As Pandemic-Era Policies End, Medicaid Programs Focus on Enrollee Access and Reducing Health Disparities Amid Future Uncertainties: Results from an Annual Medicaid Budget Survey for State Fiscal Years 2024 and 2025

Provider Rates and Taxes

Context

States have substantial flexibility to establish Medicaid provider reimbursement methodologies and amounts, especially within a fee-for-service (FFS) delivery system where a state Medicaid agency pays providers or groups of providers directly. While states with capitated managed care arrangements are generally not permitted to direct how their contracted managed care organizations (MCOs) pay providers, state determined FFS rates remain important benchmarks for MCO payments in most states. To improve access to Medicaid services across both FFS and managed care delivery systems, recently finalized rules include provisions that require states to improve payment rate transparency and promote payment adequacy for some direct care workers (see Box 1).

Fee-for-Service Rates. While federal law and regulations grant states broad latitude to determine FFS provider payments, they also require that payments be sufficient to ensure that Medicaid enrollees have access to care that is equal to the level of access enjoyed by the general population in the same geographic area.1 CMS reviews and approves state changes to FFS payment methodologies through the Medicaid State Plan Amendment process.2 In addition to FFS provider payments, states are permitted to make multiple types of “supplemental” payments. States make these payments for a variety of purposes including to supplement Medicaid “base” FFS payment rates that often do not fully cover provider costs as well as to help support the costs of care for uninsured patients.

Managed Care Provider Rates. States pay Medicaid MCOs a set per member per month (“capitation”) payment for the Medicaid services specified in their contracts. Under federal law, payments to Medicaid MCOs must be actuarially sound. Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Plan rates are usually set for a 12-month rating period and must be reviewed and approved by CMS each year. States are generally prohibited from contractually directing how a managed care plan pays its providers.3 Subject to CMS approval, however, states may implement certain “state directed payments” (SDPs)4 that require managed care plans to adopt minimum or maximum provider payment fee schedules, provide uniform dollar or percentage increases to network providers (above base payment rates), or implement value-based provider payment arrangements.

Box 1: Federal Rules Finalized in 2024

FFS / Access Rule. The recently finalized Ensuring Access to Medicaid Services final rule (Access rule)5 is designed to promote quality of care and improved health outcomes by advancing access to care for Medicaid enrollees. The rule addresses several dimensions of access: increasing provider rate transparency and accountability, standardizing data and monitoring, and creating opportunities for states to promote active enrollee engagement in their Medicaid programs. The rule requires states, in part, to:

- Conduct comparative rate analyses. States must compare their FFS payment rates for primary care, obstetrical and gynecological care, and outpatient mental health and substance use disorder services to Medicare rates, and publish the analysis every two years, with the first analysis published by July 1, 2026.

- Publish fee schedules. By July 1, 2026, states must publish all FFS rates on a publicly available and accessible website and make updates within one month of a payment rate change.

- Disclose payment rates for HCBS. By July 1, 2026, states must publish the average hourly rate paid for personal care, home health aide, homemaker, and habilitation services, and publish the disclosure every two years.

- Establish a direct care worker payment advisory group. Within two years (of effective date of the final rule), states must establish an advisory group that includes direct care workers, beneficiaries, beneficiaries’ authorized representatives, and other interested parties to advise and consult on the sufficiency of payment rates (at least every two years) for personal care, homemaker, home health aide, and habilitation services.

- Ensure HCBS payment adequacy. Beginning in July 2030, states must ensure a minimum of 80% of Medicaid payments for homemaker, home health aide, and personal care services are spent on compensation for direct cares workers, as opposed to administrative overhead or profit (known as the “80/20 rule.”)

LTC Facility Staffing Rule. One provision of the recently finalized Minimum Staffing Standards for Long-Term Care Facilities and Medicaid Institutional Payment Transparency Reporting final rule (LTC Facility Staffing rule) requires states, beginning in June 2028, to collect and report on the percent of Medicaid payments that are spent on compensation for direct care workers and support staff delivering care in nursing facilities and intermediate care facilities, for individuals with intellectual disabilities.6

Managed Care Rule. The recently finalized Medicaid and CHIP Managed Care Access, Finance, and Quality final rule (Managed Care rule) introduced a managed care payment analysis requirement and made several changes to state directed payment requirements including:

- Requiring states to submit annual payment analysis. States must submit an annual analysis comparing managed care plans’ payment rates for certain services to Medicare rates and compare certain HCBS rates to state FFS payment rates (beginning the first rating period that begins on or after July 9, 2026.)7

- Eliminating the requirement to obtain prior approval for certain SDPs. States will no longer be required to seek prior CMS approval for SDPs that impose minimum fee schedules set at the Medicare payment rate.8

- Establishing SDP payment rate ceiling for certain providers. The rule allows SDPs for inpatient and outpatient hospital services, nursing facility services, and the professional services at an academic medical center to reach “average commercial rates”9 (which is substantially higher than the Medicare payment ceiling used for many FFS supplemental payments).10

Provider Rate Implications of Economic and Fiscal Conditions. Historically, FFS provider rate changes generally reflect broader economic conditions. During economic downturns when states may face revenue shortfalls, states have typically turned to provider rate restrictions to contain costs. Conversely, states are more likely to increase provider rates during periods of recovery and revenue growth. During the COVID-19 public health emergency, however, states were able to generally avoid rate cuts due to temporary federal support from the pandemic-related enhanced Medicaid matching funds as well as enhanced funding for home and community-based services (HCBS). In FY 2024 and FY 2025, states reported inflation and workforce shortages were driving higher labor costs, resulting in pressure to increase provider rates.

