A Look at Medicaid Enrollment and Finances of the Five Largest Medicaid Managed Care Plans

Centene, CVS Health, Elevance, Molina, and UnitedHealth are the five largest publicly traded companies (also referred to as “parent” firms) operating Medicaid MCOs, accounting for half of Medicaid MCO enrollment nationally. During the unwinding of the pandemic-era Medicaid continuous enrollment provision, millions of people were disenrolled and states and plans have faced considerable rate setting uncertainty. Firms report current capitation rates do not align with higher member risk and utilization patterns, and many states have sought federal approval to adjust rates to address these shifts. As we look ahead, shifts in state fiscal conditions and talks in Congress about cutting federal Medicaid spending could result in the reductions in Medicaid funding with implications for coverage as well as plans and providers. While plans confront continued uncertainty looking ahead, plan attention and scrutiny has intensified in the aftermath of the killing of UnitedHealthcare’s CEO, Brian Thompson. Within this broad context, this brief examines enrollment and financial data through the end of September 2024 from quarterly company earnings reports and calls, financial filings, and other company materials as well as from national administrative data. Key findings include:

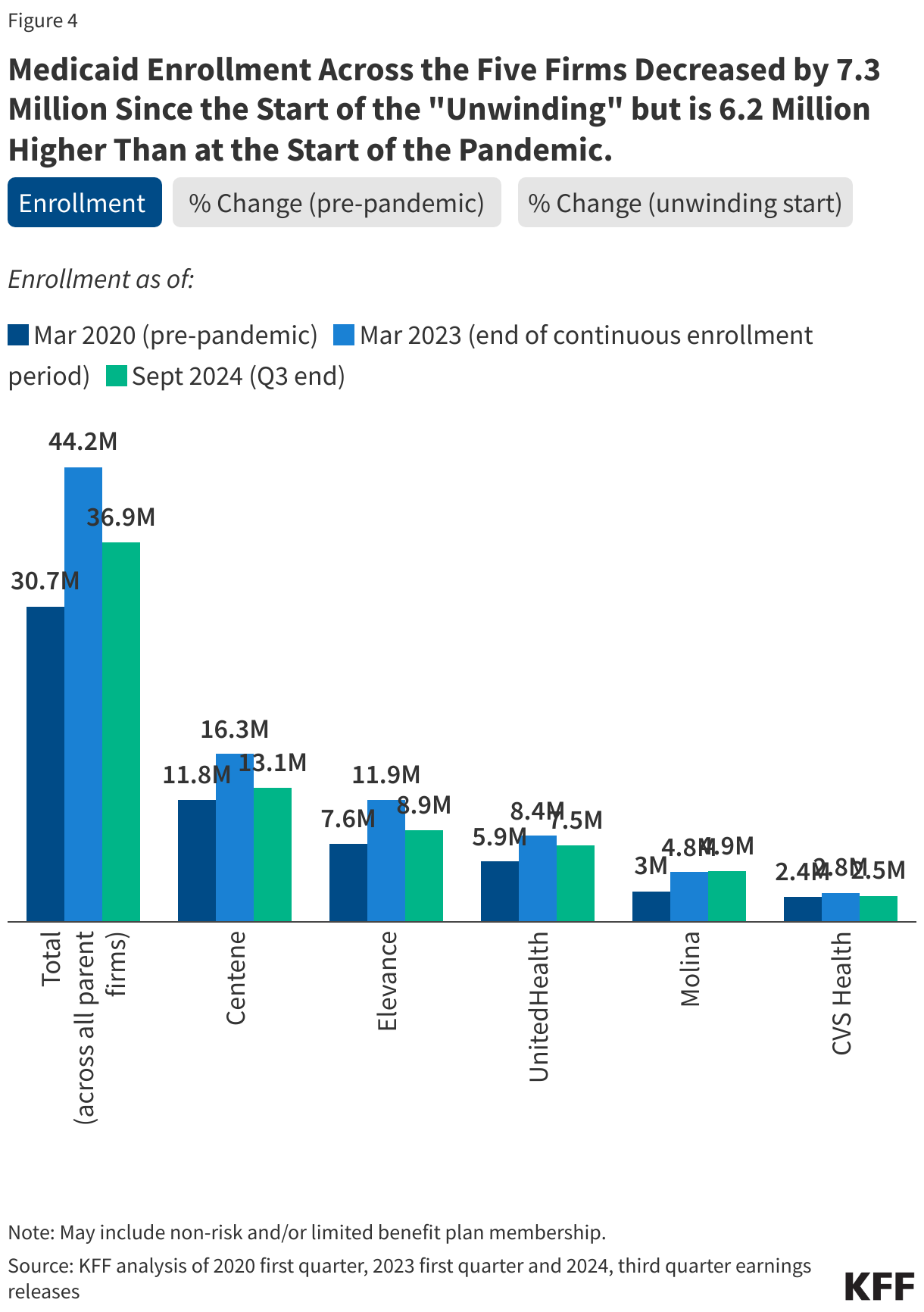

