Employer-sponsored health insurance (ESI) is the largest source of health coverage for non-elderly U.S. residents. Unlike many other nations, the U.S. relies on voluntary, private health insurance as the primary source of coverage for residents who are not elderly, poor or disabled. Providing health insurance through workplaces is an efficient way of offering coverage options to working families, and the tax benefits of employer-based coverage further enhance its attractiveness. Yet, ESI often results in uneven coverage, especially for those with low wages or those working at smaller firms. Overall, 60.4% of people under age 65, or about 164.7 million people, had employment-sponsored health insurance in 2023. The level of coverage varies significantly with income and other factors, even among working families.

The independent source for health policy research, polling, and news.

Employer-Sponsored Health Insurance 101

Published: May 28, 2024

Table of Contents

Introduction

What Is Employer-Sponsored Health Insurance?

There are several ways people get private health insurance. One is by purchasing coverage directly from an insurer, often with the help of an insurance agent or through an online platform such as Healthcare.gov. Income-based premium assistance is available under the Affordable Care Act (ACA). This is called individual or non-group health insurance. The second is coverage under a policy or plan offered by a sponsoring group, such as an employer, union, or trade association. This is called group health insurance. When an individual is sponsored specifically by an employer (or sometimes jointly by one or more employers and a union, or by a group of employers), it is often referred to as employer-sponsored health insurance or ESI.

The word “insurance” is something of a misnomer here. An employer providing health benefits for workers and their families (“plan enrollees”) can fund them in one of two ways. Employers may purchase a health insurance policy from a state-licensed health insurer, which is referred to as an insured plan. Alternatively, the employer can pay for health care for the plan enrollees directly with its own assets, referred to as a self-funded plan. Employers with self-funded plans often protect themselves from unexpected high claim amounts or volume by purchasing a type of insurance referred to as stop-loss coverage. As discussed below, most ESI plan enrollees are covered by large employers, and most large employers self-fund their health benefit plans.

Another confusing set of phrases used in conjunction with health insurance, including ESI, is “health plan” or just “plan.” The terms can refer to an entity offering coverage (e.g. Aetna) or a particular coverage option offered by an insurer or employer (e.g. the PPO plan option). However, the terms “employee benefit plan” and “plan” have specific meanings in federal law and invoke several legal obligations for employers when they offer certain benefits to their workers and their family members. Under the Employee Retirement Income Security Act, or ERISA, an employee benefit plan, or plan, is created when a private employer creates a plan, fund, or program to provide certain benefits, including health benefits, to employees. ERISA creates a structure of disclosure, enforcement and fair dealing regarding the promises made by employers to enrollees in employee benefit plans. However, ERISA does not apply to the health benefit plans created by public plans or churches, although the word plan is often still used to describe benefits offered in these settings.

ESI plans can be differentiated across several dimensions.

Comprehensive or limited benefits

Employers offer different types of health benefit options to employees. These include comprehensive benefit plans, which cover a large share of the cost of hospital, physician, and prescription costs that a family might incur during a year; service-specific benefits, such as dental or vision care plans; and supplemental benefit plans, which may provide a limited additional benefit to enrollees if certain circumstances occur (e.g. $100 per day if hospitalized). The discussion here will be limited to comprehensive benefit plans.

Open or closed provider networks

Health plans contract with hospitals, physicians, pharmacies, and other types of health providers to provide plan enrollees with access to medical care at a predetermined cost. Plan enrollees receiving services from one of these providers know that their financial liability is limited by their deductible and other cost-sharing amounts specified in their benefit plan. A closed-network plan is one where, absent special circumstances, an enrollee is only covered if they receive care from a provider in their plan’s network of contracted providers. In an open-network plan, an enrollee still has some coverage if they receive care from a provider not in the plan network, although they will likely face higher cost sharing under their benefit plan, and the provider may ask them to pay an additional amount (known as balance billing). Health maintenance organization (HMO) and exclusive provider organization (EPO) plans are two types of closed network plans. Preferred provider organization (PPO) and point of service (POS) plans are two types of open network plans.

Small and large group markets

Federal and state laws divide ESI into the small group and the large group market based on the number of full-time equivalent employees (FTEs) working for the employer sponsoring the plan. Federal regulation states that employers with fewer than 50 FTEs are often in the small group market and employers with at least 50 FTEs are in the large group market. However, states have the option to raise the small group market limit to fewer than 100 FTEs. The regulatory requirements for the small and large group markets differ somewhat. Generally, the small group insured market is subject to more extensive rules about benefits and ratings. Large employers are potentially subject to financial penalty under the ACA if they do not offer health insurance coverage meeting certain requirements to their full-time employees.

Are Employers Required to Offer Health Benefits?

The drafters of the ACA intended to provide coverage options to those without access to employer-sponsored coverage without encouraging employers to drop coverage. To achieve this balance, the ACA requires that employers with at least 50 FTEs offer health benefits which meet minimum standards for value and affordability or pay a penalty. The so-called ‘employer mandate’ constitutes two separate penalties.

First, employers are taxed if they do not offer minimum essential coverage to 95% of their full-time employees and their dependent children. This generally requires that employers offer major-medical coverage and not a limited benefit plan. Employers face this penalty when at least one of their employees receives an advance premium tax credit (APTC) to purchase coverage on the health insurance exchange markets or Marketplaces. In 2024, this penalty stipulates that employers will be assessed a tax of $2,970 for each full-time employee after their first 30 employees.

Secondly, employers are penalized if the coverage they offer is not affordable or does not provide minimum value. Plans are considered to meet the minimum value standard if they cover 60% of the health spending of a typical population. In 2023, coverage was deemed to be affordable if the employee premium contribution is less than or equal to 9.12% of their household income. Employers may be charged $3,750 for each employee enrolling on subsidized Marketplace coverage.

Defining what constitutes ‘affordable’ has been the focus of considerable attention in recent years. The Obama Administration initially issued rules that workers and their dependents would be considered to have an affordable offer if self-only coverage met the affordability test. With many employers requiring much larger premium contributions to enroll dependents, this meant that as many as 5.1 million people were in households where they had to pay a larger share of their income to enroll in the plan offered by their employers without being eligible for premium tax credits. Recent rules have addressed the so-called “family glitch” by considering the cost of family coverage when assessing affordability. While most large employers offer health benefits, many may encourage spouses and other dependents to enroll in different plans if possible. For more information on eligibility for premium credits, see the Affordable Care Act chapter.

Why Is Employer-Sponsored Health Insurance So Dominant?

ESI is by far the most common source of private health insurance. There are two primary reasons for this. The first is that providing health insurance through the workplace is efficient, with advantages relating both to risk management and to the costs of administration. The second is that contributions towards premiums by employers and (in most cases) by employees are not subject to income or payroll taxes, providing a substantial federal and state subsidy towards the costs of ESI.

ESI Efficiencies

When people have choices about whether to buy insurance and the amount of coverage to buy, it is natural that people with the highest need for coverage (e.g. people in poorer health) will be more likely to purchase and be more willing to pay higher prices. This is called adverse selection. If insurers do not address these tendencies, their risk pools will become dominated by a relatively small share of people with the highest needs, and premiums will increase to levels that only make sense for those with very high expected costs.

There are several ways insurers seek to manage the risk profile of potential enrollees to avoid adverse selection. One is by examining the health profile of each applicant, which typically includes the applicant’s health history and pre-existing conditions. This strategy is reasonably effective, but an expensive and time-consuming process. A much lower-cost approach is to provide coverage to groups of people who are grouped together for reasons other than their health or their need for health insurance. Providing coverage through the workplace is a common way of doing this. Mostly, people choose a job because of the work, not because they need health insurance. Therefore, providing coverage through workplaces provides insurers with a fairly normal mix of healthy and less healthy enrollees if certain conditions are met. These conditions include enrolling a large share of the eligible workers in coverage (typically achieved by the employer paying a large share of the cost) and limiting the range of coverage options (to avoid adverse selection among plan types). Further, as the number of employees grows, the ability to predict future costs based on prior experience also increases, reducing the uncertainty in setting premiums for the group. As uncertainty decreases, insurers can reduce what they charge for insuring the group. Overall, the same scenario generally applies to situations where employers choose to offer a self-funded plan. Therefore, these advantages occur regardless of whether an insurer or an employer is taking on the risk.

In addition to the risk management advantages, ESI has many administrative advantages. Providing coverage through a workplace adds many employees to a risk pool through a single transaction, with no need to examine their health in most cases. Employers also provide and collect enrollment information to workers and collect the employee share of premiums, dramatically reducing the number of transactions and reducing the amount of unpaid premiums that typically occur when individuals purchase insurance directly from insurers.

Tax Advantages

Federal and state tax systems provide significant tax preferences for ESI. Generally, wages and other things of value employers provide as compensation to their workers are subject to federal and state taxes. The federal government taxes wages and other forms of income through a series of marginal rates that vary with income and the marital and filing status of the taxpayer. For example, the lowest marginal rate in 2022 for a single taxpayer was 10% for income below $10,275 and the highest rate was 37% for income above $539,500. Additionally, wages are subject to federal payroll taxes to support the Social Security and Medicare programs; employers and employees are each assessed 6.2% of wages up to a maximum wage for Social Security and 1.45% of wages with no wage limit for Medicare. Wages are also subject to state income and payroll taxes for unemployment, which vary considerably.

