Spending. Medicare plays a significant role in the health care system, accounting for 21% of total national health spending in 2021, 26% of spending on both hospital care and physician and clinical services, and 32% of spending on retail prescription drug sales (Figure 16).

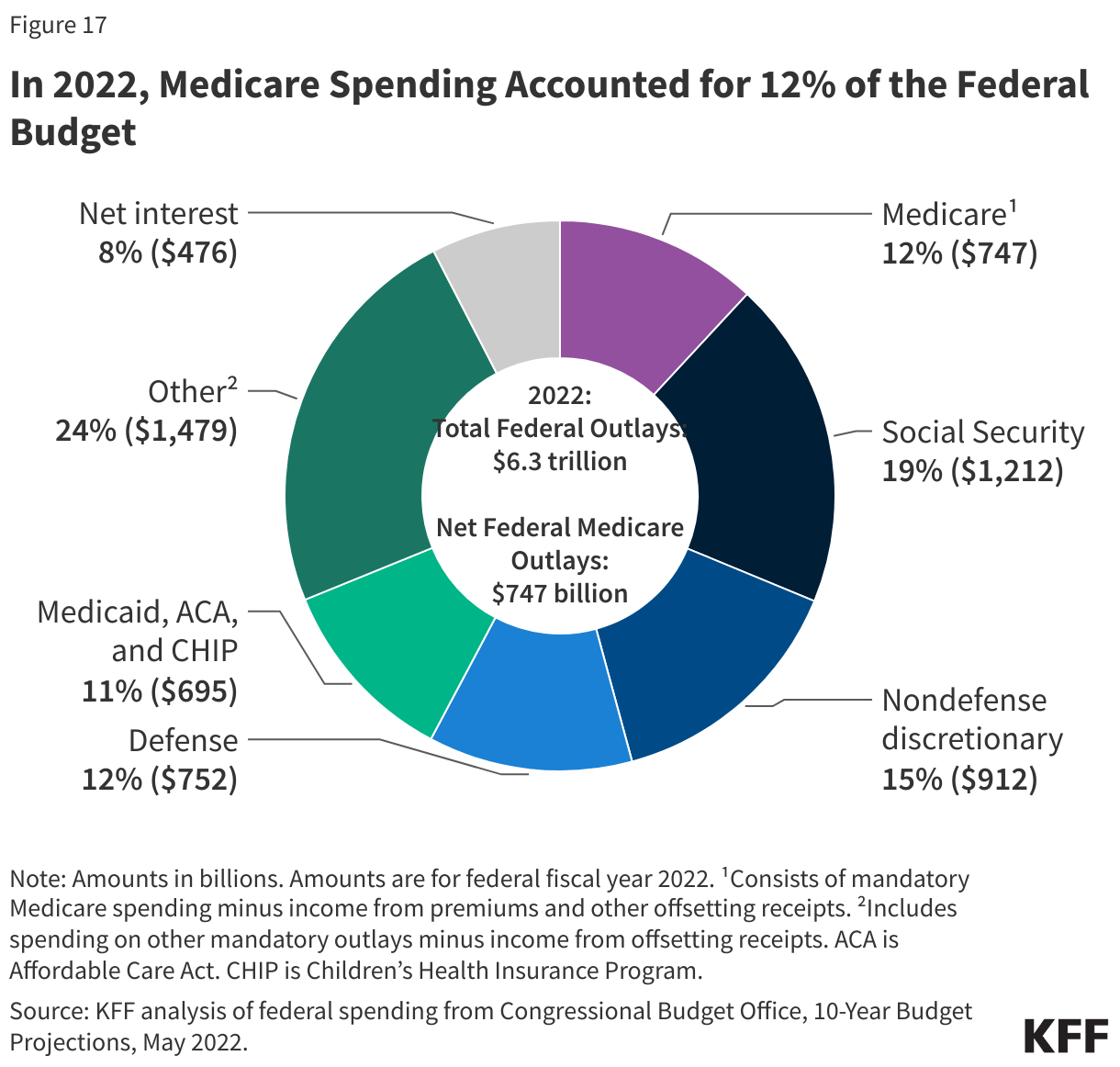

In 2022, Medicare spending, net of income from premiums and other offsetting receipts, totaled $747 billion and accounted for 12% of the federal budget—a similar share as spending on Medicaid, the ACA, and the Children’s Health Insurance Program combined, and defense spending (Figure 17).