- Medicaid enrollment. As of September 2024, combined Medicaid enrollment across the five firms was 6.2 million (or 20%) higher than enrollment at the start of the pandemic. However, Medicaid enrollment across the firms declined by more than 7 million since March 2023 (just before the “unwinding” began). Medicaid membership as a share of total medical membership has declined for all five firms.

- Medicaid revenue and MLRs. While the three firms that reported Medicaid-specific revenues (Centene, Molina, and UnitedHealth) reported growth in Medicaid revenue in the first nine months of 2024 compared to the same period in 2023, the two firms that reported Medicaid medical loss ratios (MLRs) (percentage of premium revenue spent on medical care costs) reported higher Medicaid MLRs in 2024 (Q1-Q3) compared to 2023 (Q1-Q3), implying a potential decrease in profitability.

- Member acuity and utilization trends. During Q3 2024 earnings calls, firms reported higher member acuity (i.e., average risk profile) due to unwinding redeterminations as well as increased utilization trends in 2024. Higher acuity could be related to a number of factors including that during the unwinding people with higher health care needs were less likely to be disenrolled. Firms say that the Medicaid rate updates they have received (from states) fall short of covering current acuity and cost trends. This could put upward pressure on Medicaid spending at a time when Congress may consider cuts in federal Medicaid contributions.

Medicaid enrollment in the five largest publicly traded companies operating Medicaid MCOs

