2025 Medicare Advantage Plan Choices are Stable, Following Years of Steady Growth

Note: This analysis was updated on November 25th to reflect the October version of the 2025 CMS Landscape file. For more information, please see: Medicare Advantage 2025 Spotlight: A First Look at Plan Offerings | KFF and Medicare Advantage 2025 Spotlight: A First Look at Plan Premiums and Benefits | KFF

In the months leading up to the Medicare annual open enrollment period that runs from October 15th through December 7th, there were questions about how modifications to the payment formula and higher utilization would impact the number of Medicare Advantage plans that would be offered in 2025. A review of the plans available for individual enrollment shows that the total number of plans declined by 6% (from 3,959 to 3,719). Some reports have suggested that this translates into a dramatic drop in the number of plans available to the average Medicare beneficiary. However, taking a closer look, the Medicare Advantage market appears relatively stable.

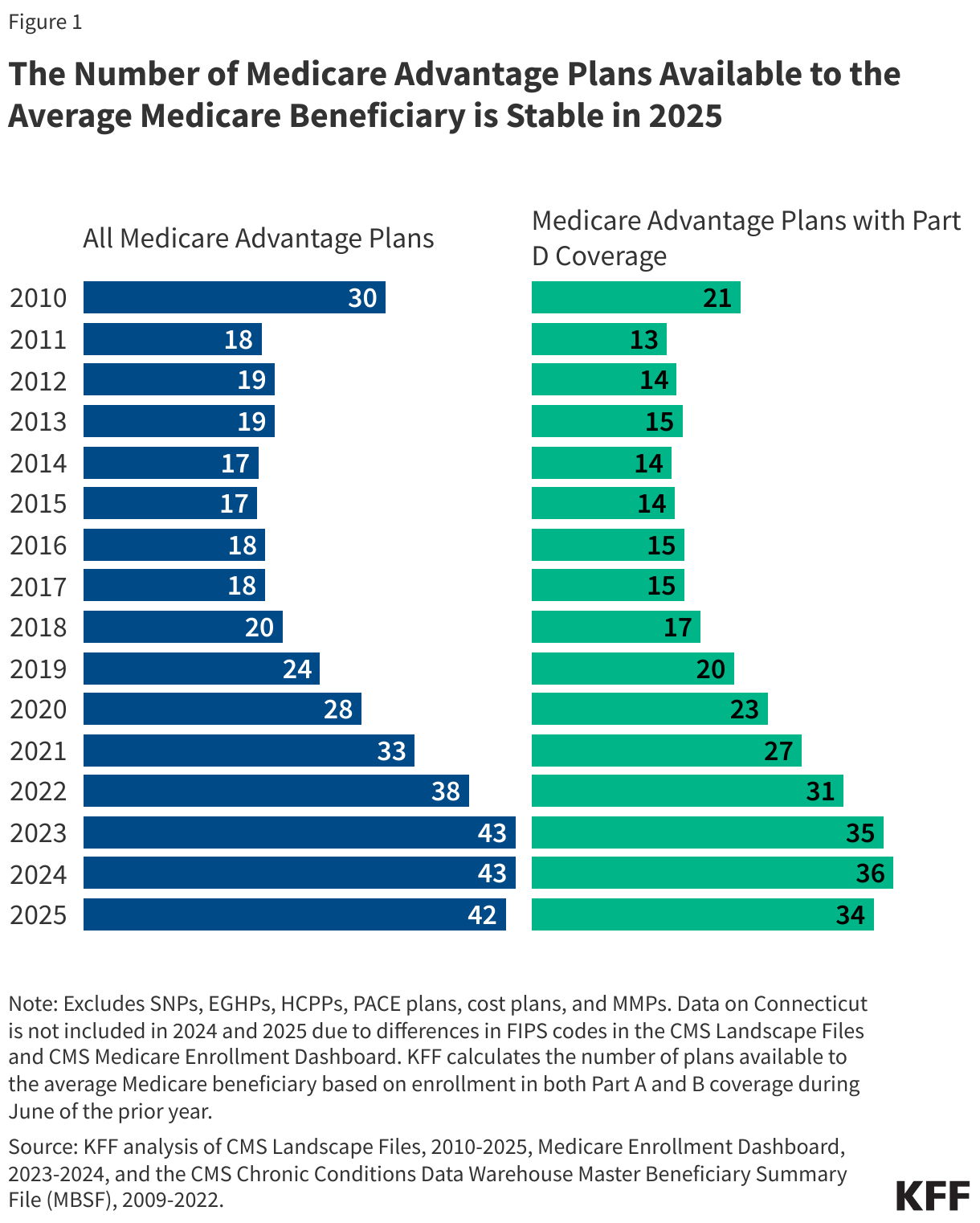

KFF analysis finds the average Medicare beneficiary will have the option of 34 Medicare Advantage prescription drug (MA-PD) plans in 2025, just 2 fewer than the 36 options available in 2024 (Figure 1). Across all plans for individual enrollment, including those with and without prescription drug coverage, the average beneficiary has 42 options in 2025, compared to 43 options in both 2023 and 2024. Since 2018, the number of plans available to the average beneficiary has doubled.

While a full KFF analysis of plan offerings and benefits will follow, at a high level, 2025 looks similar to 2024 in terms of plan choice.

-

The average Medicare beneficiary has access to plans offered by 8 different firms in 2025, the same as in 2024, and an increase of 2 firms since 2018.

Virtually all enrollees (99%) also have access to at least one zero premium plan that includes prescription drug coverage, consistent with recent years and substantially higher than the 84% in 2018.

The decrease in the total number of Medicare Advantage plans means that some Medicare beneficiaries will find that their current coverage is no longer an option for next year. In most cases, these beneficiaries live in counties where they will continue to have a myriad of Medicare Advantage plan options, potentially including some from the same insurer for the plan in which they are currently enrolled. In some cases, people will be moved into a new plan under the same insurer automatically if the contract includes another plan of the same type (i.e., HMO or PPO) in the same county. Others will have to make an active choice about their Medicare coverage if they wish to enroll in another Medicare Advantage plan.

Though higher than in previous years, a relatively small number of Medicare Advantage beneficiaries are enrolled in a plan in 2024 that has been terminated for the coming year and will not be automatically assigned to a new plan. People in this group will be able to enroll in another Medicare Advantage plan if one is available or choose traditional Medicare. If they choose traditional Medicare, they will qualify for a special enrollment period for Medigap with guaranteed issue rights, meaning they can switch to traditional Medicare and will not be denied a Medigap policy due to a pre-existing condition.

Every year, Medicare Advantage plans change in ways that could be important to enrollees, including the scope and generosity of extra benefits, cost sharing for Medicare-covered benefits, rules for using covered services (such as referral requirements and prior authorization), drug formularies, and provider networks. Despite these changes, most Medicare beneficiaries report that they do not compare coverage options on an annual basis. While reviewing the various features of plans can be daunting, beneficiaries can take some comfort in the stability of the Medicare Advantage market in terms of the number of plans available to them in 2025.