2015 Employer Health Benefits Survey

Section Three: Employee Coverage, Eligibility, and Participation

Employers are the principal source of health insurance in the United States, providing health benefits for about 147 million non-elderly people in America.1 Most workers are offered health coverage at work, and the majority of workers who are offered coverage take it. Workers may not be covered by their own employer for several reasons: their employer may not offer coverage, they may be ineligible for the benefits offered by their firm, they may elect to receive coverage through their spouse’s employer, or they may refuse coverage from their firm. Before eligible employees may enroll, almost three-quarters (74%) of covered workers face a waiting period, although the average length of waiting periods for covered workers with waiting periods has decreased in each of the last two years.

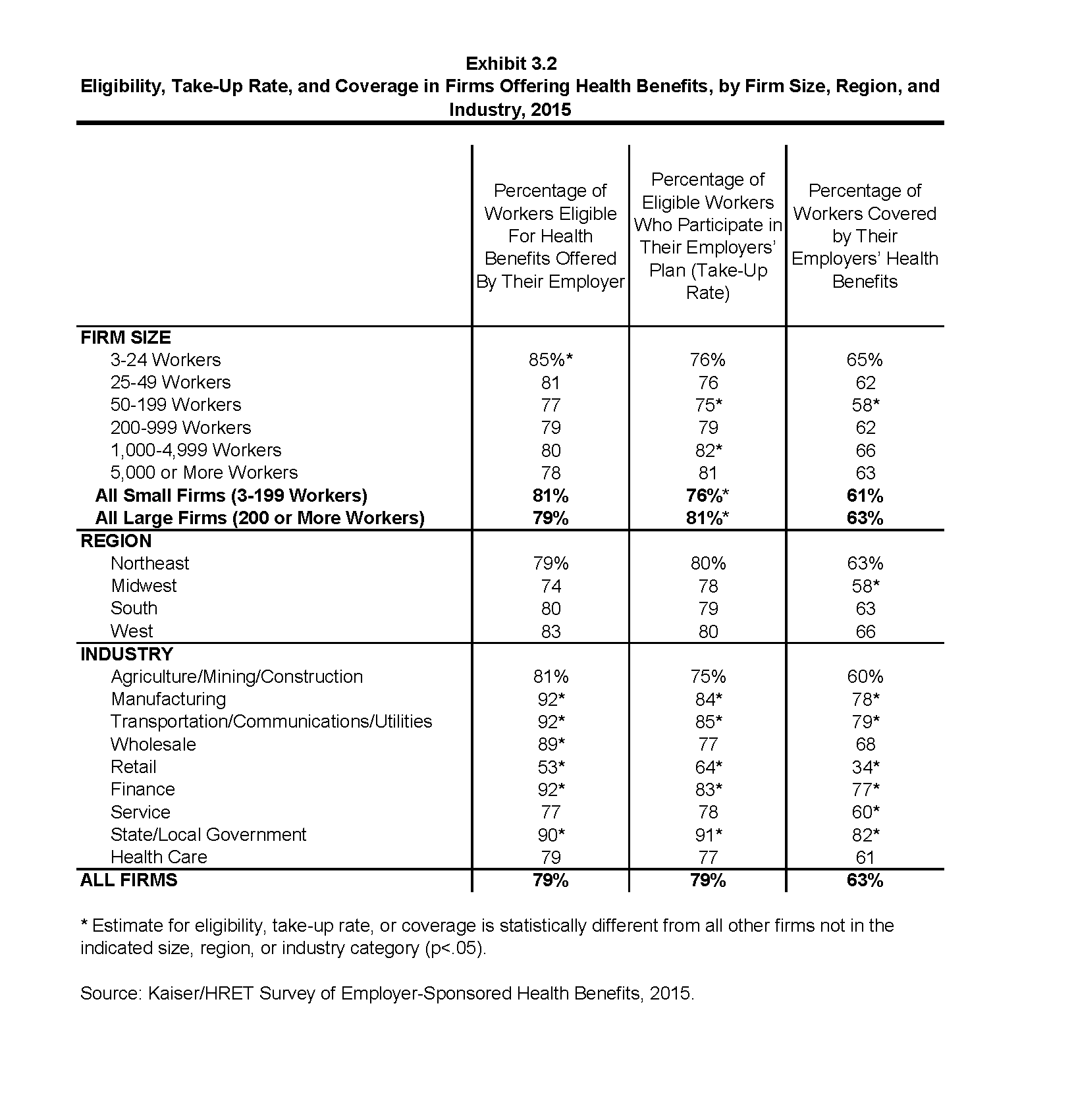

- Among firms offering health benefits, 63% percent of workers are covered by health benefits through their own employer (Exhibit 3.2).