Provider Taxes. States have considerable flexibility in determining how to finance the non-federal share of state Medicaid payments, within certain limits. In addition to state general funds appropriated directly to the Medicaid program, most states also rely on funding from health care providers and local governments generated through provider taxes, user fees, intergovernmental transfers (IGTs), and certified public expenditures (CPEs). Over time, states have increased their reliance on provider taxes, with expansions often driven by economic downturns. Federal regulations11 require provider taxes to be broad-based (imposed on all non-governmental entities, items, and services within a class), and uniform (consistent in amount and scope across the entities, items, or services to which it applies), and must not hold taxpayers harmless (i.e., directly or indirectly guarantee that the provider will be repaid for all or a portion of the tax). Also, a provider tax will meet the hold harmless “safe harbor threshold” if it generates revenue that does not exceed 6% of net patient revenue.

This section provides information about:

- Hospital reimbursement

- Nursing facility reimbursement

- FFS reimbursement rates for other provider types

- Payment rate transparency

- Provider taxes

Findings

Hospital Reimbursement – FFS Base Rates, Supplemental Payments, and State Directed Payments (SDPs)

States make different types of Medicaid payments to hospitals. The two broad categories of FFS payment are (1) FFS base rates and (2) supplemental payments, typically made in a lump sum for a fixed period of time. States use supplemental payments, including upper payment limit (UPL), disproportionate share hospital (DSH), or uncompensated care pool payments, to cover hospital costs that exceed the amounts covered by their FFS base rates. DSH payments can also be used to pay for unpaid costs of care for the uninsured. The Medicaid statute12 requires states to make Medicaid DSH payments to hospitals, and most states also make other types of FFS supplemental payments, although payment amounts and how they are distributed to hospitals vary considerably across states. Because many types of supplemental payments are interchangeable, an increase in one type can lead to a decrease in another. Increases or decreases in base FFS payments may also result in supplemental payment changes.

Hospital FFS base rates (and payment methods) also vary considerably across states and, on average, are below hospitals’ costs of providing services to Medicaid enrollees and below Medicare payment rates for comparable services,13 causing some states to rely more heavily on supplemental payments than others to help cover hospitals’ costs. Within a state, reimbursement methodologies and levels may also vary by hospital type (e.g., community, critical access, and academic medical center hospitals). While managed care organizations have flexibility to determine provider payment methodologies and amounts, they often pay rates that are similar to FFS rates. As a result, many states that contract with MCOs use state directed payments (SDPs) to make uniform rate increases that are like FFS supplemental payments.14

According to the Medicaid and CHIP Payment and Access Commission (MACPAC), in FY 2022, 61% of Medicaid payments to hospitals were made through managed care delivery systems and 39% were made on a FFS basis. Further, about half of FFS payments to hospitals were made through supplemental payments, while one-third of managed care payments to hospitals are made through SDPs.

In this year’s survey, states were asked to report on changes made to their FFS base rates, non-DSH supplemental payments, and hospital SDPs in FY 2024 and changes planned for FY 2025. DSH was excluded as individual state DSH allotments are federally determined and MACPAC is statutorily required to annually report on Medicaid DSH allotments.

Hospital FFS Base Rates & Non-DSH FFS Supplemental Payments

Overall, few responding states reported hospital rate decreases (FFS base rates or supplemental payments) in FY 2024 or FY 2025 (Table 1). Among the states that reported decreases, several reported that the decreases (to FFS base rates or non-DSH supplemental payments) offset increases in other areas. For example, two states (California and Oklahoma) reported transitions in utilization from FFS to managed care caused non-DSH supplemental payments to decrease while managed care state directed payments increased (in FY 2024 and/or FY 2025.) Michigan reported its reduction in total non-DSH supplemental payments (in FY 2024) offset an increase in FFS base rates for hospitals designated as Level I or Level II Trauma Centers. Massachusetts reported while hospital base rates were set to decrease in FY 2025, overall payments to hospitals would increase when add-on and incentive payments are included. In contrast, Utah reported plans to reduce a small graduate medical education (GME) supplemental payment in FY 2025 without noting any offsetting FFS base rate increases.

More than half of responding states (26 states) reported increasing both inpatient and outpatient hospital FFS base rates in FY 2024 (Table 1). Nearly half (20 states) reported plans to increase inpatient and outpatient FFS base rates in FY 2025. A few states commented on more significant FFS hospital base rate increases:

- Illinois reported a 10% across the board increase for both inpatient and outpatient base rates in FY 2024.

- Maine reported substantial increases to inpatient DRG (diagnosis-related group) rates in FY 2025 to align more closely with Medicare rates and increased outpatient rates in both FY 2024 and FY 2025, benchmarking them to Medicare outpatient rates.

- Missouri reported an average 9% increase in FFS hospital per diems in FY 2025 due to increased cost trends.

Many states reported increases in both hospital base rates and non-DSH supplemental payments in both FY 2024 and FY 2025 (Figure 9). Most responding states reported making non-DSH supplemental payments for both inpatient (42 of 48 in both years) and outpatient (37 of 48 in FY 2024 and 36 of 47 in FY 2025) hospital services (Table 1). Of the 42 states with inpatient supplemental payments, nearly half in FY 2024 (18 states) and one-third in FY 2025 (14 states) planned to increase both FFS base rates and supplemental payments (Figure 9). Of the states reporting outpatient supplemental payments (37 in FY 2024 and 36 in FY 2025), over one-third in FY 2024 (13 states) and about one-quarter in FY 2025 (9 states) planned to increase both FFS base rates and supplemental payments.