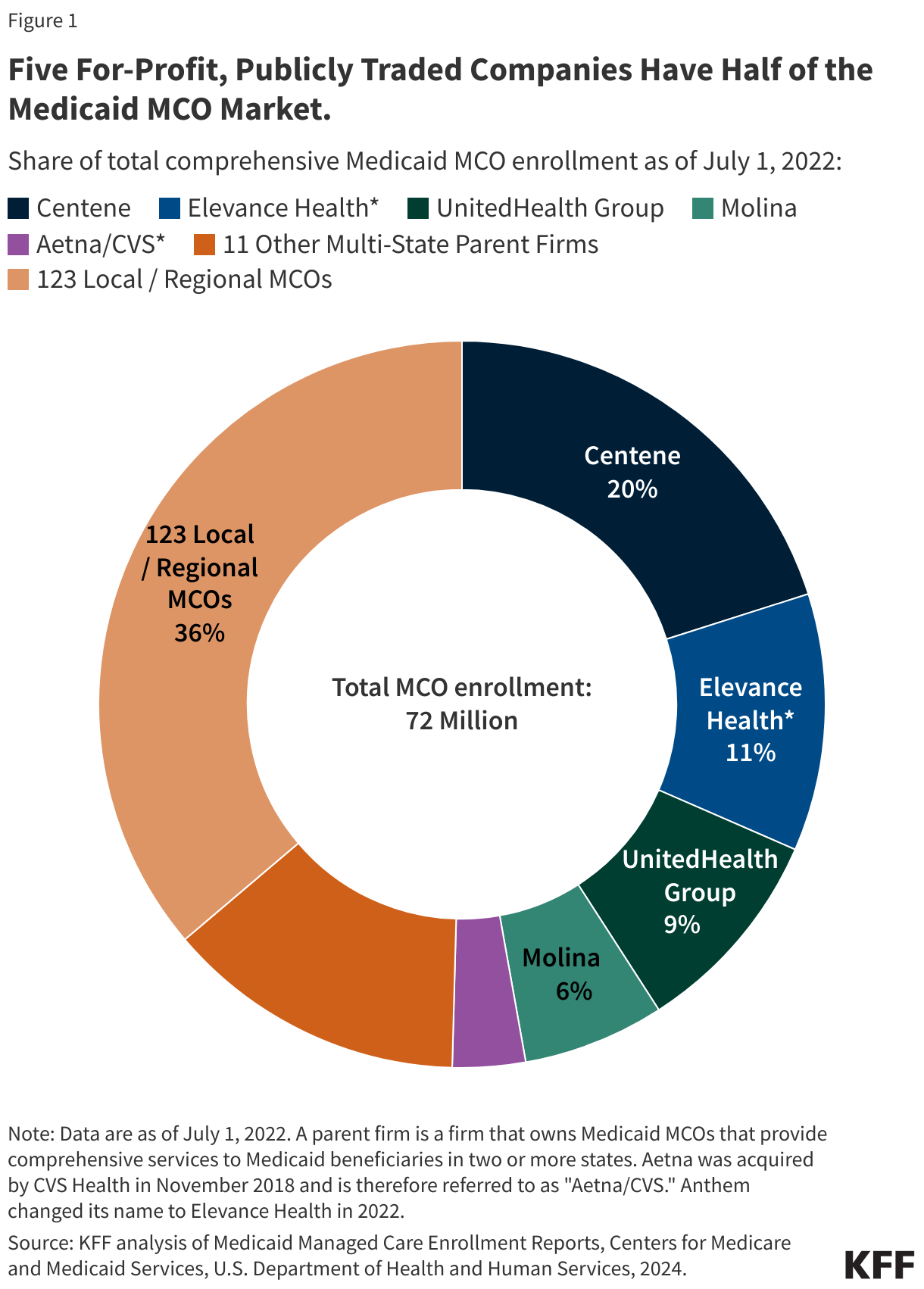

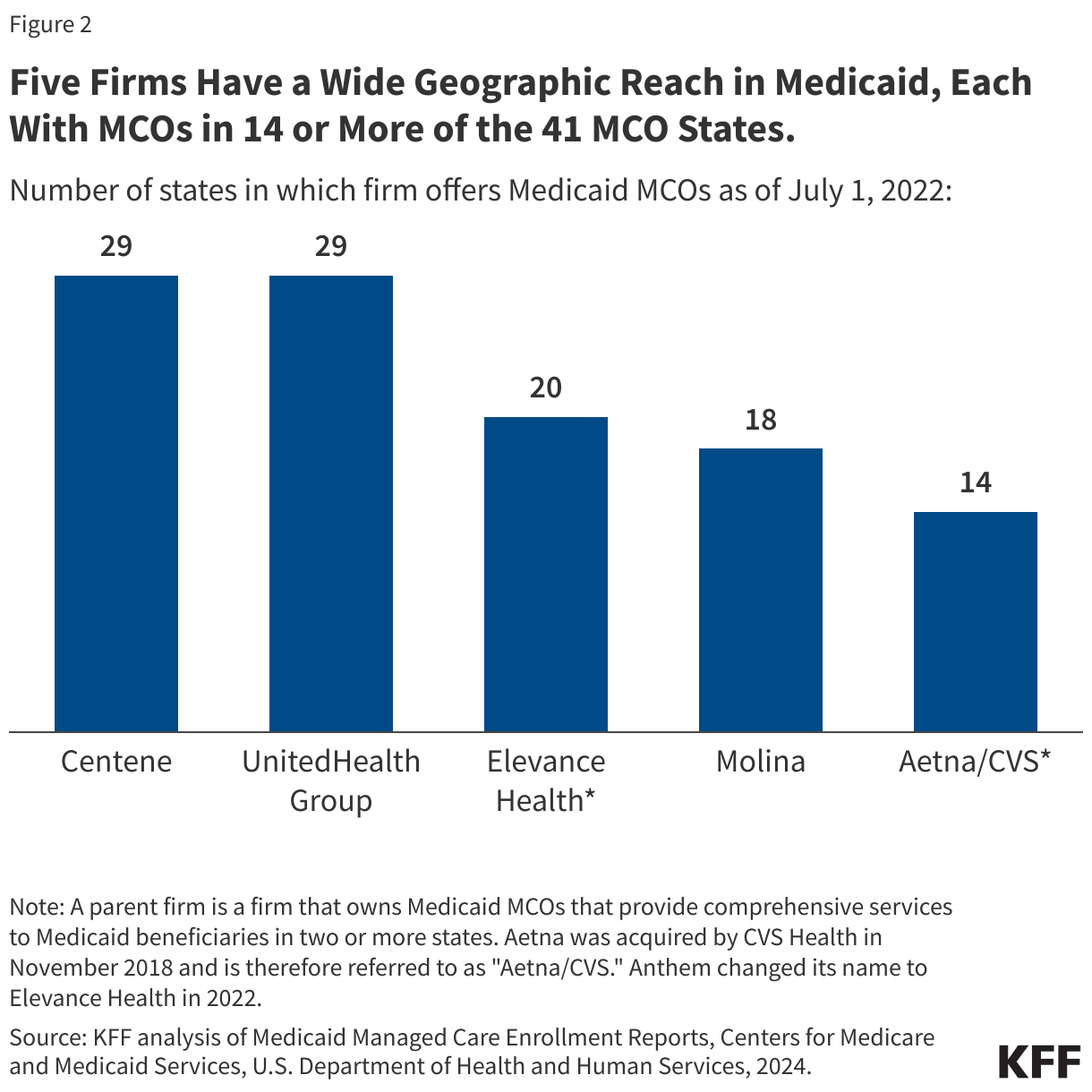

Five for-profit, publicly traded companies – Centene, Elevance (formerly Anthem), UnitedHealth Group, Molina, and CVS Health – account for 50% of Medicaid MCO enrollment nationally (Figure 1). All five are ranked in the Fortune 500. Each company operates Medicaid MCOs in 14 or more states (Figure 2).