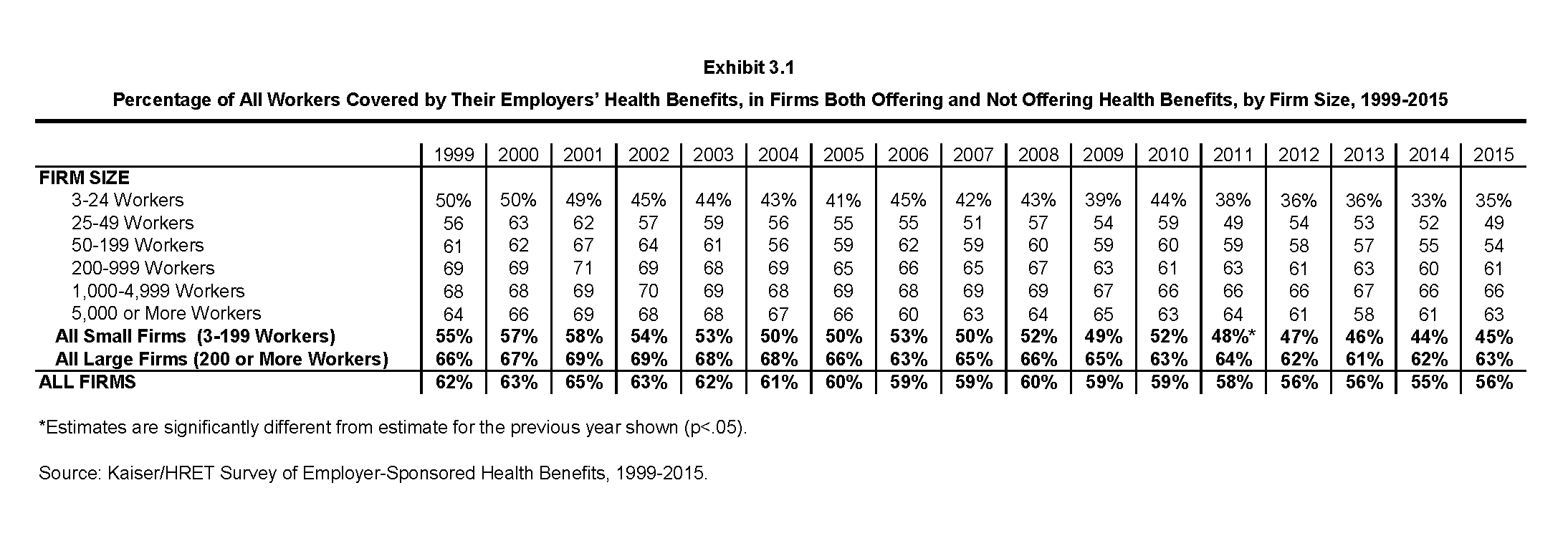

- When considering both firms that offer health benefits and those that do not, 56% of workers are covered under their employer’s plan (Exhibit 3.1).

- The coverage rates at both offering and non-offering firms has decreased over time for workers at small firms (3 to 199 workers) from 50% in 2005 to 45% in 2015. The coverage rate for large firms is statically unchanged from 66% in 2005 to 63% in 2015 (Exhibit 3.1).

Eligibility

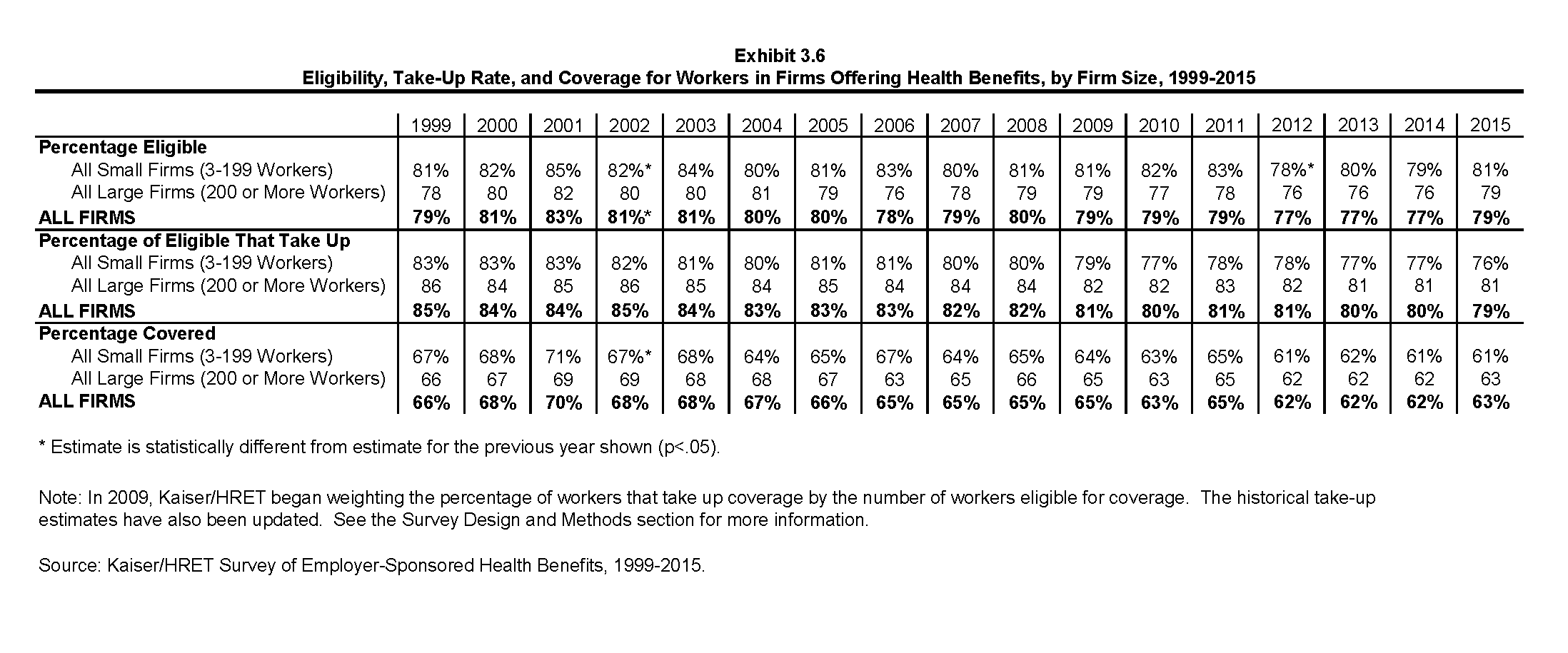

- Not all employees are eligible for the health benefits offered by their firm, and not all eligible employees “take up” (i.e., elect to participate in) the offer of coverage. The share of workers covered in a firm is a product of both the percentage of workers who are eligible for the firm’s health insurance and the percentage that choose to take up the benefit. The percentage of workers eligible for health benefits at offering firms in 2015 is similar to last year for both small firms (3 to 199 workers) and large firms (Exhibit 3.6).

