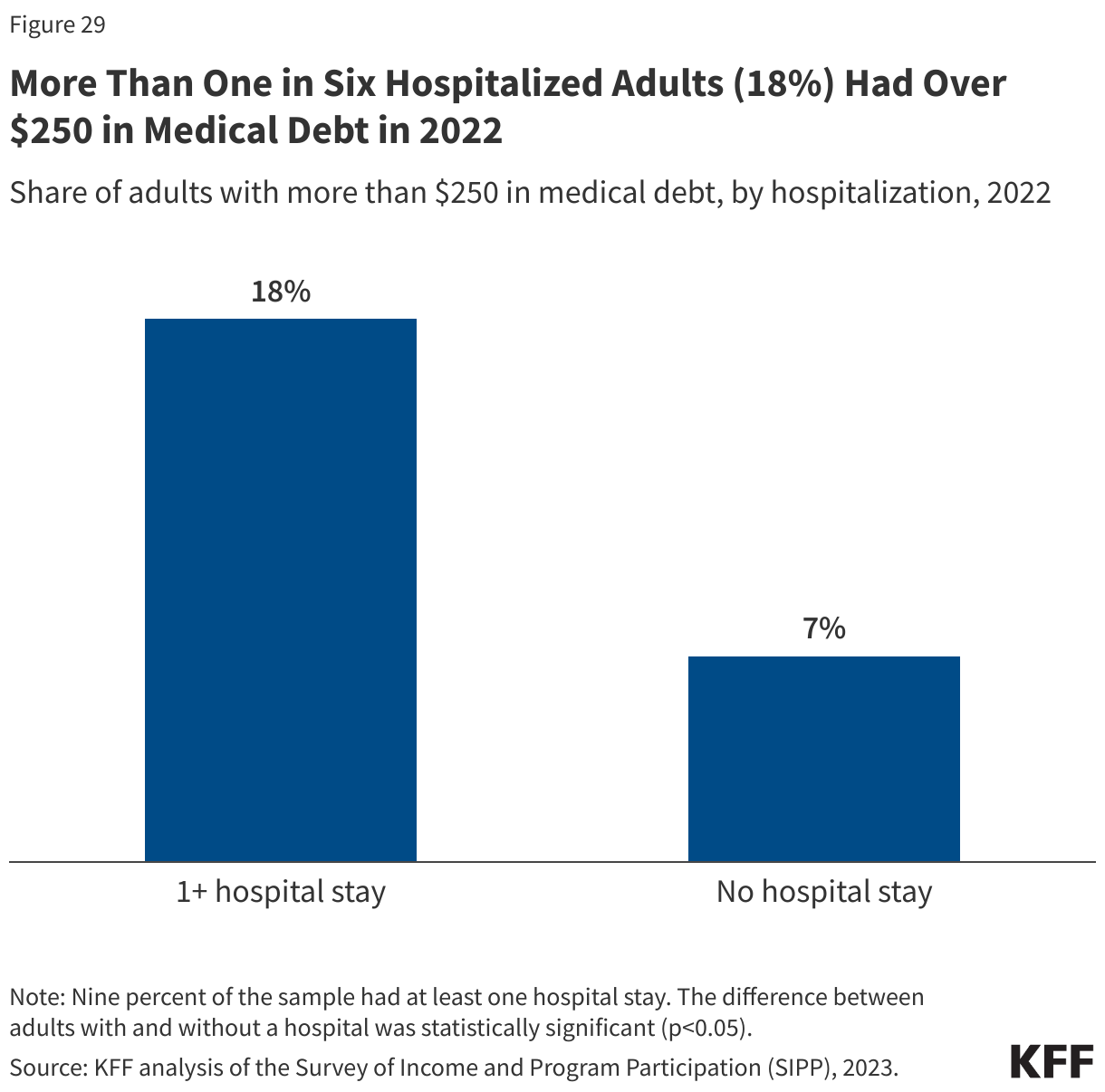

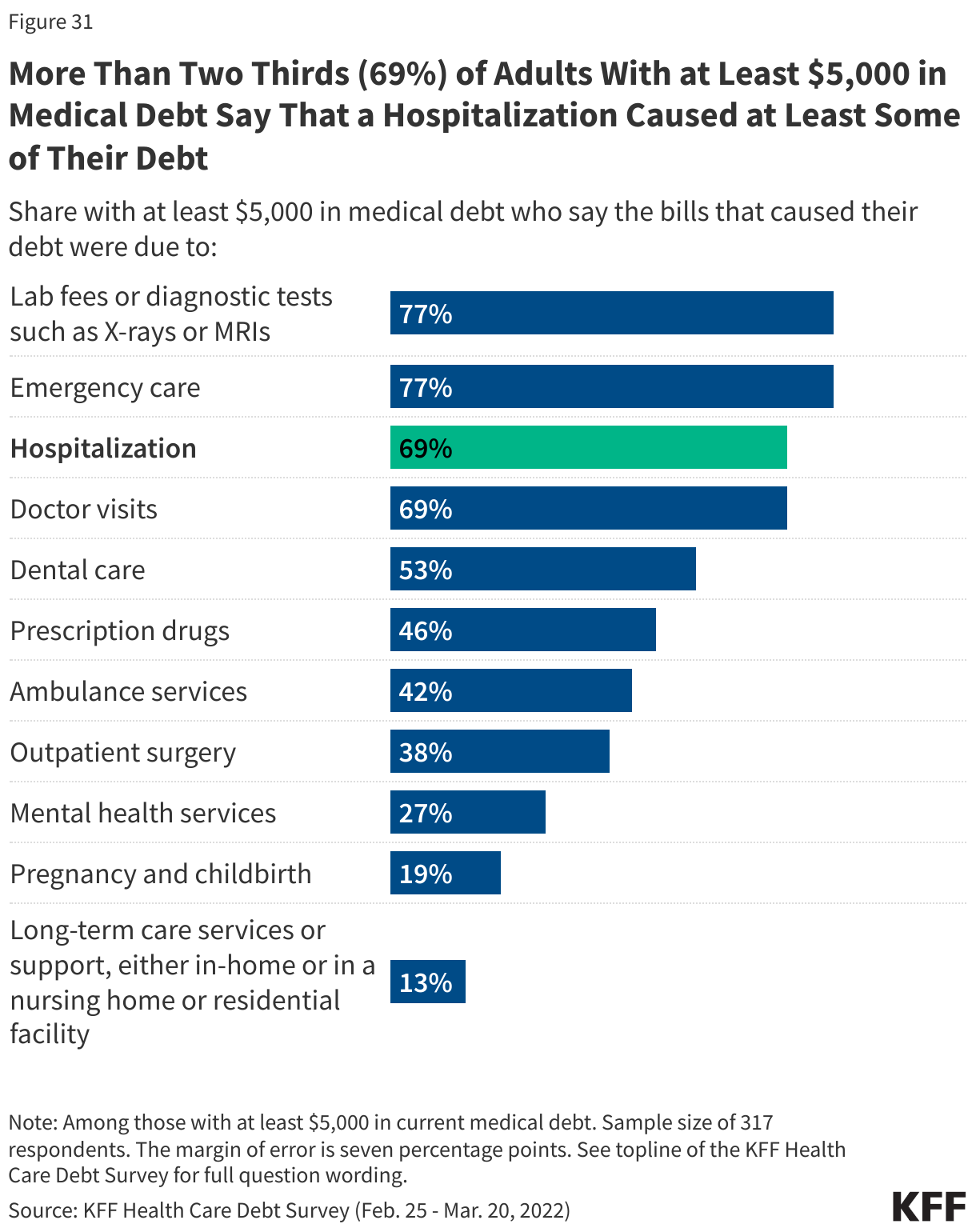

KFF Health Care Debt Survey. The KFF Health Care Debt Survey is a nationally representative survey of U.S. adults that was conducted from February 25 through March 20, 2022.

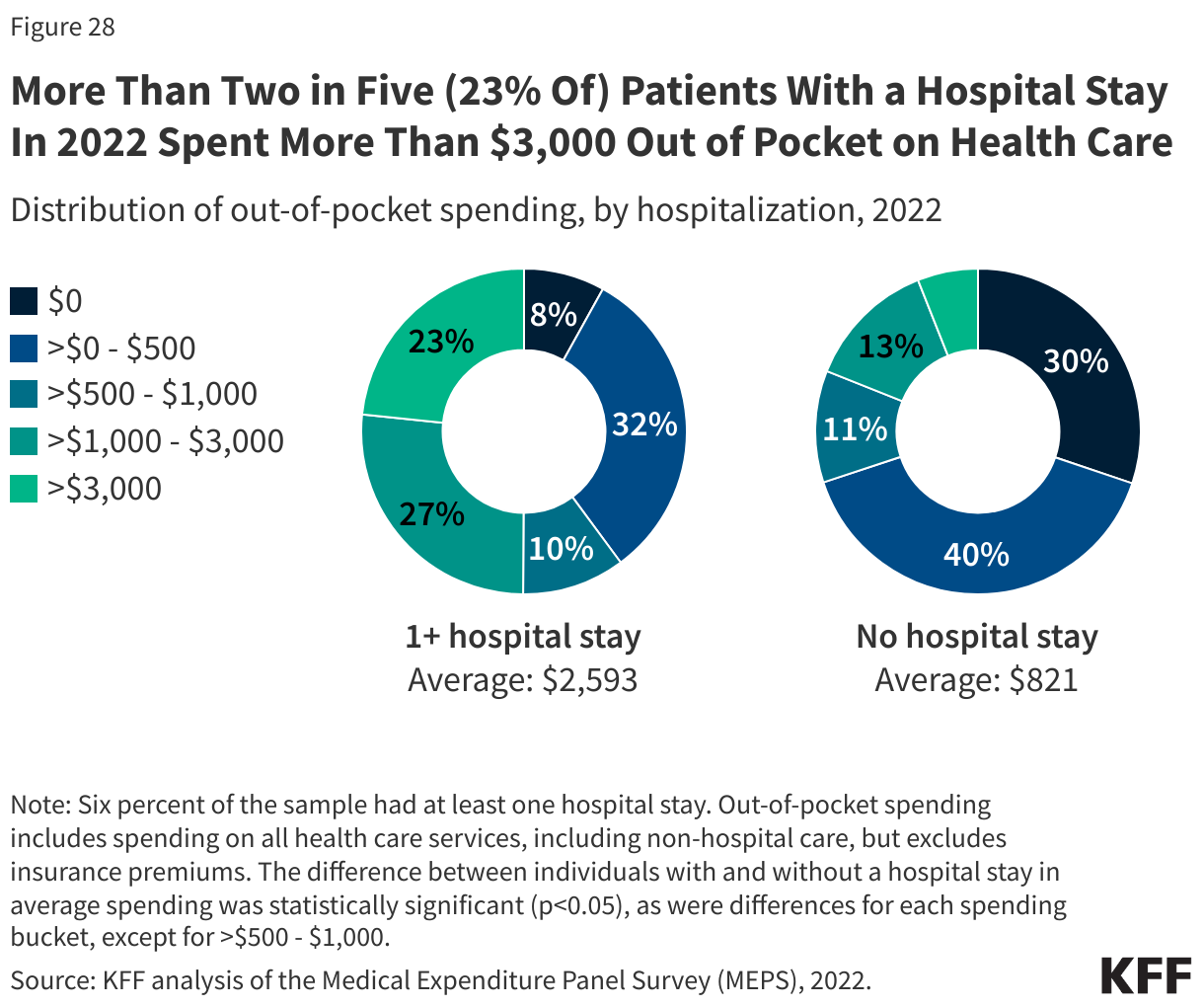

Medical Expenditures Panel Survey (MEPS). MEPS is a nationally representative survey of the U.S. civilian non-institutionalized population that includes information about health care expenditures and sources of payment, among other things. The analysis of out-of-pocket spending relied on the MEPS Household Component (HC).