Hospital State Directed Payments

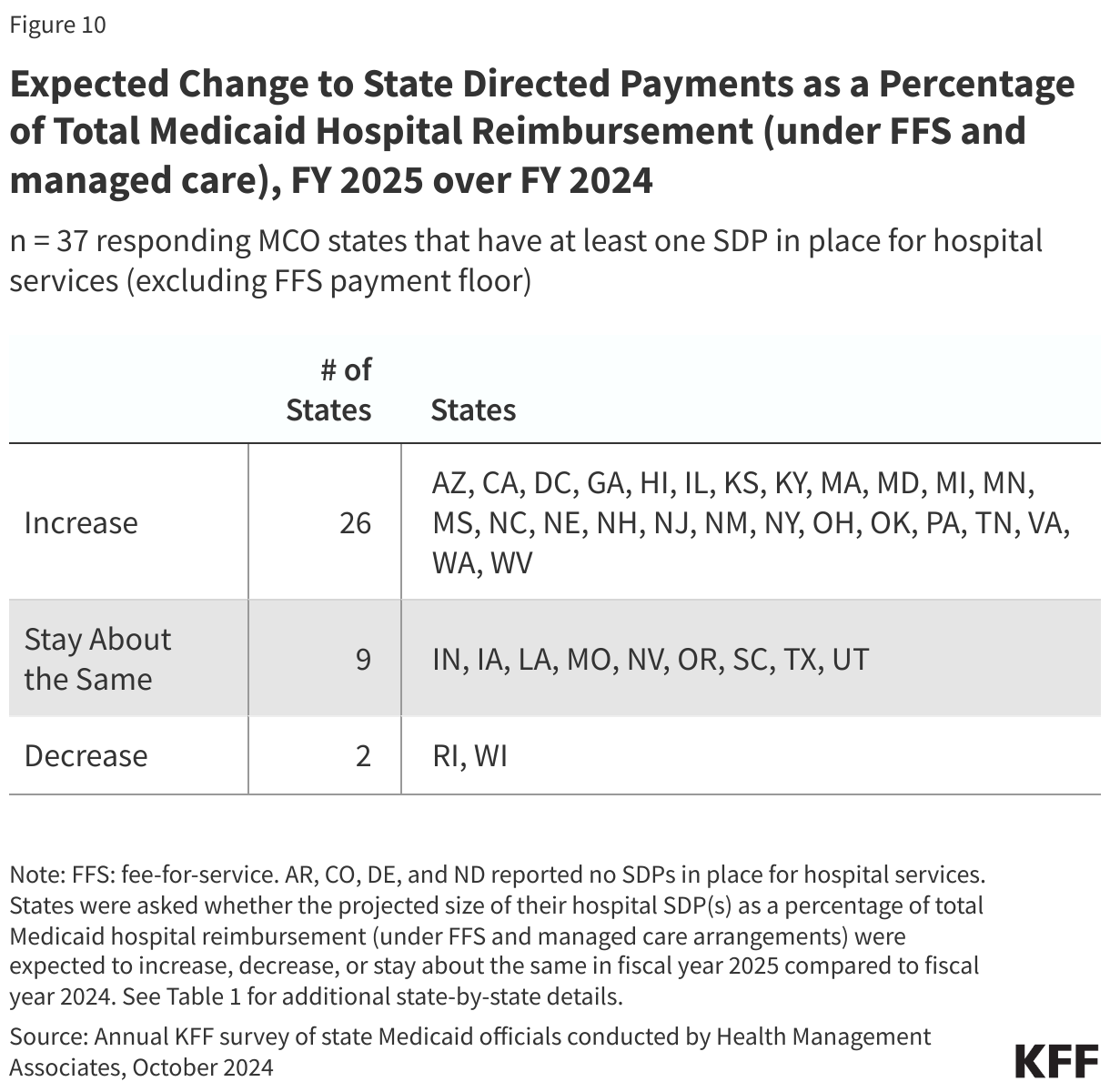

Recent reports indicate state directed payments have been a major driver of Medicaid expenditure growth in recent years. New Medicaid managed care rules finalized in 2024 permit states to pay hospitals and nursing facilities at the average commercial payment rate (ACR) when using directed payments, which is substantially higher than the Medicare payment ceiling used for other Medicaid FFS supplemental payments. Recently revised CBO Medicaid spending projections for 2025-2034 reflect a 4% (or $267 billion) increase with half of the increase attributed to expected growth in directed payments in Medicaid managed care (driven in part by the rule change allowing states to pay at the ACR).

Thirty-seven15 of 41 responding states that contract with MCOs reported an SDP for hospital services (excluding SDPs requiring a FFS payment floor) in place as of July 1, 2024. Only four states that contract with MCOs reported no SDPs in place (Arkansas, Colorado, Delaware, and North Dakota). States reporting a hospital SDP in place were also asked about whether the projected size of their hospital SDP(s) as a percentage of total Medicaid hospital reimbursement (under FFS and managed care arrangements) was expected to increase, decrease, or stay about the same in FY 2025 compared to FY 2024. The vast majority of MCO states (26 of 37) reported that the hospital SDP payments, as a percentage of total Medicaid hospital reimbursement, were projected to increase in FY 2025 (Figure 10 and Table 1). A few states commented on significantly increasing, or plans to significantly increase, hospital SDPs in FY 2024 or 2025, including increases up to the ACR ceiling:

- The District of Columbia reported seeking CMS approval to increase hospital inpatient and outpatient SDPs up to the ACR ceiling effective in FY 2025.

- Michigan increased its inpatient hospital SDP by $2.5 billion in FY 2024 (113.64%), with $1.8 billion coming from federal funds.

- Nebraska is implementing a new hospital SDP in FY 2025 expected to generate approximately $1 billion in federal funds per year.16

- Utah reported having SDPs in place targeting 95% of ACR for private hospitals and 100% of ACR for state-owned hospitals in FY 2025.

Nursing Facility Reimbursement – FFS Base Rates and Supplemental Payments

State Medicaid programs typically pay nursing facilities a daily “per diem” rate that is determined by state-specific methodologies that are often cost-based and commonly account for several specified cost categories such as direct care costs (including nursing and other direct care worker wages and benefits), indirect care costs (ancillary costs such as social services, patient activities, medical directorship, and clinical consultants), administration (such as administrative services, food service, housekeeping, maintenance, laundry, and utilities), and capital costs for the physical building.17 Most states also adjust base rates by patient acuity and may also choose to make quality incentive payments and supplemental payments intended to make up the difference between base FFS payments and the amount that Medicare would have paid for the same service. To address workforce shortages in nursing facilities, the recently finalized LTC Facility Staffing rule creates new minimum staffing requirements for nursing facilities with implications for Medicaid nursing facility reimbursement policies and budgets.