- Seventy-nine percent of workers in firms offering health benefits are eligible for the coverage offered by their employer (Exhibit 3.2).

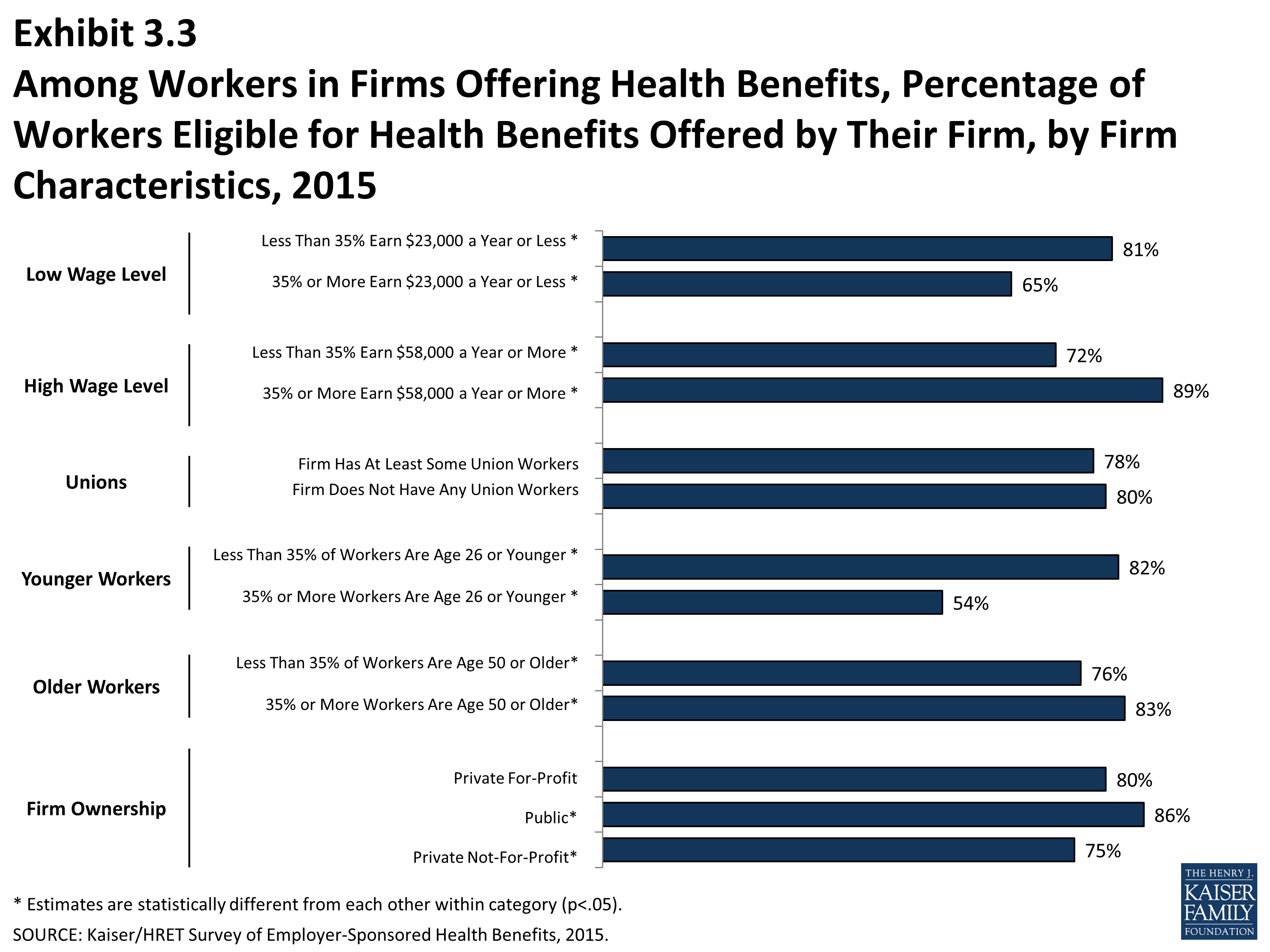

- Eligibility varies considerably by wage level. Employees in firms with a lower proportion of low-wage workers (less than 35% of workers earn $23,000 or less annually) are more likely to be eligible for health benefits than employees in firms with a higher proportion of low-wage workers (81% vs. 65%). We observe a similar pattern among firms with many high-wage workers (35% or more of workers earn $58,000 or more annually) (89% vs. 72%) (Exhibit 3.3).

- Eligibility also varies by the age of the workforce. Those in firms with fewer younger workers (less than 35% of workers are age 26 or younger) are more likely to be eligible for health benefits than those in firms with many younger workers (82% vs. 54%) (Exhibit 3.3).