Unlike wages, ESI provided by employers as part of their compensation to employees is not considered income under the federal income tax code, nor are they considered wages subject to federal payroll taxes (See 26 USC sections 105 and 106). Federal law also permits employers to establish programs that exclude employee contributions towards ESI from these taxes. These exclusions lower the cost of health insurance for employees. For example, just considering the federal tax advantages, if an employee earns annual wages of $100,000, an employer can provide the employee with a $20,000 family policy for an additional $20,000 in compensation. However, if ESI were subject to federal taxes, that same employee would need to earn an additional $27,460 in wages to be able to buy a $20,000 family policy with after-tax dollars, assuming a 22% marginal federal income tax rate and a combined 15.3% payroll tax for Social Security and Medicare. Looked at another way, for this employee, for every dollar that the employer raises the employee’s compensation, the employee can get a dollar of health benefits or just under 63 cents in wages after taxes. State tax laws, which follow federal definitions of income and wages in this situation, further lower the cost of ESI for workers, although the impacts are much smaller.

The exclusion of ESI from federal income tax is a long-standing and somewhat controversial part of federal tax policy, first appearing due to a decision by the War Labor Board in 1942, which in turn allowed employers to use fringe benefits to attract workers during the war. In 1954, ESI exclusion was enacted in the tax code. This tax policy, combined with the risk management and administrative advantages of group coverage, contributed to the rapid growth and continued market dominance of commercial hospital and medical insurance during this period. Detractors of the tax exclusion have argued that it encourages workers to over-consume health insurance by demanding health benefits that are richer than what they would want under a tax-neutral approach (e.g. if health benefits were taxed in the same way as wages). Richer benefits, it is argued, contribute to higher health care costs because people with better insurance use more health care than they otherwise would since they are not facing the actual costs of care (sometimes called moral hazard). Another criticism is that the income tax exclusion favors higher-paid employees because they have higher marginal tax rates: the effective income tax benefit for a dollar of ESI is only 10 cents for a worker with very low wages but can be up to 37 cents for those with the highest wages. In contrast, the exclusion of health benefits from payroll taxes has the same dollar benefit for workers at all wage levels (up to the Social Security earning limit), which results in a higher percentage exclusion (share of wages) for those with lower wages. The tax exclusion was estimated to cost the federal government $273 billion (about $840 per person in the US) in income and payroll taxes in 2019.

Who Is Covered by Employer-Sponsored Health Insurance?

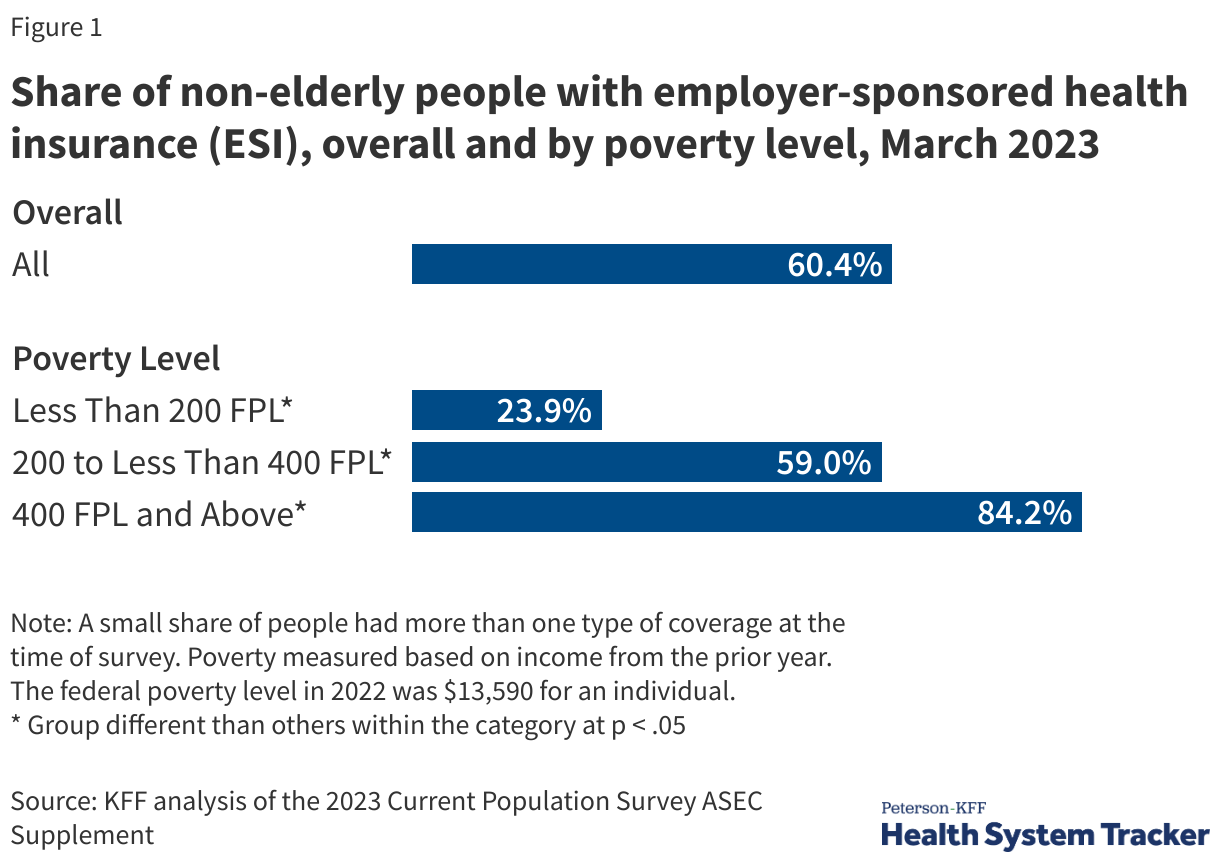

As of March 2023, 60.4% of the non-elderly, or about 164.7 million people, had ESI. Of these, 84.2 million had ESI from their own job, 73.8 million were covered as a dependent by someone within their household, and 6.7 million were covered as a dependent by someone outside of their household.

A relatively small share of these people also held other coverage at that time: 3.2% were also covered by Medicaid or other public coverage and 0.6% were also covered by non-group coverage.

ESI coverage varies dramatically with income. In March 2023, more than 4 in 5 (84.2%) non-elderly adults with incomes at least 400% of the federal poverty level (FPL) had ESI, compared to 59.0% with incomes between 200% and 399% of the FPL and 23.9% with incomes below 200% of the FPL.

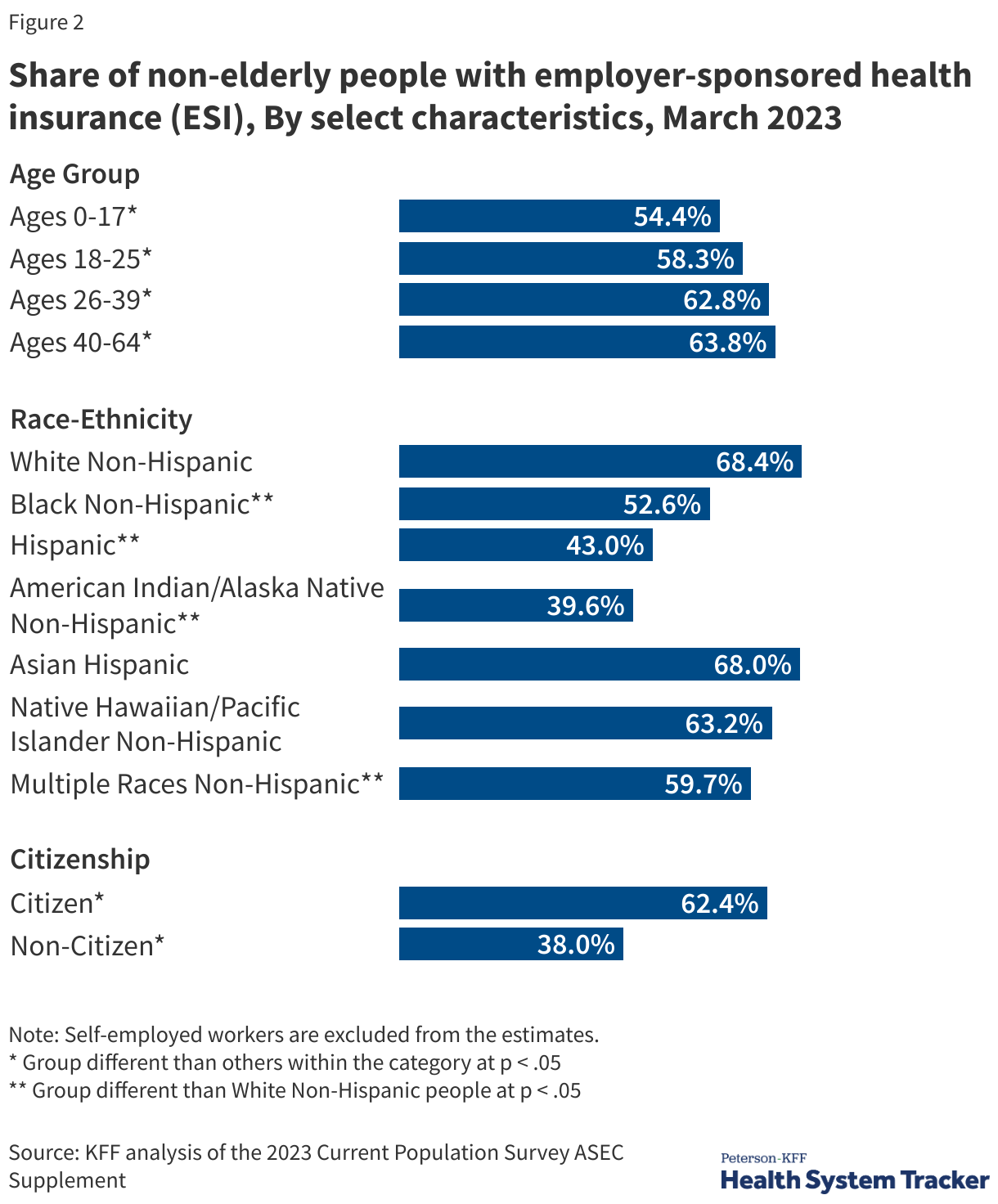

ESI also varies with age, as well as other worker characteristics. Among non-elderly people in March of 2023, people in younger age groups were less likely than those in older age groups to have ESI, and U.S. citizens were much more likely than non-citizens to have ESI. ESI coverage also varied across race and ethnic categories: compared to non-Hispanic White people, Hispanic people and non-Hispanic people who are Black, American Indian or Alaskan Native, or of mixed race were less likely to have ESI.

