Key Facts About Medicare Part D Enrollment, Premiums, and Cost Sharing in 2024

The Medicare Part D program provides an outpatient prescription drug benefit to more than 50 million older adults and people with long-term disabilities in Medicare who enroll in private plans, including stand-alone prescription drug plans (PDPs) to supplement traditional Medicare and Medicare Advantage prescription drug plans (MA-PDs) that include drug coverage and other Medicare-covered benefits. This brief analyzes Medicare Part D enrollment and costs in 2024 and trends over time, based on data from the Centers for Medicare & Medicaid Services (CMS).

This analysis highlights the continuing growth of Medicare Advantage drug plans as a source of Part D drug coverage, with enrollment overall concentrated in a handful of large plan sponsors. Average premiums for drug coverage are much lower in MA-PDs than in stand-alone PDPs, mainly because most MA-PD enrollees are in zero-premium plans, which is in turn related to the ability of Medicare Advantage plan sponsors to use rebates to buy down the Part D premium. Median cost-sharing amounts for drugs covered on some formulary tiers are the same or similar in PDPs and MA-PDs, but PDP enrollees are more likely than MA-PD enrollees to face coinsurance for preferred brands and non-preferred drugs, while MA-PD enrollees face higher median coinsurance for specialty tier drugs.

These trends in Medicare Part D drug coverage and the costs that people with Medicare pay for drug plans and for their prescriptions are worth watching as provisions of the Inflation Reduction Act to improve the Part D benefit roll out, including a $35 insulin copay cap and a new out-of-pocket drug spending cap (set at $2,000 in 2025). Such changes will help to lower out-of-pocket costs for Part D enrollees but could also make it harder for some Part D plan sponsors to offer low-priced coverage, particularly sponsors of stand-alone drug plans. This could mean fewer affordable PDP plan choices for Medicare beneficiaries in traditional Medicare and further tilt Medicare enrollment towards Medicare Advantage, which has broader implications for Medicare program spending.

Medicare Advantage drug plans continue to attract more enrollees compared to stand-alone drug plans