Take-up Rate

- Employees who are offered health benefits generally elect to take up the coverage. In 2015, 79% of eligible workers take up coverage when it is offered to them, similar to 80% last year (Exhibit 3.6).2

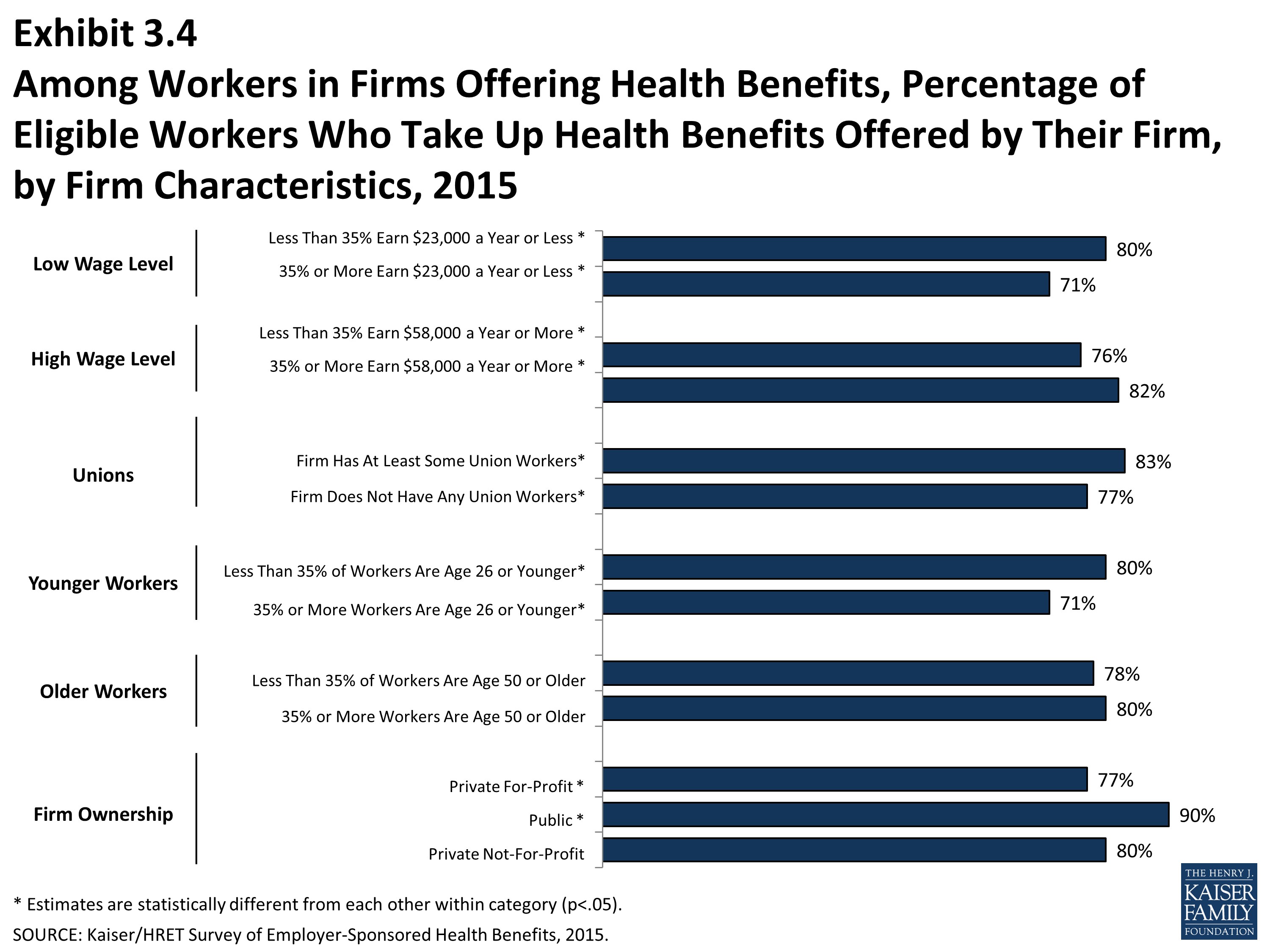

- The likelihood of a worker accepting a firm’s offer of coverage also varies with the workforce’s wage level. Eligible employees in firms with a lower proportion of low-wage workers are more likely to take up coverage (80%) than eligible employees in firms with a higher proportion of low-wage workers (35% or more of workers earn $23,000 or less annually) (71%). Similar patterns exist in firms with a larger proportion of higher-wage workers, with workers in these firms being more likely to take up coverage than those in firms with a smaller share of high-wage workers (82% vs. 76%) (Exhibit 3.4).

- Ninety percent of workers at public employers who offer health benefits take up coverage. (Exhibit 3.4).

Coverage

- The percentage of workers at firms offering health benefits that are covered by their firms’ health plan in 2015 is 63%. The coverage rate at firms offering health benefits is similar to last year for both small firms (3 to 199 workers) and large firms (Exhibit 3.6).

- There is significant variation by industry in the coverage rate among workers in firms offering health benefits. For example, only 34% of workers in retail firms offering health benefits are covered by the health benefits offered by their firm, compared to 77% of workers in finance, and 79% of workers in the transportation/communications/utilities industry category (Exhibit 3.2).

- Among workers in firms offering health benefits, those in firms with fewer low-wage workers (less than 35% of workers earn $23,000 or less annually) are more likely to be covered by their own firm than workers in firms with many low-wage workers (65% vs. 46%). A comparable pattern exists in firms with a larger proportion of high-wage workers (35% or more earn $58,000 or more annually) offering health benefits (73% vs. 55%) (Exhibit 3.5).

- Among workers in firms offering health benefits, those in firms with fewer younger workers (less than 35% of workers are age 26 or younger) are more likely to be covered by their own firm than those in firms with many younger workers (66% vs.39%) (Exhibit 3.5).