National Health Expenditures. These data are published annually by the Centers for Medicare & Medicaid Services and provide estimates of national spending on health care, by payer and by type of service.

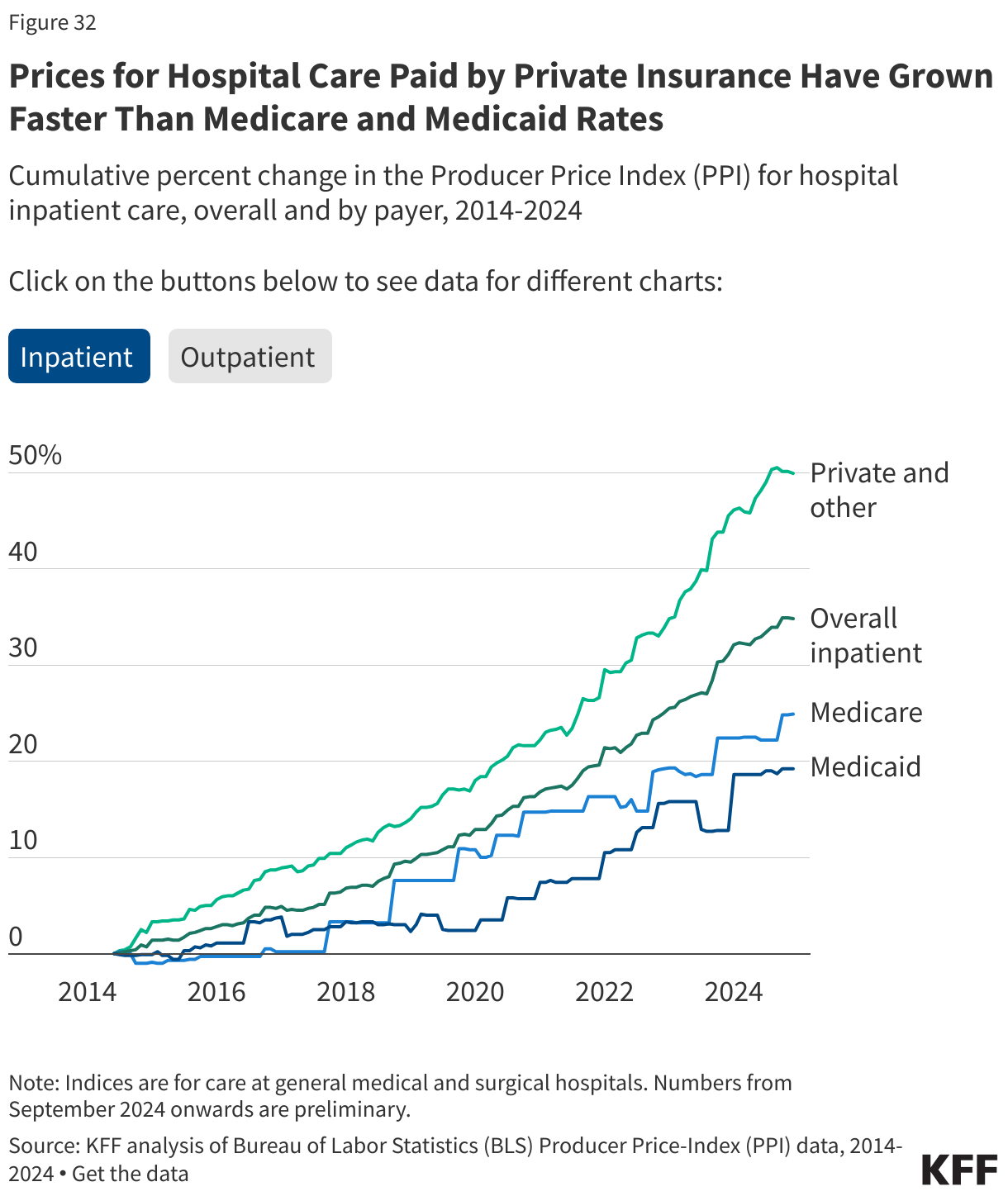

Producer Price Index (PPI). These data come from the Bureau of Labor Statistics (BLS). As BLS notes, PPI indices measure “the average change over time in selling prices received by domestic producers of goods and services.” The health care PPIs reflect the reimbursement that providers receive for health care services. The Medicare, Medicaid, and private and other patient PPIs are mutually exclusive. The Medicare and Medicaid PPIs take account of private Medicare and Medicaid plans. The PPI may exclude supplemental payments that are paid to hospitals as a lump sum.

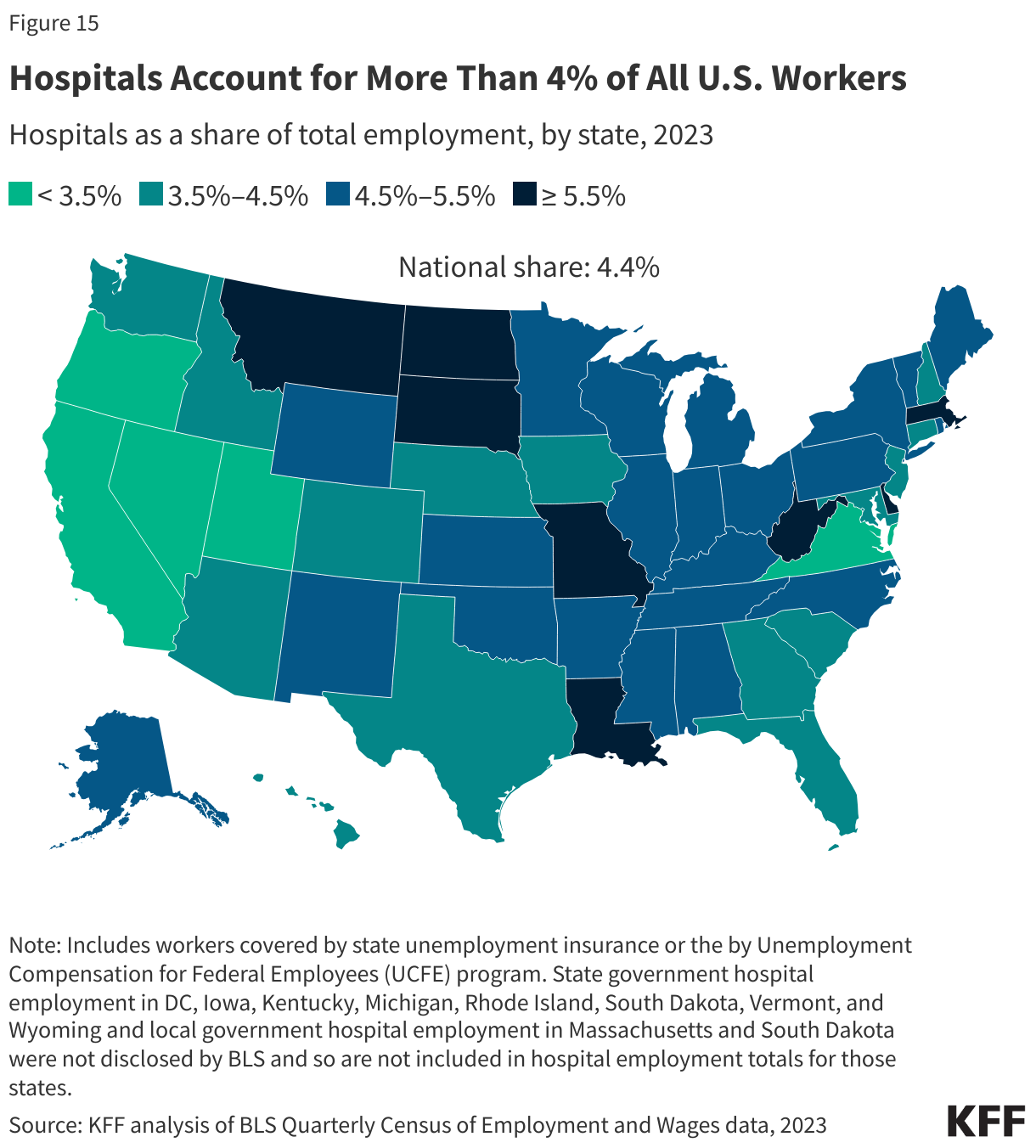

Quarterly Census of Wages and Employment (QCEW). These data also come from BLS. As BLS notes, the QCEW data provide a “quarterly count of employment and wages reported by employers covering more than 95 percent of U.S. jobs.” The QCEW includes workers covered by state unemployment insurance laws as well as federal workers covered by the Unemployment Compensation for Federal Employees (UCFE) program. Analyses of hospital and other employment relied on the average annual employment numbers reported by BLS. Industry subsector rankings were based on 3-digit NAICS codes. Employment for a given industry subsector and employer type were not included in totals when not disclosed by BLS.