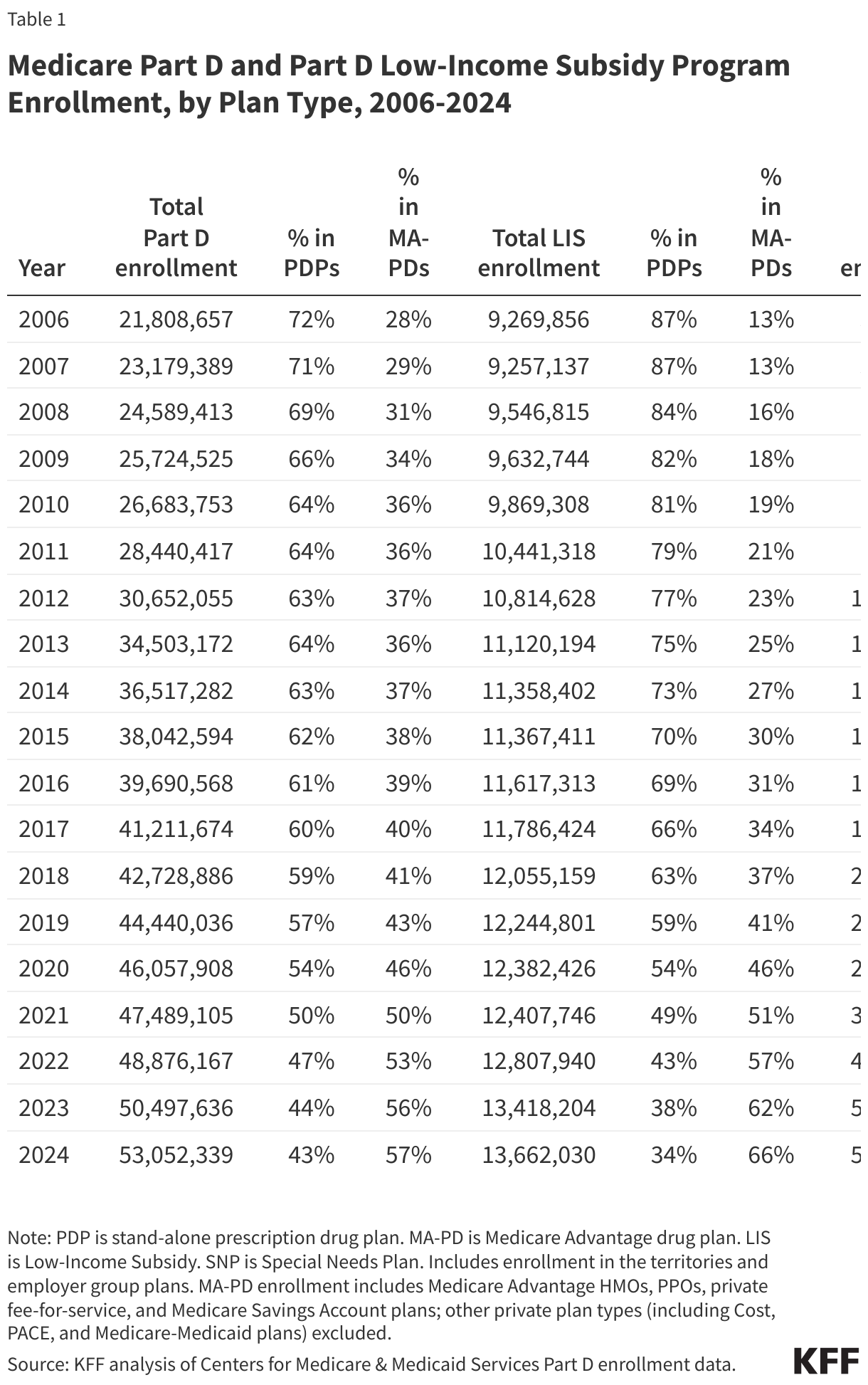

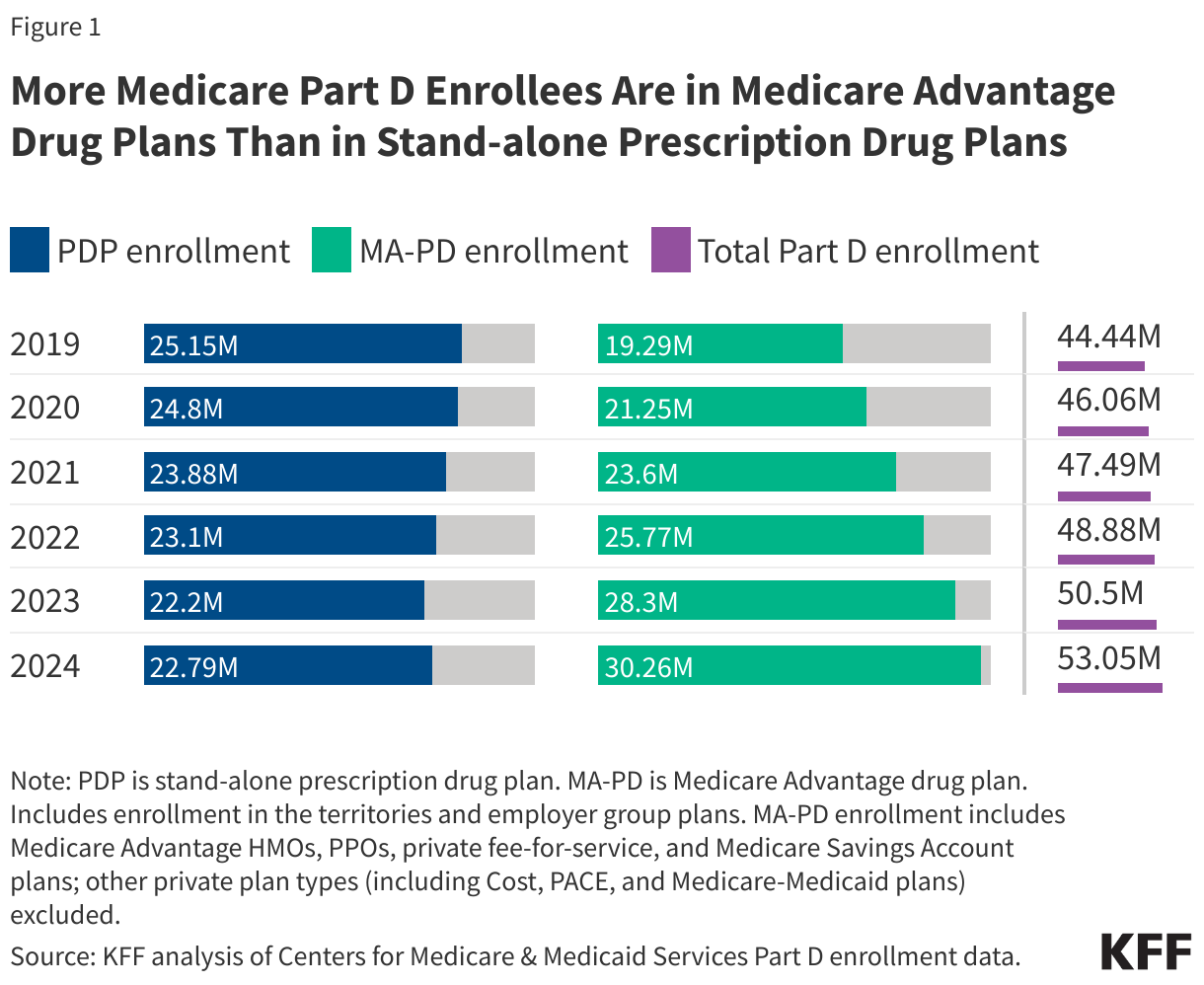

Well over half (57%) of Part D enrollees in 2024 are in Medicare Advantage drug plans, continuing a trend of increasing enrollment in Medicare Advantage plans and declining or relatively static enrollment in stand-alone prescription drug plans (Figure 1).