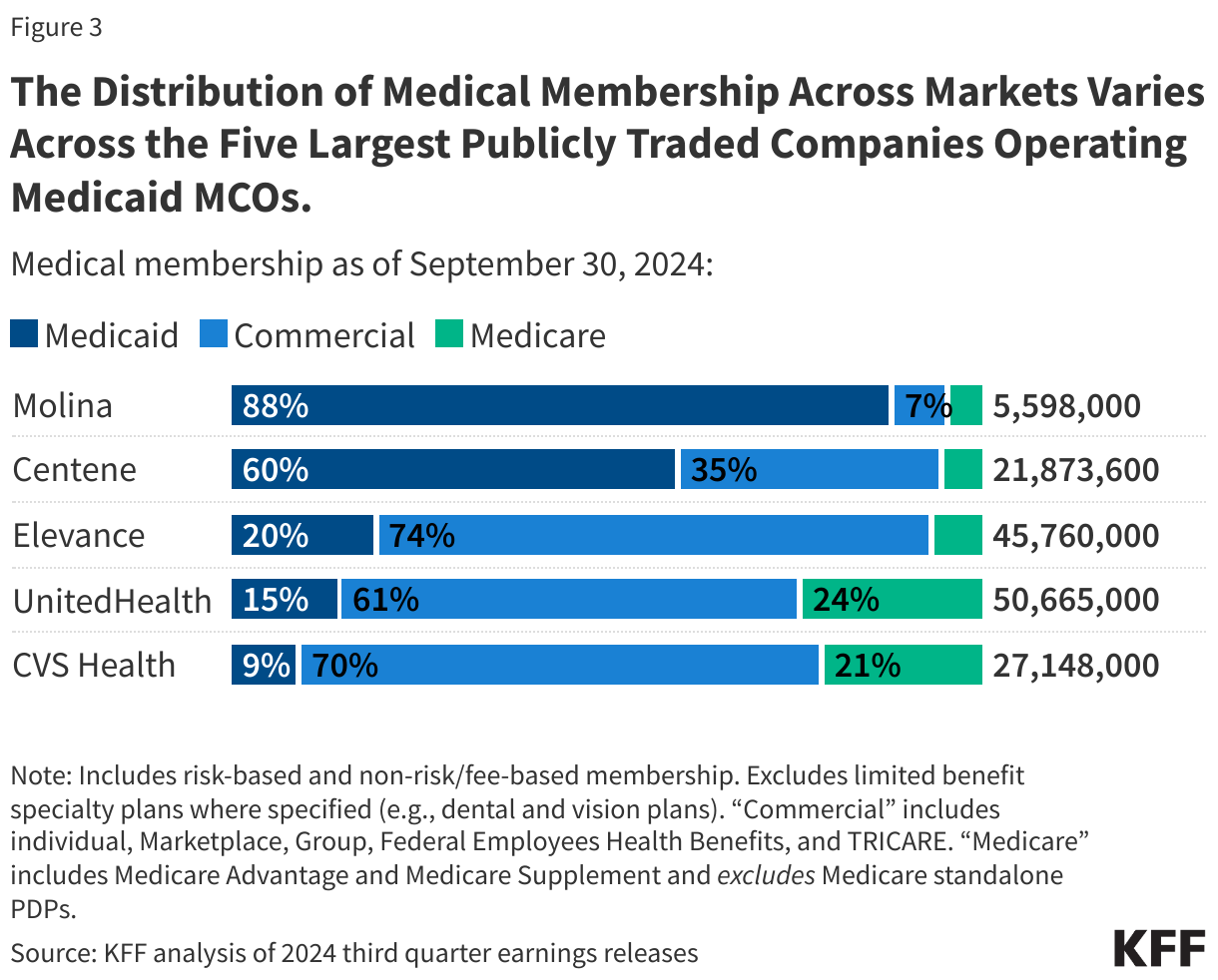

All five firms also operate in the commercial and Medicare markets (Figure 3); however, the distribution of membership across markets varies across firms. Two firms – Molina and Centene – have historically focused predominantly on the Medicaid market. Medicaid members accounted for nearly 90% of Molina’s overall medical membership and about 60% of Centene’s medical membership as of September 2024 (Figure 3). Since March 2023 (just before unwinding began), Medicaid membership as a share of total medical membership has declined for all five firms, ranging from a decline of about 1 percentage point for UnitedHealth to 8 percentage points for Centene. The unwinding may have contributed to membership distribution shifts.

Despite a combined 7.3 million decline in enrollment during the unwinding, Medicaid enrollment across the five firms remains higher by 6.2 million (or 20%) compared to enrollment at the start of the pandemic (Figure 4). In comparison, national data show total Medicaid/CHIP enrollment in September 2024 was 11% higher than Medicaid/CHIP enrollment in February 2020, prior to the pandemic. These changes in “net” enrollment reflect the people who are dropped from Medicaid as well as those who newly enroll, and those who re-enroll within a short timeframe following disenrollment, also known as “churn.” Changes in parent firm enrollment also reflect activity including firm acquisitions or sales and new or lost Medicaid contracts.

