Health Insurance Coverage in 2013: Gains in Public Coverage Continue to Offset Loss of Private Insurance

Continued Economic Recovery

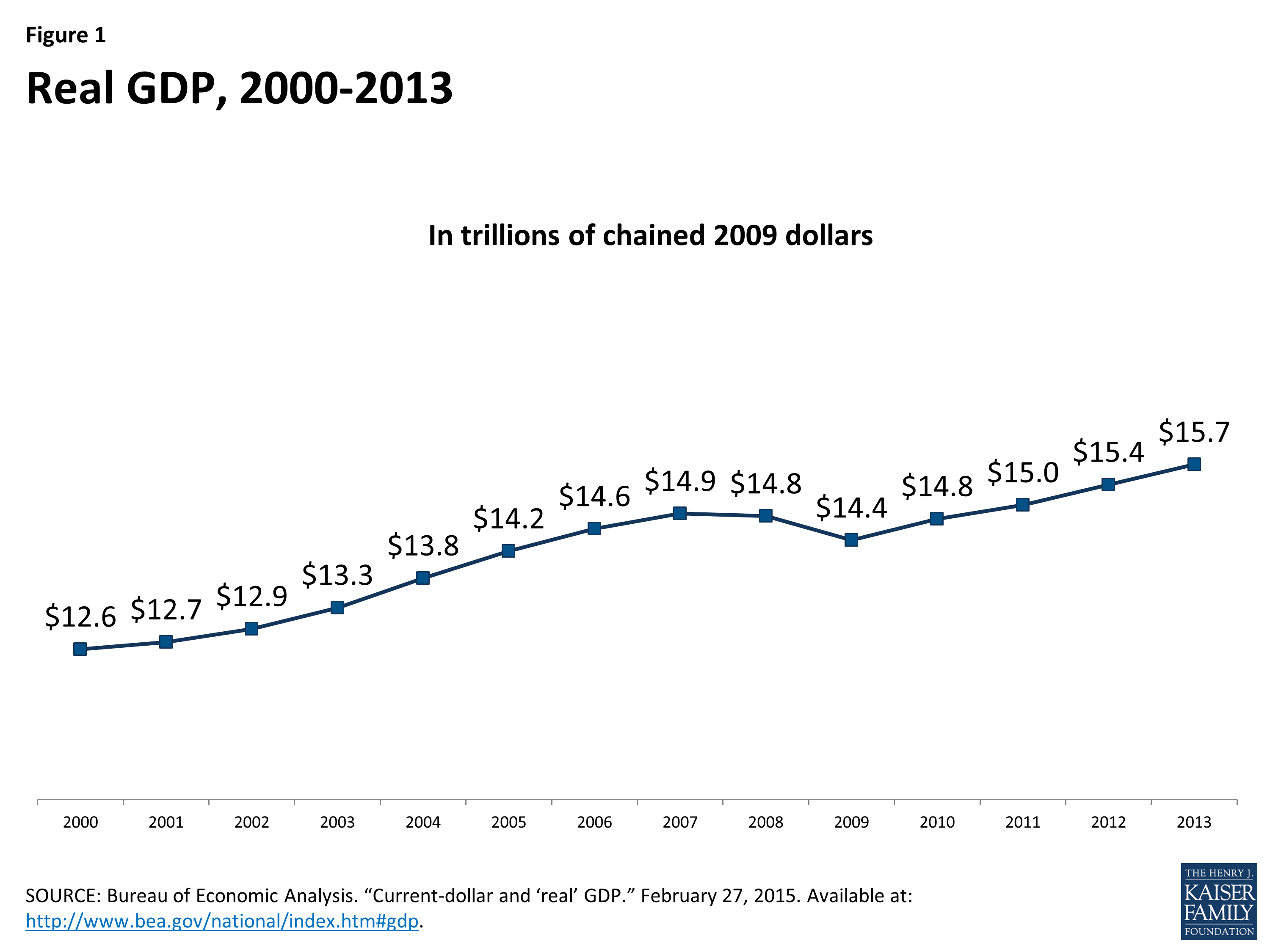

Figure 1: Real GDP, 2000-2013 (in trillions)

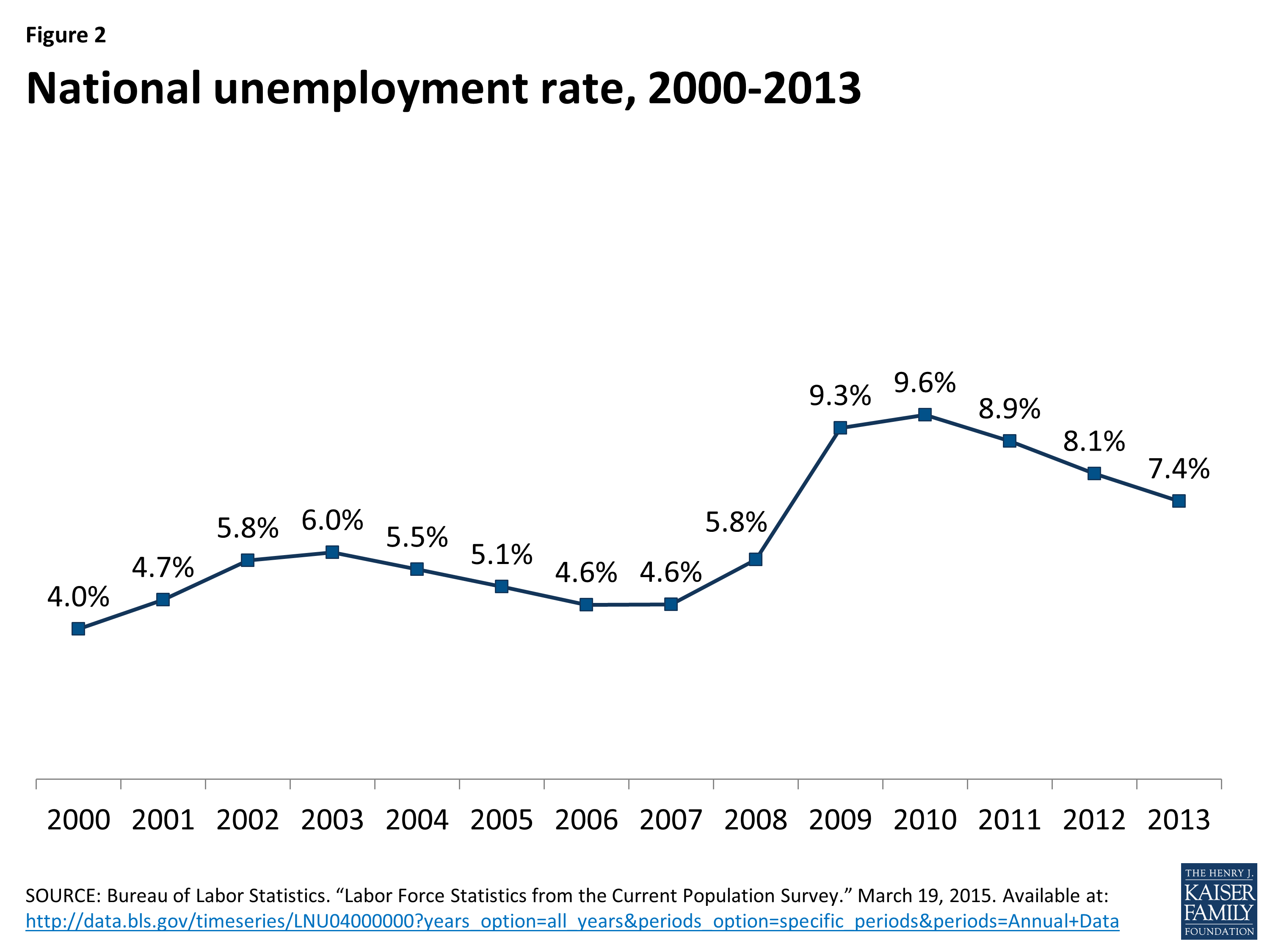

Most economic indicators suggest continued recovery since the peak of the recession in 2009 and 2010. Real GDP fell from $14.9 trillion in 2007 to $14.4 trillion in 2009 but recovered starting in 2010 to hit $15.7 trillion in 2013 (Figure 1). The unemployment rate increased from 4.6 percent in 2007 to peak at 9.6 percent in 2010, falling back to 7.4 percent in 2013 (Figure 2). The most recent data (February 2015) suggest that the unemployment rate has now recovered to 2008 levels (5.6 percent).1