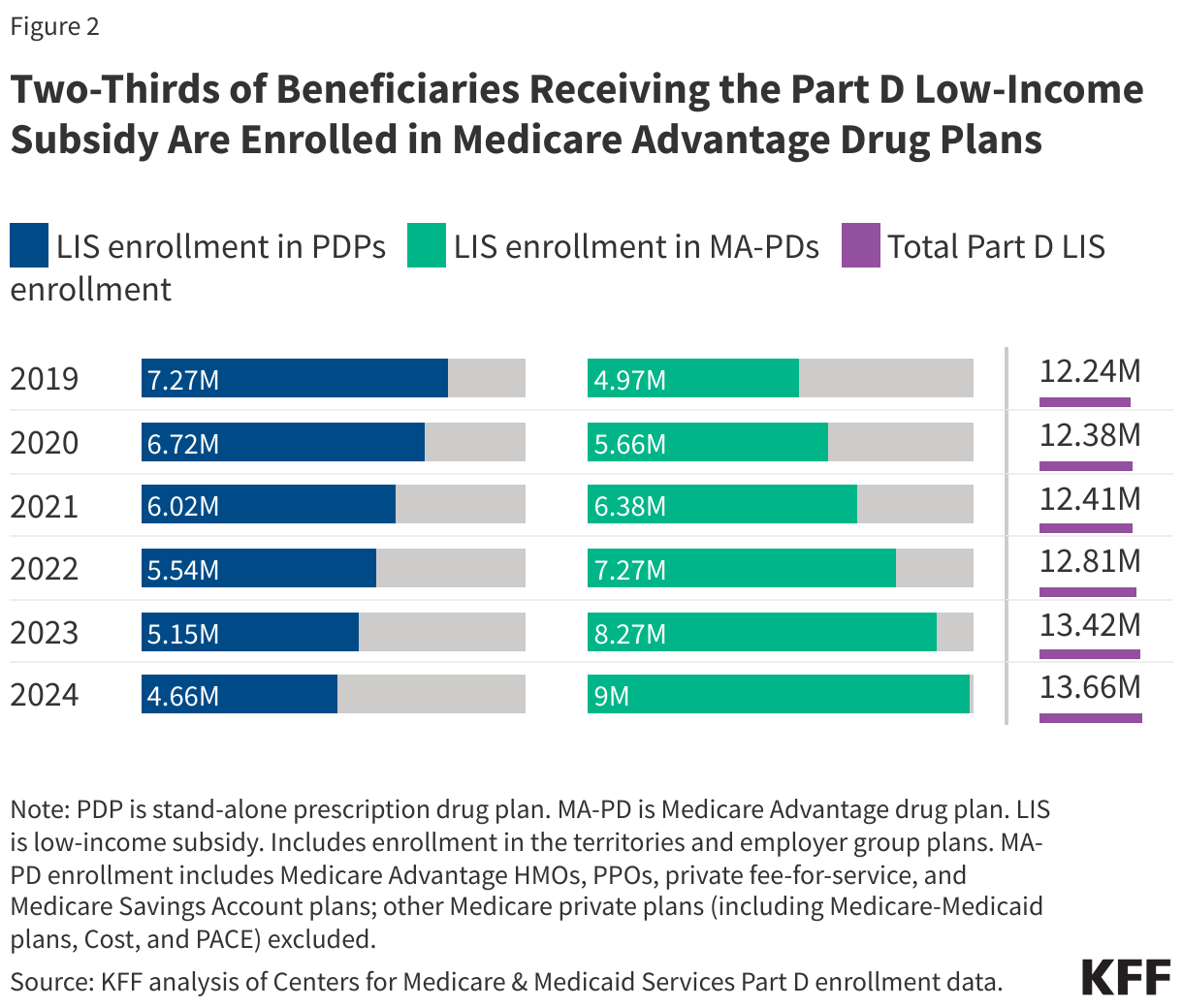

Low-Income Subsidy enrollment is tilted even more towards Medicare Advantage drug plans than overall Part D enrollment

Two-thirds of LIS enrollees – 9 million out of 13.7 million – are enrolled in Medicare Advantage drug plans in 2024 (Figure 2). Nearly 6 million LIS enrollees are in Medicare Advantage Special Needs Plans (SNPs), nearly all of which (95%) are in plans designed specifically for dual-eligible individuals (Table 1). On average, LIS enrollees can choose from substantially more MA-PDs than PDPs in their area that have drug premiums below the regional low-income subsidy premium benchmark amount – 15 MA-PDs versus 3 PDPs – meaning they can enroll in these plans for zero premium.