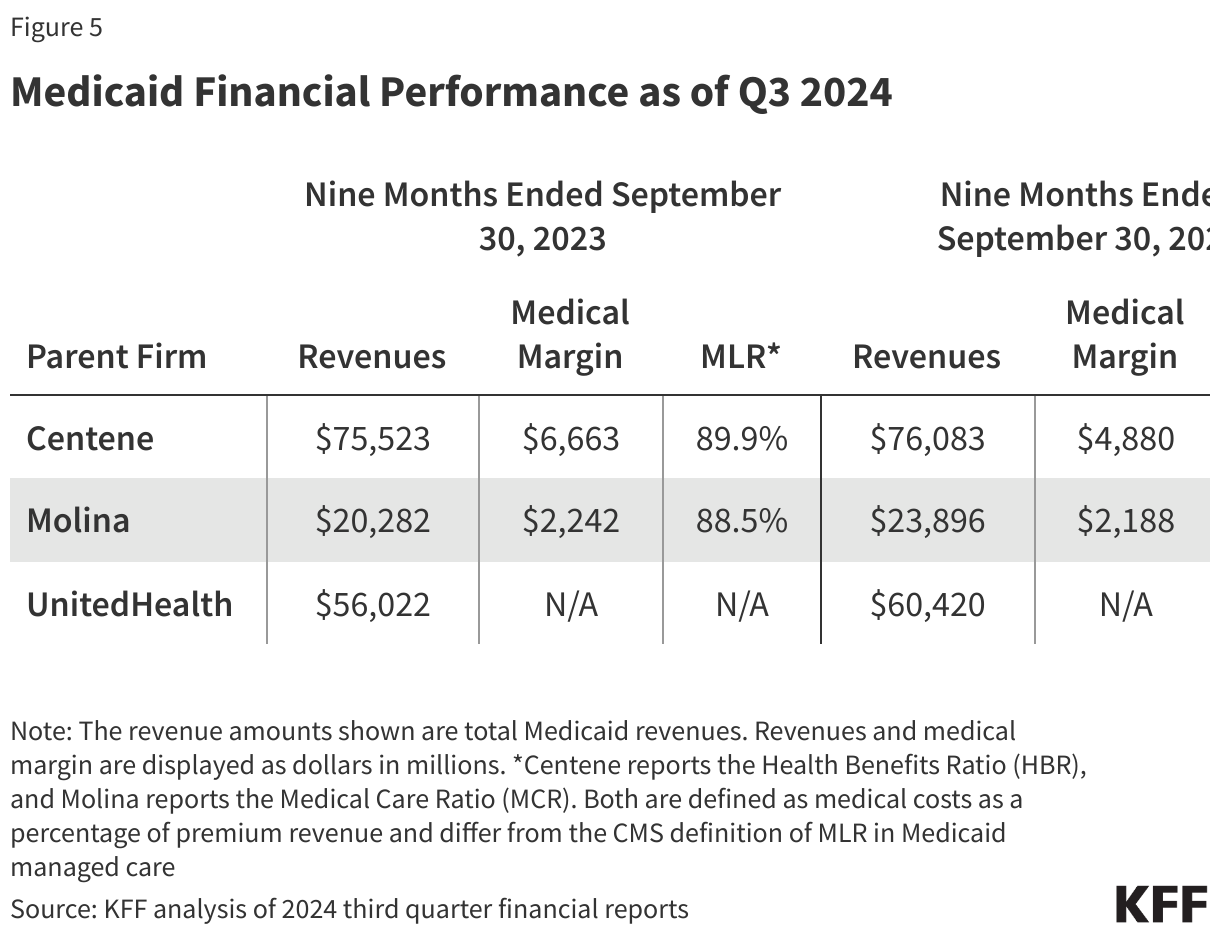

While some firms report growth in Medicaid revenue through the end of September 2024, other measures of financial performance (gross margins and medical loss ratios) show a potential decrease in profitability (Figure 5). Even accounting for enrollment declines due to the unwinding, the three firms that report Medicaid-specific financial information through Q3 (UnitedHealth, Molina, and Centene) reported growth in Medicaid revenue in the first nine months of 2024 compared to the same period in 2023. For the first nine months of 2024, medical margins (the amount by which premium revenue exceeds medical costs) earned by the Medicaid segment declined by 27% for Centene and 2% for Molina when compared to the same period in 2023, and Medicaid simple medical loss ratios (medical costs as a share of premium revenue) increased for Centene from 89.9% to 92.3% and for Molina from 88.5% to 90.3%, implying a potential decrease in profitability.