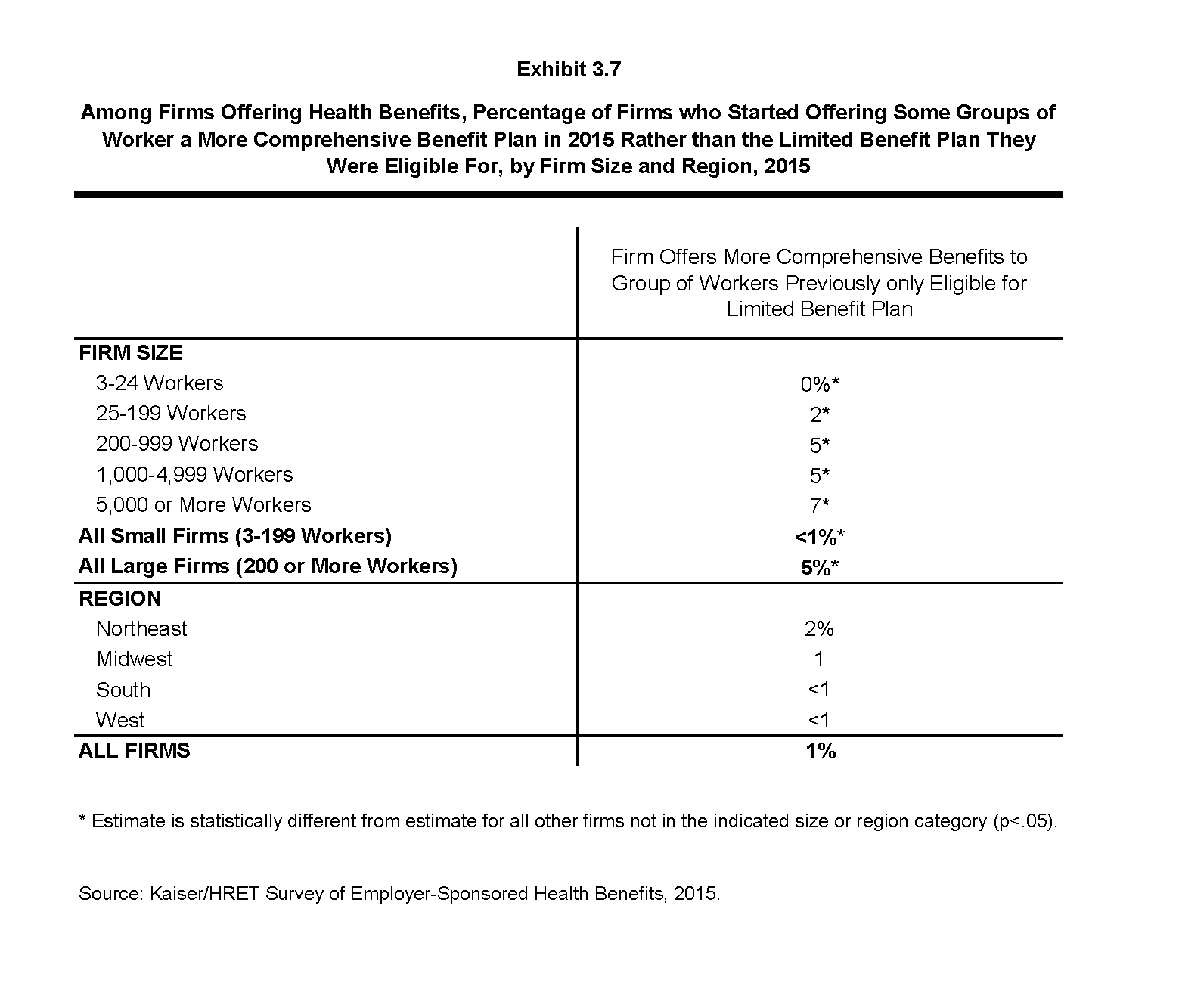

- Five percent of large firms (200 or more workers) and less than 1% of small firms indicated that they started offering a more comprehensive benefit plan in 2015 to some workers who were previously only eligible for a limited benefit plan (Exhibit 3.7).

Waiting Periods

- Waiting periods are a specified length of time after beginning employment before employees are eligible to enroll in health benefits. With some exceptions, the Affordable Care Act requires that waiting periods cannot exceed 90 days.3 For example, employers are permitted to have orientation periods before the waiting period begins which, in effect, means an employee is not eligible for coverage 3 months after hire. If an employee is eligible to enroll on the 1st of the month, after three months of employment, this survey “rounds-up” and considers the firm’s waiting period four months. For these reasons, some employers still have waiting periods exceeding the 90 day maximum.