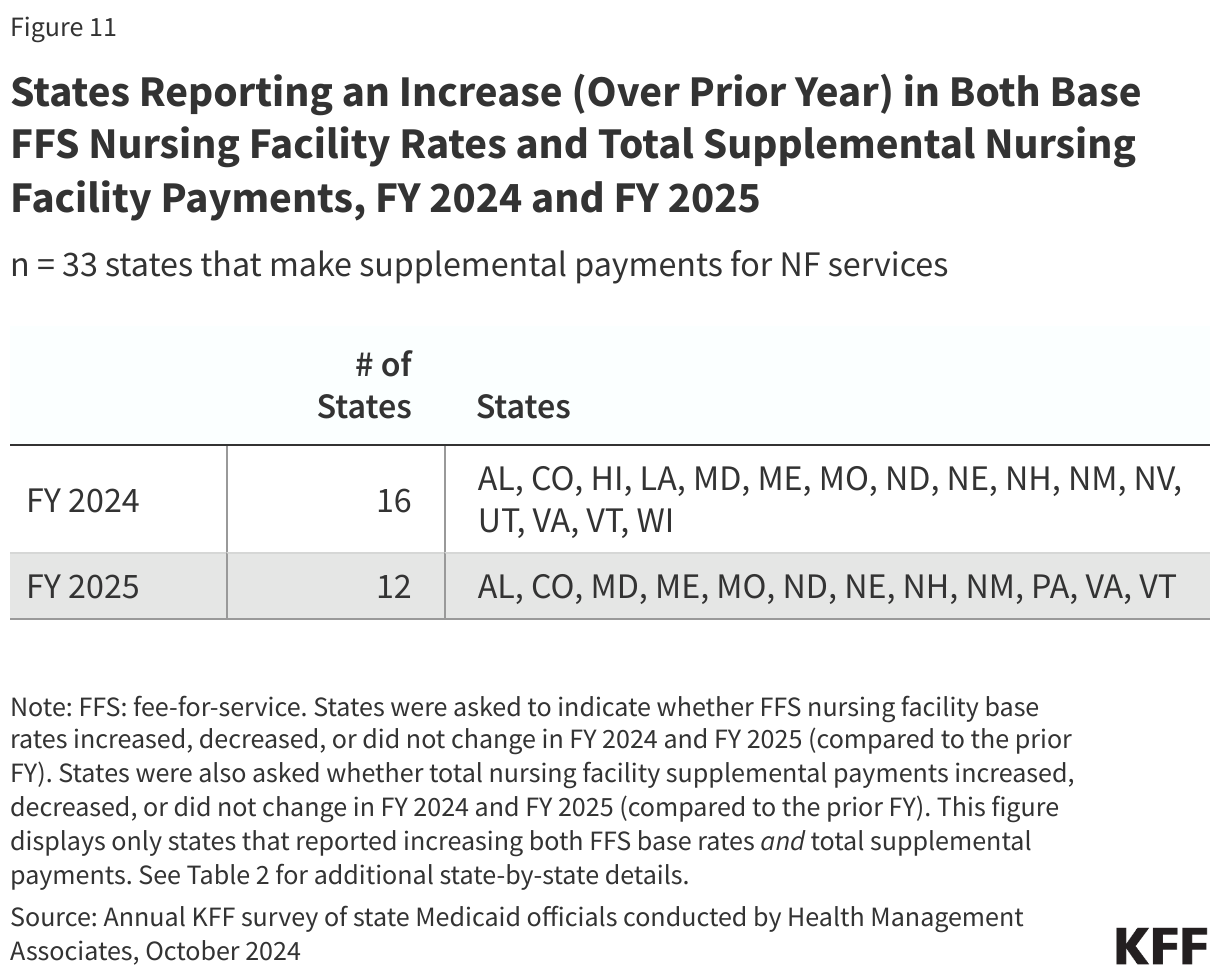

Overall, few responding states (5) reported nursing facility rate decreases (FFS base rates or supplemental payments) in FY 2024 or FY 2025 (Table 2). One of these states (California) attributed its decrease in total nursing facility supplemental payments to utilization shifts from FFS to managed care. Another state (Indiana) reporting a decrease in total nursing facility supplemental payments is implementing an LTSS managed care program in FY 2025.

Most responding states reported increasing nursing facility FFS base rates in both FY 2024 (45 of 49) and FY 2025 (39 of 49) (Table 2). Reflecting the ongoing staffing challenges impacting nursing facility services, several states reported more significant nursing facility base rate increases. Examples include:

- Iowa reported a 25.49% base rate increase in FY 2024.

- Montana increased base rates by 8.24% effective July 1, 2024.

- Nevada reported increased base, pediatric, and ventilator rates by 24.5% in FY 2024.

- Ohio reported a 17% increase in FY 2024.

- Rhode Island reported completing a rate review which will result in a 14.5% increase to the direct care, indirect care, and other direct care components of the nursing facility base rates as of October 1, 2024.

- Texas reported increasing rates by 8-14% across the various Resource Utilization Groups effective September 1, 2023.

Many states reported increasing both nursing facility FFS base rates and total nursing facility supplemental payments in both FY 2024 and FY 2025 (Figure 11). About two-thirds of responding states (33 of 49) made supplemental payments for nursing facility services for both FY 2024 and FY 2025 (Table 2). Of these 33 states, nearly half (16 states) in FY 2024 and over one-third (12 states) in FY 2025 planned to increase both FFS base rates and supplemental payments.