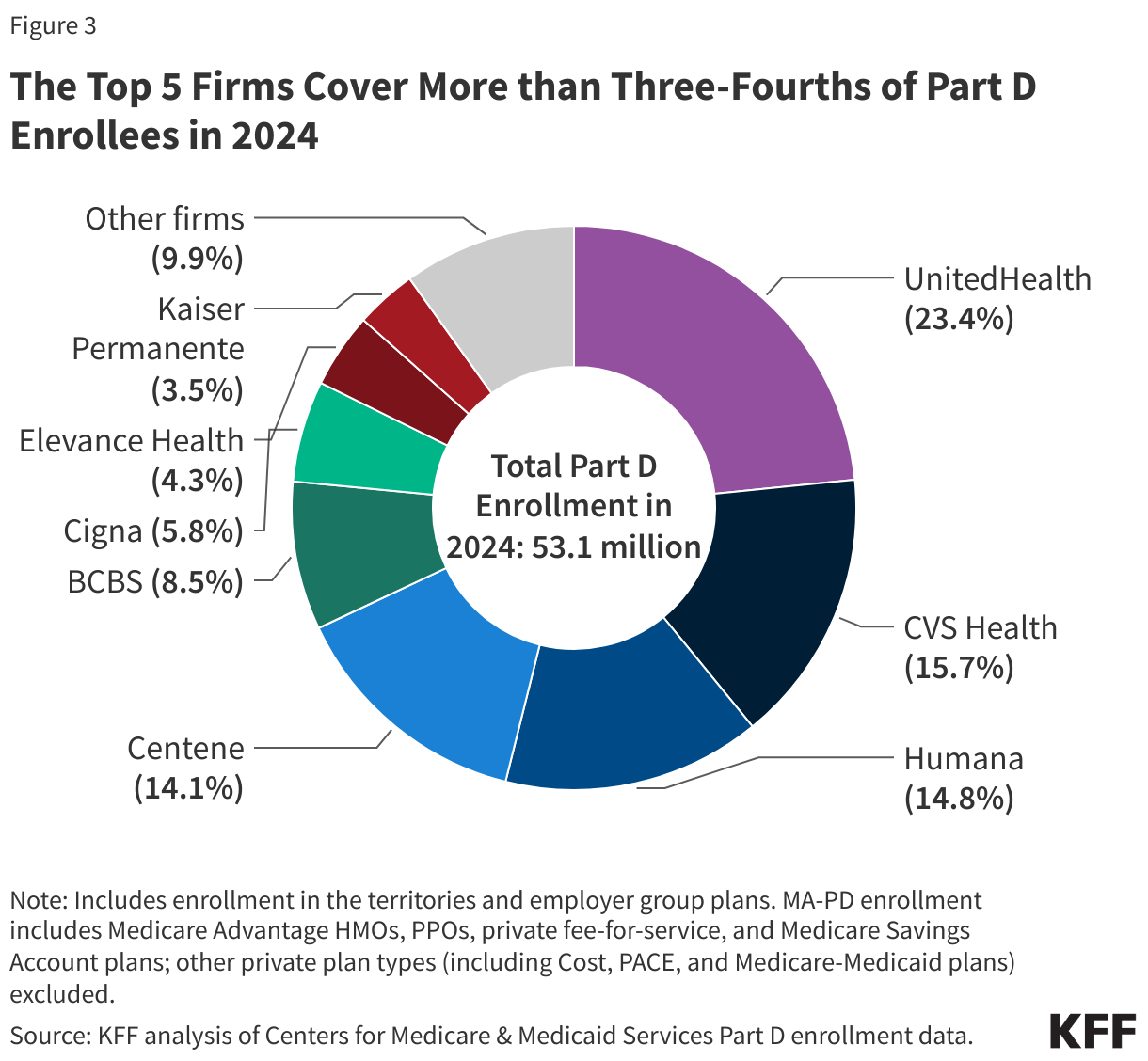

The top 5 firms cover more than three-fourths of Part D enrollees in 2024

Part D enrollment is concentrated in a handful of top plan sponsors, with 5 firms covering 77% of all Part D enrollees in 2024, or 40.1 million out of 53.1 million enrollees (Figure 3). Nearly 1 in 4 enrollees (12.4 million) are in Part D plans sponsored by UnitedHealth, including both stand-alone PDPs and MA-PDs. CVS, Humana, and Centene each have around 15% of the Part D market, with enrollees in both types of Part D plans.