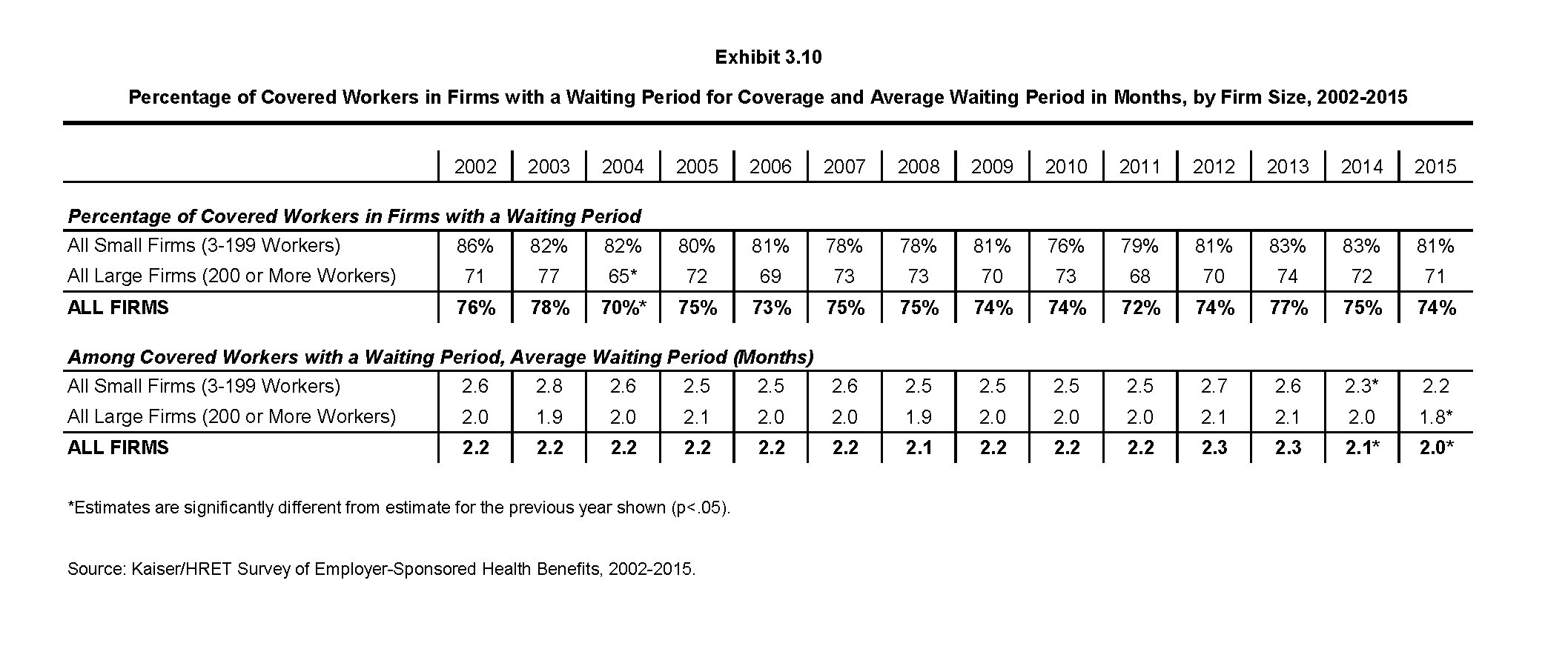

- The percentage of covered workers who face a waiting period is similar to last year (Exhibit 3.10).

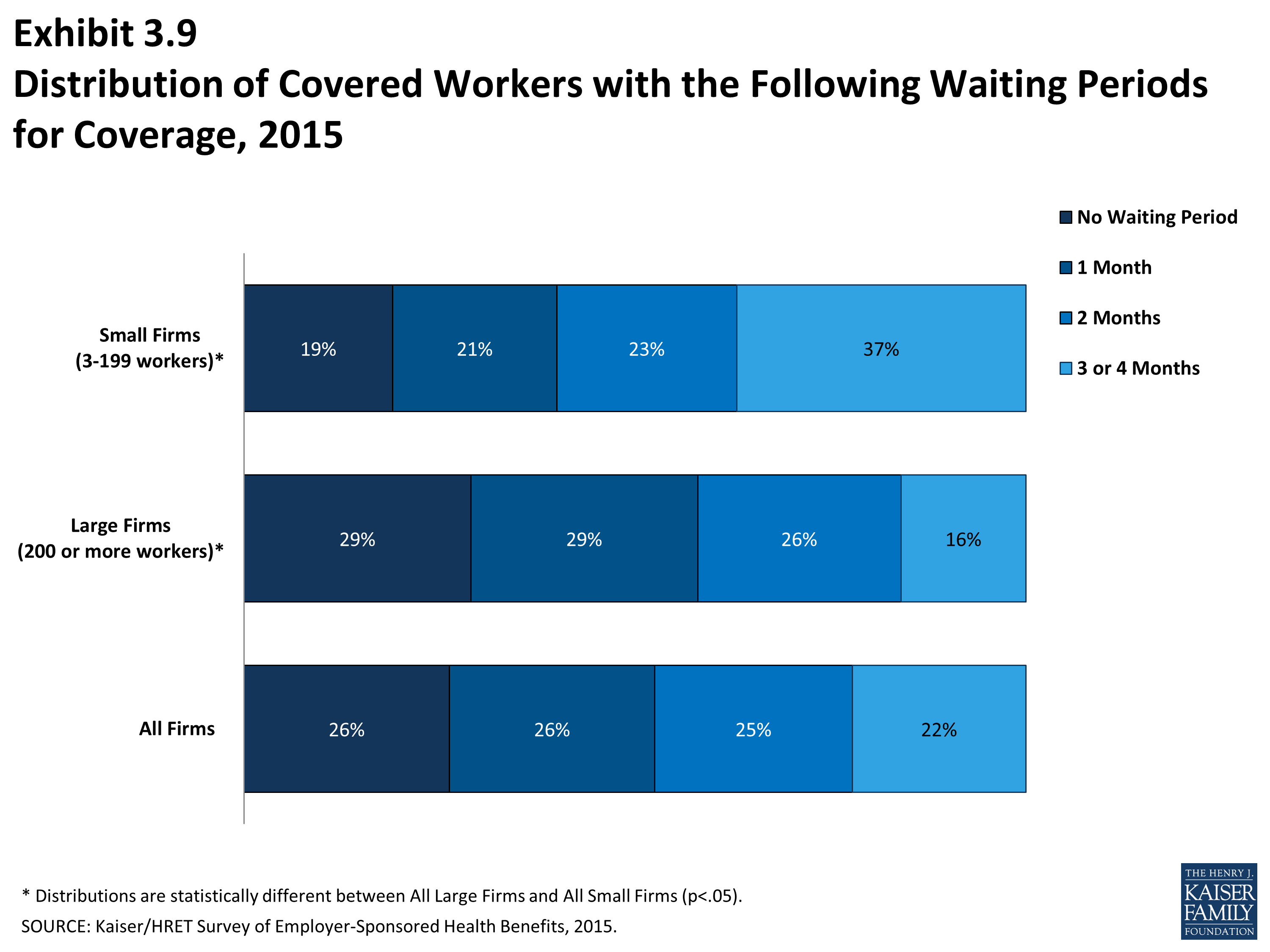

- Seventy-four percent of covered workers face a waiting period before coverage is available. Covered workers in small firms (3 to 199 workers) are more likely than those in large firms to have a waiting period (81% vs. 71%) (Exhibit 3.8).