How Many Workers Have Access to Employer-Sponsored Health Insurance at Their Job?

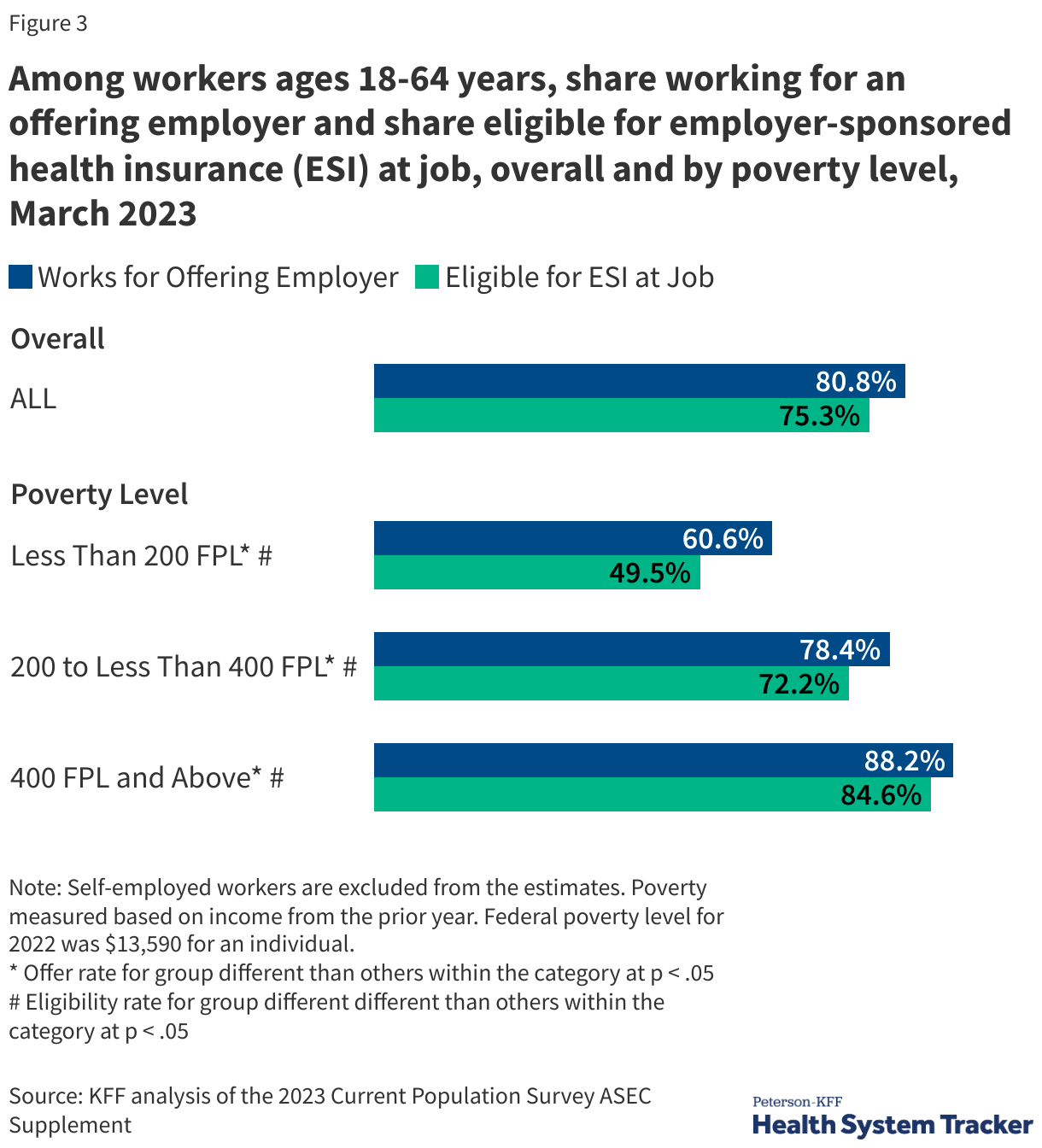

For people in working families to have ESI, one or more workers must work for an employer that makes coverage available to them. For workers to access ESI, they need to work for an employer that offers ESI and be eligible to enroll in coverage offered at their job. About four in five (80.8%) adult non-elderly workers worked for an employer that offered ESI to at least some employees as of March 2023. Most (93.1%) of these workers were eligible for the ESI offered at their job. Overall, in 2023, about 3 in 4 of all workers were eligible to enroll in the ESI offered at their job.

Both the share of workers working for employers offering coverage and the share of workers eligible for coverage at their jobs varies significantly by income. Among adult non-elderly workers, the share working for an employer offering ESI ranged from 60.6% for workers with incomes under 200% of the FPL to 88.2% for workers with incomes at least 400% of the FPL. Similarly, the share eligible for coverage ranged from 49.5% for workers with incomes under 200% of the FPL to 84.6% for workers with incomes of at least 400% of the FPL.

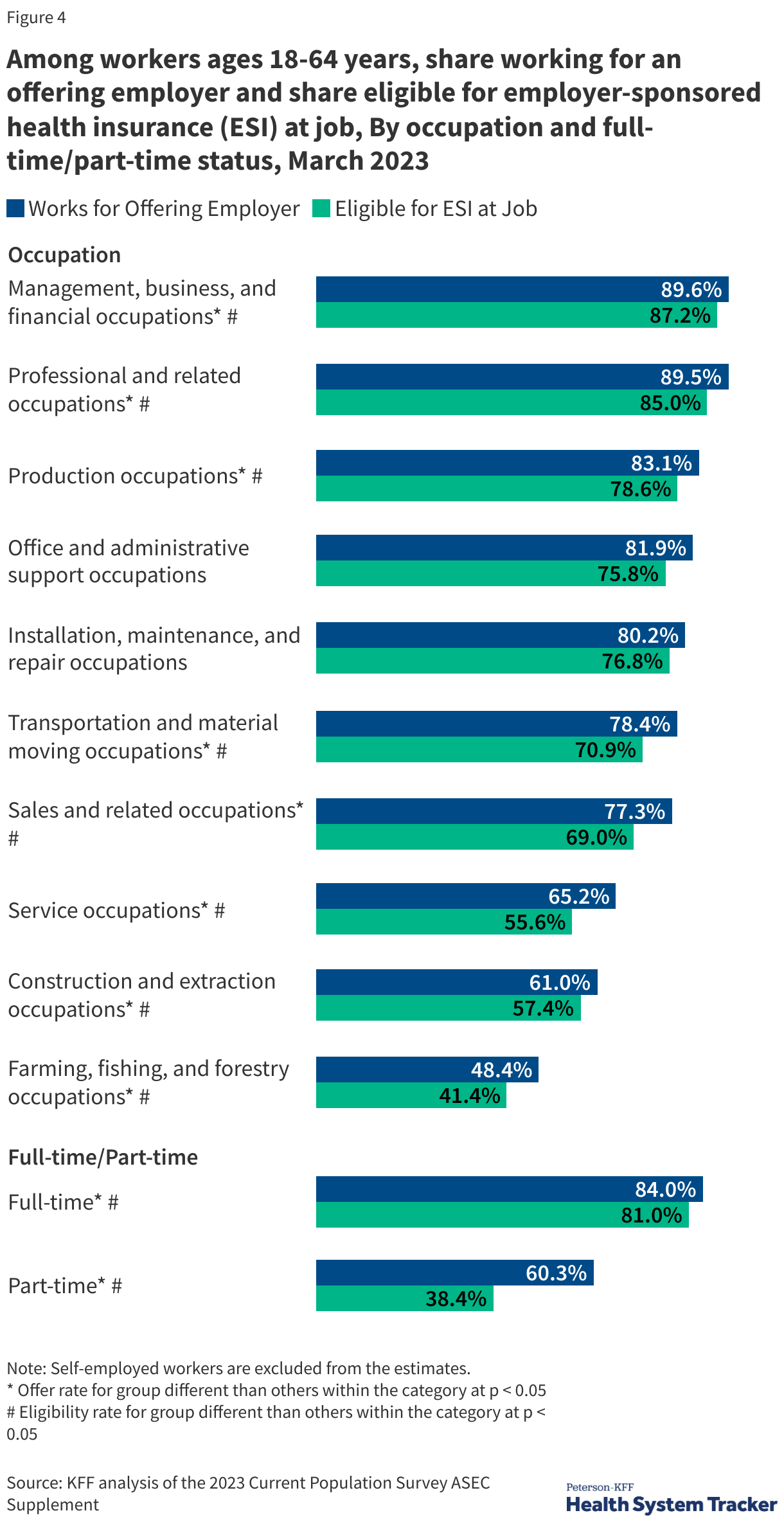

Working for an offering employer and being eligible for the offered coverage is dependent on a combination of characteristics. As of March of 2023, non-elderly workers working in construction, service, sales, and farm, fishing and forestry-related occupations were less likely to be working for an employer offering ESI and to be eligible for ESI at their jobs. Full-time workers were much more likely to be working for an employer offering ESI and to qualify for coverage at their job. There also was significant variation in offer rates and eligibility within sex, age group, race and ethnicity, and citizenship.

How Many Workers Take Employer-Sponsored Health Insurance Available at Their Job?