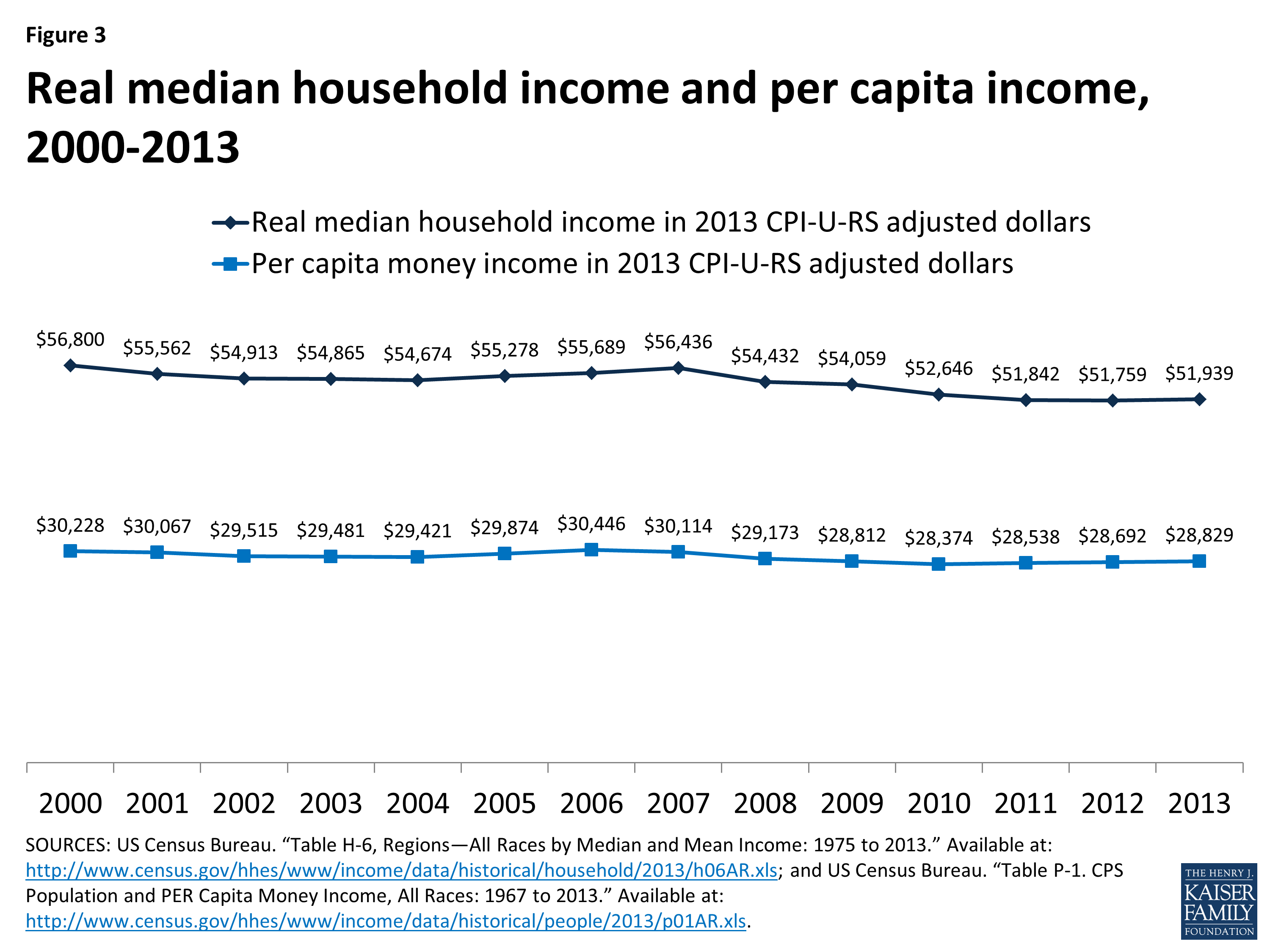

Real median household income and real per capita income also fell between 2008 and 2010 and have shown less recovery than other economic indicators. Median household income continued to fall between 2010 and 2012 and increased only $180 between 2012 and 2013, not a statistically significant change. Similarly, real per capita income remains more than $1,500 below its 2006 peak (Figure 3).