In 2023, Medicare benefit payments are estimated to total $1 trillion, up from $583 billion in 2013 (including spending for Part A, Part B, and Part D benefits in both traditional Medicare and Medicare Advantage). Medicare spending per person has also grown, increasing from $5,800 to $15,700 between 2000 and 2022 – or 4.6% average annual growth over the 22-year period. In recent years, however, growth in Medicare spending per person has been lower in Medicare than in private health insurance.

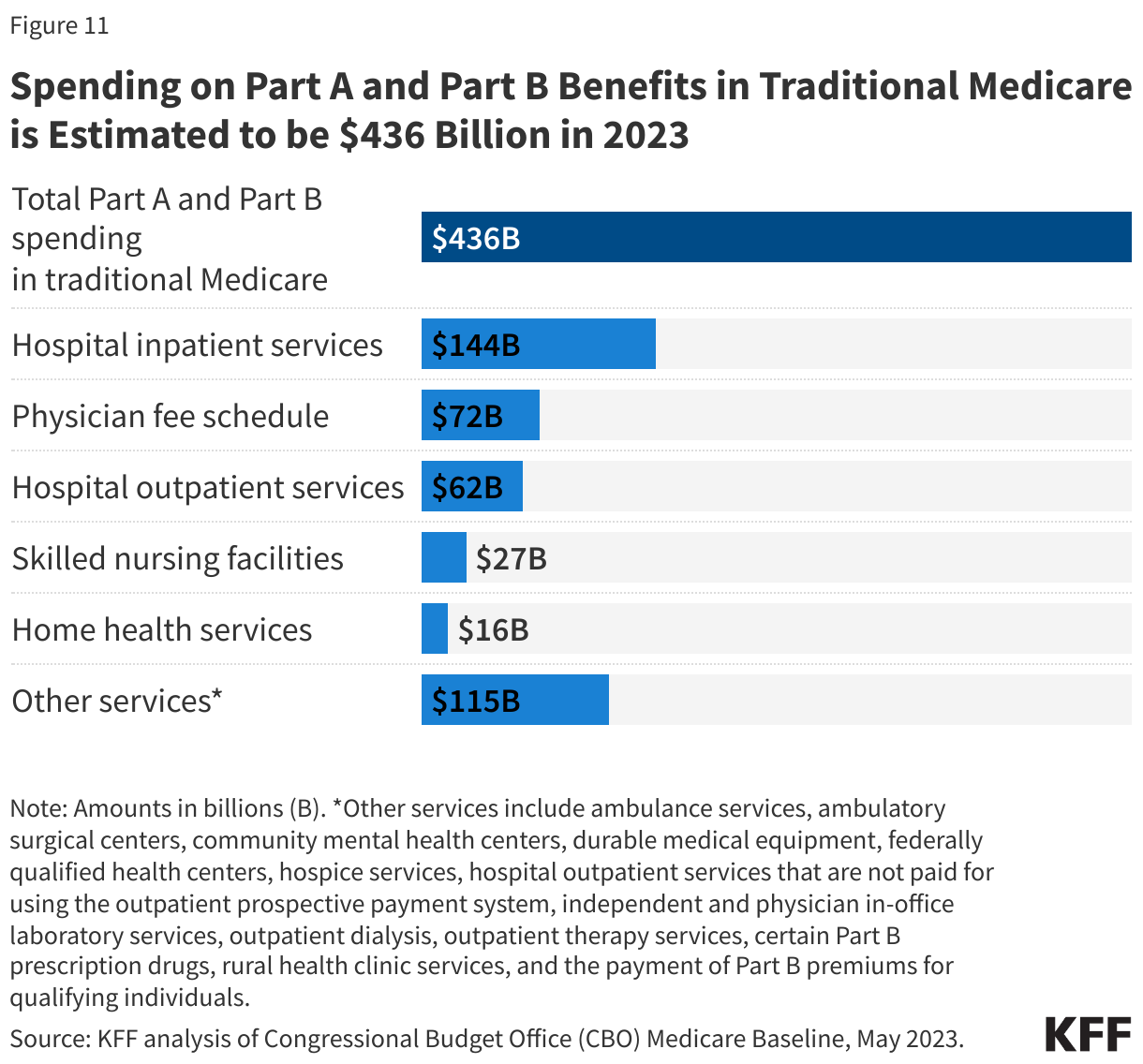

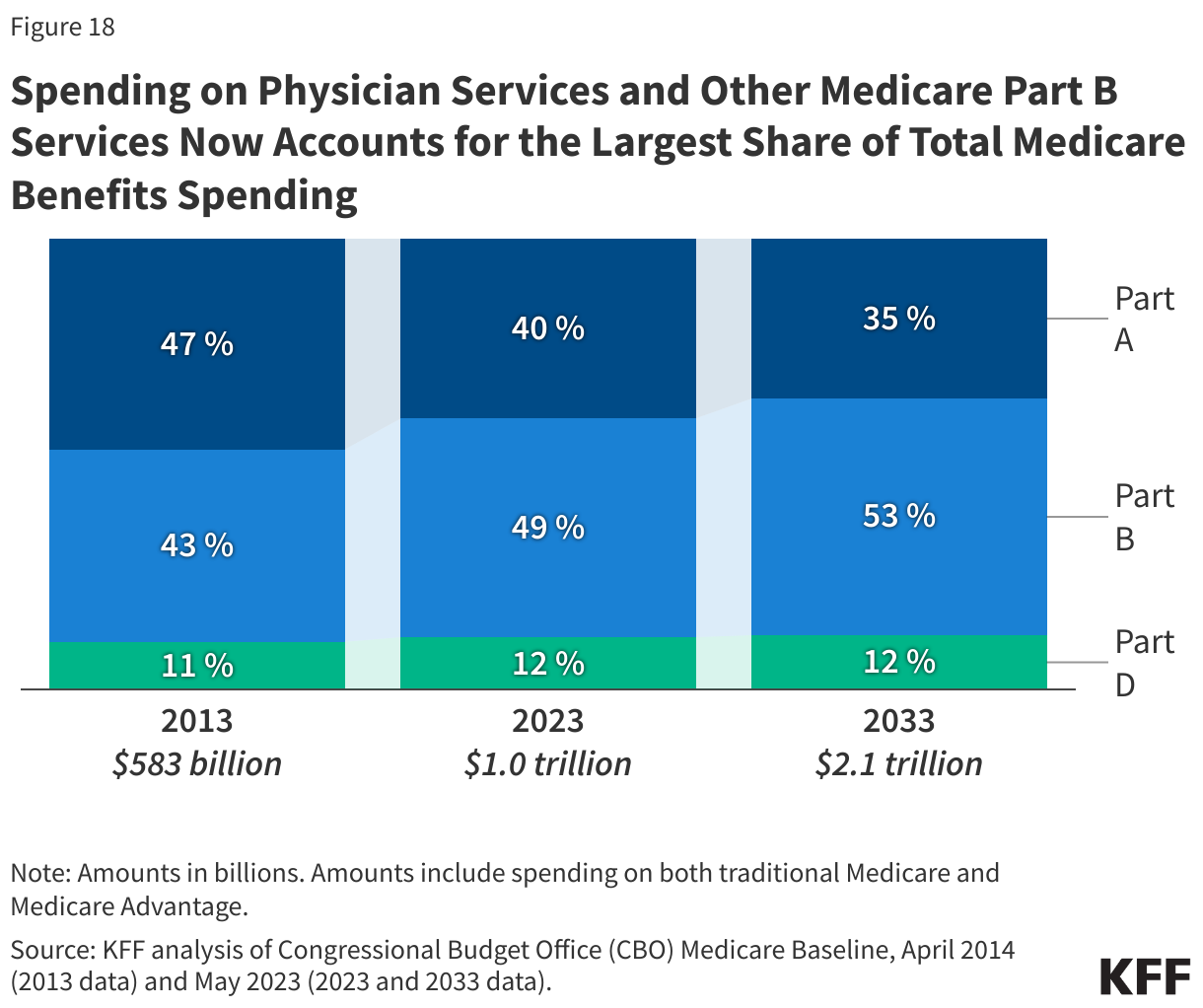

Spending on Medicare Part A benefits (mainly hospital inpatient services) has decreased as a share of total Medicare spending over time as care has shifted from inpatient to outpatient settings, leading to an increase in spending on Part B benefits (including physician services, outpatient services, and physician-administered drugs). Spending on Part B services now accounts for the largest share of Medicare benefit spending (49% in 2023) (Figure 18). Moving forward, Medicare spending on physician services and other services covered under Part B is expected to grow to more than half of total Medicare spending by 2033, while spending on hospital care and other services covered under Part A is projected to decrease further as a share of the total.