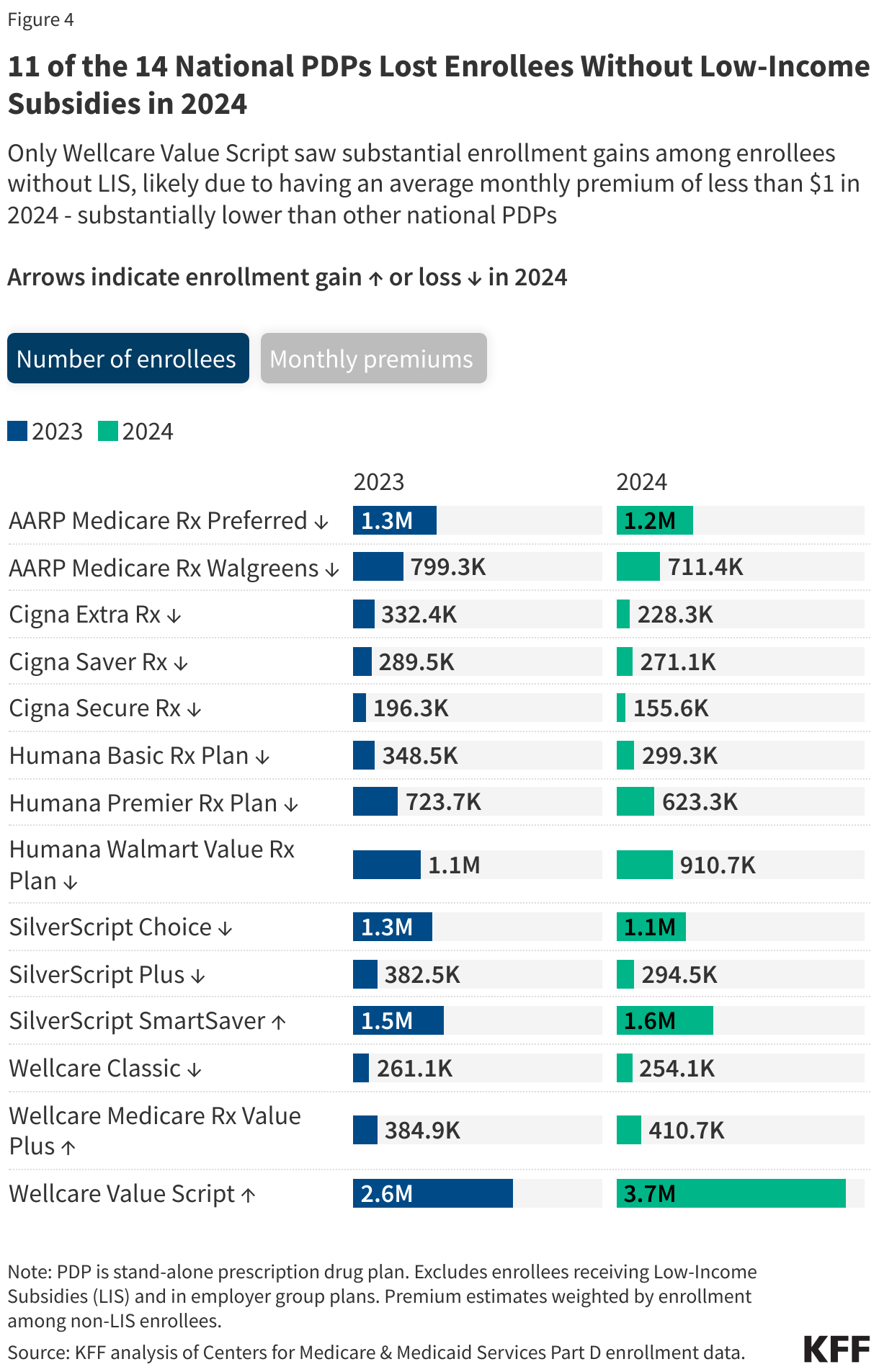

Enrollment among beneficiaries without low-income subsidies declined in 11 of the 14 national PDPs in 2024

Most of the national PDPs available in 2024 lost enrollment among beneficiaries without low-income subsidies (Figure 4). Only Wellcare Value Script saw substantial enrollment gains among enrollees without LIS – from 2.6 million to 3.7 million – likely due to having a median monthly premium of less than $1, substantially lower than all other national PDPs.