Figure 2: National unemployment rate, 2000-2013

Figure 3: Real median household income and per capita income, 2000-2013

Changes in Health Insurance Coverage from 2012 to 2013

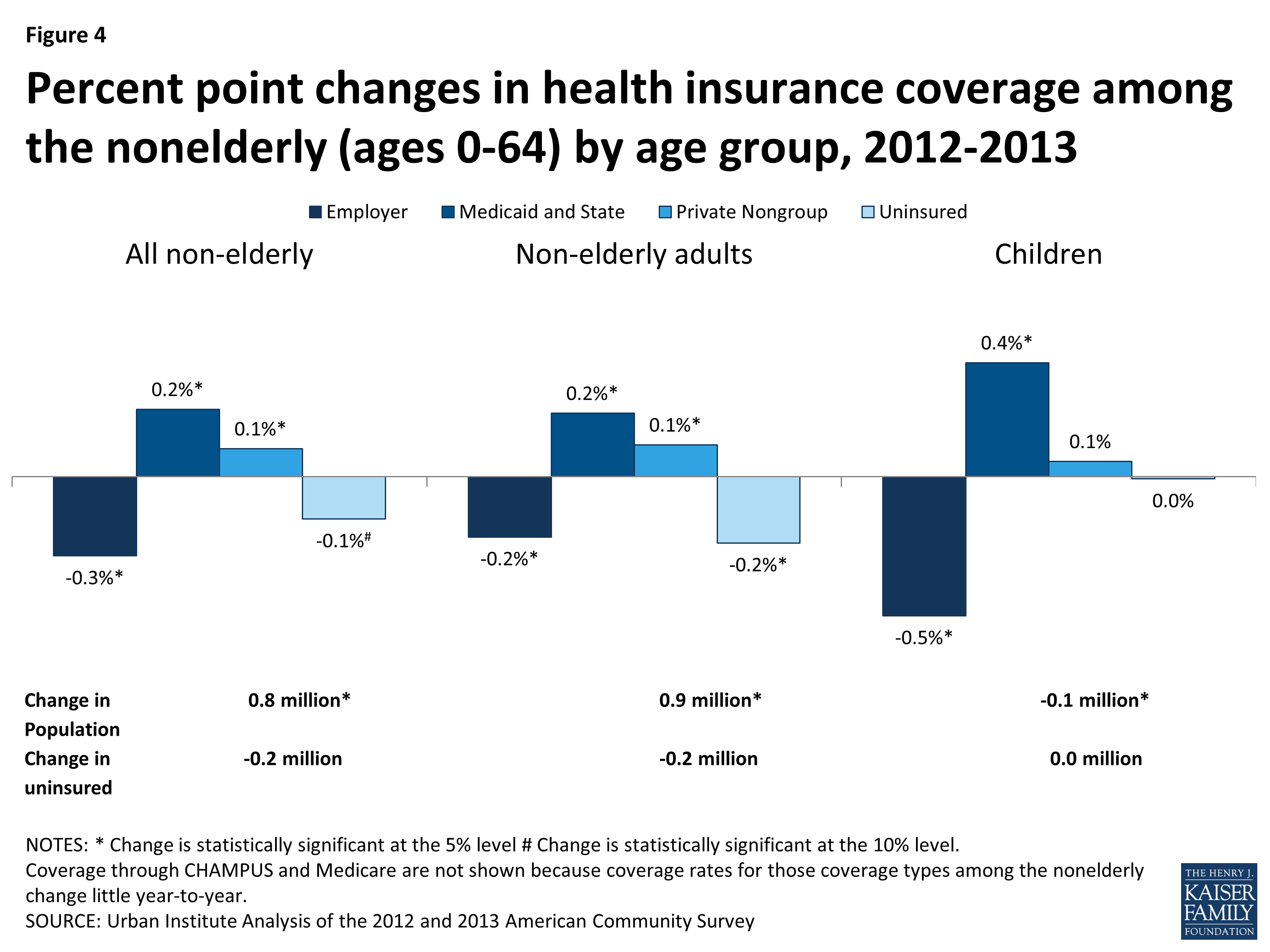

As the economy continued to improve between 2012 and 2013, the uninsured rate fell by 0.1 percentage point and the number of uninsured Americans fell by 200,000 (Figure 4). The decrease in the uninsured rate was entirely among nonelderly adults and was primarily due to increases in public coverage. From 2012 to 2013, the ESI coverage rate declined 0.3 percentage points, leading to 300,000 fewer people with ESI, while Medicaid and Children’s Health Insurance Program (CHIP) coverage increased by 0.2 percentage points, or 700,000 people. The reduction in ESI and increase in Medicaid and CHIP coverage rates were more prominent among children than nonelderly adults. In addition, nearly all of the reduction in the number of uninsured was among non-Hispanic whites below 138 percent of the FPL (data not shown). Finally, private non-group coverage increased by 0.1 percentage points among nonelderly adults, all of which was due to an increase of non-group coverage among young adults (young adult data not shown). The additional 200,000 young adults with non-group coverage may reflect young adults staying on their parents’ non-group plan until age 26 or, potentially, misreporting of October through December 2013 enrollment in the Marketplaces for 2014.2 Because the changes in insurance coverage from 2012 to 2013 were small overall, the remainder of this brief will focus on trends in insurance coverage from 2008 to 2013.

Figure 4: Percent point changes in health insurance coverage among the nonelderly (ages 0-64) by age group, 2012-2013

Changes in Coverage among the Nonelderly Population, 2008-2013

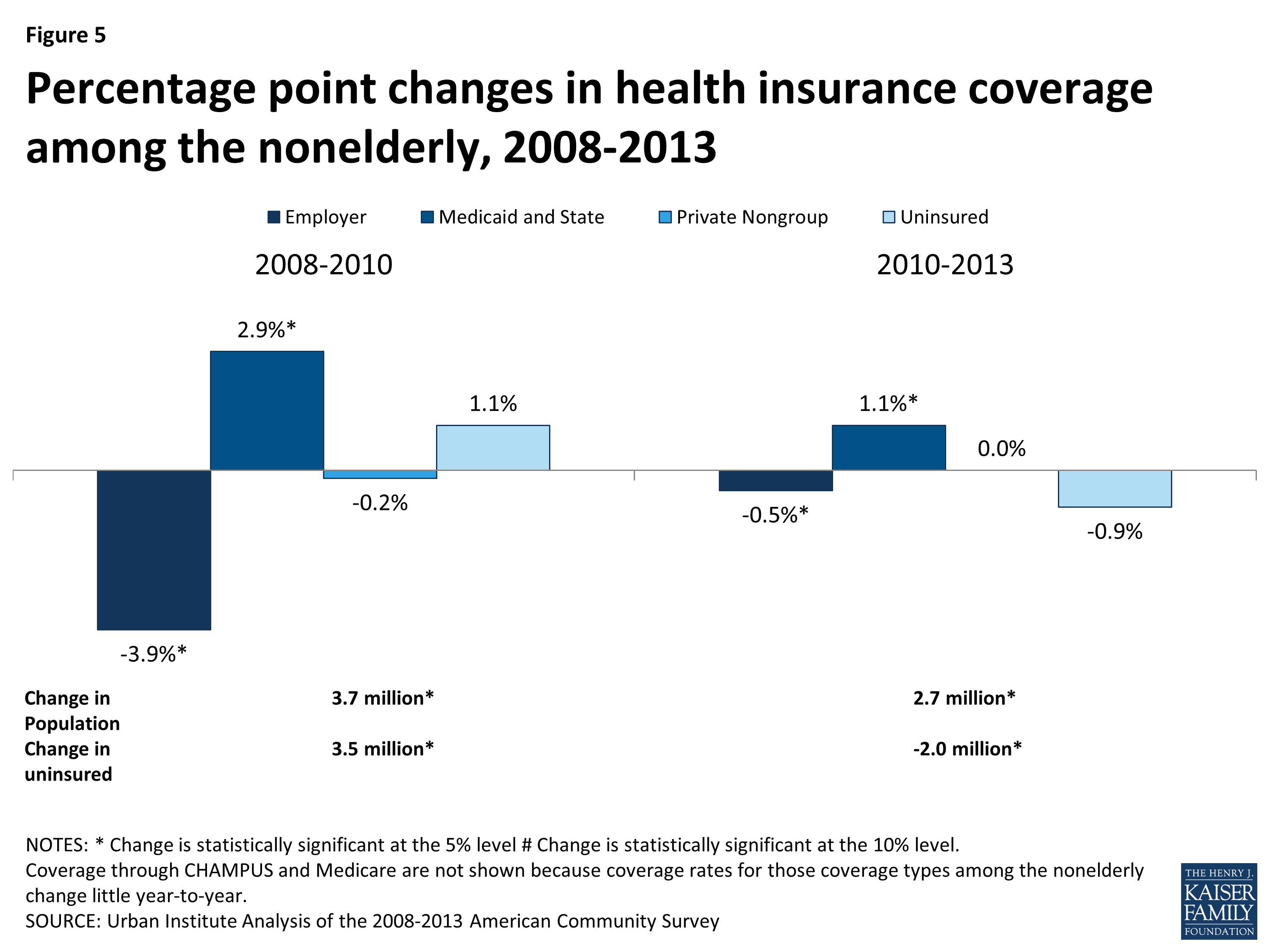

Figure 5 shows the changes in health insurance coverage that occurred during the recession and recovery for the nonelderly population (under age 65). The Great Recession began in December 2007 and ended in June 2009, making 2010 the first full year since 2007 in which GDP did not decline.3 Therefore, 2010 is used as the break point between the recession and recovery throughout this brief. From 2008 to 2010, the ESI coverage rate fell from 61.0 percent to 57.1 percent. At the end of this period, 8.2 million fewer nonelderly adults and children had ESI coverage. In addition, 500,000 fewer people had private non-group coverage at the end of this period. Some of these coverage losses were offset by gains in public coverage. The Medicaid coverage rate increased from 15.3 percent to 18.2 percent during this period, resulting in 8.1 million additional people with Medicaid coverage. In addition, military (CHAMPUS) and Medicare coverage increased by 0.3 percent (data not shown).4 In total, the uninsured rate grew from 16.8 percent to 17.9 percent, meaning 3.5 million more people were uninsured in 2010 than in 2008.