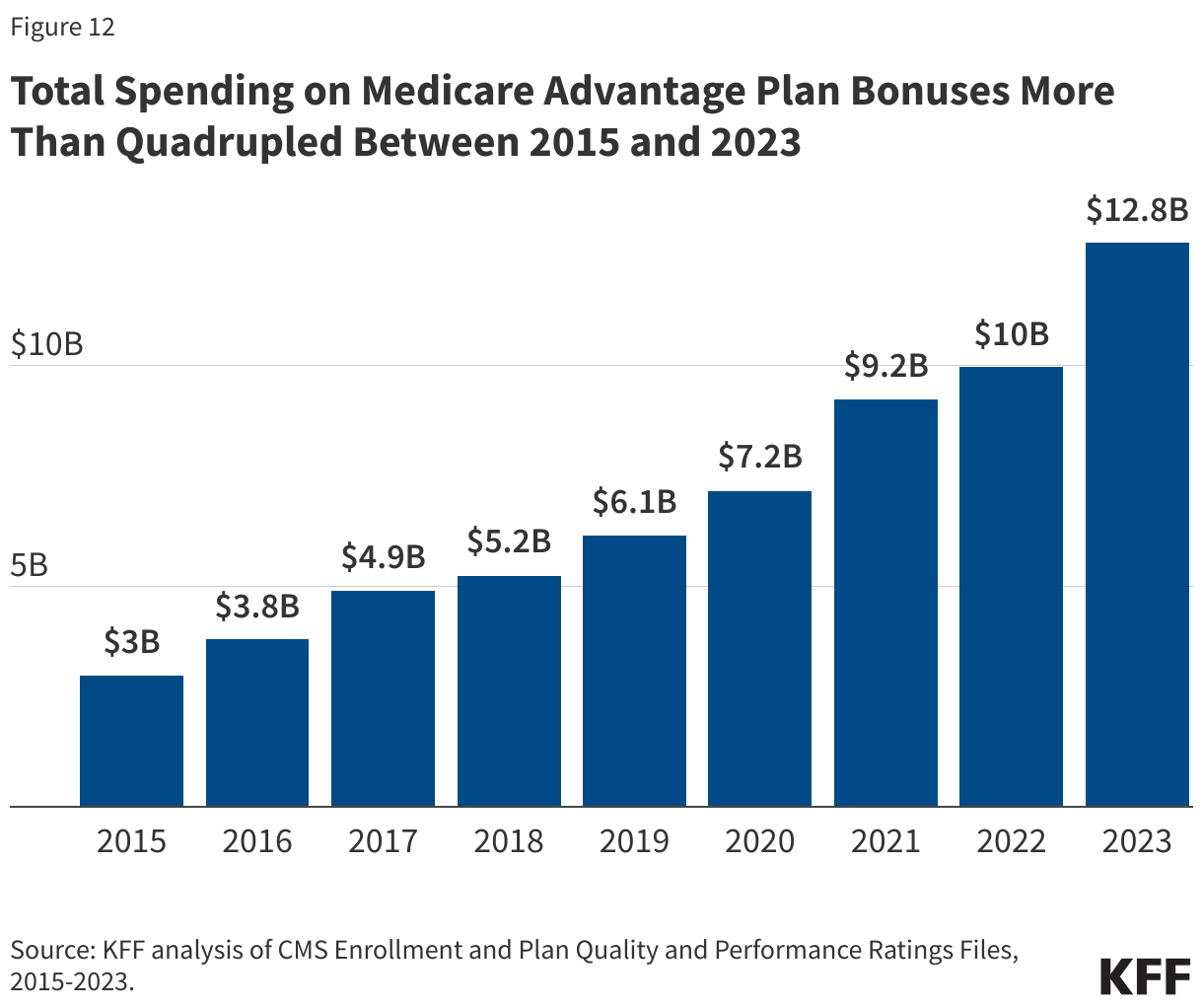

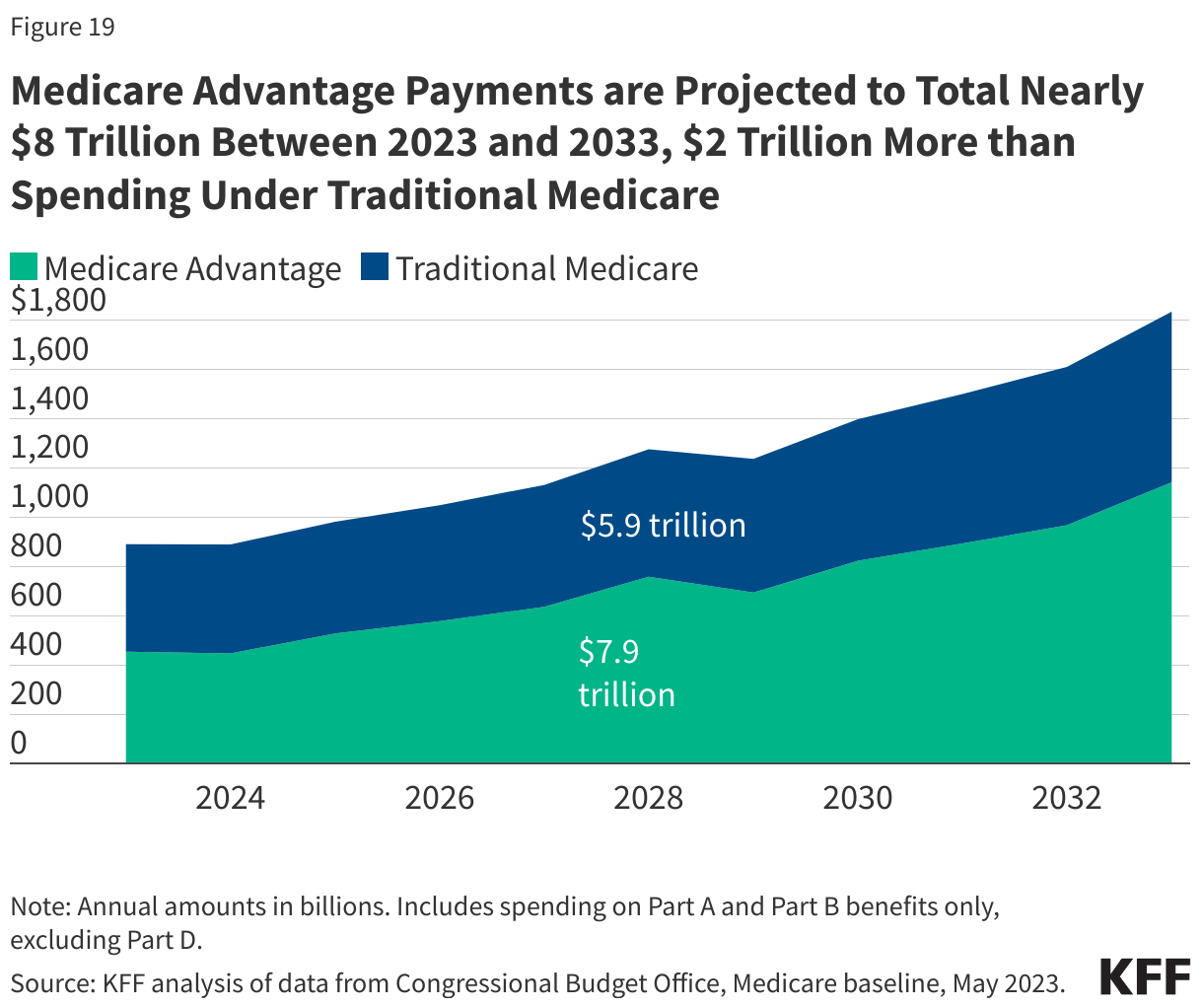

Payments to Medicare Advantage plans for Part A and Part B benefits tripled as a share of total Medicare spending between 2013 and 2023, from $145 billion to $454 billion, partly due to steady enrollment growth in Medicare Advantage plans. Growth in spending on Medicare Advantage also reflects that Medicare pays more to private Medicare Advantage plans for enrollees than their costs in traditional Medicare, on average. (See “How Does Medicare Pay Private Plans in Medicare Advantage and Medicare Part D?” for additional information.) These higher payments have contributed to growth in spending on Medicare Advantage and overall Medicare spending. In 2023, just over half of all Medicare program spending for Part A and Part B benefits was for Medicare Advantage plans, up from just under 30% in 2013. Between 2023 and 2033, Medicare Advantage payments are projected to total nearly $8 trillion, $2 trillion more than spending under traditional Medicare (Figure 19).