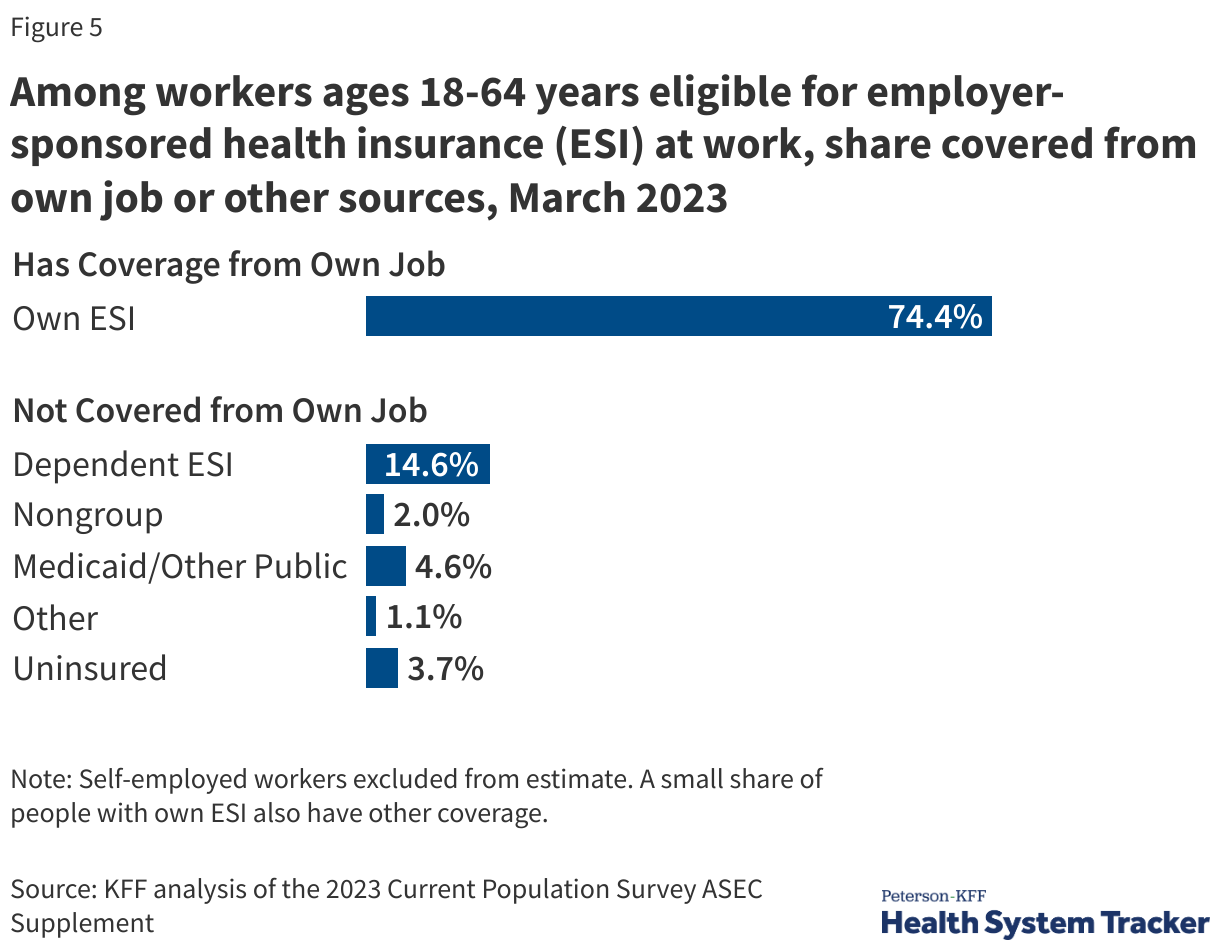

Among non-elderly adult workers eligible for ESI at their jobs in March 2023, 74.4% were ESI policyholders. Of those who did not have ESI from their own job, 14.6% were covered by ESI as a dependent, 4.6% had Medicaid or other public coverage, 2.0% had non-group coverage, 1.1% had some other coverage, and 3.7% were uninsured. A small share of workers with ESI from their job also had other coverage at the same time: 2.4% also had Medicaid or other public coverage and 0.6% also had non-group coverage.

What Share of Employers Offer Health Benefits to Their Workers?

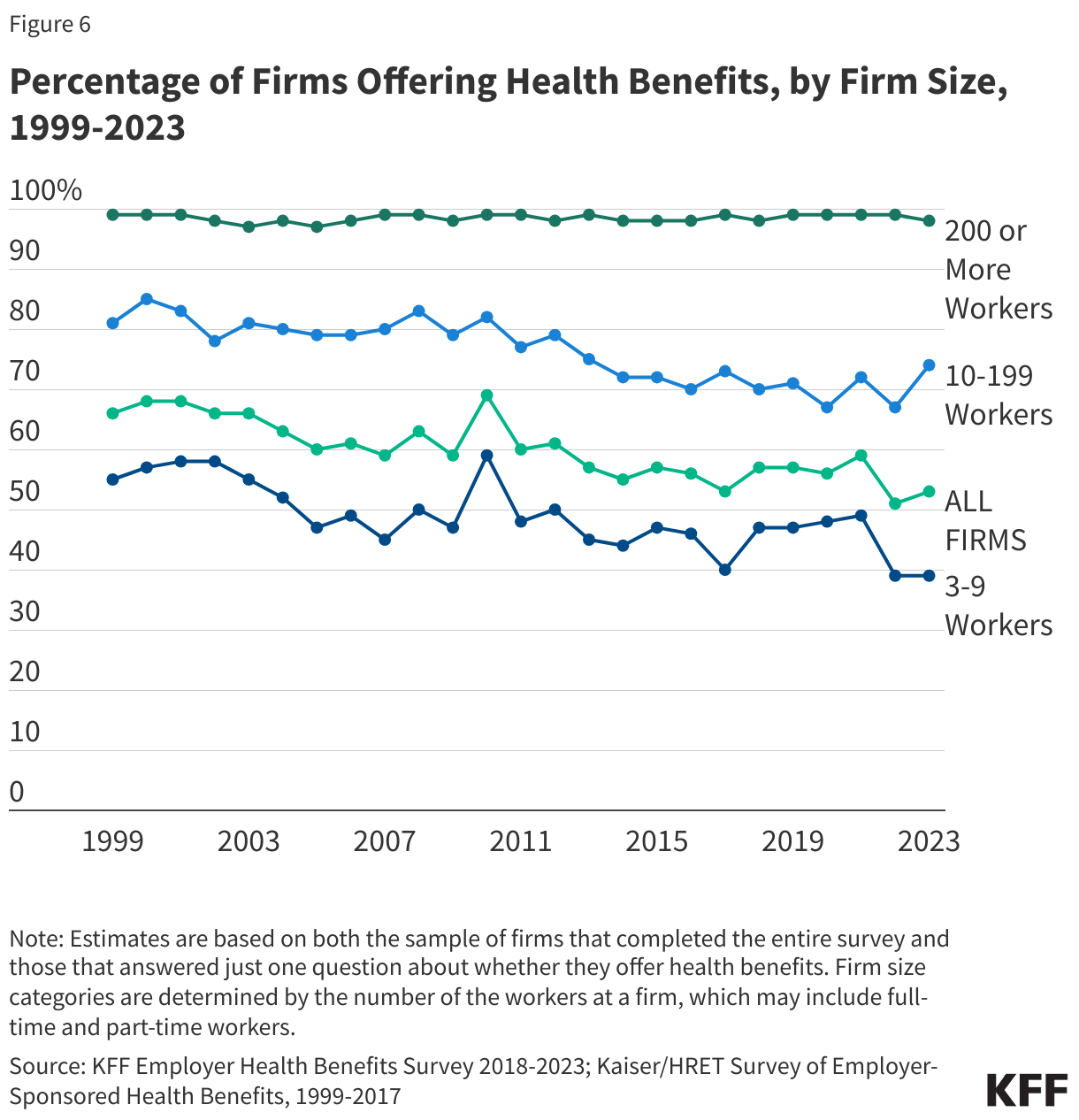

Among firms with three or more workers, just over half (53%) offered health benefits to at least some of their workers in 2023. Firm offer rates differed significantly with firm size. Only 39% of firms with three to nine workers offered health benefits, while virtually all (98%) firms with at least 200 employees did so. While a large majority of firms are small, 83% of firms with three or more employees have fewer than 25 employees, and these firms employ just 16% of workers. Sixty-four percent of workers work for firms with 200 or more employees, where the employer offer rate is almost 100%.

Among firms offering health benefits, 13% of firms with fewer than 200 workers and 26% of larger firms offered health benefits to part-time workers in 2023.

Ninety-five percent of firms offering health benefits offered them to dependents (e.g. spouses and children) of their workers. In 2023, among firms with 200 or more workers offering health benefits, 32% offered benefits to opposite-sex domestic partners and 38% offered benefits to same-sex domestic partners. Many small firms reported that they had not encountered this issue or that they did not know.

What Are the Premiums for Employer-Sponsored Health Insurance?