Between 2010 and 2013, as the economy began to improve, the uninsured rate began to fall. In 2013, the uninsured rate had fallen to 16.9 percent, still slightly above the level of 2008. Most of the gains in insurance coverage during the economic recovery came from public coverage sources. Between 2010 and 2013, there was a 1.1 percentage point increase in Medicaid and CHIP coverage,5 resulting in 3.5 million additional people covered by the Medicaid program. While this increase in Medicaid coverage may reflect, in part, the early Medicaid expansions undertaken in 2010 and 2011 by four states (California, Connecticut, the District of Columbia, and Minnesota), those early expansions alone did not affect a large enough population to account for the entire increase in Medicaid coverage.6 From 2010 to 2013, ESI coverage declined another 0.5 percentage points, from 57.1 percent to 56.6 percent.

Figure 5: Percentage point changes in health insurance coverage among the nonelderly, 2008-2013

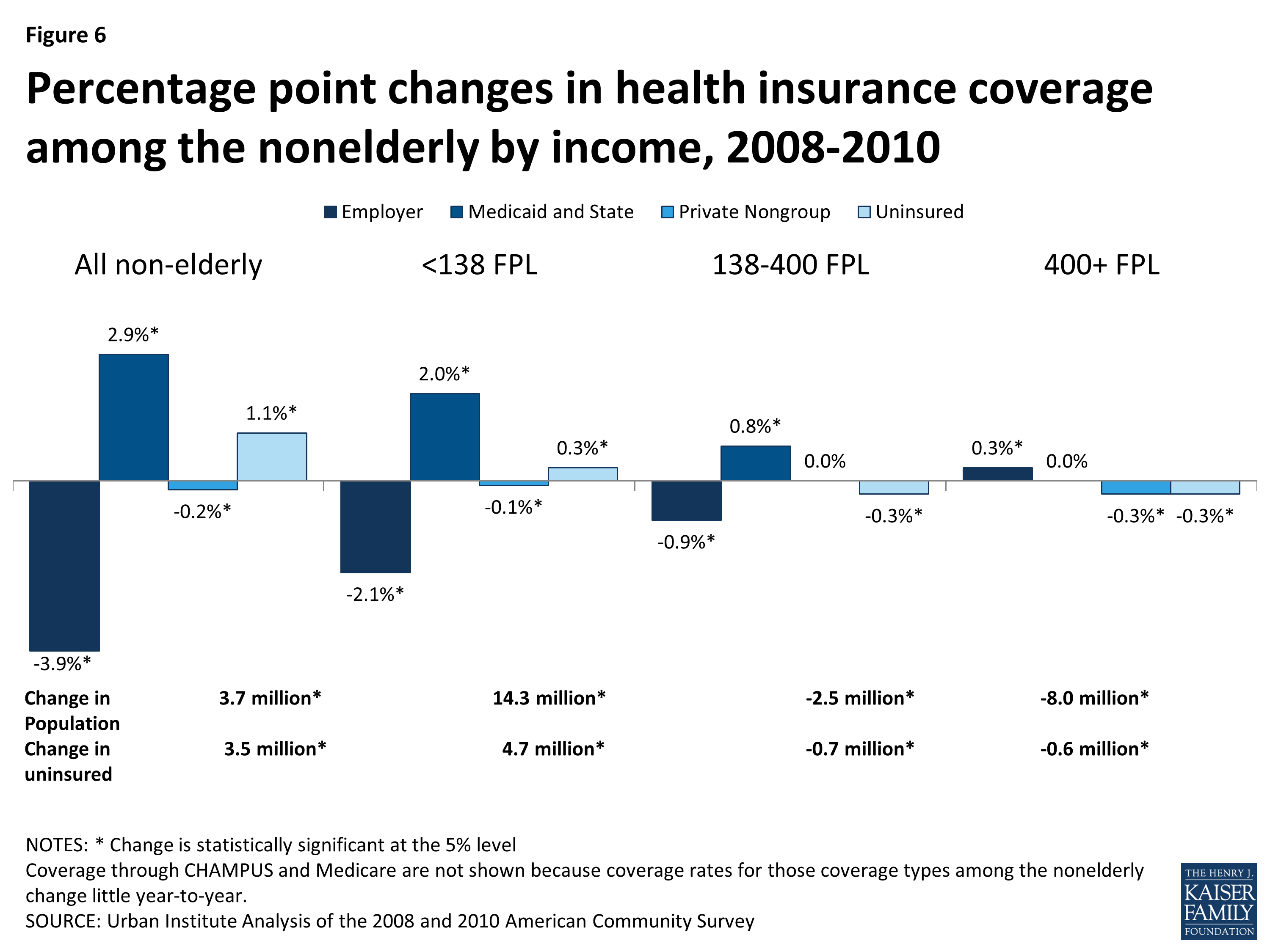

Changes in Coverage by Income

Figure 6: Percentage point changes in health insurance coverage among the nonelderly by income, 2008-2010

Between 2008 and 2010, the entirety of the net increase in the number of uninsured was due to loss in coverage among those with family incomes below 138 percent of the FPL (Figure 6). Increases in Medicaid coverage made up for much of the loss of ESI in this income group, and the uninsured rate among this group increased by only 0.3 percentage points. However, the size of the population with income below 138 percent of the FPL swelled by 14.3 million, leading to 4.7 million more low-income Americans uninsured. In contrast, both the income group between 138 to 400 percent FPL and the income group above 400 percent FPL shrank between 2008 and 2010, and there were 1.3 million fewer uninsured Americans in these income groups in 2010 than in 2008.