- The average waiting period among covered workers who face a waiting period is 2 months (Exhibit 3.8). While 22% of covered workers face a waiting period of 3 months or more, workers in small firms (3 to 199 workers) generally have longer waiting periods than workers in large firms (Exhibit 3.9).

Auto Enrollment

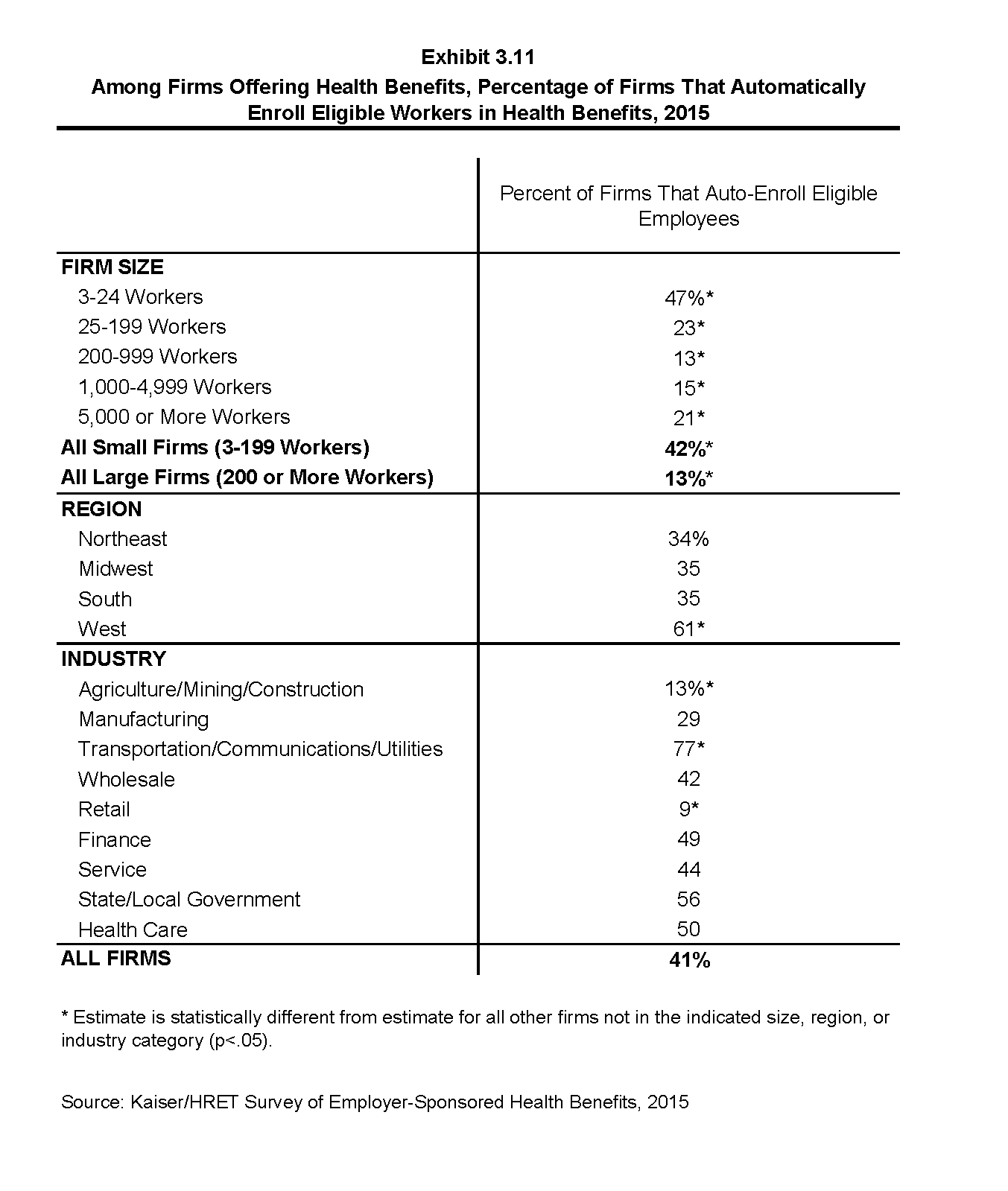

The Affordable Care Act requires that employers with 200 or more workers automatically enroll eligible full-time workers in their health benefits after any waiting periods. The implementation of this provision has been delayed by the Department of Labor rules.4

- In 2015, 13% of large employers (200 or more workers) indicated that they automatically enrolled employees after any waiting periods are met (Exhibit 3.11).

- Small employers (3 to 199 workers) were more likely than large firms to automatically enroll eligible employees after any waiting periods (42% vs. 13%) (Exhibit 3.11).