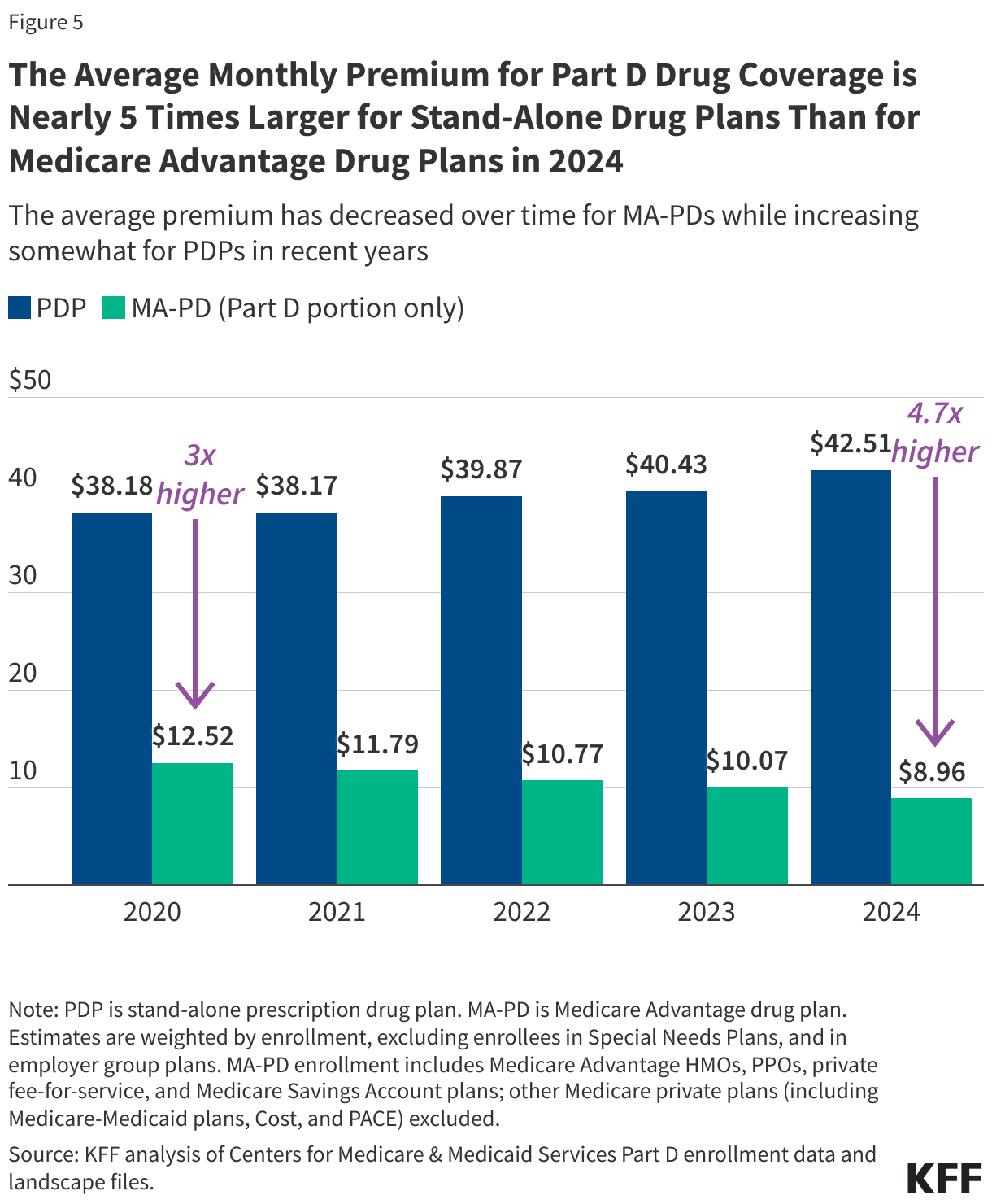

The average monthly premium for Part D coverage is nearly 5 times larger for PDPs than for MA-PDs

On average, PDP enrollees pay substantially more each month for their Part D drug coverage than enrollees in Medicare Advantage drug plans. The average monthly PDP premium is $43, nearly 5 times higher than the $9 average monthly premium for drug coverage in MA-PDs (weighted by enrollment) (Figure 5; Table 2). (The total average premium for MA-PDs, including all Medicare-covered benefits, is $14 per month in 2024.)

The difference between average monthly premiums for drug coverage offered by PDPs and MA-PDs has been growing larger, with the PDP average rising and the MA-PD average falling. The average premium for drug coverage in MA-PDs is heavily weighted by zero-premium plans because MA-PD sponsors can use rebate dollars from Medicare payments to lower or eliminate their Part D premiums. Rebates to Medicare Advantage plans have more than doubled since 2018 and now exceed $2,000 per year per beneficiary.

The $43 weighted average PDP premium, based on current enrollment after the end of the open enrollment season for 2024, is lower than the estimated $48 monthly PDP premium for 2024, which was based on enrollment in June 2023 and did not account for plan switching by current enrollees or plan choices by new enrollees during the open enrollment period. Taking into account plan switching and new enrollment into lower premium plans resulted in the lower enrollment-weighted average monthly premium for 2024. Rather than an estimated increase of 21% over the 2023 average premium (from $40 to $48), the actual increase is 5% (from $40 to $43).