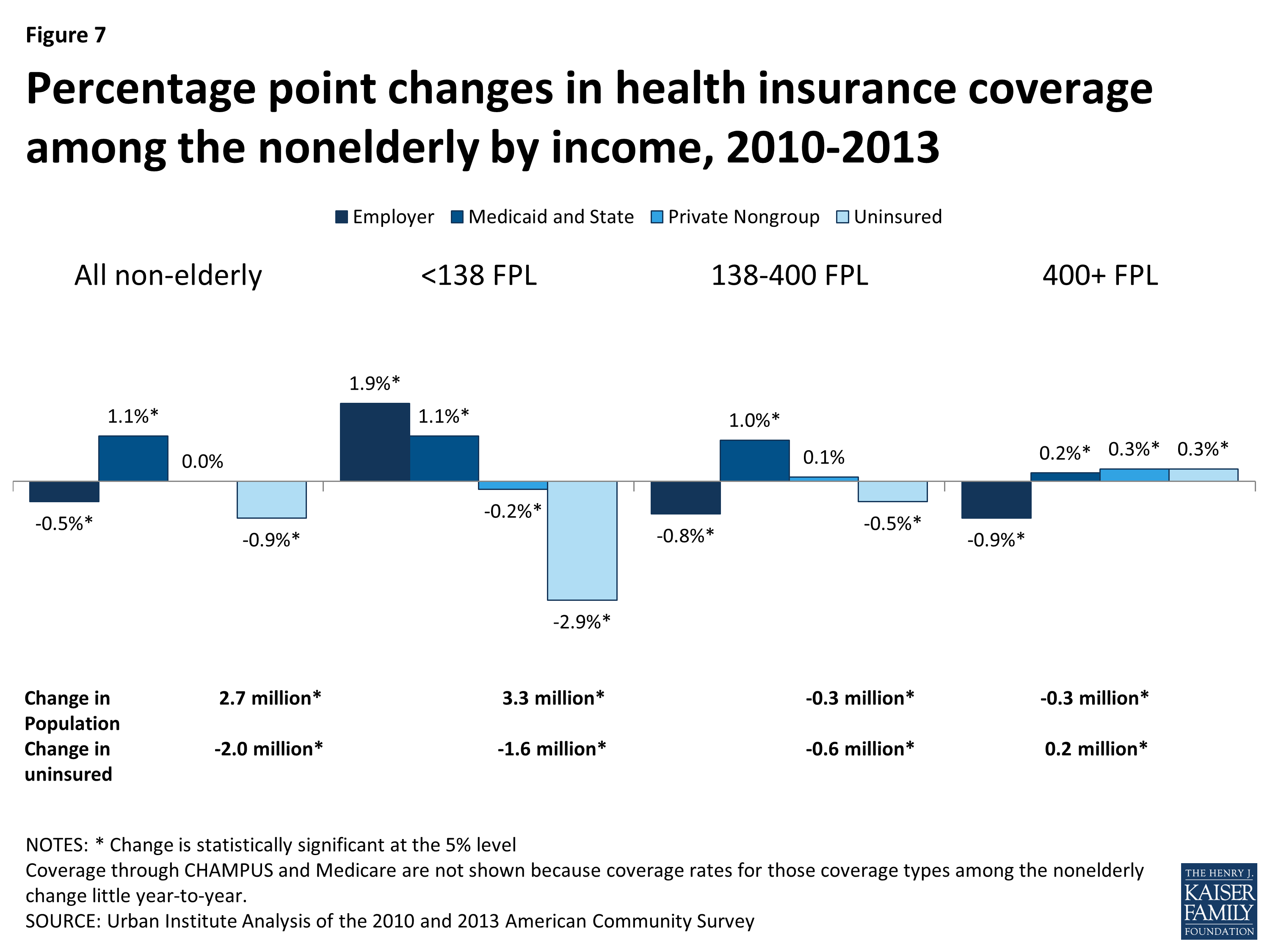

As shown in Figure 7, the uninsured rate for those with family incomes below 138 percent of the FPL declined as the economy improved between 2010 and 2013, leading to 1.6 million fewer uninsured Americans in this income group. Only those with incomes below 138 percent of the FPL showed a net gain in ESI coverage between 2010 and 2013, though the ESI coverage rate for that group remained low at 20.8 percent (compared to 18.9 percent in 2010).

Figure 7: Percentage point changes in health insurance coverage among the nonelderly by income, 2010-2013

ESI coverage declined from 64.6 percent to 63.8 percent for those with incomes between 138 and 400 percent of the FPL, and from 88.1 percent to 87.2 percent for those with incomes above 400 percent of the FPL between 2010 and 2013. The loss of ESI was offset by gains in Medicaid among the middle income group, and the uninsured rate fell 0.5 percentage points for that group. The highest income group showed a 0.3 percent increase in the uninsured rate, meaning an additional 200,000 people with incomes above 400 percent of the FPL were uninsured. Overall, there were 2 million fewer uninsured Americans in 2013 than in 2010 due to increases in Medicaid coverage among those with incomes below 400 percent of the FPL and increases in ESI among those with incomes below 138 percent of the FPL, who had the largest ESI losses during the Great Recession.

Changes in Coverage by Age

The health insurance coverage patterns for children, young adults, and adults differ from 2008 to 2013. The uninsured rate for nonelderly adults was more than double that for children throughout this period, in part because Medicaid and CHIP have higher income eligibility limits for children. In addition, the ACA provision allowing young adults to stay on their parents’ plan until the age of 26 led to significant gains in ESI coverage among this population beginning in 2010 that were not shared by older adults.7 Given these different policy contexts, we examined coverage changes from 2008 to 2013 separately for each of these age groups.

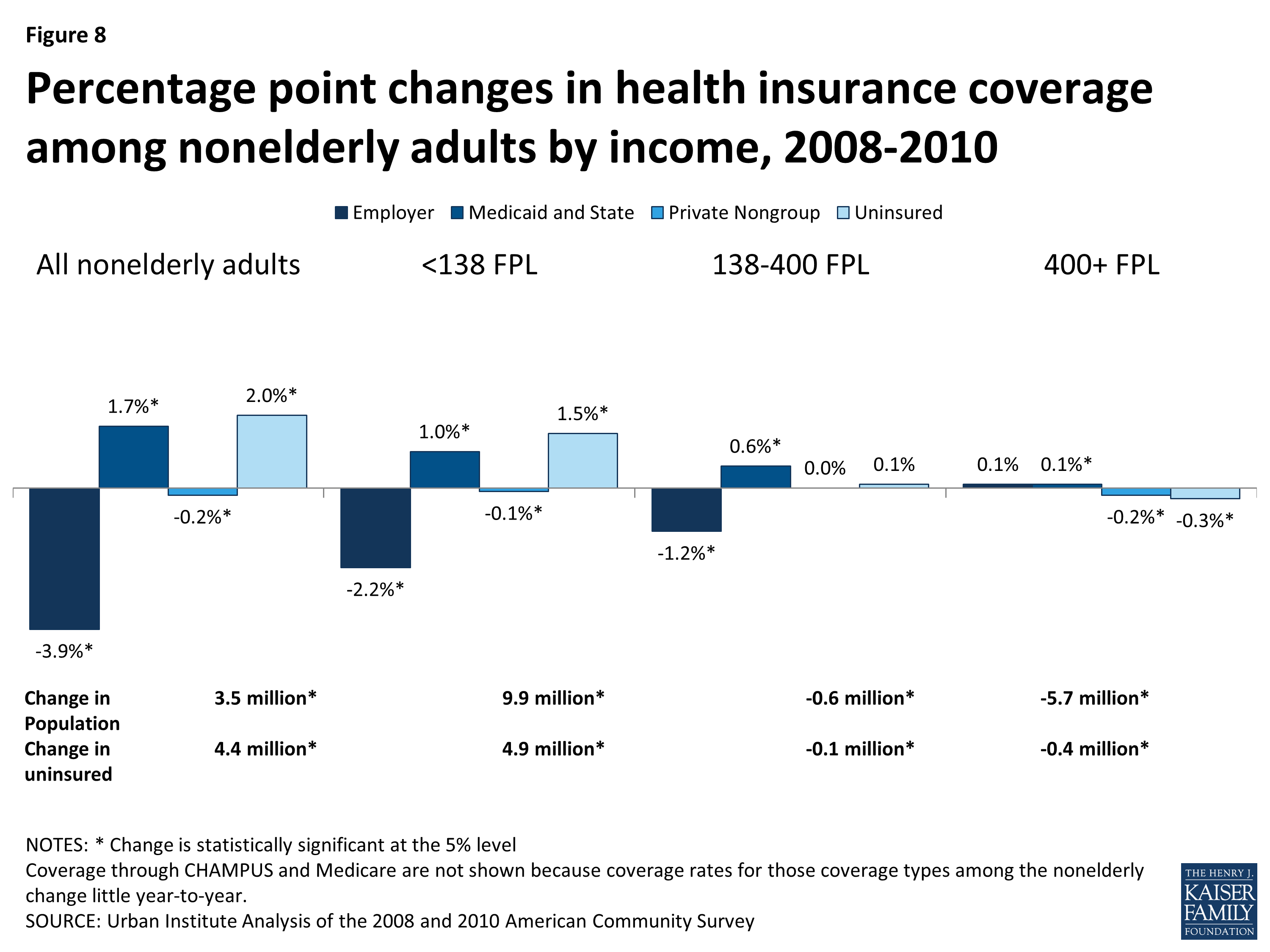

All Nonelderly Adults

Figure 8: Percentage point changes in health coverage among the nonelderly by income, 2008-2010