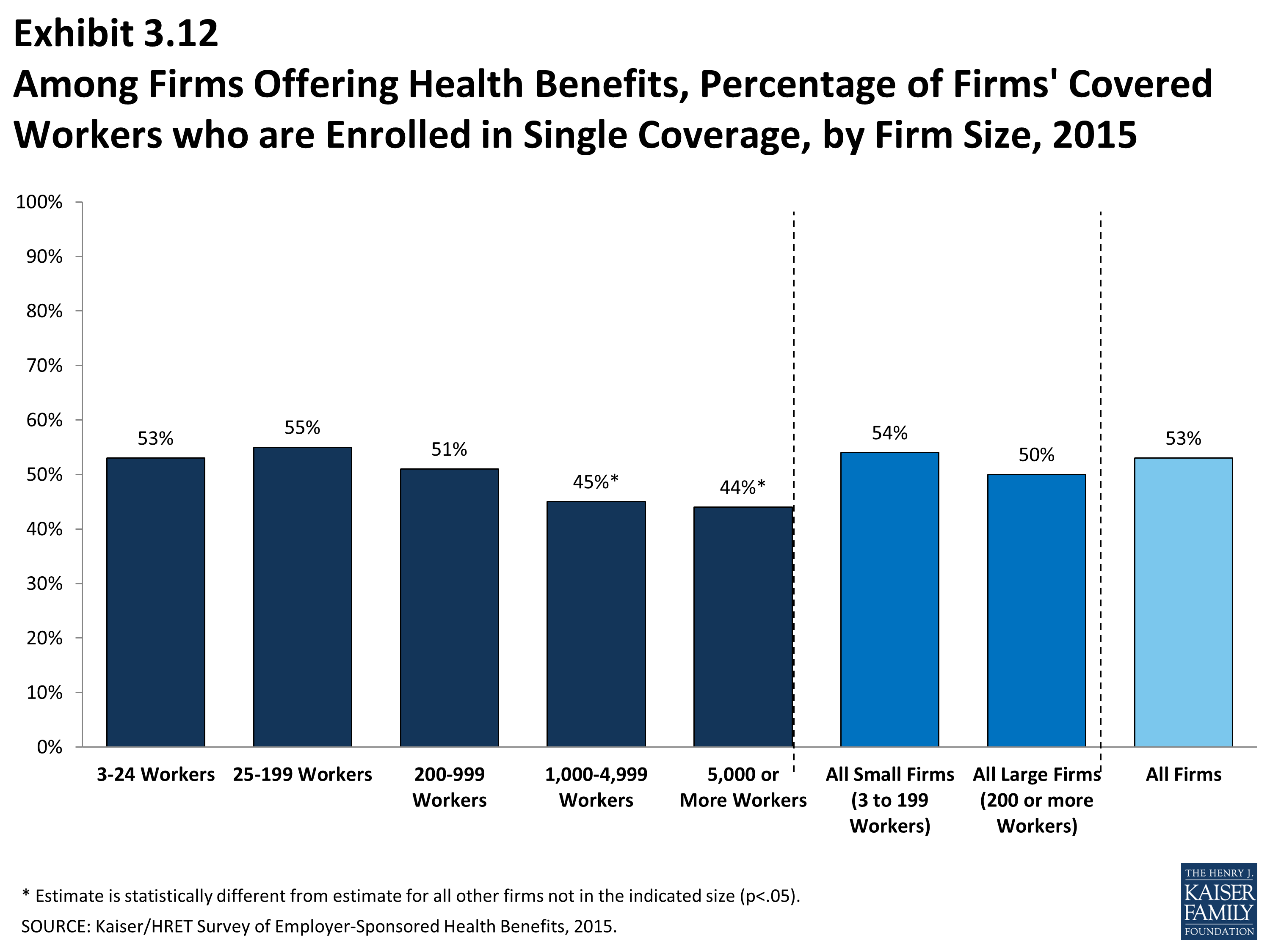

Single Coverage Enrollment

- Covered workers in small firms (3 to 99 workers) are more likely to be enrolled in single coverage than covered workers in large firms (54% vs. 44%) (Exhibit 3.12).

Percentage of All Workers Covered by Their Employers’ Health Benefits, in Firms Both Offering and Not Offering Health Benefits, by Firm Size, 1999-2015

Eligibility, Take-Up Rate, and Coverage in Firms Offering Health Benefits, by Firm Size, Region, and Industry, 2015

Among Workers in Firms Offering Health Benefits, Percentage of Workers Eligible for Health Benefits Offered by Their Firm, by Firm Characteristics, 2015

Among Workers in Firms Offering Health Benefits, Percentage of Eligible Workers Who Take Up Health Benefits Offered by Their Firm, by Firm Characteristics, 2015

Among Workers in Firms Offering Health Benefits, Percentage of Workers Covered by Health Benefits Offered by Their Firm, by Firm Characteristics, 2015

Eligibility, Take-Up Rate, and Coverage for Workers in Firms Offering Health Benefits, by Firm Size, 1999-2015

Among Firms Offering Health Benefits, The Percentage of Firms who Started Offering Some Groups of Worker a More Comprehensive Benefit Plan in 2015 Rather than the Limited Benefit Plan they were Eligible For, by Firm Size and Region, 2015

Percentage of Covered Workers in Firms with a Waiting Period for Coverage and Average Waiting Period in Months, by Firm Size, Region, and Industry, 2015

Distribution of Covered Workers with the Following Waiting Periods for Coverage, 2015

Percentage of Covered Workers in Firms with a Waiting Period for Coverage and Average Waiting Period in Months, by Firm Size, Region, and Industry, 2002-2015

Among Firms Offering Health Benefits, Percentage of Firms Which Automatically Enroll Eligible Workers in Health Benefits, 2015