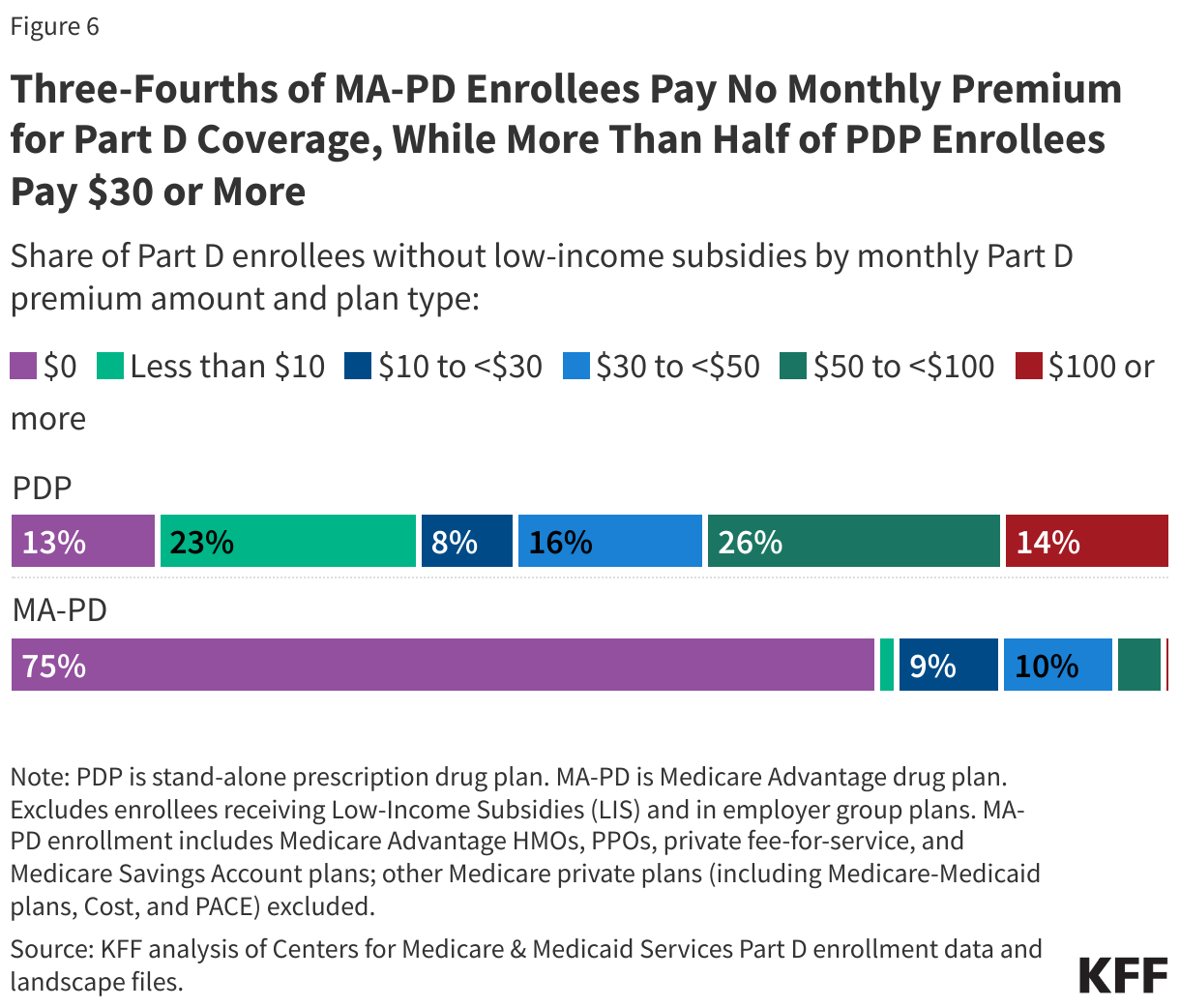

Most Medicare Advantage drug plan enrollees pay no premium for their drug coverage, while more than half of PDP enrollees pay $30 per month or more

Three-fourths of MA-PD enrollees without low-income subsidies pay no monthly premium for Part D coverage in 2024, while more than half of PDP enrollees without LIS (56%) pay $30 or more – including 1 in 7 PDP enrollees without the LIS who pay at least $100 per month for their Part D plan (Figure 6). For 2024, all Medicare beneficiaries had access to zero-premium MA-PD plans – 27 on average – whereas only 1 PDP was available for zero premium for non-LIS enrollees in only 14 out of 34 PDP regions.