Impact of unwinding for the five largest publicly traded companies operating Medicaid MCOs

During Q3 2024 earnings calls, firms reported current capitation rates do not align with increased Medicaid medical cost trends. Capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit (see Box 1). Plan capitation rates, usually for a 12-month rating period, are set using baseline utilization and cost data from prior periods (which can lag one to two years, to allow claims to complete) trended forward to determine per member per month payment amounts. States may also use different mechanisms to adjust plan risk (e.g., to ensure payments are not too high or too low), including risk-sharing arrangements (see Box 1). During Q3 2024 earnings calls, firms reported higher member acuity (i.e., average risk profile) due to unwinding redeterminations as well as increased utilization trends in 2024. Specifically, firms pointed to increased utilization of behavioral health care, pharmaceuticals (including GLP-1s), and long-term services and supports (LTSS).

A recent analysis conducted by Wakely, a consulting firm with actuarial expertise, highlights many states have recently implemented program changes to improve access to care (e.g., increasing provider rates, implementing limitations to prior authorization, etc.), which can affect utilization trends and put upward pressure on per person costs. Wakely notes that these program changes may be adding complexity to an “already challenging year for capitation rate setting.”

Parent firms expect the misalignment between rates and emerging acuity and cost/utilization trends is temporary but may extend through 2025. In a 2024 KFF survey of Medicaid directors, about two-thirds of responding MCO states reported seeking CMS approval for a capitation rate amendment to address shifts in the average risk profile (or “acuity”) of MCO members in FY 2024 and/or FY 2025. During earnings calls, firms say that the rate updates they have received fall short of covering current acuity and cost trends. Parent firms also report continuing discussions with states on adjustments to 2024 rates and on the development of 2025 rates (which often renew on January 1 or July 1). Centene and Elevance reported sharing current experience / trend data with states to inform these discussions.

Box 1: Medicaid Managed Care Capitation Rate Setting

MCOs are at financial risk for services covered under their contracts, receiving a per member per month “capitation” payment for these services. While plans set rates in the commercial and Medicare Advantage markets, Medicaid managed care rates are developed by states and their actuaries and reviewed and approved by CMS. Under federal law, payments to Medicaid MCOs must be actuarially sound. Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Unlike fee-for-service, capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit.

In developing actuarially sound rates, states must follow accepted actuarial methods and specific federal requirements outlined in regulations and other guidance. Plan rates, usually for a 12-month rating period (which typically run on a state fiscal year or a calendar year basis), are set using baseline utilization and cost data from prior periods (which can lag one to two years, to allow claims to complete). Baseline spending data is trended forward to determine per member per month payment amounts and must take into account/adjust for factors such as medical cost inflation, expected changes in utilization, and state Medicaid program changes (e.g., changes to eligibility, benefits, cost-sharing, FFS payment rate changes (if state bases managed care rates on FFS rates)).

States may use a variety of mechanisms to adjust plan risk, incentivize plan performance, and ensure payments are not too high or too low, including risk-sharing arrangements (including risk corridors), risk and acuity adjustments, medical loss ratios (MLRs, which reflect the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement), or incentive and withhold arrangements. (Many states implemented pandemic-related “risk corridors” (where states and health plans agree to share profit or losses), allowing for the recoupment of funds.) Even if the risk mitigation strategies are in place, states may determine rate amendments are necessary if their actual experience differs significantly from the assumptions used for the initial certified rates.