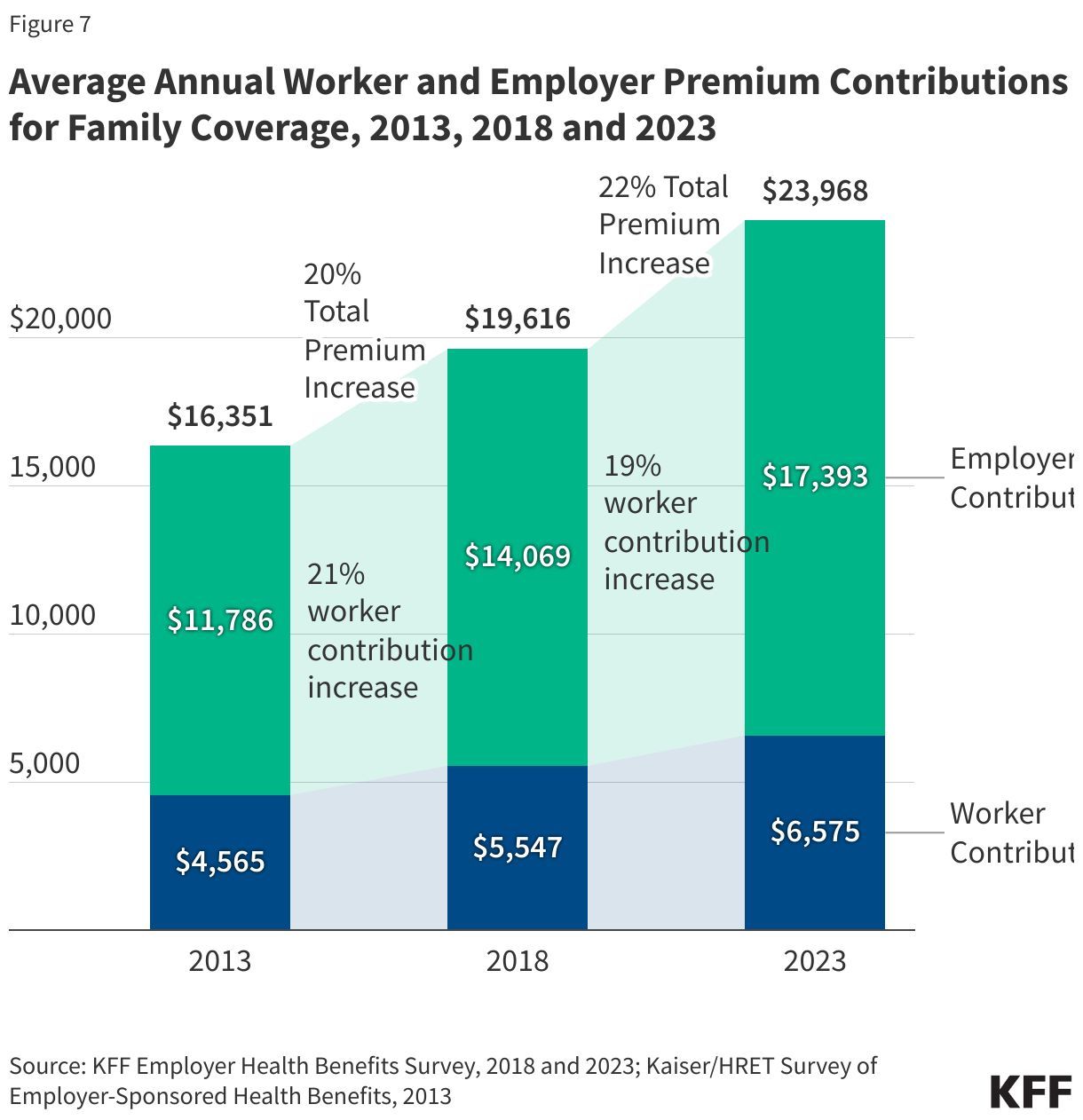

Employer health insurance premiums are the total of what employers and employees pay to providers for health coverage through employment. Generally, premiums are the estimated cost of health spending for the covered population, as well as the administrative costs and fees associated with the plan. Therefore, premiums usually increase when a covered population either uses more health services or the prices for health care increase. In 2023, the average total premiums for covered workers were $8,435 for single coverage and $23,968 for family coverage (for a family of four). Employer contributions to an employee’s health insurance premium are a sizeable share of an employee’s overall compensation (6.9% for private industry as of June 2023).

Premiums varied around these averages due to factors such as the age and the health of the workforce, the cost of the providers included in the network, and the generosity of the coverage. In 2023, 10% of covered workers worked at a firm with an average annual premium of at least $31,500 for family coverage. The robustness of plan offerings varies across firms, with some employers offering generous benefits to attract new employees, while others prioritize more affordable plan options. Some employers sponsor limited-benefit plans, which may cover a limited number of services but have lower costs. The average family premium for covered workers at firms with a relatively large share of lower-wage workers (firms where at least 35% of the workers earn $31,000 annually or less) is lower than at firms with fewer lower wage workers. On the other hand, the average premiums for single and family coverage are relatively higher in the Northeast, in private not-for-profit firms, and in firms with a large share of older workers. There is additional discussion of how premiums vary with firm characteristics here.

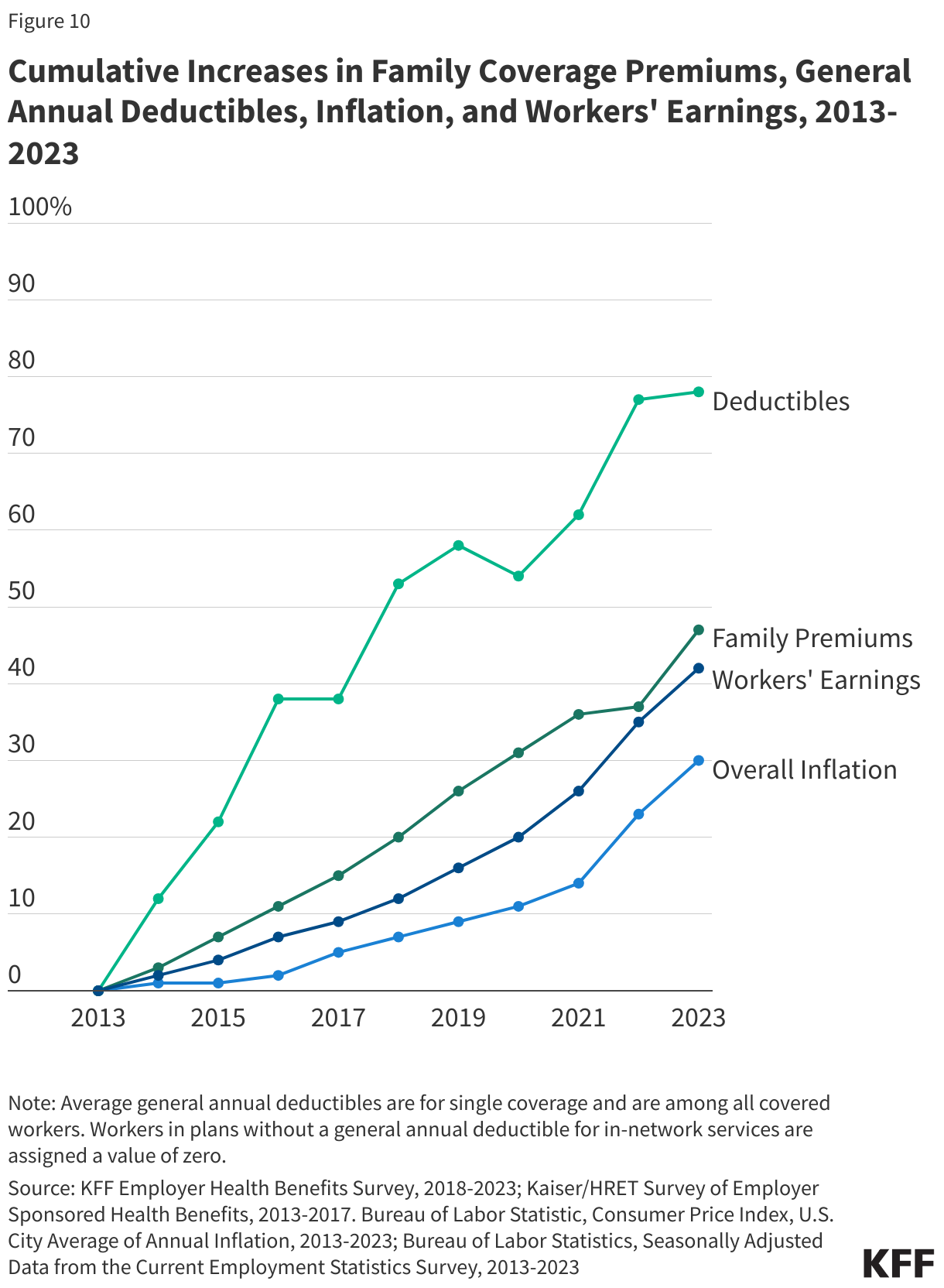

During the late 1990’s and early 2000’s health insurance premiums grew at a rate considerably faster than inflation and workers’ wages. Recently, the rate of growth has moderated. For example, over the last five years, family premiums have grown 22%, roughly comparable to the rate of inflation (21%) and the change in wages (27%). When faced with higher premium costs employers can adjust their plan offerings, increase cost sharing, drop high-cost providers, or change how benefits are covered in other ways.

How Much Do Workers Contribute Towards the Premiums for Employer-Sponsored Health Insurance?

Workers contribute to health insurance in two ways. First through a premium contribution, which is typically deducted from an employees’ paycheck. Then, secondly, through cost sharing such as copays, coinsurance, and/or deductibles, which are paid when the employee utilizes services covered by their plan. While all workers enrolled in the plan must pay their premium (or have it paid by the employer), overall cost sharing is higher for workers who use more services.

Workers with health coverage in 2023, on average, were responsible for 17% of the premium for single coverage and 29% of the premium for family coverage. In dollar terms, the average annual contribution for covered workers was $1,401 for single coverage and $6,575 for family coverage.

Over time, the average premium contribution for covered workers has increased. For example, over the last 10 years, the single coverage average contribution has increased 40% and the family coverage average contribution has increased 44%. At the same time, the share of the premium paid for by workers has remained relatively consistent. In 2023, covered workers contributed, on average, 17% of the premium for single coverage and 29% of the premium for family coverage, which was similar to these averages a decade ago. This is because as premiums have increased over time, both employers and employees have faced similar increases on average.