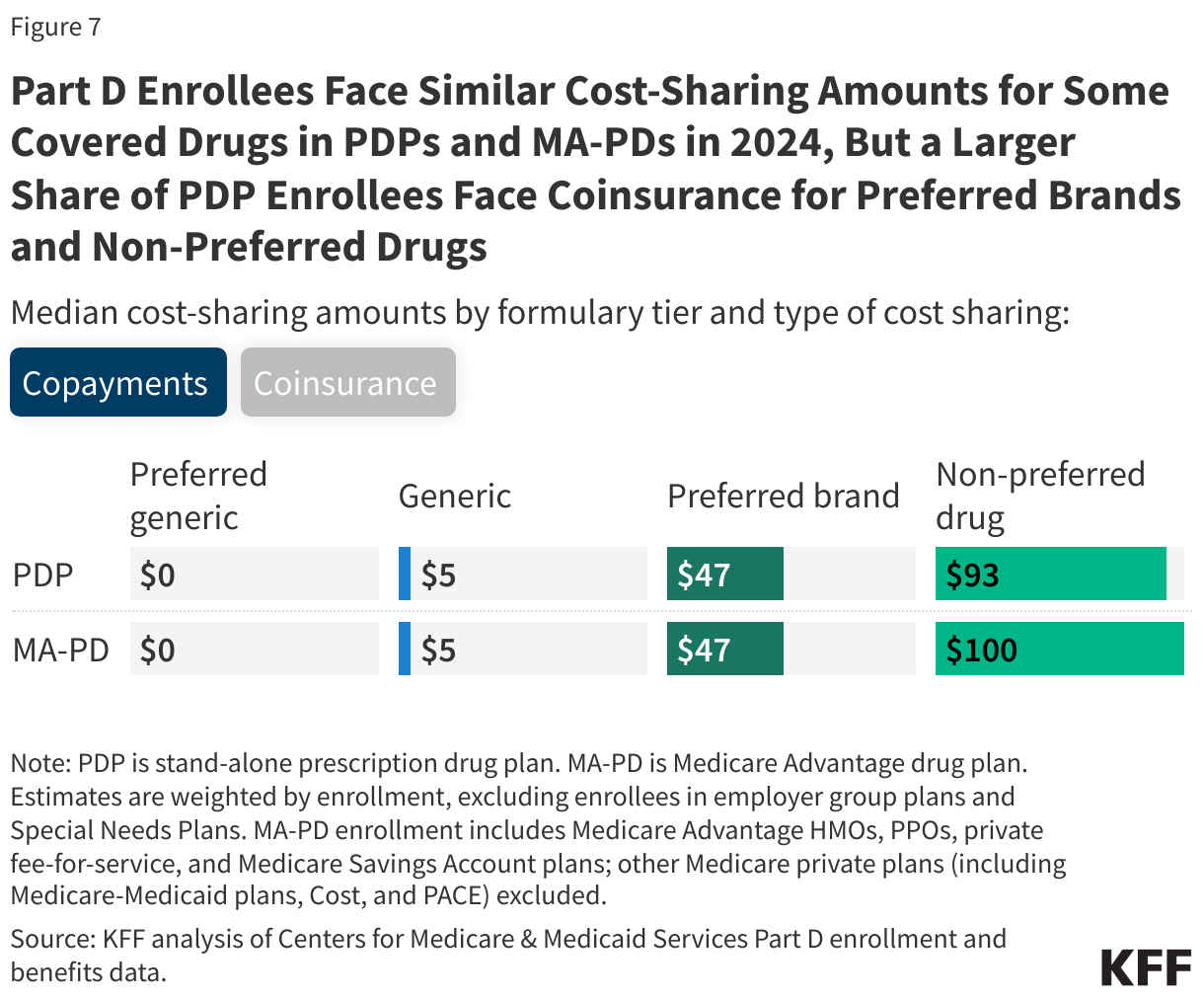

PDP enrollees are more likely than MA-PD enrollees to face coinsurance for preferred brands and non-preferred drugs, while MA-PD enrollees face higher median coinsurance for specialty tier drugs

As in previous years, Part D enrollees face low copayments for generic drugs and higher cost-sharing amounts for preferred brands, non-preferred drugs, and specialty drugs, regardless of whether they are in PDPs or MA-PDs (Figure 7). Median cost-sharing amounts for drugs covered on some formulary tiers are the same or similar in PDPs and MA-PDs, but PDP enrollees are much more likely than MA-PD enrollees to pay coinsurance, or a percentage of a drug’s price, for preferred brands and non-preferred drugs. Whereas nearly all MA-PD enrollees face a median copay of $47 for preferred brands, most PDP enrollees face median coinsurance of 22%; for non-preferred drugs, MA-PD enrollees face a median copay of $100 while PDP enrollees face coinsurance of 47%.

Median coinsurance for specialty tier drugs (those that cost over $950 in 2024) is higher for MA-PD enrollees than PDP enrollees – 33% vs. 25%. Plans that waive some or all of the standard deductible – which is the case for most MA-PDs – are permitted to set the specialty tier coinsurance rate above 25%.

These cost-sharing amounts apply when beneficiaries fill prescriptions in the initial coverage phase of the Part D benefit. As of 2024, through a provision in the Inflation Reduction Act, beneficiaries no longer face cost sharing in the catastrophic coverage phase of the Part D benefit, which translates to a cap of about $3,300 out of pocket for brand-name drugs. In 2025, Medicare beneficiaries will pay no more than $2,000 out of pocket for prescription drugs covered under Part D.

Juliette Cubanski is with KFF. Anthony Damico is an independent consultant.