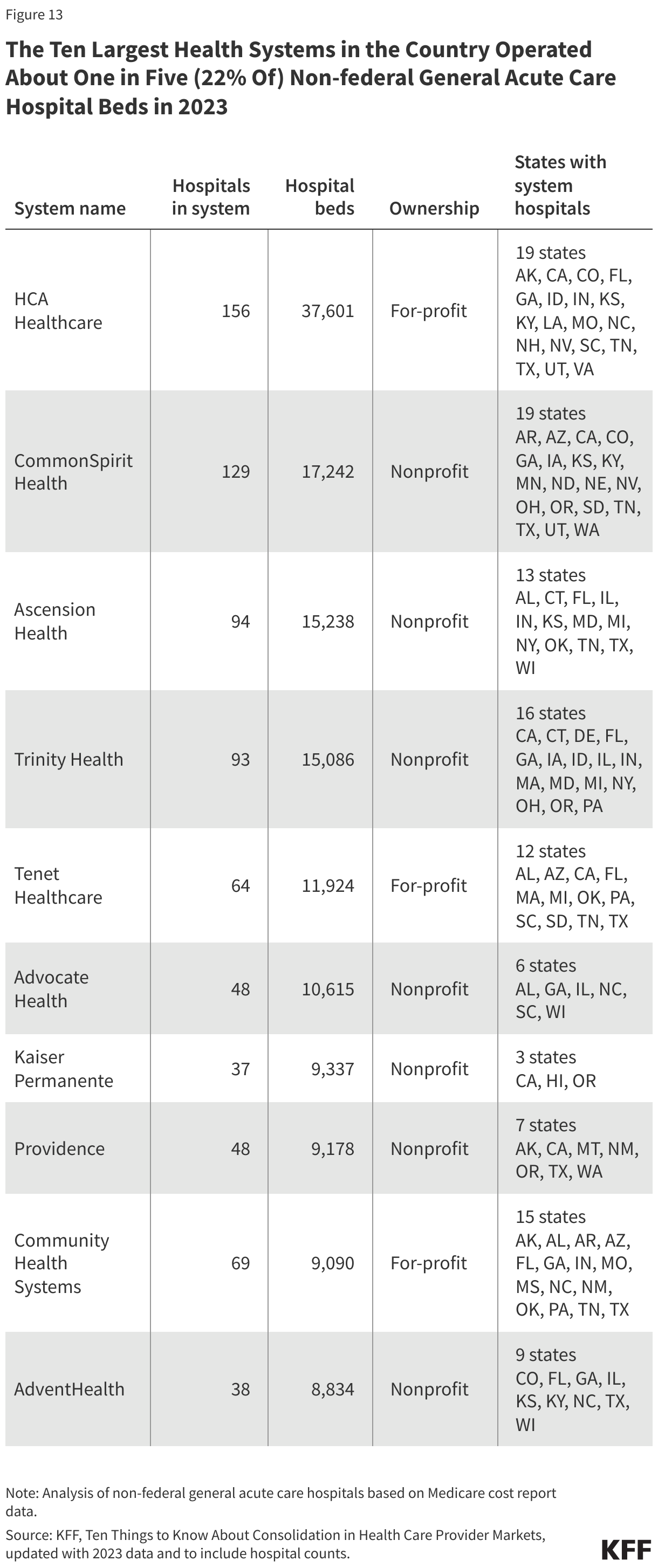

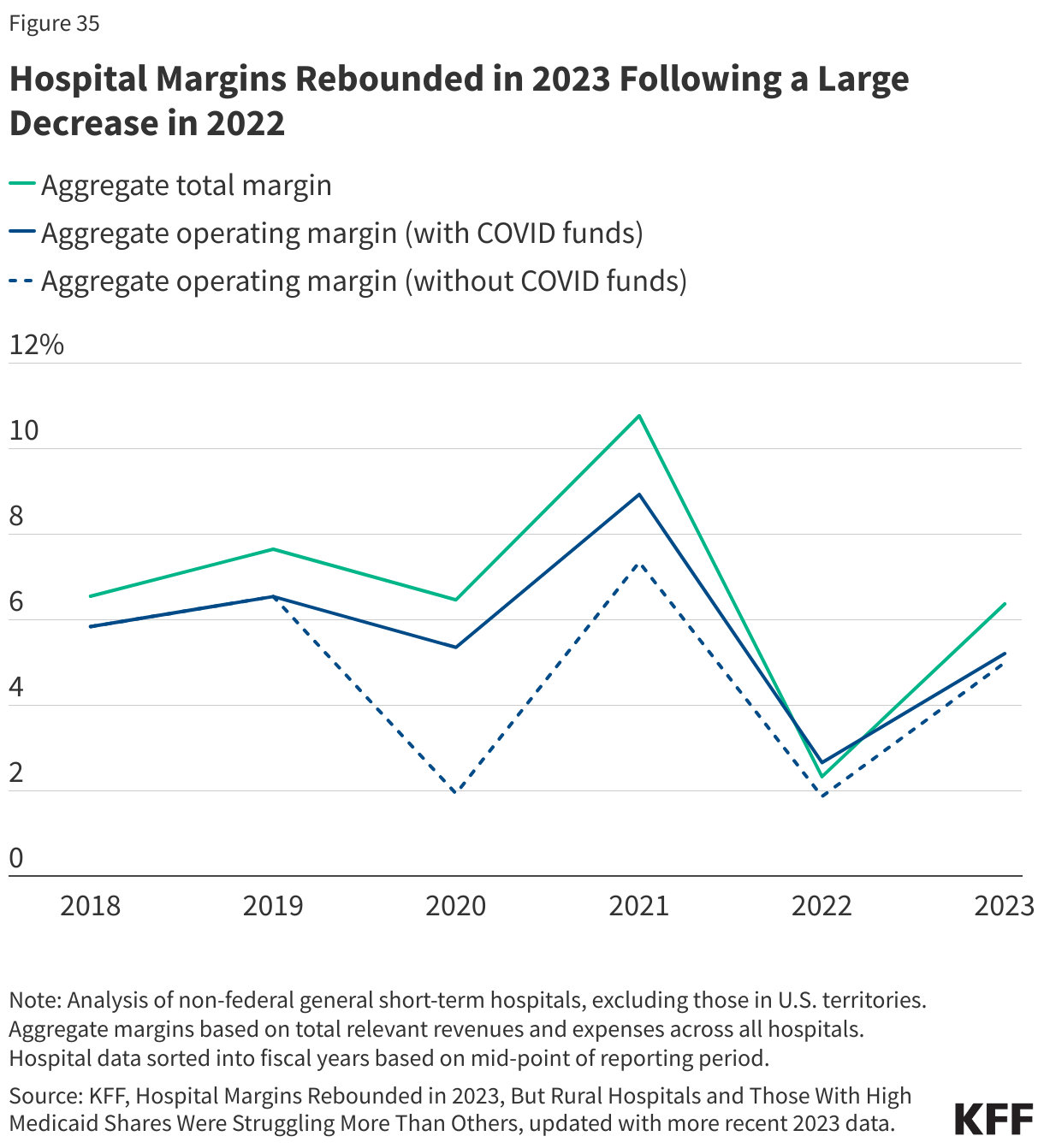

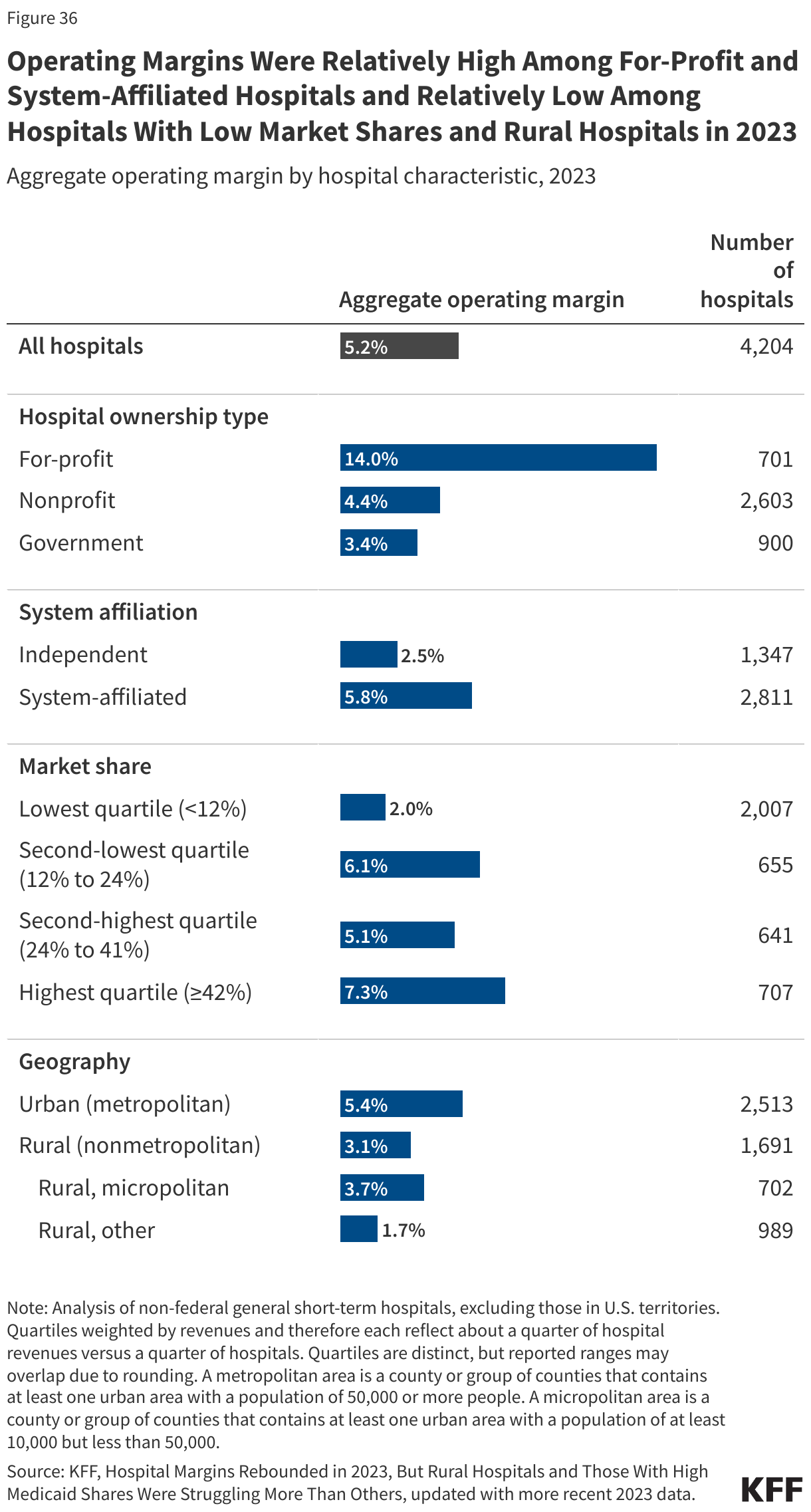

RAND Hospital Data. These data are a cleaned and processed version of annual cost reports that Medicare-certified hospitals are required to submit to the federal government. Cost reports include information about hospital characteristics, utilization, and finances. The RAND Hospital Data also crosswalk hospitals to health systems based on the Agency for Healthcare Research and Quality (AHRQ) Compendium of U.S. Health Systems.