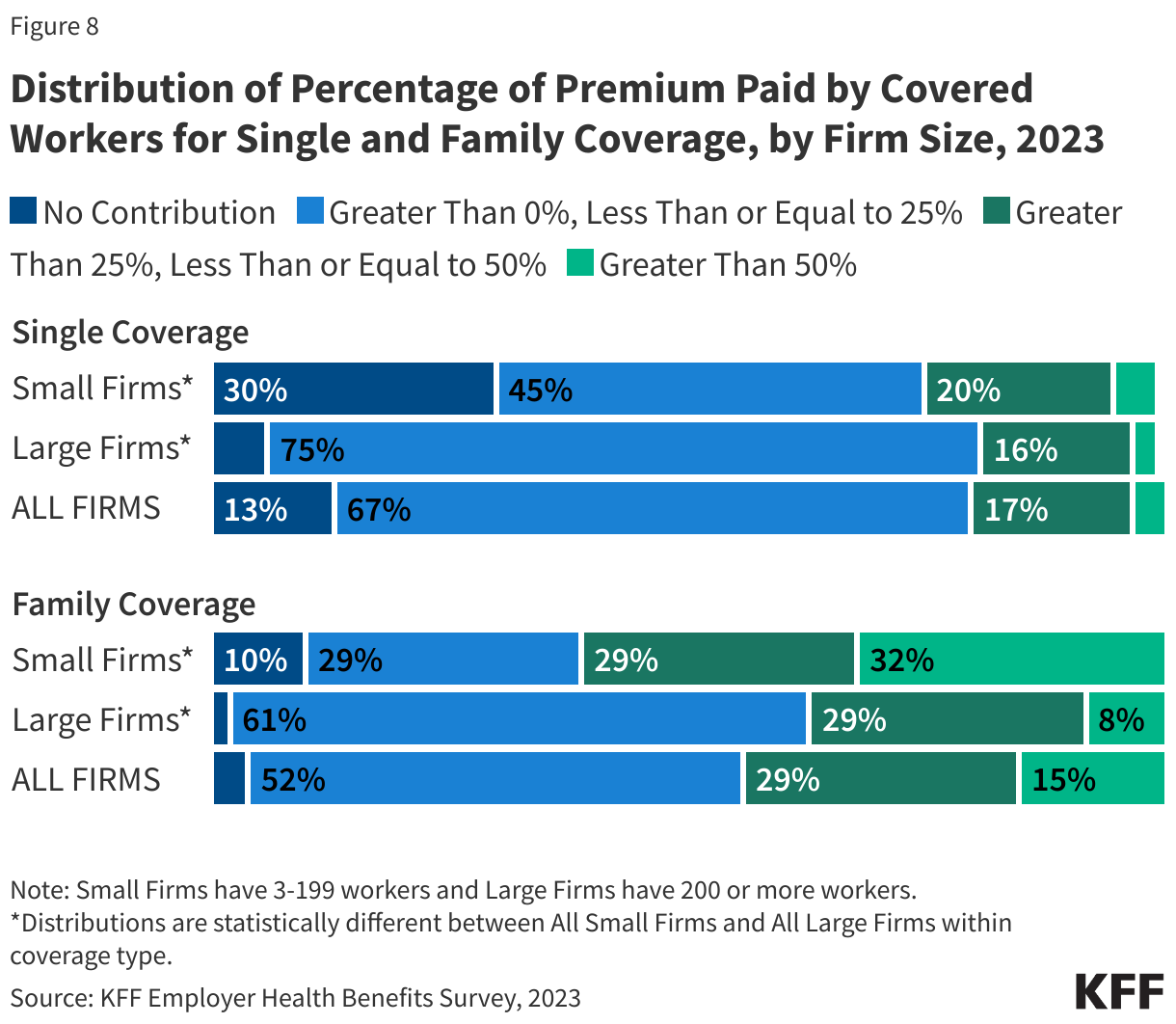

There remains a lot of variation in how much workers are required to contribute to their health plan across firms, particularly within firm size. In 2023, 30% of covered workers at small firms were enrolled in a plan where the employer paid the entire premium for single coverage. This was only the case for 6% of covered workers at large firms. However, 32% of covered workers at small firms were in a plan where they must contribute more than half of the premium for family coverage, compared to 8% of covered workers at large firms. The average family contribution rate for covered workers in firms with fewer than 200 employees was 38%, which is higher than the average contribution rate of 25% for covered workers in larger firms. Small firms often approach the cost of health insurance differently than large firms, sometimes making the same employer contribution regardless of whether the employee enrolls any dependents. Similarly, some large employers encourage spouses and dependents to enroll in other plans, if they have access, through spousal surcharges.

In addition to any required premium contributions, most covered workers must pay a share of the cost of the medical services they use. The most common forms of cost sharing are deductibles (an amount that must be paid before most services are covered by the plan), copayments (fixed dollar amounts), and coinsurance (a percentage of the charge for services). Some plans combine cost sharing forms, such as requiring coinsurance for a service up to a maximum amount or requiring either coinsurance or a copayment for a service, whichever is higher. The type and level of cost sharing may vary with the kind of plan in which the worker is enrolled. Cost sharing may also vary by the type of service, with separate classifications for office visits, hospitalizations, and prescription drugs. Plans often structure their cost sharing to encourage enrollees to reflect on their use, reducing overall utilization.

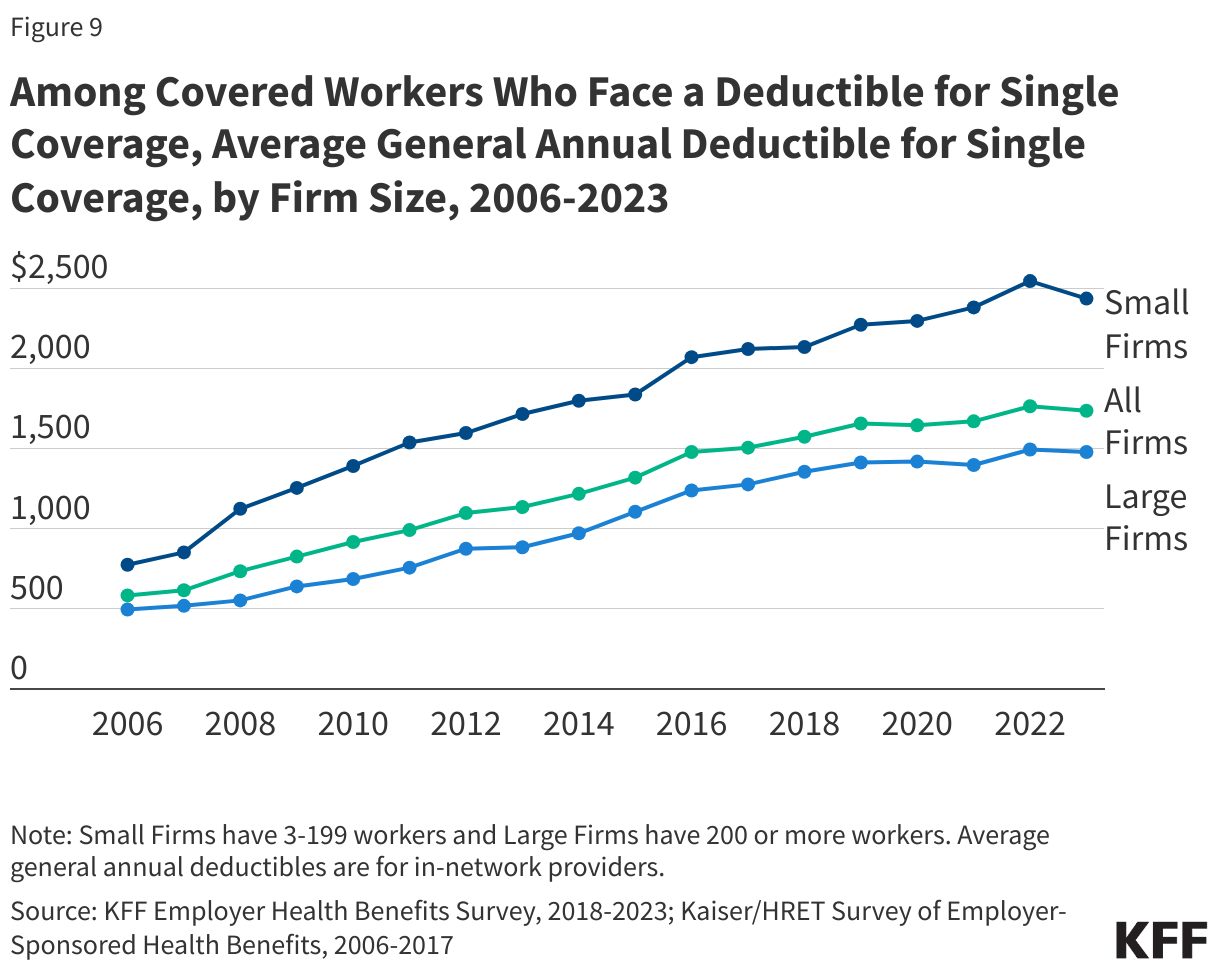

In recent years, general annual deductibles have grown in prominence in plan design. In 2023, 90% of covered workers were enrolled in a health plan which required that an enrollee met a deductible before the plan covered most services. The average deductible amount as of 2023 for workers with single coverage and a general annual deductible was $1,735. On average, covered workers at smaller firms face higher deductibles than those at large firms ($2,434 vs. $1,478). Generally, a substantial share of workers faced relatively high deductibles. Forty-seven percent of workers at small firms and 25% of workers at large firms had a general annual deductible of $2,000 or more. Over the last five years, the percentage of covered workers with a general annual deductible of $2,000 or more for single coverage has grown from 26% to 31%.

While average deductibles have not grown over the last few years, the growth over the last ten years outpaces increases in premiums, wages, and inflation. The rise in deductible costs has focused attention on consumerism in health care. Some believe that increasing deductibles will place a greater incentive on enrollees to shop for services, therefore reducing total plan spending. Alternatively, deductibles are less common in Health Maintenance Organization (HMO) plans, which use forms of gatekeeping to dissuade utilization. The growth of deductibles has had important consequences for the financial protection that health insurance provides. A multitude of plans require deductibles well in excess of the financial assets of many of their enrollees. As opposed to coinsurances and copays that accumulate throughout the year, deductible spending may require enrollees to finance relatively high expenses all at once.