From 2008 to 2010, there was a 3.9 percentage point decrease in the ESI coverage rate for nonelderly adults and a 1.7 percentage point increase in Medicaid and other state coverage (Figure 8). In total, the uninsured rate for nonelderly adults increased by 2.0 percentage points, and 4.4 million more nonelderly adults were uninsured. All of the increase in the number of uninsured was among adults in families with income at or below 138 percent of the FPL (4.9 million). The number of nonelderly adults in families with incomes above 400 percent of the FPL shrank significantly, by 5.7 million, and this group saw a small decrease in the uninsured rate of 0.3 percentage points between 2008 and 2010.

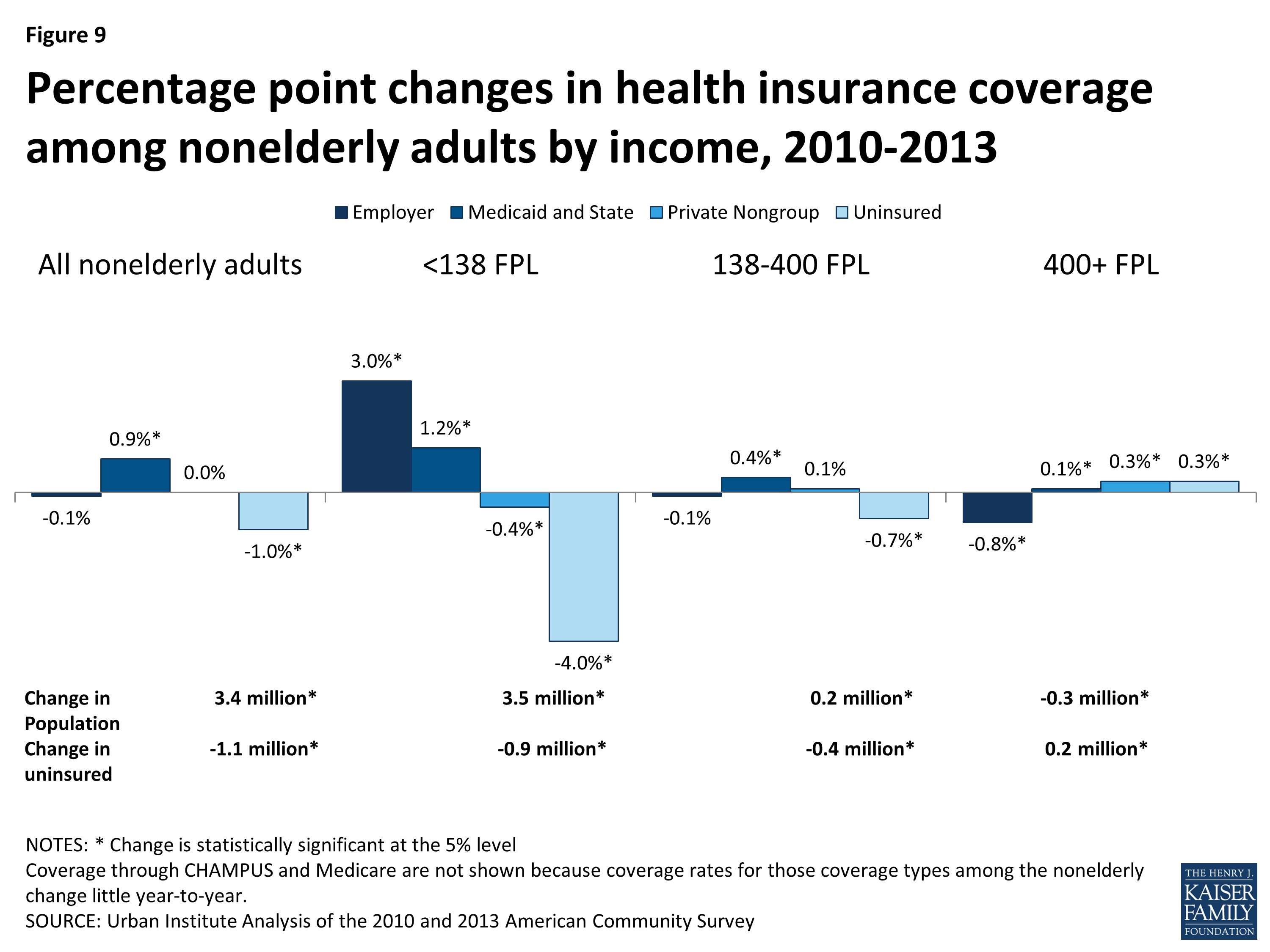

Figure 9: Percentage point changes in health insurance coverage among the nonelderly by income, 2010-2013

Between 2010 and 2013, the overall ESI coverage rate for nonelderly adults was nearly stable, and the uninsured rate declined by 1 percentage point in part due to increases in public coverage. However, there was significant variation by income group. Nonelderly adults below 138 percent of the FPL saw a 3.0 percentage point gain in ESI coverage and a 1.2 percentage point gain in Medicaid and CHIP coverage, leading to a 4.0 percentage point reduction in the uninsured rate for that income group. In contrast, ESI coverage for those with incomes above 400 percent of the FPL continued to decline, leading to a 0.3 percentage point increase in the uninsured rate for that group.

Young Adults

Figure 10: Percentage point changes in health insurance coverage among nonelderly adults by age, 2008-2010