FFS Reimbursement Rates for Other Provider Types

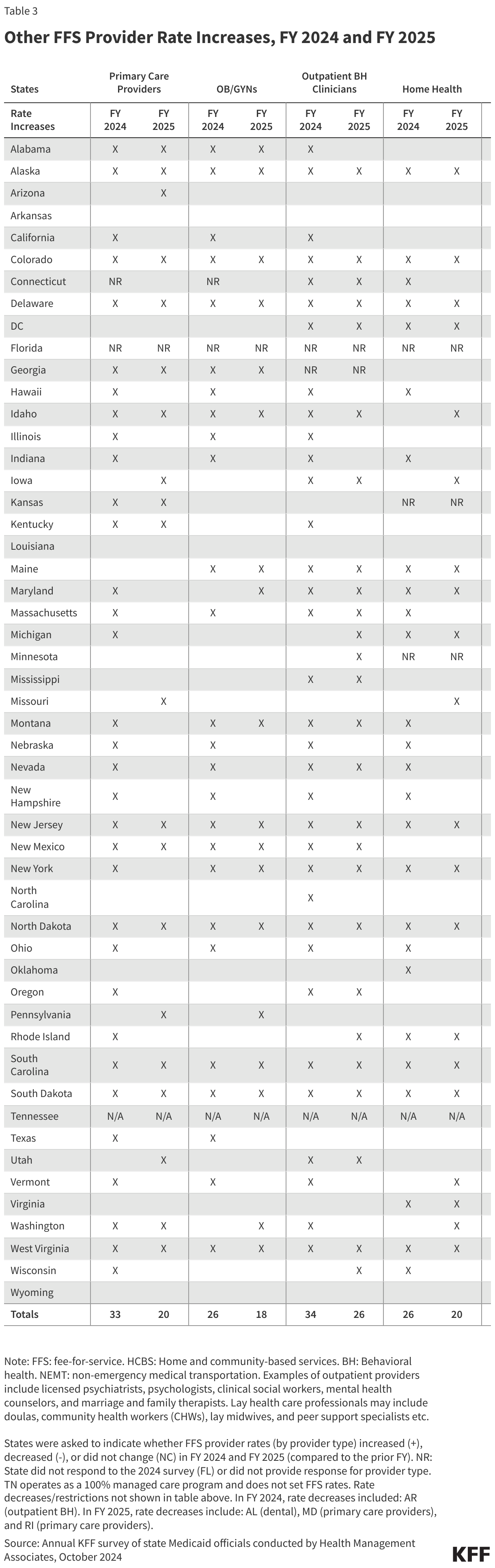

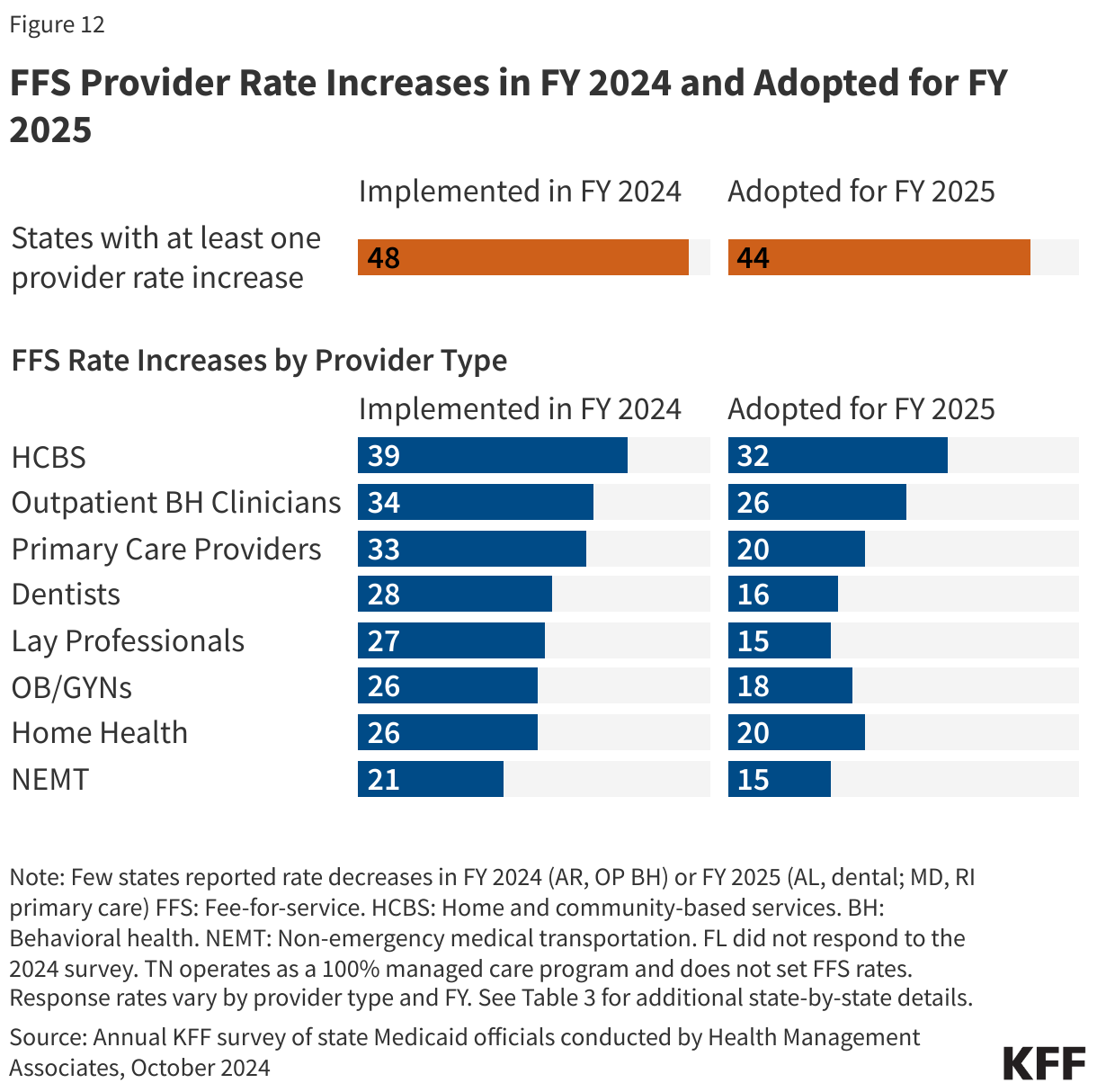

In addition to nursing facility and hospital rates, this year’s survey asked states to report FFS rate changes in FY 2024 and FY 2025 for the following provider types: primary care providers, OB/GYNs, outpatient behavioral health (BH) clinicians, home health, dentists, lay professionals, home and community-based services (HCBS) providers, and providers of non-emergency medical transportation (NEMT).