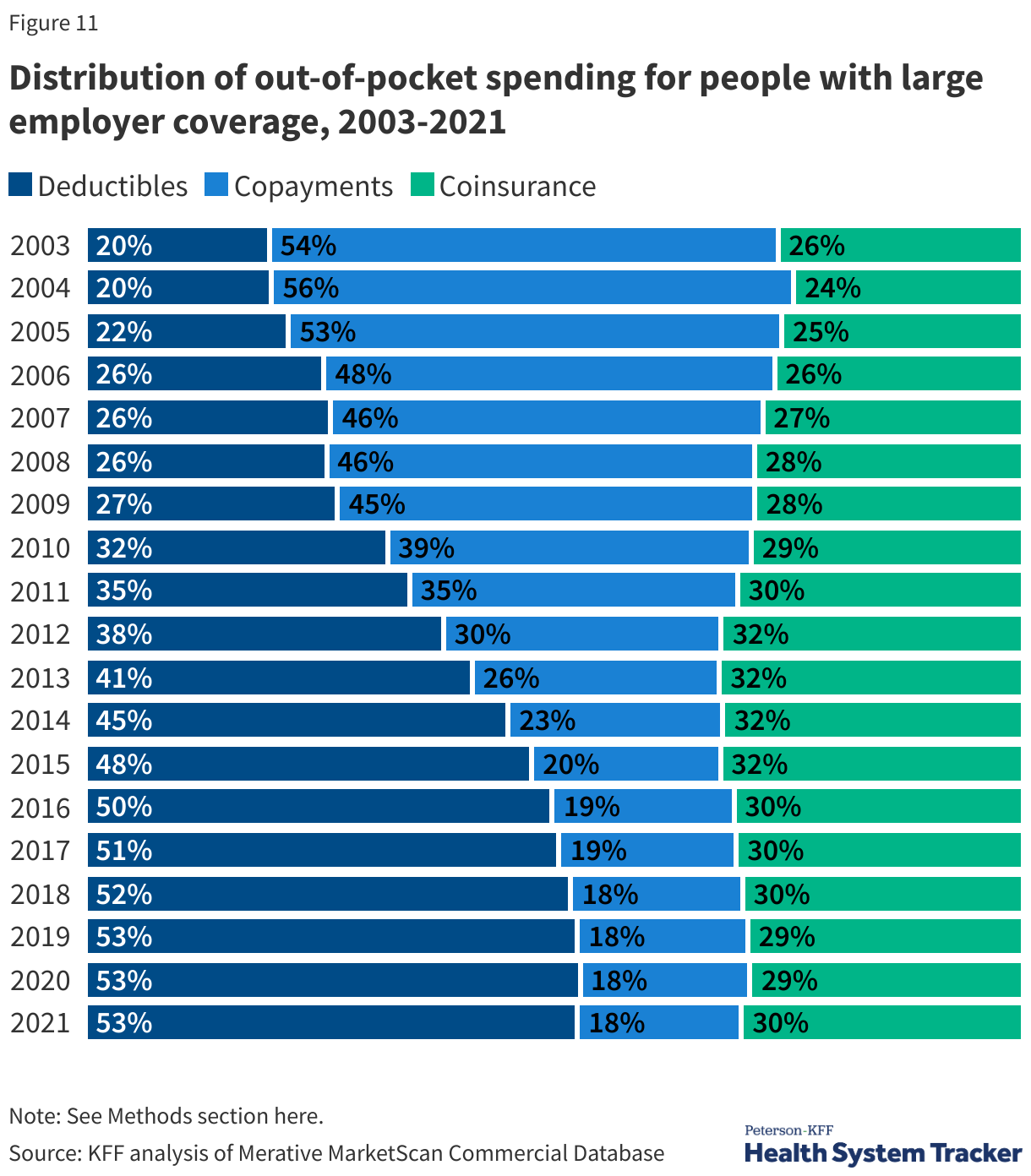

In addition to looking at the average obligations enrollees face under their health plan, we can look at the actual spending incurred by enrollees in large group plans. In 2021, deductibles accounted for more than 53% of an enrollee’s cost-sharing liability, which is significantly greater than 35% of enrollee liability ten years ago.

The amount of cost sharing large group enrollees face varies, particularly around how many health services a person uses. Individuals who have a hospitalization or a chronic condition which requires ongoing management often incur higher cost sharing over the year. For example, large group enrollees faced an average of $779 in cost sharing, but individuals with a diabetes diagnosis (even without complications) incurred costs of $1,585 in 2017.

While some employer health plans have relatively generous benefits, there remains a concern about affordability, particularly for lower-wage workers who do not have the assets to meet the cost sharing required under their plan, as well as for individuals enrolling in family coverage at smaller firms. Overall, individuals in families with employer coverage spend 2.7% of their income on the worker contribution required to enroll in an employer-sponsored health plan, and another 1.3% of their income on typical out-of-pocket spending on cost sharing. Individuals covered by employer-sponsored plans in households at or below 199% of the FPL contribute over 10% of their income on average towards their premiums and cost sharing.

A key component of plan design is the out-of-pocket maximum, which caps the amount of money an enrollee spends on in-network covered benefits within a year.

The ACA requires that almost all plans have an out-of-pocket (OOP) maximum below a federal determined limit. In 2023, 13% of covered workers in plans with an OOP maximum had an OOP maximum of less than $2,000 for single coverage, while 21% of these workers had an OOP maximum above $6,000.

What Types of Employer-Sponsored Health Insurance Plans Do Workers Have?

Today virtually all plans have preferential cost sharing for enrollees to visit providers participating in a preferred provider network. Some plans require enrollees to visit a primary care physician or other gatekeeper before they are referred to a specialist. Plans are often categorized based on these characteristics.

Preferred Provider Organization (PPO)

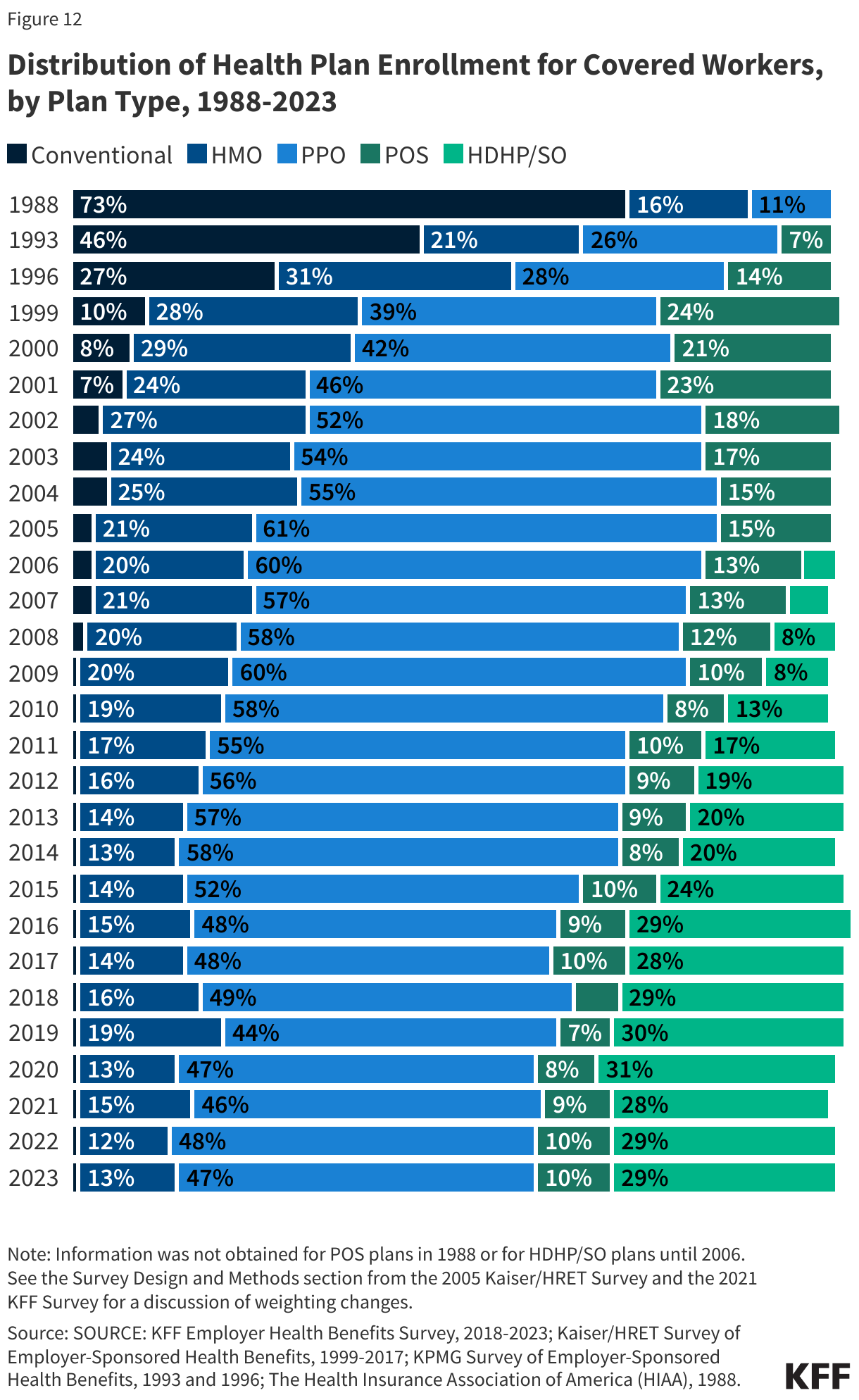

PPO plans are the most common plan type. These plans typically have broader provider networks and do not require gatekeeping for specialist services. However, insurers may still use utilization management tools, such as prior authorization, to determine appropriate use and which services will be paid for under the plan. Point-of-service (POS) plans have a provider network like a PPO plan but require gatekeeping for referrals. POS plans are more common in the Northeast and among smaller firms.