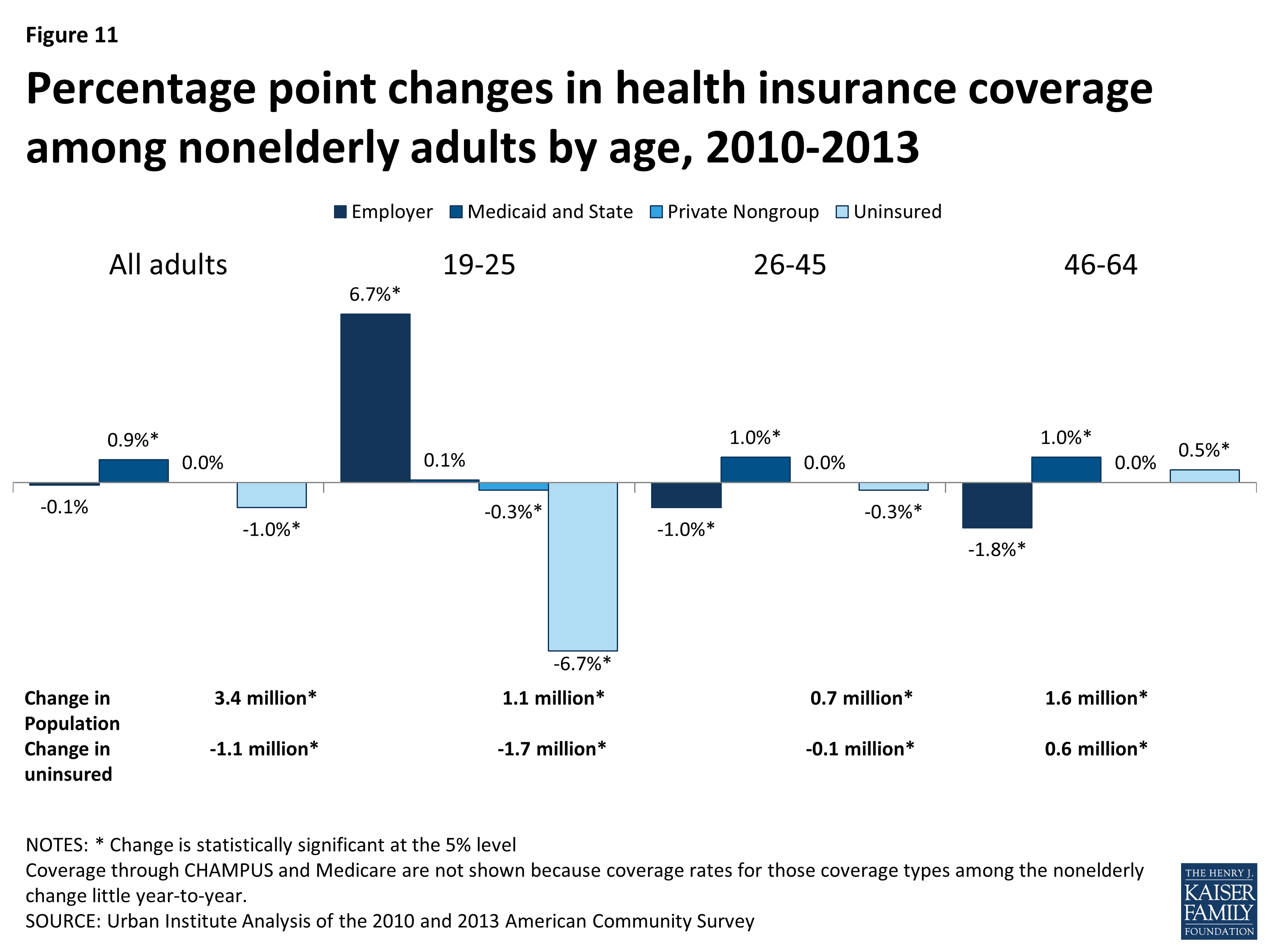

Beginning in September 2010, the ACA required most health plans to allow children to stay on their parents’ plan as a dependent until age 26. Between 2008 and 2010, this age group lost ESI coverage at a rate similar to the rest of the adult population (Figure 10). However, the trend for young adults diverged significantly from other nonelderly adults from 2010 to 2013 (Figure 11). While other age groups continued to lose ESI coverage, albeit more slowly than between 2008 and 2010, young adults had large gains in ESI coverage. Between 2010 and 2013, 2.6 million young adults gained ESI coverage, a 6.7 percentage point increase in the ESI coverage rate (Figure 11). Young adults did not gain Medicaid and CHIP coverage as quickly as other age groups in this time period.

Figure 11: Percentage point changes in health insurance coverage among nonelderly adults by age, 2010-2013

These gains for young adults created a near-stabilization of ESI coverage rates between 2010 and 2013 for all nonelderly adults. For other adult groups, however, ESI coverage losses continued, resulting in 700,000 adults ages 26 to 64 losing ESI coverage between 2010 and 2013. Similarly, nearly all of the decrease in the uninsured rate and number uninsured seen among nonelderly adults between 2010 and 2013 was among young adults. While the ACA policy had the intended effect of decreasing the uninsured rate among young adults, it masked a continued trend of loss in ESI coverage among other age groups.

Children

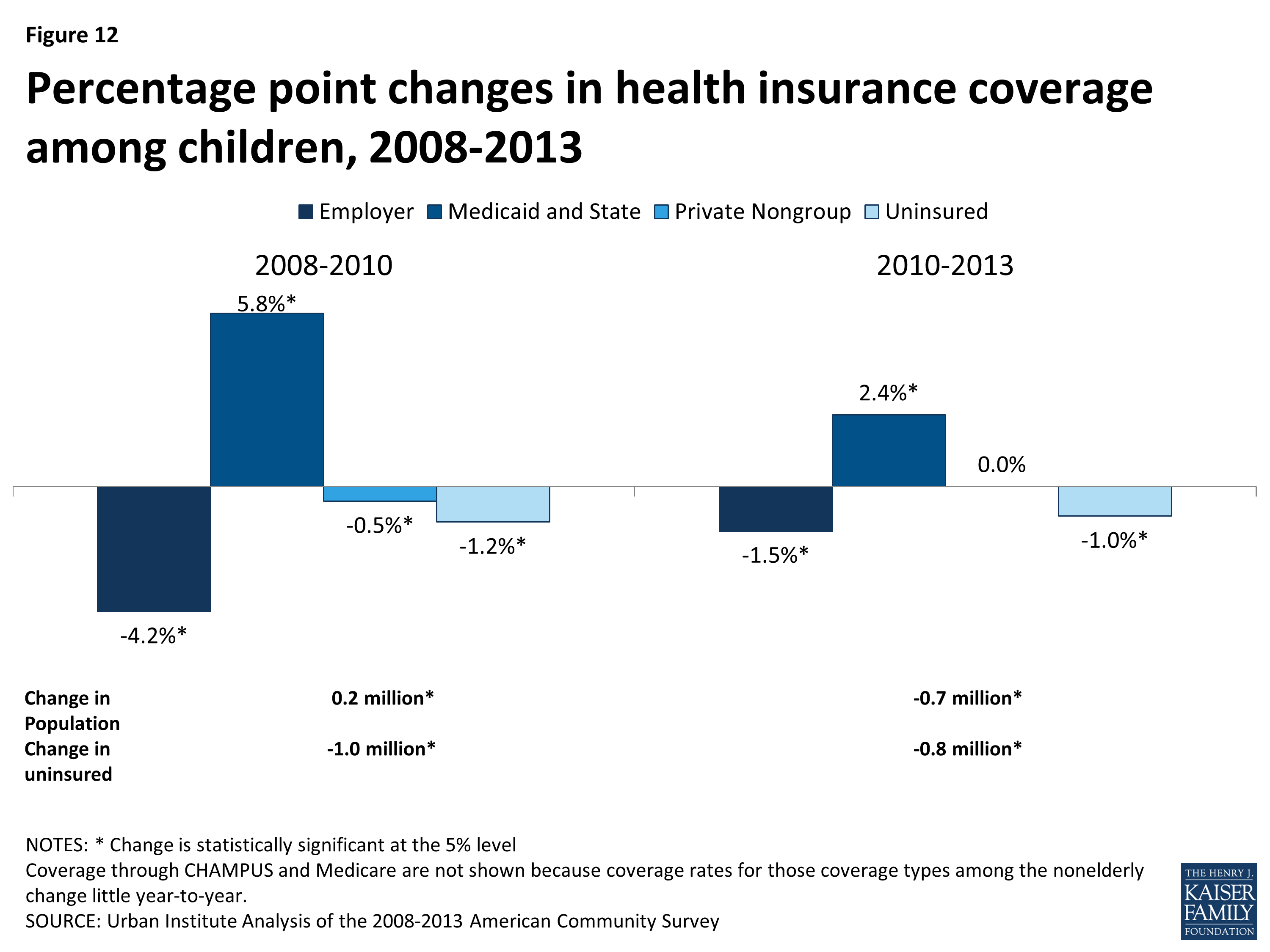

The pattern of coverage for children under age 19 is different from that of adults, primarily due to greater access to Medicaid and CHIP coverage. During the recession, children were more likely to lose access to ESI than adults. Between 2008 and 2010, the ESI coverage rate for children fell 4.2 percentage points, from 54.7 percent to 50.5 percent (Figure 12). Most of this loss of ESI was among low-income children and was more than made up for by increases in Medicaid and CHIP coverage. The Medicaid and CHIP coverage rate for children increased from 31.7 percent to 37.5 percent in this time period, meaning 4.6 million additional children were covered in those programs, 4.5 million of whom had family incomes below 138 percent of the FPL. Overall, the uninsured rate for children actually declined during the recession, from 9.2 percent to 8.0 percent, and 1 million fewer children were uninsured in 2010 than in 2008.