At the time of the survey, responding states had implemented or were planning more FFS rate increases than rate restrictions in both FY 2024 and FY 2025 (Figure 12 and Table 3).18,19 Forty-eight states in FY 2024 and 44 states in FY 2025 reported implementing FFS rate increases for at least one (non-hospital, non-nursing facility) provider category. Only one state in FY 2024 and three in FY 2025 implemented or were planning to implement at least one rate restriction.

States reported rate increases for HCBS providers more often than for other provider categories (Figure 12). Between April 1, 2021 and March 31, 2022, states received an additional 10 percent in federal matching funds for HCBS spending, funded through the American Rescue Plan Act (ARPA). States were required to reinvest the additional federal funding in Medicaid HCBS, resulting in an estimated $37 billion of new HCBS funding. As of the end of 2023, the largest use of funds was for workforce recruitment and retention, often through payment rate increases or retention bonuses for HCBS workers. The ARPA funding will end in most states by March 2025 (though some states have received extensions into 2026). In this year’s survey, most states reported increasing HCBS rates in both FY 2024 (39 states) and FY 2025 (32 states). One state (Wyoming) commented that it planned to continue enhanced ARPA-funded rates in both FY 2024 and FY 2025 and was also planning to seek permanent funding from its legislature to continue the enhanced rates beyond the expiration of ARPA HCBS funding. Examples of other HCBS rate increases reported include the following:

- California and the District of Columbia reported HCBS rate increases in both FY 2024 and FY 2025 to account for increases in California’s statewide minimum wage and the District of Columbia’s living wage. Over 6,000 California HCBS providers also received retention payments in FY 2024.

- Connecticut enacted several HCBS rate increases including a 12.5% increase to home-delivered meals and 8.6% increase to adult day services for individuals enrolled in the State’s 1915(i) waiver.

- Kentucky implemented a legislatively mandated 10% rate increase for HCBS providers in FY 2024 and will study HCBS rates in FY 2025.

- Mississippi increased all HCBS rates by 4% in FY 2024.

- Texas enacted legislation in 2023 to increase personal care attendant rates in FY 2024 from $8.11 to $10.60, a 30% increase.

Thirty-three states reported increasing primary care provider rates in FY 2024 and 20 states reported plans to do so in FY 2025. States reporting notable primary care rate increases for FY 2024 or FY 2025 include Kansas (9% in FY 2025), Michigan (7.5% in FY 2024), Ohio (6% in FY 2024), and South Dakota (5% in FY 2024). Other states reported benchmarking to Medicare rates, for example, 87.5% of Medicare in California and 70% of Medicare (if rates were lower) in Illinois.

This year’s survey found a continued focus on improving dental rates with 28 states implementing a dental rate increase in FY 2024. Sixteen states also reported planned increases to dental rates in FY 2025. States reporting notable dental rate increases for FY 2024 or FY 2025 include Ohio (93% increase on average per procedure in FY 2024), Wyoming (25% increase in FY 2025), Nebraska (12.5% increase in FY 2025), Vermont (raising rates to 75% of regional commercial rates in FY 2024), and Missouri (increases in FY 2025 to cover a larger percentage of usual and customary rates).

Thirty-four states implemented FFS rate increases for one or more outpatient behavioral health providers in FY 2024 and 26 states plan to do so in FY 2025. Examples of outpatient providers include licensed psychiatrists, psychologists, clinical social workers, mental health counselors, and marriage and family therapists. Examples of rate increases reported for FY 2024 or FY 2025 include:

- Mississippi will increase behavioral health codes by 15% over the course of FY 2024 and FY 2025 for those services billed using the Healthcare Common Procedure Coding System (HCPCS) codes.

- Montana conducted a BH provider reimbursement rate study, resulting in rate increases (which vary by service) in FY 2024 and FY 2025, bringing rates closer to identified benchmarks.

- New Mexico increased behavioral health service rates to a minimum of 120% of the 2023 Medicare fee schedule in FY 2024.

- South Dakota increased rates for Community Mental Health Centers (CMHCs) and substance use disorder (SUD) services by 16% in FY 2024.

- Washington increased developmental screening codes by 100% and implemented varied rate increases for mental and behavioral health services ranging from 7% to 22% in FY 2024.

In FY 2024, 27 states that reimburse services provided by lay professionals on a FFS basis implemented rate increases for one or more lay professionals and 15 states plan to do so in FY 2025. Lay health care professionals, such as doulas, community health workers (CHWs), lay midwives, and peer support specialists, are frontline health workers with a deep understanding of the communities they serve. Typically, they have received some training and may be certified in some cases but are not licensed clinicians. Many state Medicaid programs have chosen to reimburse services provided by one or more types of lay professionals to help reduce health disparities, support other health care providers, and improve health outcomes. Many states reporting rate increases for lay professionals did not specify the type of lay professional impacted by the increase(s), but those that did frequently identified doulas and CHWs. A number of states noted the recent addition of doula coverage including the District of Columbia, Massachusetts, Michigan, New Hampshire, Oklahoma, Pennsylvania, and Washington.