Health Maintenance Organization (HMO)

HMO plans represent 13% of covered workers. HMO enrollment has decreased over the past few decades, compared to nearly 3 in 10 workers who were enrolled in HMOs in the late 1990s. HMOs do not cover non-emergency out-of-network services, and some integrate health care financing and services delivery. Since providers in these plans are not paid on a fee-for-service basis, they are designed to encourage lower utilization to reduce costs.

High Deductible Health Plan with a Savings Option (HDHP-SO)

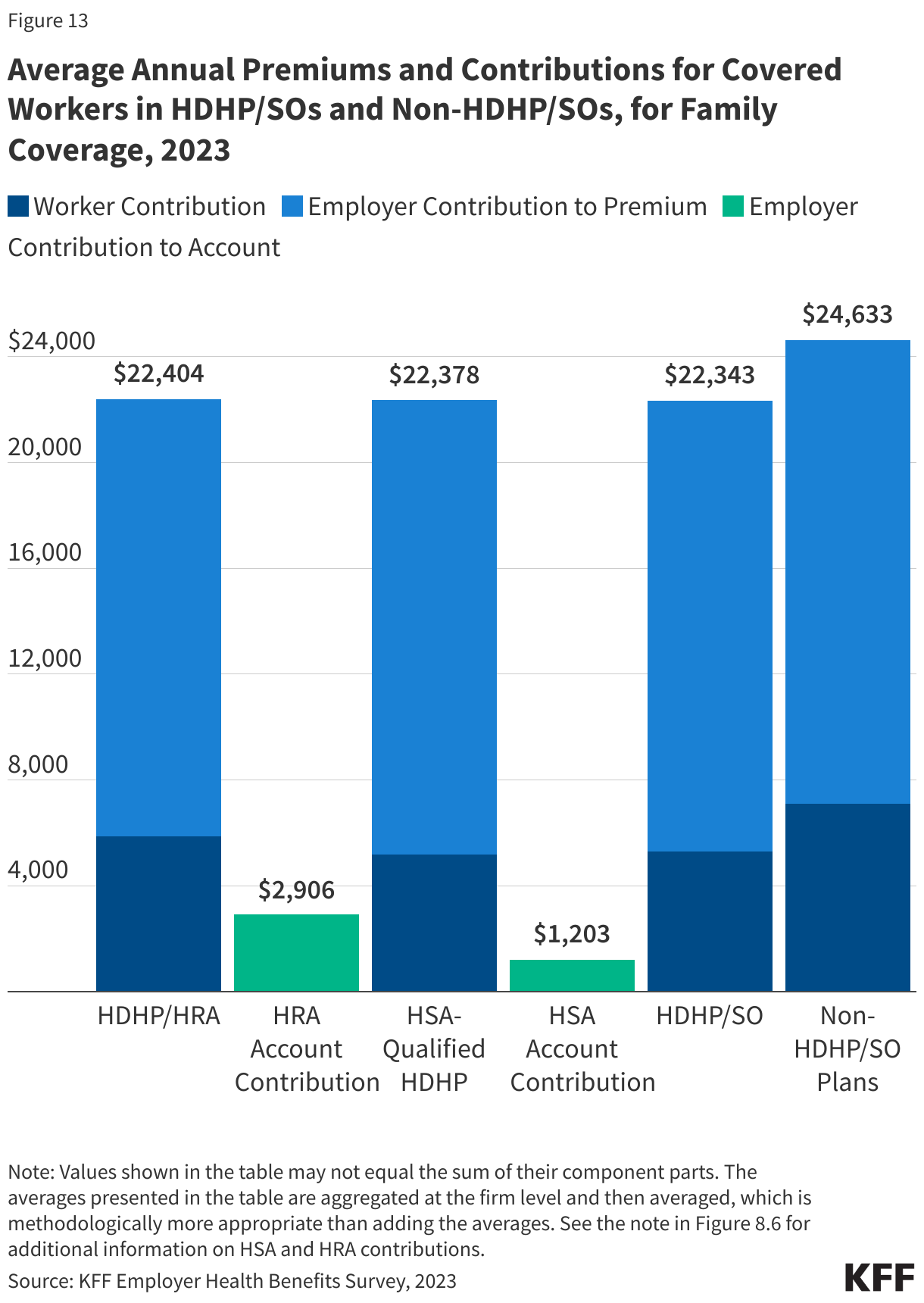

HDHP-SO is a relatively new plan type. This plan pairs a high deductible with either a Health Reimbursement Arrangement (HRA) or Health Savings Account (HSA). HSA-qualified plans were first authorized in the Medicare Modernization Act of 2003 and grew precipitously until 2015. HDHP-SO plans now represent almost 3 in 10 covered workers, including almost a quarter enrolled in an HSA-qualified plan. These plans may be an HMO, PPO, or POS, meeting specified federal guidelines. HSA-qualified plans allow both employers and enrollees to contribute to a tax-preferred savings account, which enrollees can use to meet their cost-sharing requirements or save for future health spending. On average, HSA-qualified health plans have higher deductibles than other plan types and lower premiums. The growing enrollment in HSA-qualified plans has led to a growth in general annual deductibles overall. While having a higher deductible in other plan types generally increases enrollee out-of-pocket liability, this is not necessarily true for HDHP-SO plans. Many HDHP-SO enrollees receive an account contribution from their employers, reducing the higher cost sharing in these plans. Sixty-two percent of employers offering single coverage and 59% of employers offering family coverage, as well as an HSA-qualified health plan, contribute to the enrollee’s account. On average, employers contribute $657 to single-coverage HSA-qualified HDHPs, and $1,203 to family-coverage HSA-qualified HDHPs. Some employers may make their account contribution contingent on other factors, such as completing wellness programs.

What Types of Network Strategies Do Employer-Sponsored Health Insurance Plans Use?

Employer plans typically include provider networks, in which enrollees face lower out-of-pocket expenses if they receive care from a designated provider. Firms and health plans structure their networks of providers to ensure access to care and encourage enrollees to use providers who are lower cost or who provide better care. Employees generally prefer broad network plans, and job-based plans are typically broader than those offered on the Marketplaces. Even so, some employers offer a health plan with a relatively small network of providers. These narrow network plans limit the number of providers that can participate to reduce costs and are more restrictive than standard HMO networks. In 2023, 9% percent of firms offering health benefits reported that they offer at least one narrow network plan to their employees.

More frequently, firms use tiered or high-performance networks in which providers are selected and then grouped within the network based on the quality, cost, and/or efficiency of care they deliver. Enrollees then receive lower cost sharing by choosing a provider in a lower tier.

Another way plans designate preferred providers is through “Centers of Excellence,” which are facilities or providers that health plans and employers single out as suppliers of exceptionally high-value specialty care for specific conditions. Plans and employers may encourage or require enrollees to use these designated providers to receive coverage for certain types of care.

As major purchasers of health care, many view employers as having considerable leverage in health care markets based on their network design. This leverage is dampened by a combination of factors, including the prevalence of highly concentrated provider markets, employees’ preferences for broad network plans, and the challenges of building networks capable of delivering timely access.

One specific concern is the availability of mental health providers. In 2023, most firms (91%) reported that they believed their largest plan offered timely access to primary care providers. However, only 67% of firms believed there were enough mental health providers in their largest plan’s network to provide timely access to services. As plan costs continue to rise for employers, these networks may be further limited as high-cost providers are removed to mitigate costs.

Future Outlook

While ESI seems likely to remain the dominant source of health insurance for working families, employers and working families each face challenges relating to affordability and access to care. These include:

Ultimately, health care is expensive, and the cost of good ESI coverage can place a strain on employers and employees, particularly for workers with lower wages. Additionally, only about half of workers with incomes below 200% of the FPL are even eligible for ESI at their workplace. Can ESI be a source of affordable coverage for all working families, or are novel approaches to providing affordable coverage options needed for these families?

Many ESI policies have significant deductibles and other out-of-pocket costs to keep the premium costs down, while increasing the cost of obtaining care for enrollees. Can and will employers continue to increase out-of-pocket costs, and, if not, how will they control the costs of ESI going forward?

What avenues are available to employers to increase access to care for people with mental health and substance use care needs? Is telehealth a sufficient response?

Can employers and health plans develop provider networks that provide quality health care at lower costs?

Resources

- 2023 Employer Health Benefits Survey

- 2023 Employer Health Benefits Chart Pack

- Long-Term Trends in Employer-Based Coverage – Peterson-KFF Health System Tracker

- Long-Term Trends in Employer-Based Coverage

- Many Workers, Particularly at Small Firms, Face High Premiums to Enroll in Family Coverage, Leaving Many in the ‘Family Glitch’

- How many people have enough money to afford private insurance cost sharing?

- The burden of medical debt in the United States

- How affordability of employer coverage varies by family income

- Increases in cost-sharing payments continue to outpace wage growth

- What do we know about people with high out-of-pocket health spending?

- Preventive services use among people with private insurance coverage

- Many Workers, Particularly at Small Firms, Face High Premiums to Enroll in Family Coverage, Leaving Many in the ‘Family Glitch’

- Out-of-pocket spending on insulin among people with private insurance

- Employer Responsibility Under the Affordable Care Act

Citation

Claxton, G., Rae, M., & Winger, A., Employer-Sponsored Health Insurance 101. In Altman, Drew (Editor), Health Policy 101, (KFF, May 28, 2024) https://www.kff.org/health-policy-101-employer-sponsored-health-insurance/ (date accessed).