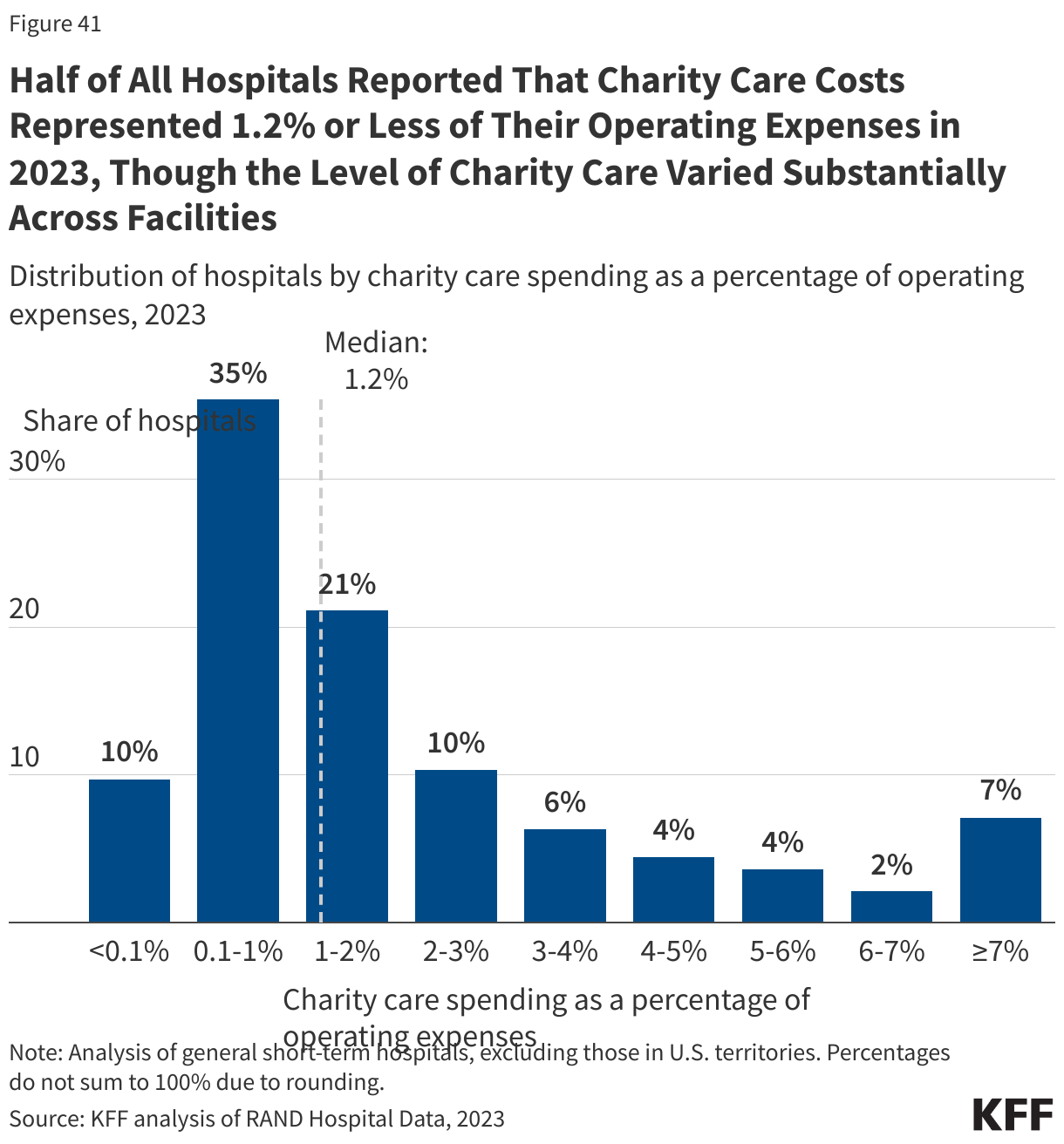

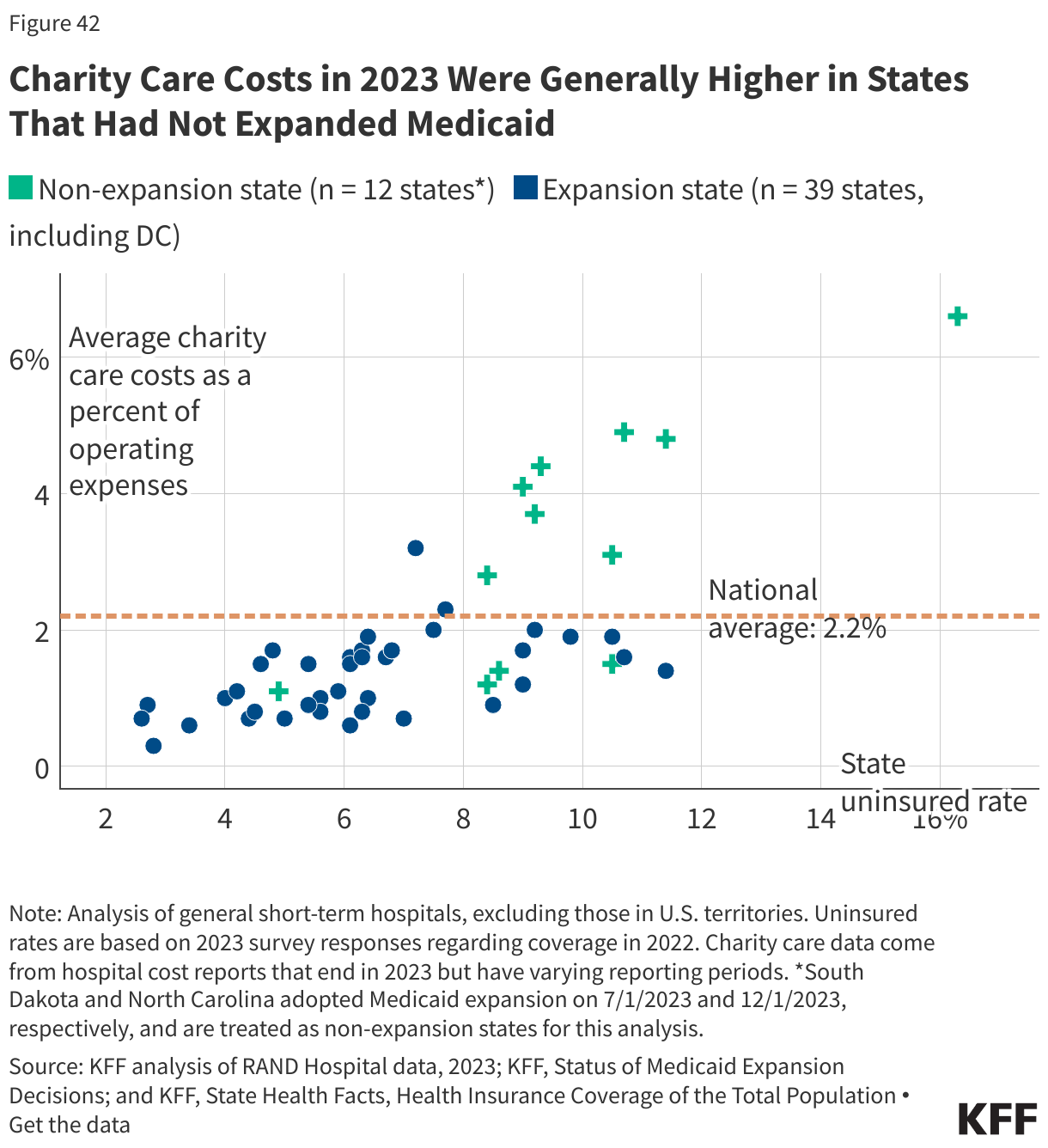

For charity care analyses, missing charity care costs were recoded as $0 if the hospital reported total unreimbursed and uncompensated care costs. Hospitals were excluded if they had missing or negative operating expenses or charity care costs, outlier amounts of charity care as a percent of operating expenses (≥18.1%), or reporting periods less than or greater than one year. Cost report instructions indicate that hospitals should report amounts related to both charity care and uninsured discounts as part of their charity care costs. MedPAC has noted that current HCRIS calculations favor hospitals with higher markups, and it has recommended revisions that would put hospitals on more equal footing and reduce reported charity care costs on average.