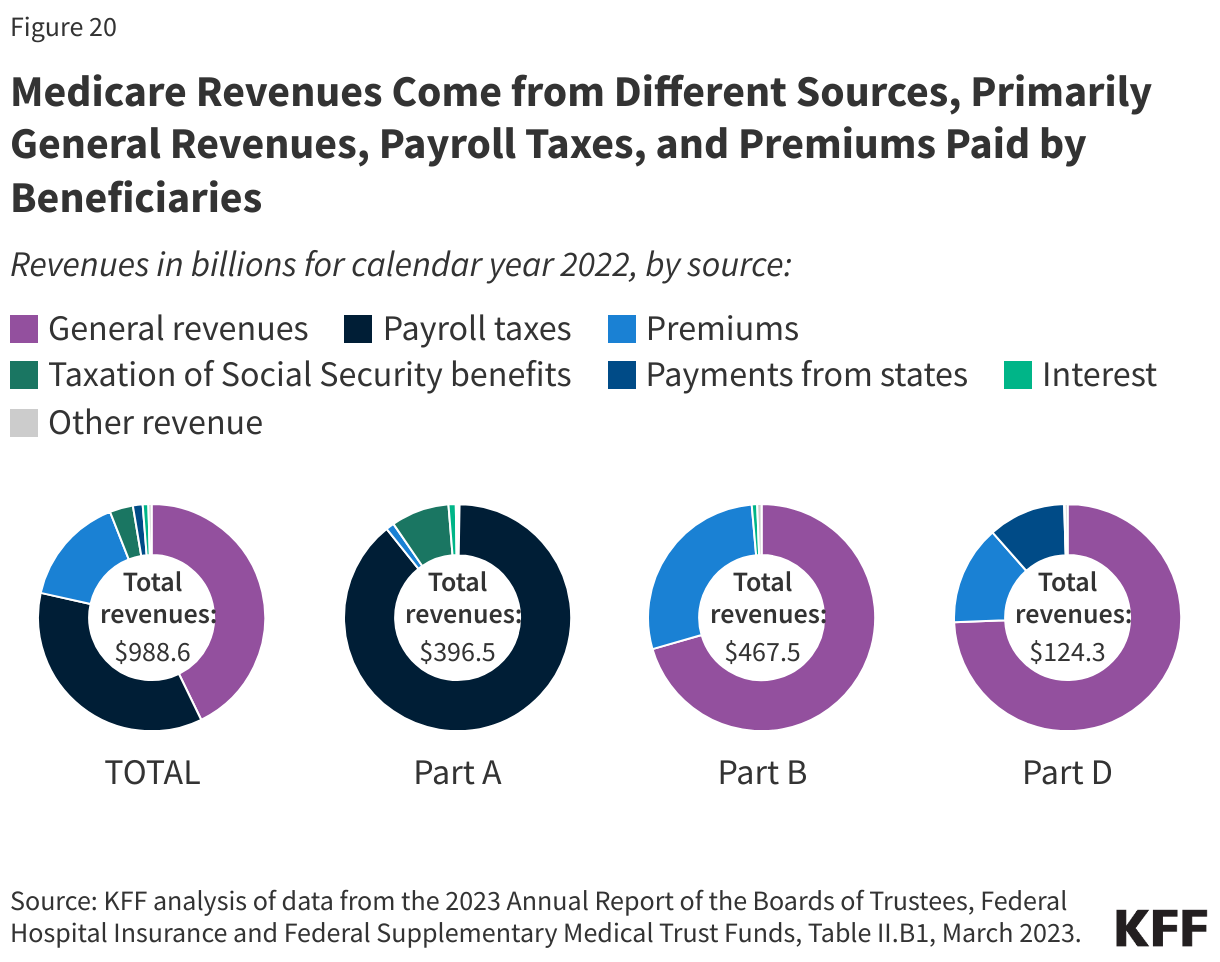

Financing. Medicare funding, which totaled $989 billion in 2022, comes primarily from general revenues (43%), payroll tax revenues (36%), and premiums paid by beneficiaries (16%). Other sources include taxes on Social Security benefits, payments from states, and interest.

The different parts of Medicare are funded in varying ways, and revenue sources dedicated to one part of the program cannot be used to pay for another part (Figure 20).

- Part A, which covers inpatient hospital stays, skilled nursing facility (SNF) stays, some home health visits, and hospice care, is financed primarily through a 2.9% tax on earnings paid by employers and employees (1.45% each). Higher-income taxpayers (more than $200,000 per individual and $250,000 per couple) pay a higher payroll tax on earnings (2.35%). Payroll taxes accounted for 89% of Part A revenue in 2022.

- Part B, which covers physician visits, outpatient services, preventive services, and some home health visits, is financed primarily through a combination of general revenues (71% in 2022) and beneficiary premiums (28%) (and 1% from interest and other sources). The standard Part B premium that most Medicare beneficiaries pay is calculated as 25% of annual Part B spending, while beneficiaries with annual incomes over $103,000 per individual or $206,000 per couple pay a higher, income-related Part B premium reflecting a larger share of total Part B spending, ranging from 35% to 85%.

- Part D, which covers outpatient prescription drugs, is financed primarily by general revenues (74%) and beneficiary premiums (14%), with an additional 11% of revenues coming from state payments for beneficiaries enrolled in both Medicare and Medicaid. Higher-income enrollees pay a larger share of the cost of Part D coverage, as they do for Part B.

- The Medicare Advantage program (sometimes referred to as Part C) does not have its own separate revenue sources. Funds for Part A benefits provided by Medicare Advantage plans are drawn from the Medicare HI trust fund. Funds for Part B and Part D benefits are drawn from the Supplementary Medical Insurance (SMI) trust fund. Beneficiaries enrolled in Medicare Advantage plans pay the Part B premium and may pay an additional premium if required by their plan. In 2023, 73% of Medicare Advantage enrollees pay no additional premium.

