What resources are available for privately insured patients who get surprise balance bills?

For privately insured patients, surprise medical bills can arise from either having to pay a high deductible, or from “balance billing.” Typically, health plans negotiate payments to in-network providers. Out-of-network providers may directly bill privately insured patients the difference between the typical in-network health plan payment and the full charge, also known as “balance bills”. In these cases, patients can be liable for the balance bill in addition to any deductible, coinsurance, or copay under the health plan.

The No Surprises Act prohibits many of these balance bills starting in 2022. Privately insured patients (including those with employer-based coverage, non-group plans, and grandfathered plans) are protected from certain surprise balance bills. The surprise balance billing protections require private health plans to cover out-of-network claims and apply in-network cost sharing (deductibles, copayments) for certain covered benefits. The law prohibits certain providers, hospitals, and air ambulance from surprise balance billing patients for out-of-network care, unless the patient consents ahead of time.

The new protections require plans and providers to take the patients out of many of the most common payment disputes. Though it is possible that patients still get balance bills, including because of plan or provider billing mistakes, the bill is not covered under the new law (for example, ground ambulance rides, non-covered services, patient consents to out-of-network care costs), or the health plan denies the claim completely as not covered by the plan.

The patient might get balanced bills, for instance, if the patient’s plan incorrectly processes a claim or applies out-of-network cost-sharing amount when the NSA prohibits it. A patient could get billed more than they ought to be, for example, if the plan does not recognize that a claim is subject to the No Surprises Act, or because of a billing oversight. Patients can appeal these mistakes using the plan’s internal claims and appeals procedure. Under the federal law, the patient has the right to appeal a health plan denial (called an adverse benefit determination or “ABD”). ABDs also include plan decisions to apply the incorrect cost-sharing amount. Once the adverse benefit determination has been made, the health plan must give the patient at least 180 days to file an internal appeal. For post-service claims, the plan must then complete the internal appeal no later than 60 days after it is filed. If the plan upholds its denial, the patient has a new right under the NSA to ask for an independent external appeal for NSA compliance issues. Federal regulations provide several examples for when NSA-related decisions can be reviewed by an external reviewer, including a decision about whether a specific claim involves an item or service that is covered by the NSA as a surprise bill.