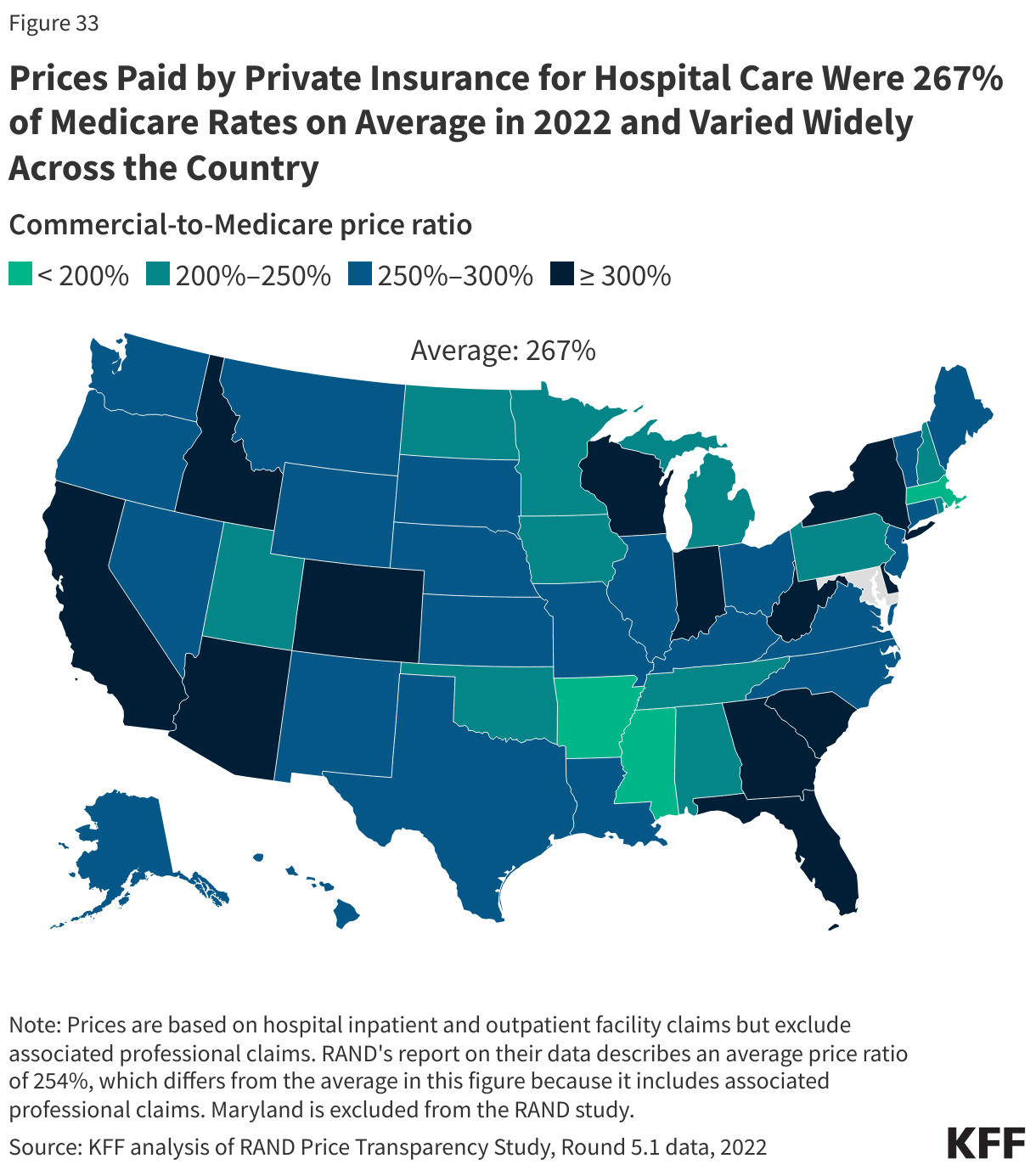

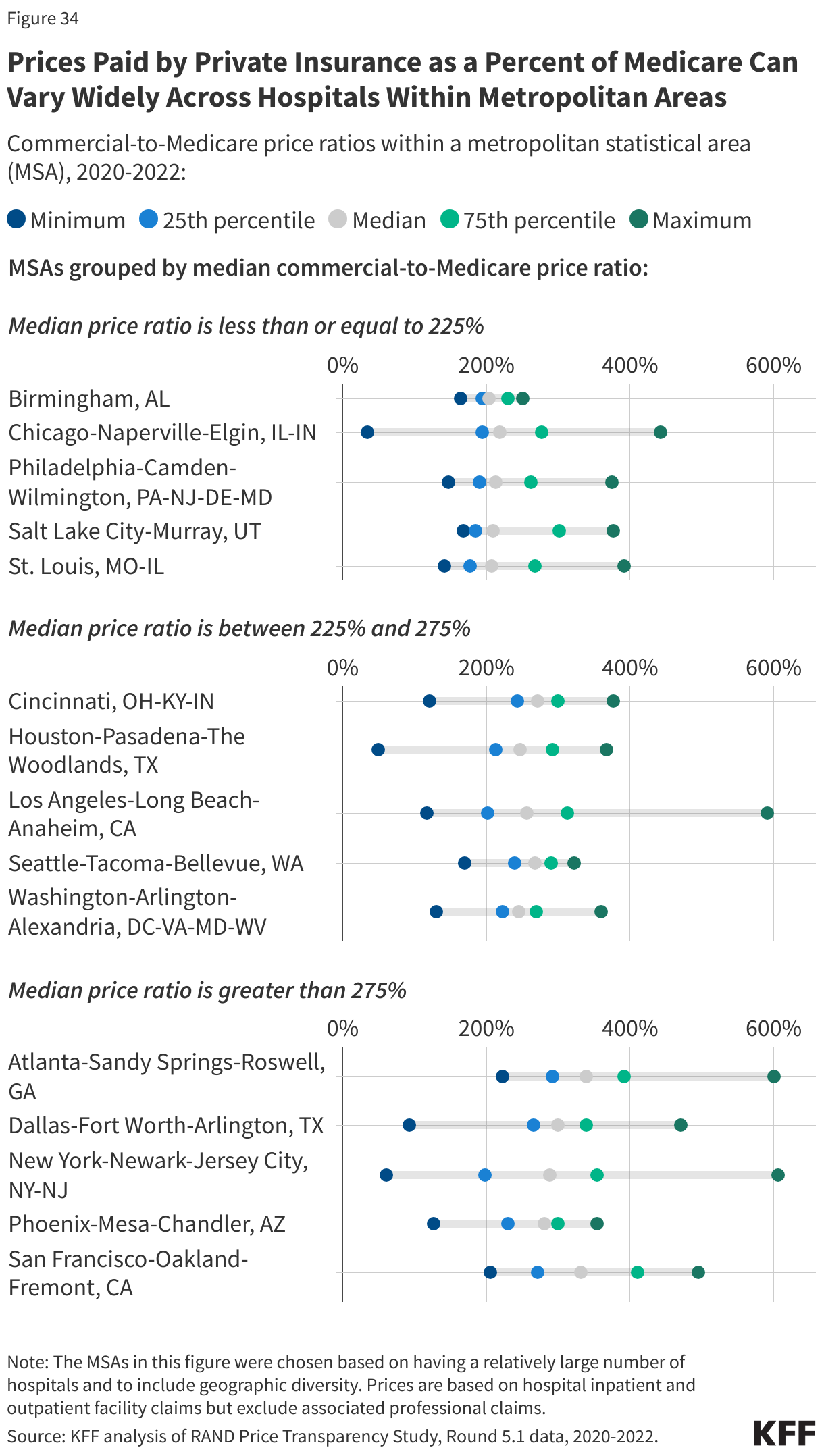

RAND Price Transparency Study, Round 5.1. These data are based on commercial claims for employer-sponsored health insurance plan enrollees collected from participating self-insured employers and health plans as well as from all-payer claims databases (APCDs) from 12 states. Commercial-to-Medicare price ratios are based on the actual allowed amount from the claims and an estimate of the allowed amount had Medicare covered the same services. Ratios presented in key facts include facility claims for hospital inpatient and outpatient services but exclude associated professional claims (which are also available through the RAND study). Analyses of metropolitan areas exclude hospitals for which RAND did not disclose relevant data while state and national analyses include all hospitals in the RAND study.

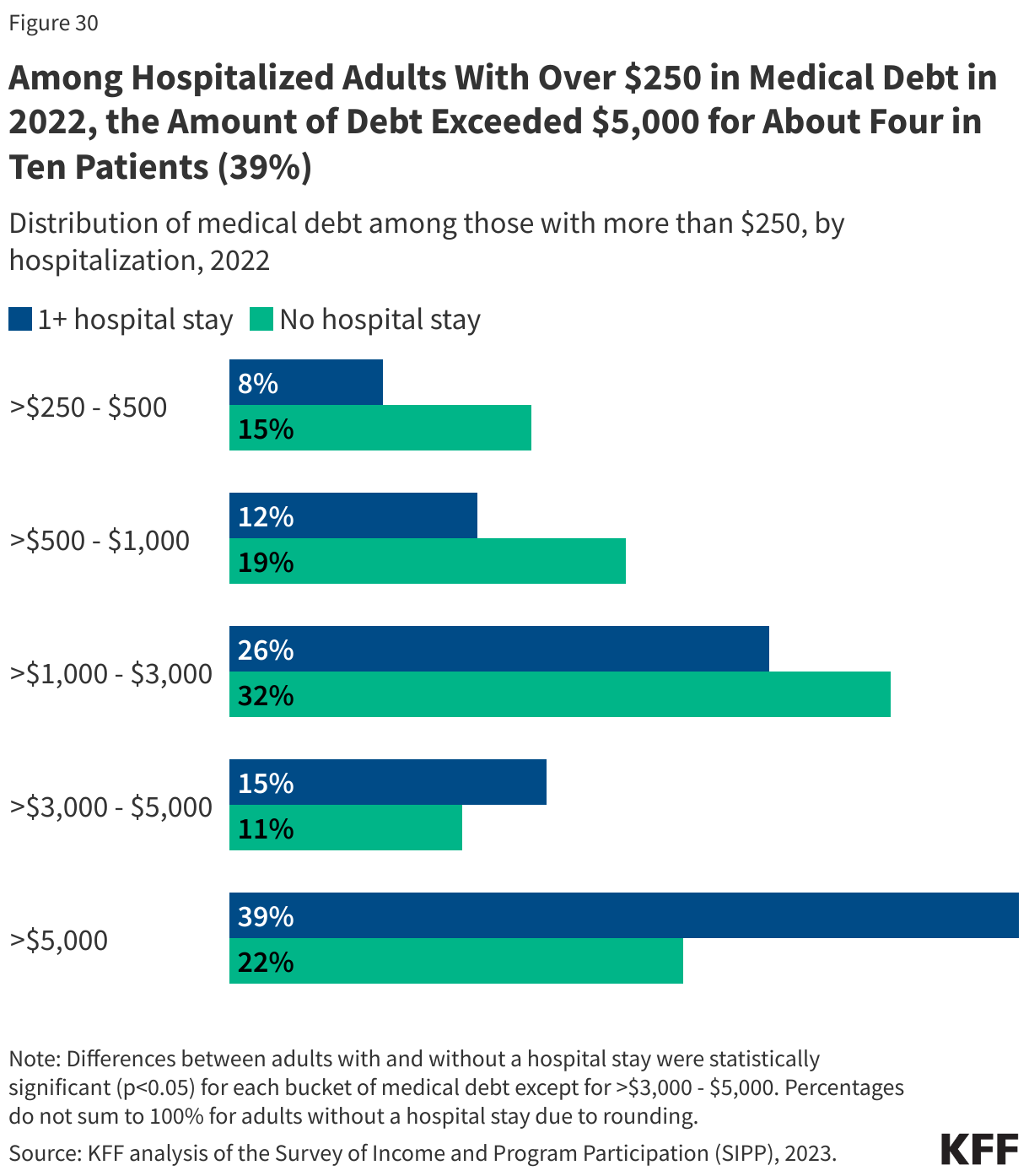

Survey of Income and Program Participation (SIPP). SIPP is a nationally representative survey of the civilian noninstitutionalized population. Among other questions, SIPP asks individuals ages 15 and older about their medical debt. The analysis of medical debt further restricted the sample to adults ages 18 and older.