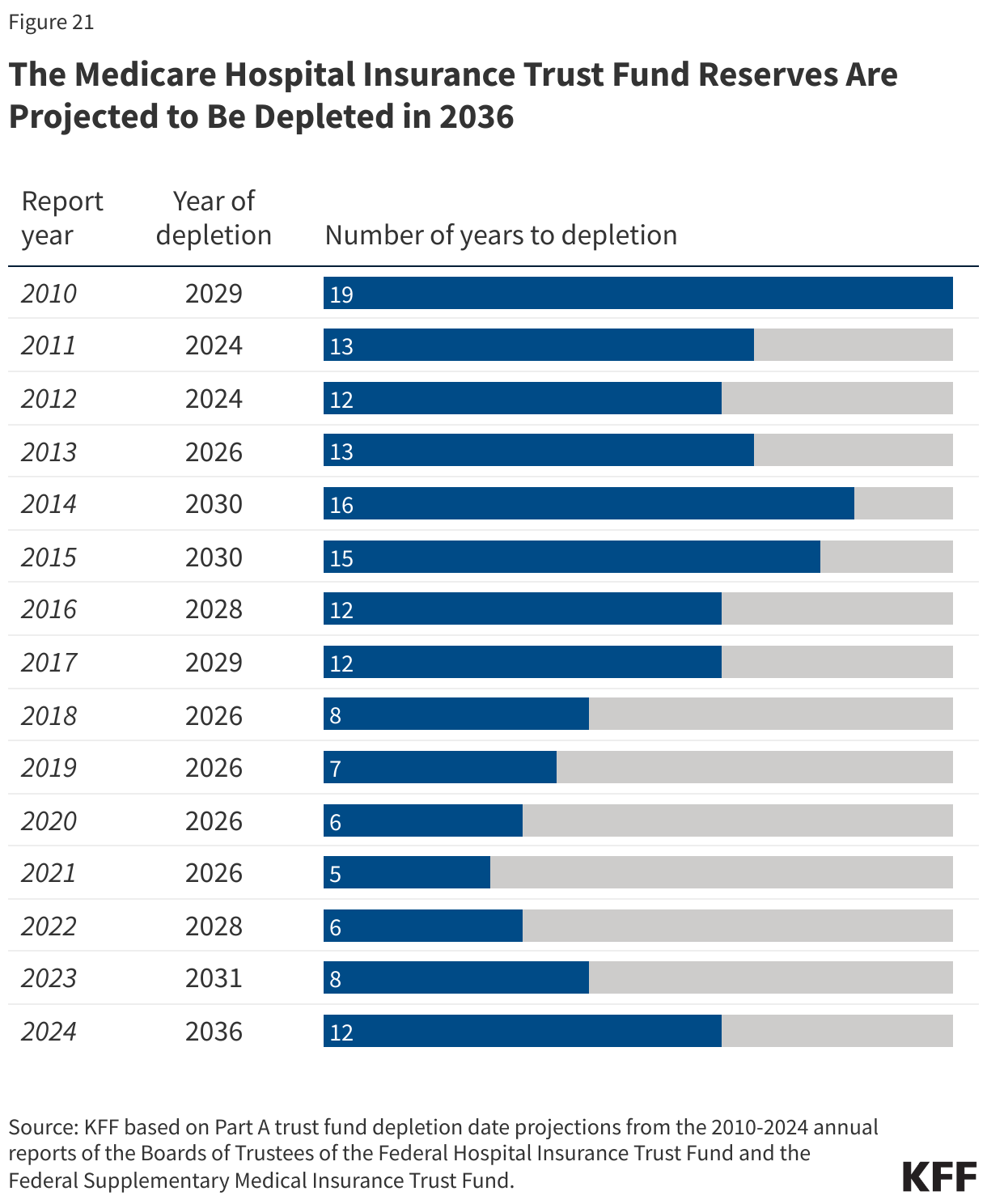

Measuring the level of reserves in the Medicare Hospital Insurance trust fund, out of which Part A benefits are paid, is a common way of measuring Medicare’s financial status. Each year, Medicare’s actuaries provide an estimate of the year when the reserves are projected to be fully depleted. In 2024, the Medicare Trustees projected sufficient funds would be available to pay for Part A benefits in full until 2036, 12 years from now. At that point, in the absence of Congressional action, Medicare will be able to pay 89% of costs covered under Part A using payroll tax revenues. Since 2010, the projected year of trust fund reserve depletion has ranged from 5 years out (in 2021) to 19 years out (in 2010) (Figure 21).

The level of reserves in the Part A Trust Fund is affected by growth in the economy, which affects revenue from payroll tax contributions, health care spending and utilization trends, and demographic trends: an increasing number of beneficiaries as the population ages, especially between 2010 and 2030 when the baby boom generation reaches Medicare eligibility age, and a declining ratio of workers per beneficiary making payroll tax contributions.

Part B and Part D do not have financing challenges similar to Part A, because both are funded by beneficiary premiums and general revenues that are set annually to match expected outlays. However, future increases in spending under Part B and Part D will require increases in general revenue funding and higher premiums paid by beneficiaries.