In FY 2024, 21 states that set FFS NEMT rates implemented FFS rate increases and 15 states plan to do so in FY 2025. State Medicaid programs are required to provide non-emergency medical transportation (NEMT) for enrollees who have no other means of transportation to access medically necessary health care services. NEMT is provided in several ways. States may reimburse transportation providers directly on a FFS basis, outsource the service on a FFS or capitated basis to a “transportation broker” (which could be a private vendor or a local or county governmental entity); or carve the benefit into an MCO contract.20 Two states reported particularly notable FFS rate increases: Illinois reported an average statewide increase of 40% for NEMT rates in FY 2024 and Ohio implemented a 79% increase for certain NEMT services that are not county-administered.

Payment Rate Transparency

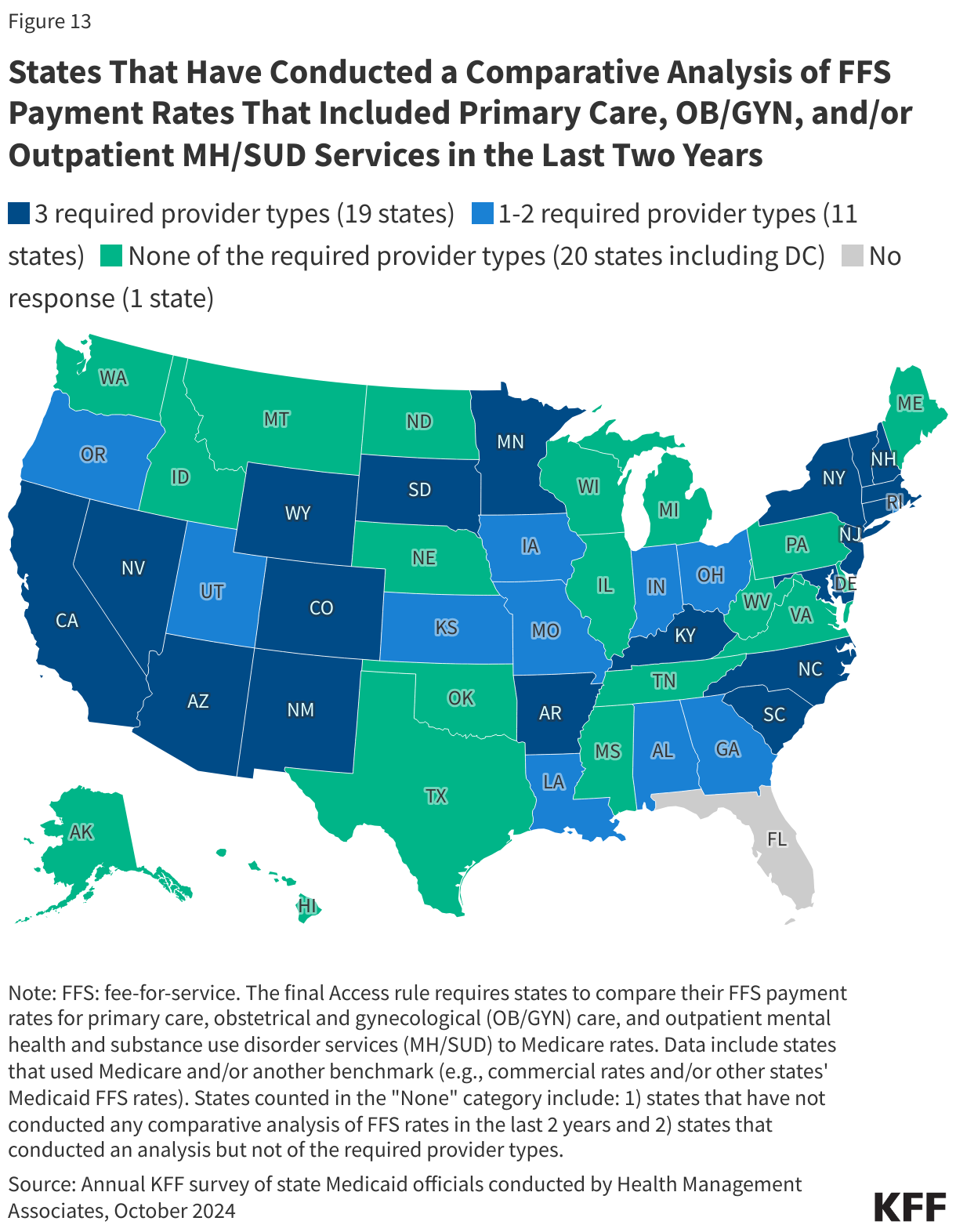

The recently finalized Access rule rescinds regulations that previously required states to produce and submit to CMS at least once every three years Access Monitoring Review Plans (AMRPs) that analyzed the sufficiency of access to care. Instead, the Access Rule has replaced the AMRP requirement with a more streamlined and standardized process that in part requires states to compare FFS payment rates for rates for primary care, OB/GYN, and outpatient mental health and substance use disorder (SUD) services to Medicare rates at least every two years, with the first analysis published by July 1, 2026. The recently finalized Managed Care rule requires a similar payment analysis annually. This year’s survey asked states whether they have conducted comparative rate analyses of FFS Medicaid payment rates within the last two years.

FFS Analysis

More than one-third of responding states (19 of 50) reported conducting a comparative rate analysis of FFS Medicaid payment rates that included primary care, OB/GYN, and outpatient MH/SUD services within the last two years (Figure 13). An additional eleven states reported conducting an analysis including one or two of the required provider types, while 20 states reported that they had not conducted an analysis of any of the three required provider types. Of the 30 states that had conducted a FFS comparative rate analysis (for at least one “required” provider type), over half benchmarked their FFS rates to Medicare rates. Several states reported benchmarking to a combination of Medicare and another benchmark (e.g., commercial rates and/or other states’ FFS rates). Many states also reported including other physician specialists and dental providers in their analyses. In addition to the various benchmarks used, there may be other methods states used for their comparative rate analyses that differ from those required in the final Access rule.