Back to top

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

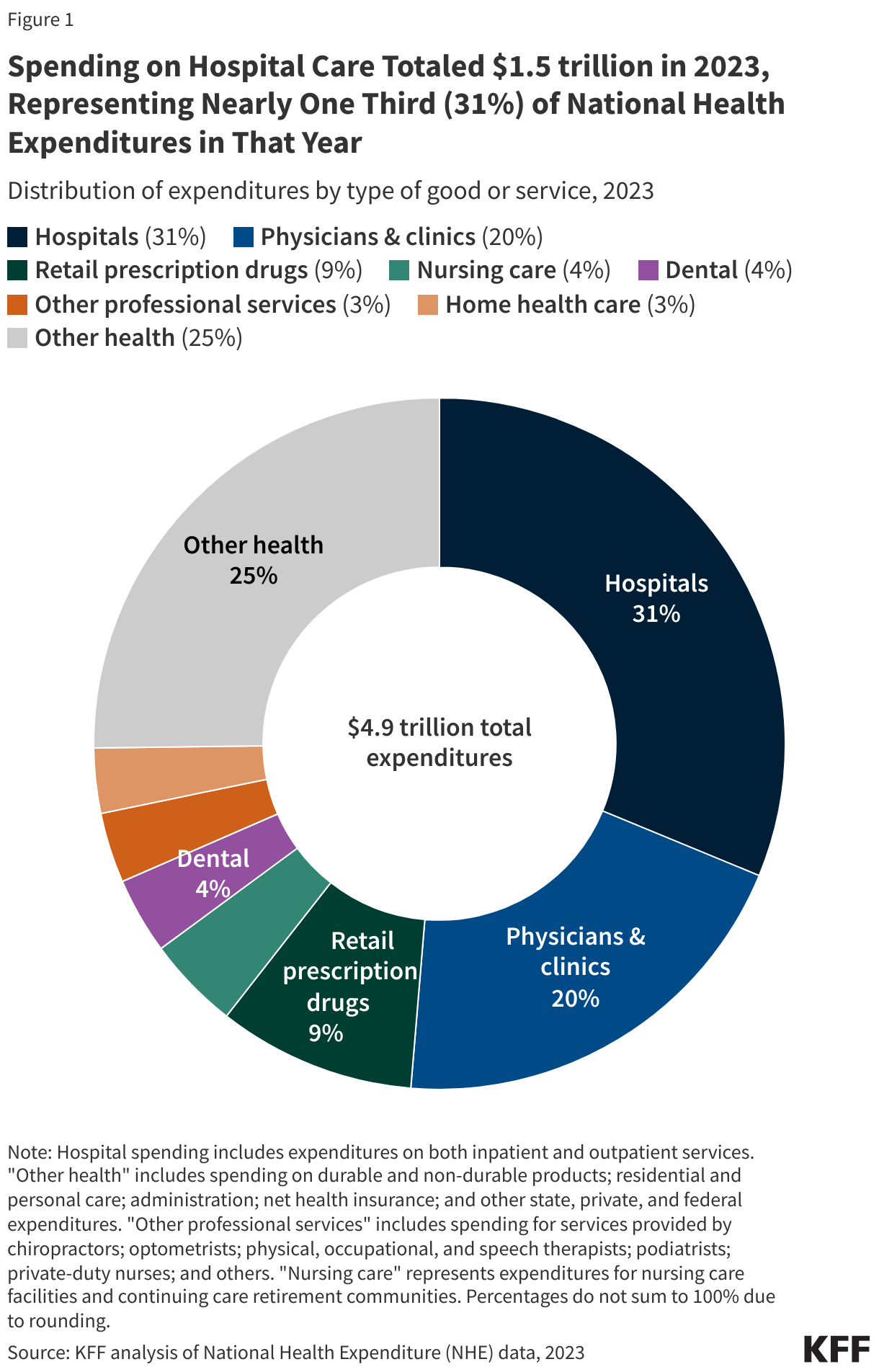

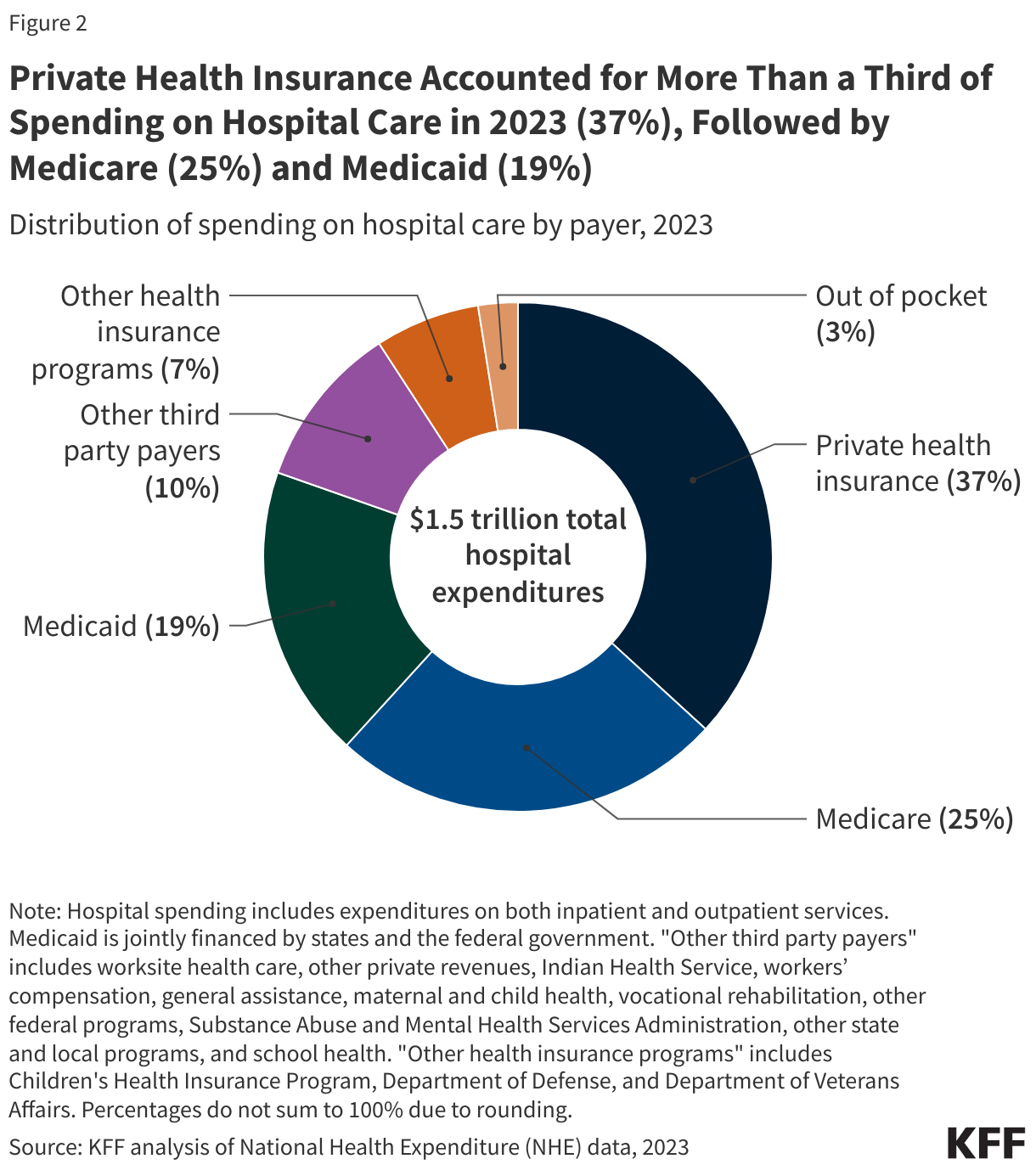

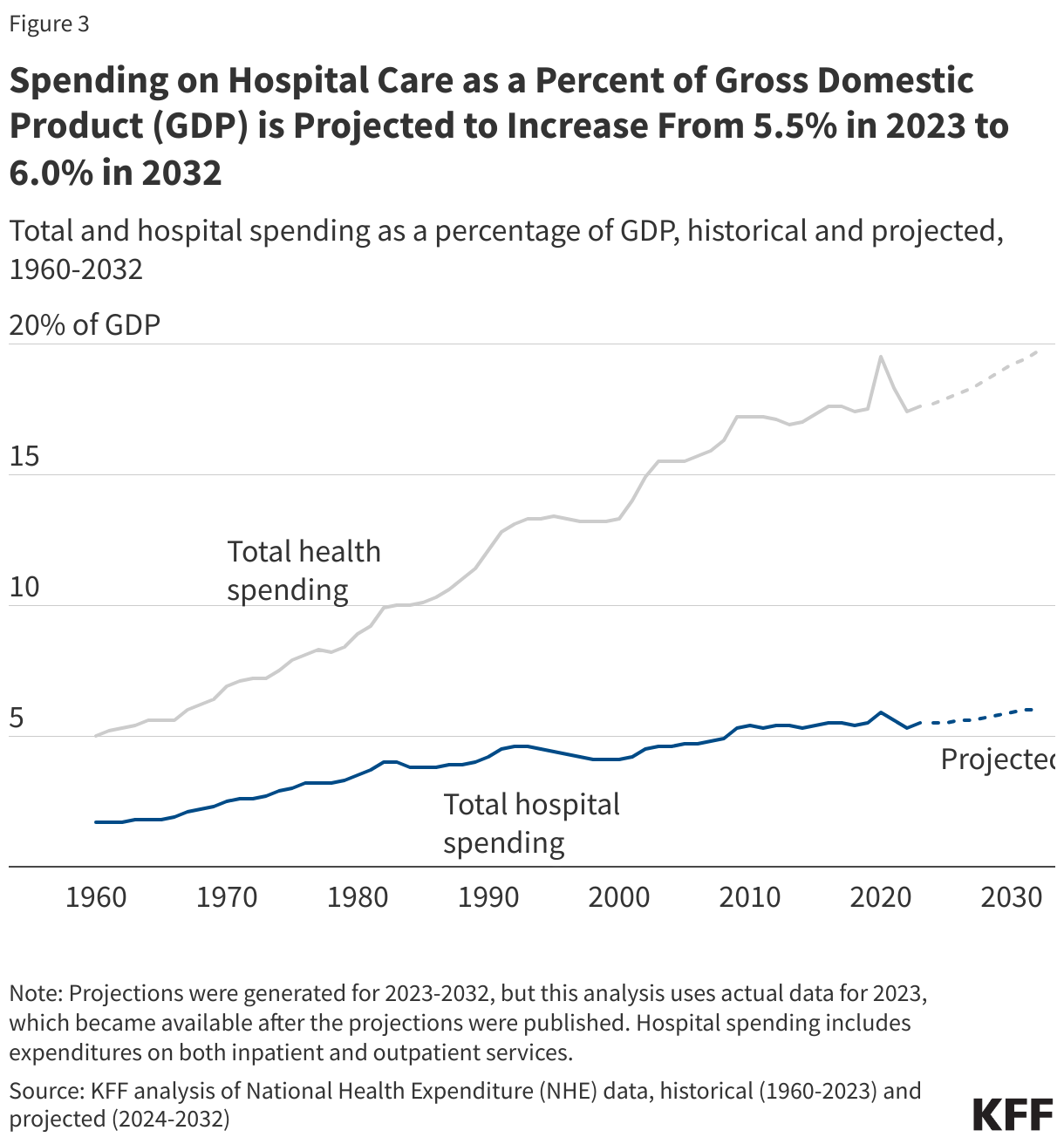

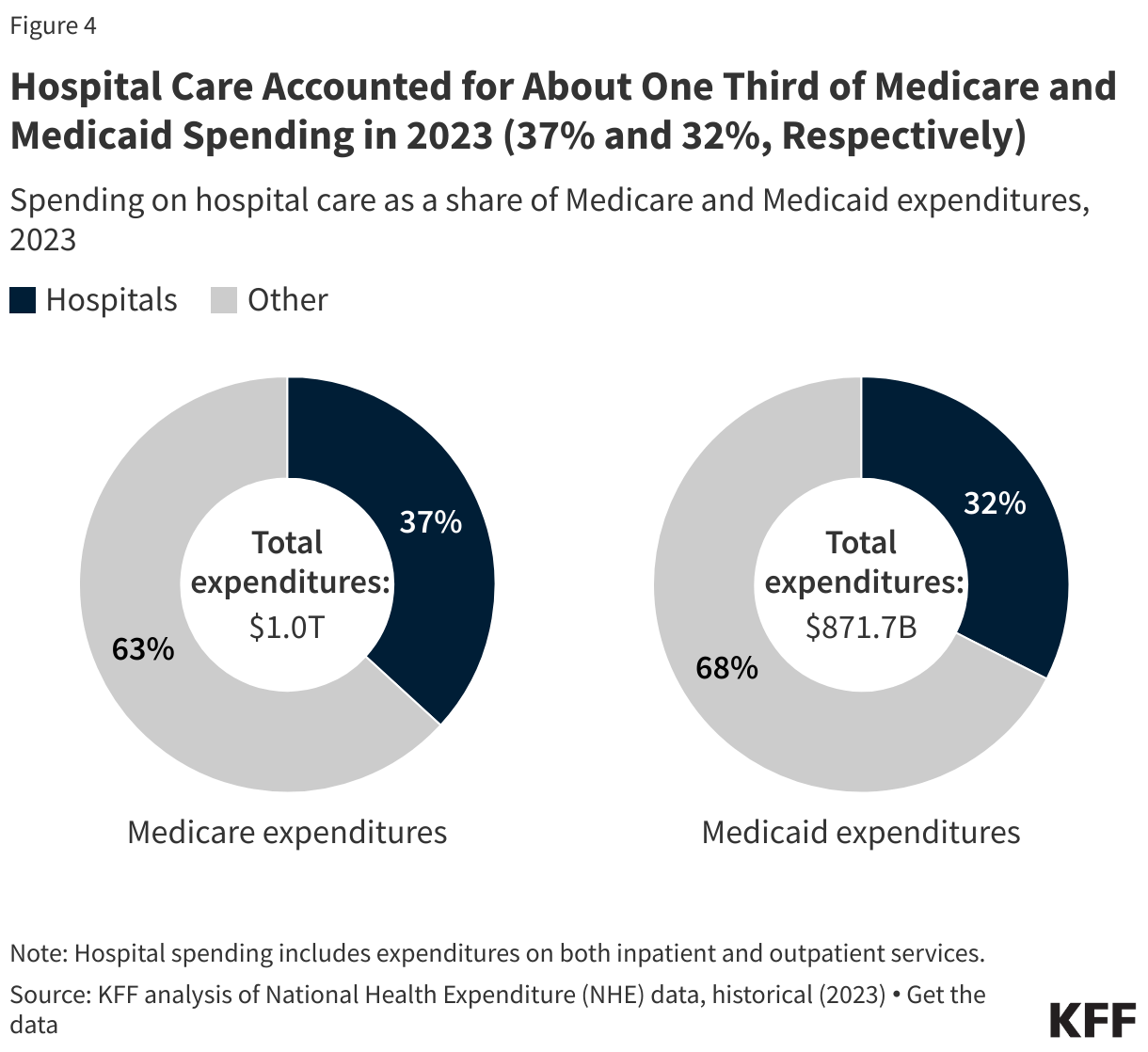