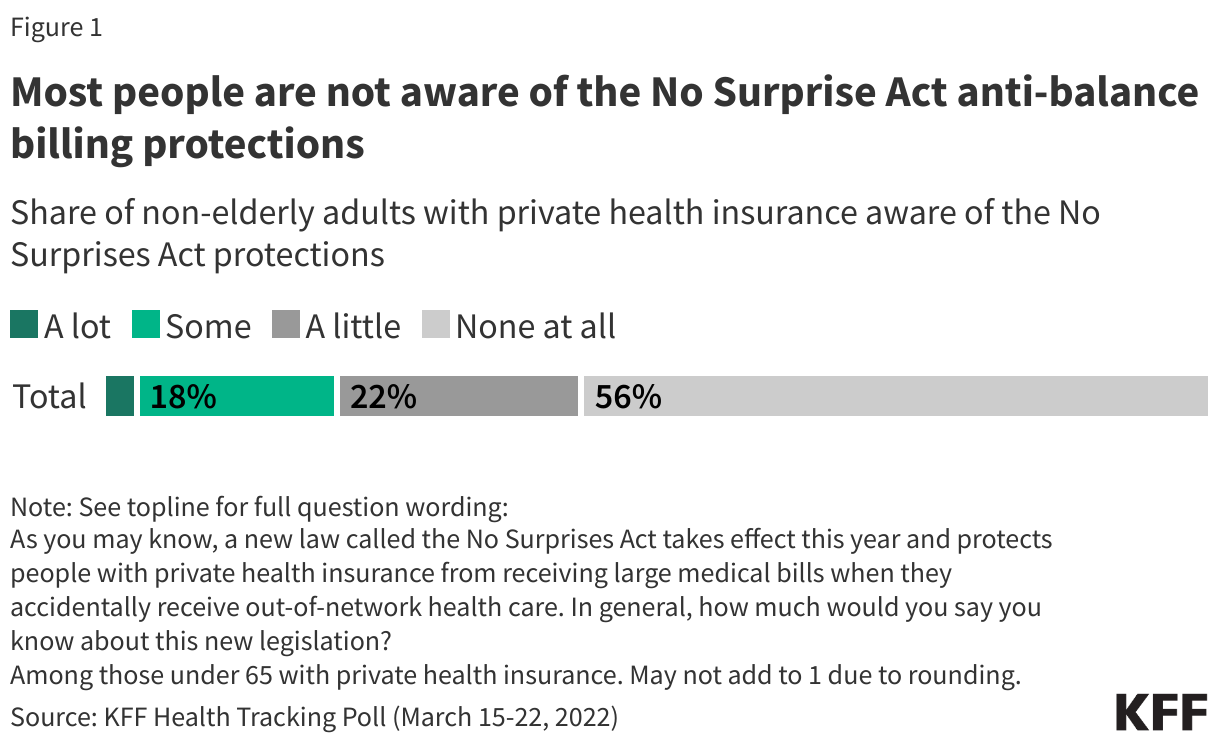

For patients who receive a surprise bill when they should not, what follows may be more complicated. To correct the situation, patients would first need to recognize that the plan’s decision was incorrect and that the provider bill is subject to the No Surprises Act. KFF polling finds the vast majority of Americans (78%) know little or nothing about the new consumer protections law, so the effectiveness of self-advocacy by consumers could be limited if problems arise. Under current law, any health plan ABDs must include contact information for state consumer assistance programs (CAPs) and notice that such programs (in states where they exist) can help people file an appeal. Consumers could reach out to CAPs to get an assessment of whether the bill they received is valid. Additionally, as part of the No Surprises Act, the Centers for Medicare and Medicaid Services (CMS) has established resources for patients to seek review of their medical bills (through this website: https://www.cms.gov/medical-bill-rights/help/submit-a-complaint or by calling the No Surprises Help Desk at 1-800-985-3059 which is available 24/7 and through holidays). This no-wrong-door complaints system is available for consumers who are concerned their plan may have incorrectly denied or covered a surprise medical bill.

Meanwhile, however, if a plan incorrectly denies or covers a surprise bill and the patient does not recognize the mistake in order to be able to either appeal or ask for a state or federal review, the patient might get stuck with the bill.

While patients appeal, there is no federal rule preventing providers from trying to collect the outstanding bill. For incorrect bills, if the patient appeals, the out-of-network provider might be able to bill the patient for the full charge while the appeal is underway. Patients who are unable to pay the outstanding bill may be referred to collection agencies. Though the Consumer Finance Protection Bureau (CFPB) has outlined additional guidelines restricting coercive practices from collection agencies. KFF polling has found that 41% of adults have health care debt according to a broader definition, which includes health care debt on credit cards or owed to family members. KFF analysis of a census survey suggests Americans may owe at least $220 Billion in medical debt. People with medical debt report cutting spending on food, clothing, and other household items, spending down their savings to pay for medical bills, borrowing money from friends or family members, or taking on additional debts. Medical debt may make it difficult for patients to get loans for daily living like housing or car.

Later, if the patient prevails on the appeal, the health plan would need to reprocess the claim, this time following the No Surprises Act rules, and the out-of-network provider would then be required to refund the patient for any amount collected in excess of the applicable in-network cost sharing amount.

Under the Affordable Care Act and the No Surprises Act, federal agencies can impose penalties on health plans and providers for incorrectly billing patients. For plans who incorrectly process claims, they can be charged up to $100 per day per affected beneficiary under federal law. State regulators may have additional authority and enforcement tools they can use to address billing problems. On the provider side, the penalty for incorrect billing is up to $10,000 per violation. That is, if a provider sends 200 incorrect bills, the provider could be penalized $2 million. But for these penalties to happen, the patient would have to successfully lodge a complaint with federal regulators and the regulators would need to investigate and enforce.

Through October 2023, about 11,000 patient complaints have been filed through the federal feedback portal. The federal government has said 248 complaints involved a violation and resulted in $3 million in monetary relief paid to consumers or providers. At this point, it is unclear whether the federal government has issued penalties to providers or health plans for incorrect billing practices.

Discussion

Most patients do not know about the new surprise billing protections and likely also do not know of resources available to seek recourse for incorrect medical bills. It’s advisable to ask about the cost ahead of time, when possible. Additionally, when patients get a large, unexpected bill, a good first step is to call the health plan. New federal resources allow patients to submit complaints and get a response from the federal government. The federal process does not provide a determination or help the consumer fight a bill with the payer. Patients may have little recourse, however, if their plan does not cover certain items or services, or if their surprise balance bill is not protected under federal law.

Plans and providers can now arbitrate disagreements over payments for out-of-network care via the No Surprises Act independent dispute resolution. Most payment determinations through the arbitration process have been in favor of the providers’ asking price. Yet most of the lawsuits against the No Surprises Act are also being brought by providers. The federal government recently proposed several changes with the goal of making the IDR process more efficient and increasing early communication between the parties. In the midst of the legal disputes over the dispute resolution process for payment rates, patients are required to be held harmless for surprise, out-of-network balance bills.

Patients are not supposed to get surprise balance bills, unless there’s a mistake or the surprise bill is not protected. In these situations, patients have some recourses, though they are only helpful if people know about them.