Provider Taxes

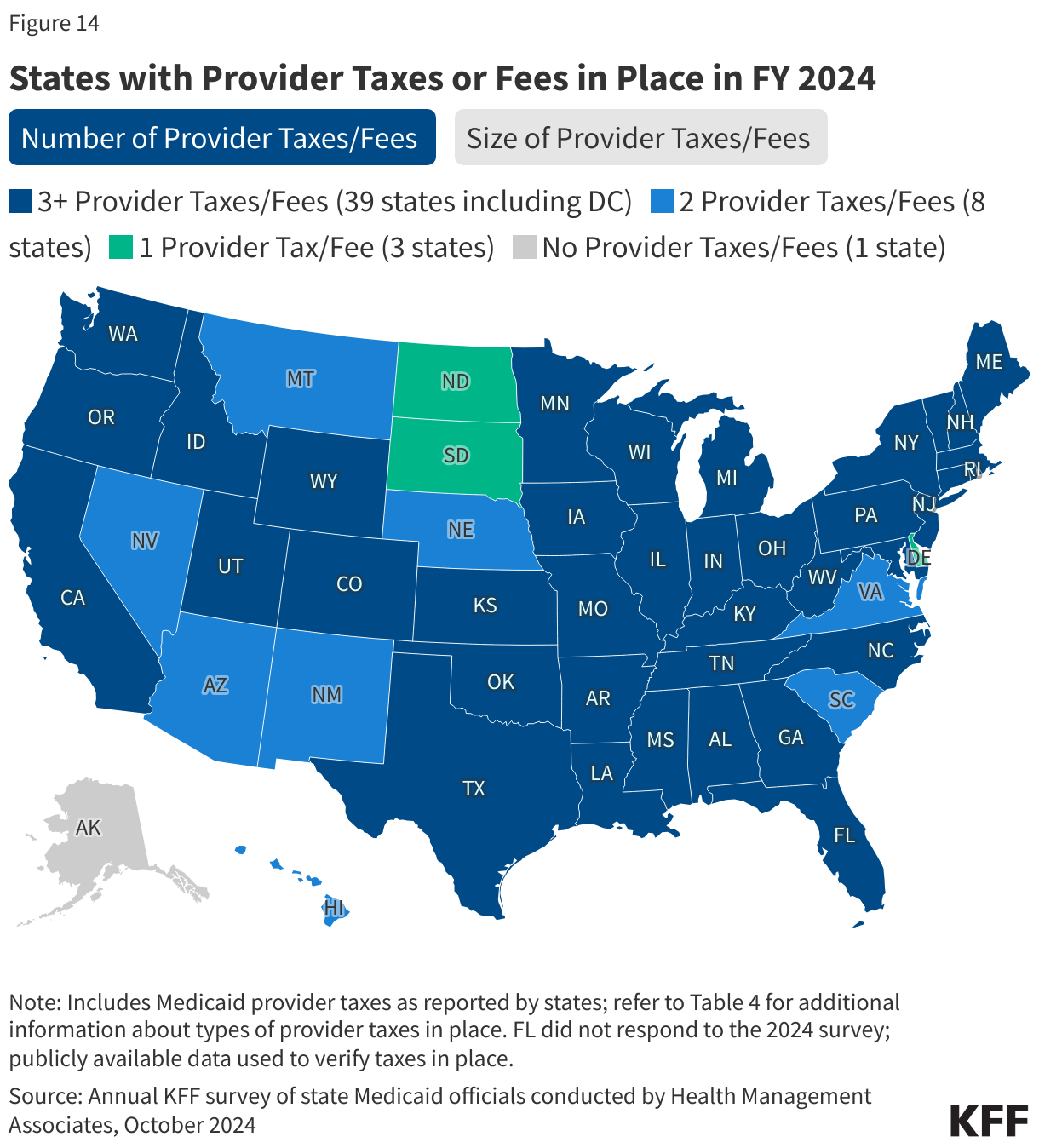

States continue to rely on provider taxes and fees to fund a portion of the non-federal share of Medicaid costs. Provider taxes are an integral source of Medicaid financing, comprising approximately 17% of the non-federal share of total Medicaid payments in FY 2018 according to the U.S. Government Accountability Office (GAO).21 At the beginning of FY 2003, 21 states had at least one provider tax in place. By FY 2013, all but one state (Alaska) had at least one provider tax or fee in place. In this year’s survey, states reported a continued reliance on provider taxes and fees to fund a portion of the non-federal share of Medicaid costs. In FY 2024, 39 states had three or more provider taxes in place, eight states had two provider taxes in place, and three states had one provider tax in place (Figure 14).22 As of July 1, 2024, 38 responding states reported at least one provider tax that is above 5.5% of net patient revenues, which is close to the maximum federal safe harbor or allowable threshold of 6%. Federal action to lower that threshold or eliminate provider taxes, as has been proposed in the past, would therefore have financial implications for many states.

Few states made or are making significant changes to their provider tax structure in FY 2024 or FY 2025 (Table 4). The most common Medicaid provider taxes in place in FY 2024 were taxes on nursing facilities (46 states) and hospitals (45 states), intermediate care facilities for individuals with intellectual disabilities (32 states), MCOs23 (20 states), and ambulance providers (17 states). Seven states reported plans to add new taxes in FY 2025 (Nebraska and New Mexico adding a hospital tax, Massachusetts and New York adding a managed care tax, and Oregon, South Carolina, and Wyoming adding an ambulance tax). Maine will eliminate both a critical access hospital tax and a service provider tax (on certain community support services providers) in FY 2025. Twenty-three states reported planned increases to one or more provider taxes in FY 2025. Missouri was the only state planning tax decreases in FY 2025, reporting planned decreases in two of its taxes.24