National Hospital Spending

National Hospital Spending The Hospital

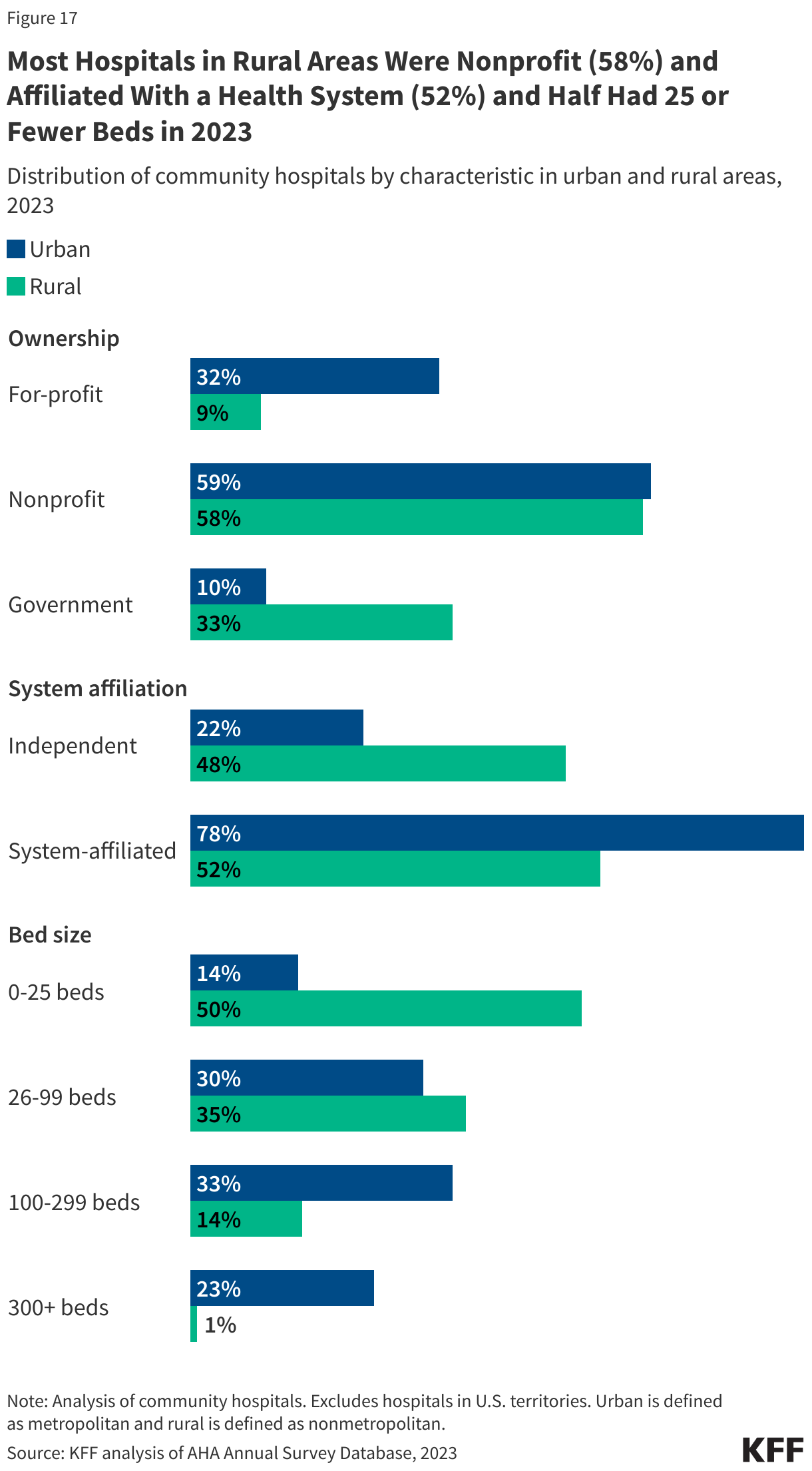

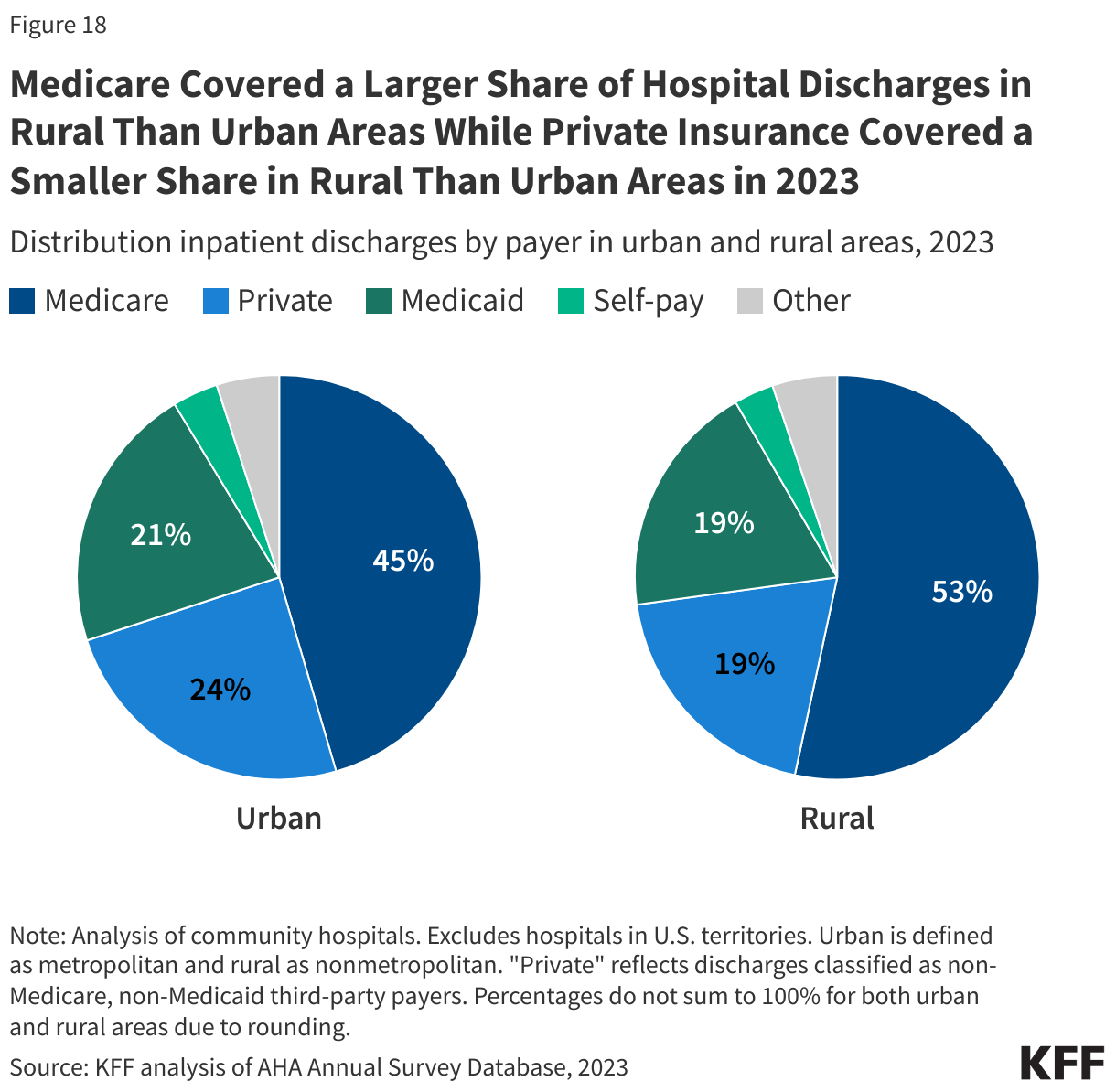

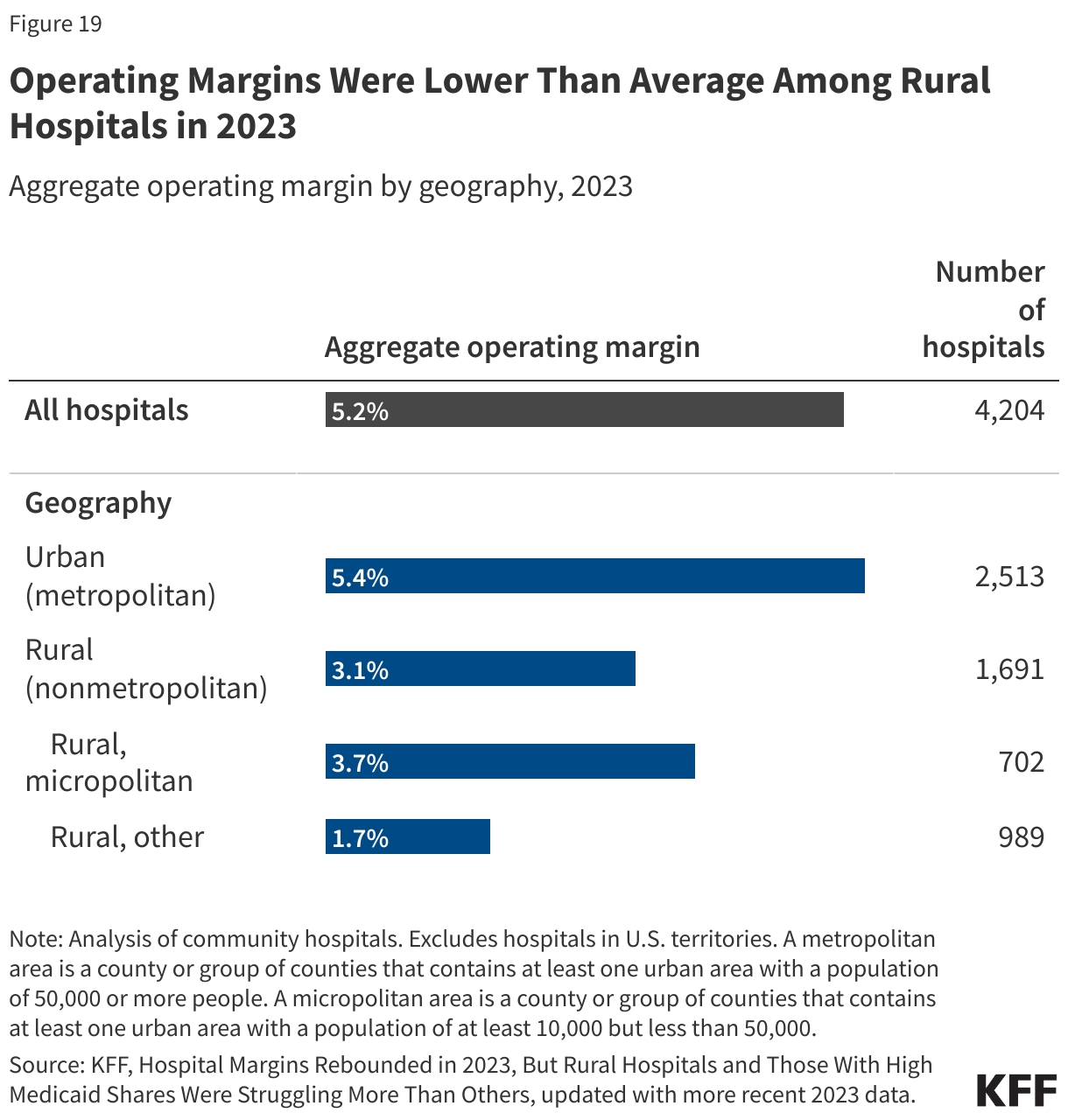

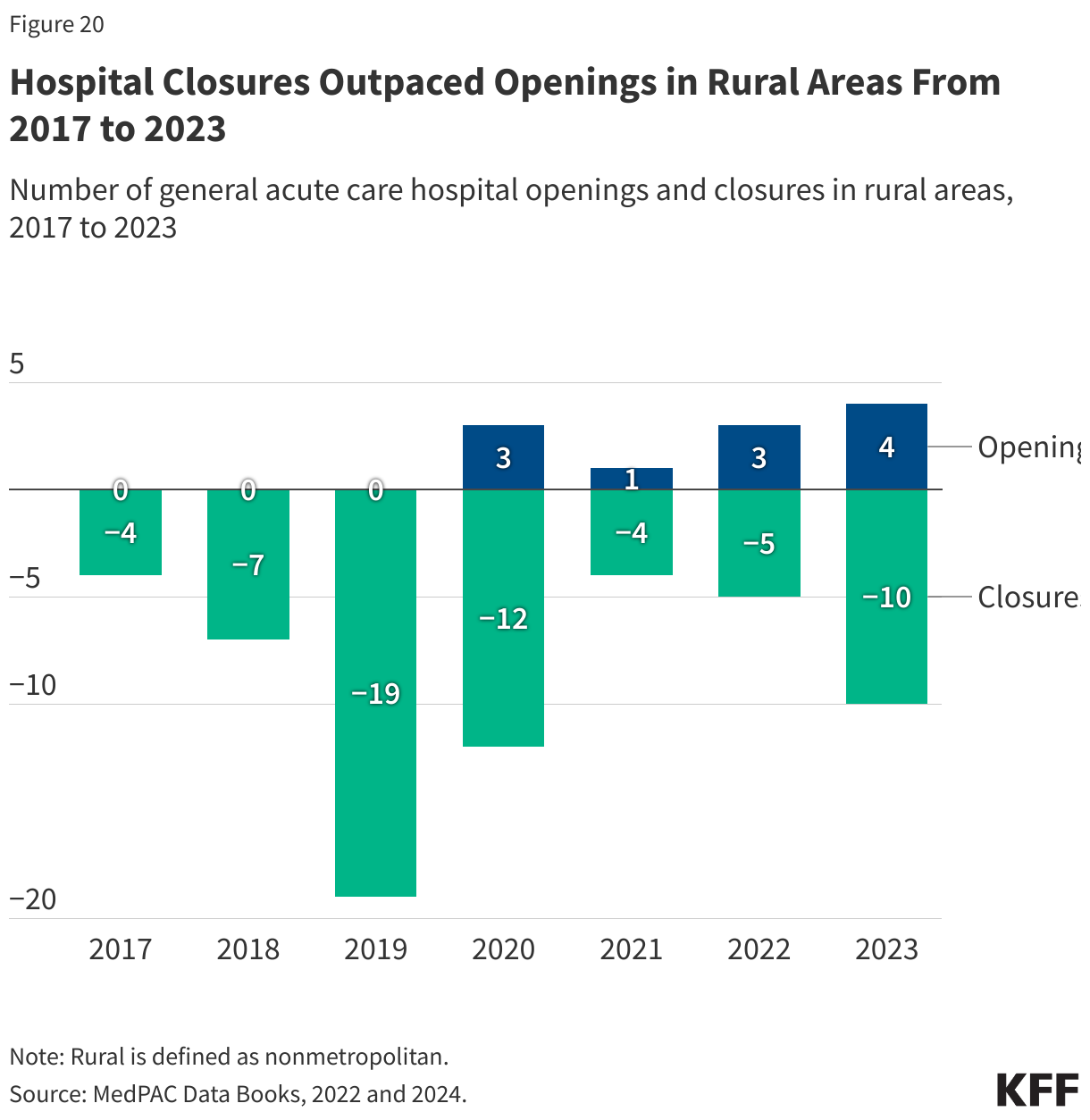

The Hospital Rural Hospitals

Rural Hospitals Use of Hospital Care

Use of Hospital Care Out-of-Pocket Spending and Medical Debt

Out-of-Pocket Spending and Medical Debt Hospital Prices

Hospital Prices Hospital Finances

Hospital Finances Charity Care

Charity Care