Figure 12: Percentage point changes in health insurance coverage among children, 2008-2013

The economic recovery from 2010 to 2013 showed a similar pattern for children (Figure 12). The ESI coverage rate among children continued to fall, from 50.5 percent in 2010 to 49.1 percent in 2013. This continued reduction in ESI coverage was spread across all income groups. However, this loss of ESI coverage was more than made up for by continued gains in Medicaid and CHIP coverage, which increased from 37.5 percent in 2010 to 39.8 percent in 2013. Overall, 800,000 fewer children were uninsured in 2013 than in 2010, 700,000 of whom had with family incomes below 138 percent of the FPL. The uninsured rate for children with family incomes above 400 percent of the FPL increased 0.3 percentage points between 2010 and 2013, largely due to losses of ESI coverage in that income group (data not shown).

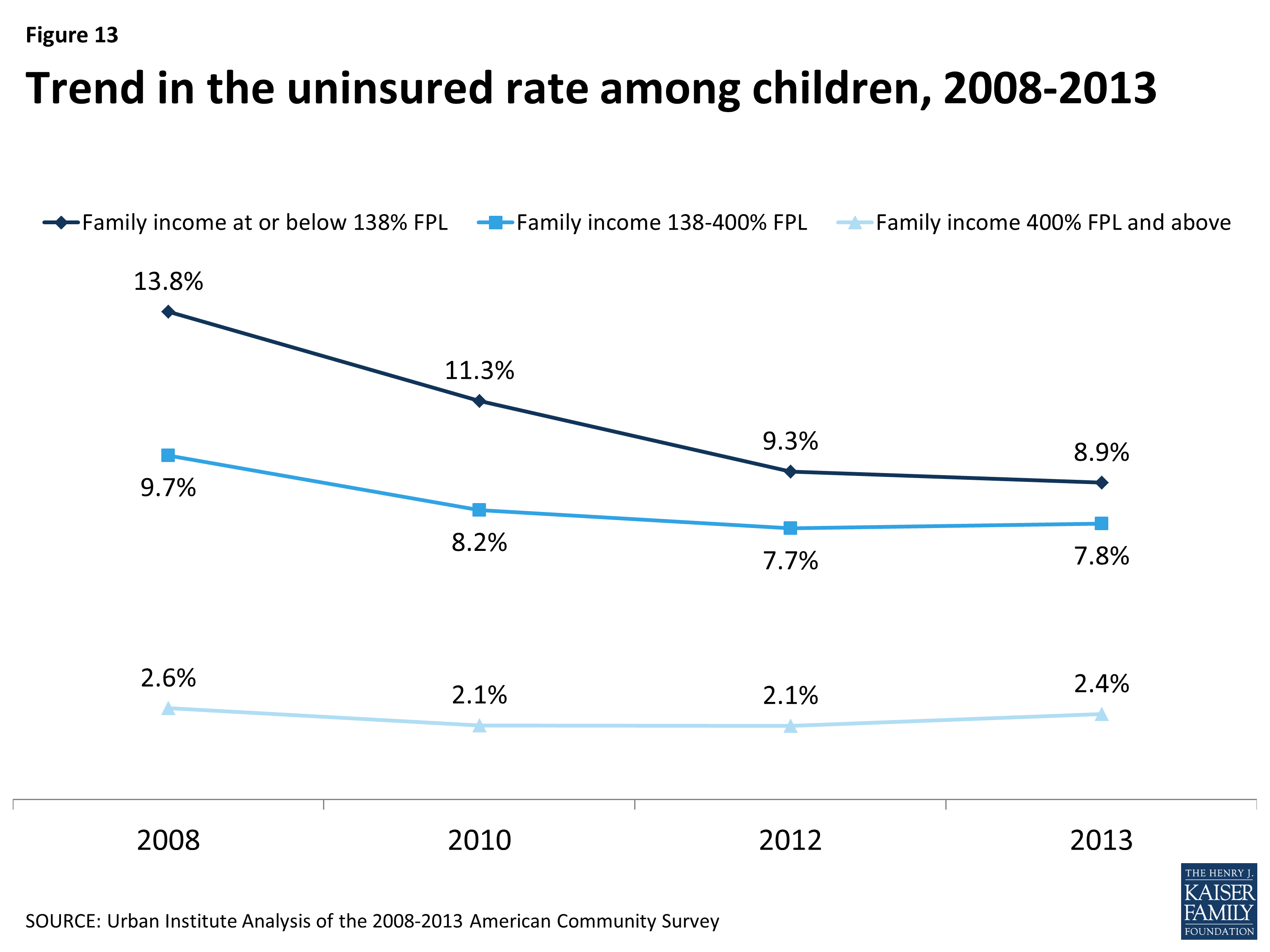

The increases in Medicaid and CHIP coverage rates for children seen during the Great Recession and recovery have reduced the disparity in the uninsured rate among children by income (Figure 13). In 2008, children in families with income of less than 138 percent of the FPL had an uninsured rate of 13.8 percent, versus 2.6 percent for those in families with incomes above 400 percent of the FPL. By 2013, the uninsured rate for low-income children was down to 8.9 percent, compared to 2.4 percent for higher-income children.

Figure 13: Trend in the uninsured rate among children, 2008-2013

Changes in Coverage by Other Demographic Characteristics

There are two important demographic trends in the United States that affect health insurance coverage among the nonelderly. First, racial and ethnic minority populations have grown. Between 2008 and 2013, the non-Hispanic White population shrank by 5.4 million people, while the Hispanic population grew by 6.4 million people. The non-Hispanic Black population also grew by 1.5 million people during this time period, and other racial and ethnic groups also grew by 3.8 million people.8 Hispanics and non-Hispanic Blacks have lower rates of ESI and higher uninsured rates than non-Hispanic Whites, so increases in the size of these populations tend to increase the uninsured rate and the number of uninsured. Second, the US population has shifted geographically. The Northeast and Midwest saw almost no population growth between 2008 and 2013, while the South and West grew by 4.3 million people and 1.9 million people, respectively. On average, the South and West have lower ESI coverage rates and higher uninsured rates than the Northeast and Midwest. In addition, states that have not expanded Medicaid under the ACA are concentrated in these regions, which will exacerbate the regional disparities in uninsured rates in 2014.

Race and Ethnicity

Between 2008 and 2010, non-Hispanic Blacks and Hispanics had more substantial reductions in ESI coverage than non-Hispanic Whites (Figure 14). While some of this disparity was made up by increases in public coverage, overall 2.3 of the 3.5 million people who lost coverage between 2008 and 2010 were people of color. The increases in the uninsured rate were concentrated among low-income people of all racial and ethnic groups. Non-Hispanic Whites over 400 percent of the FPL fared best during the recession, experiencing an increase in the ESI coverage rate and 400,000 fewer uninsured (data not shown).

Figure 14: Percentage point changes in health insurance coverage by race and ethnicity, 2008-2010

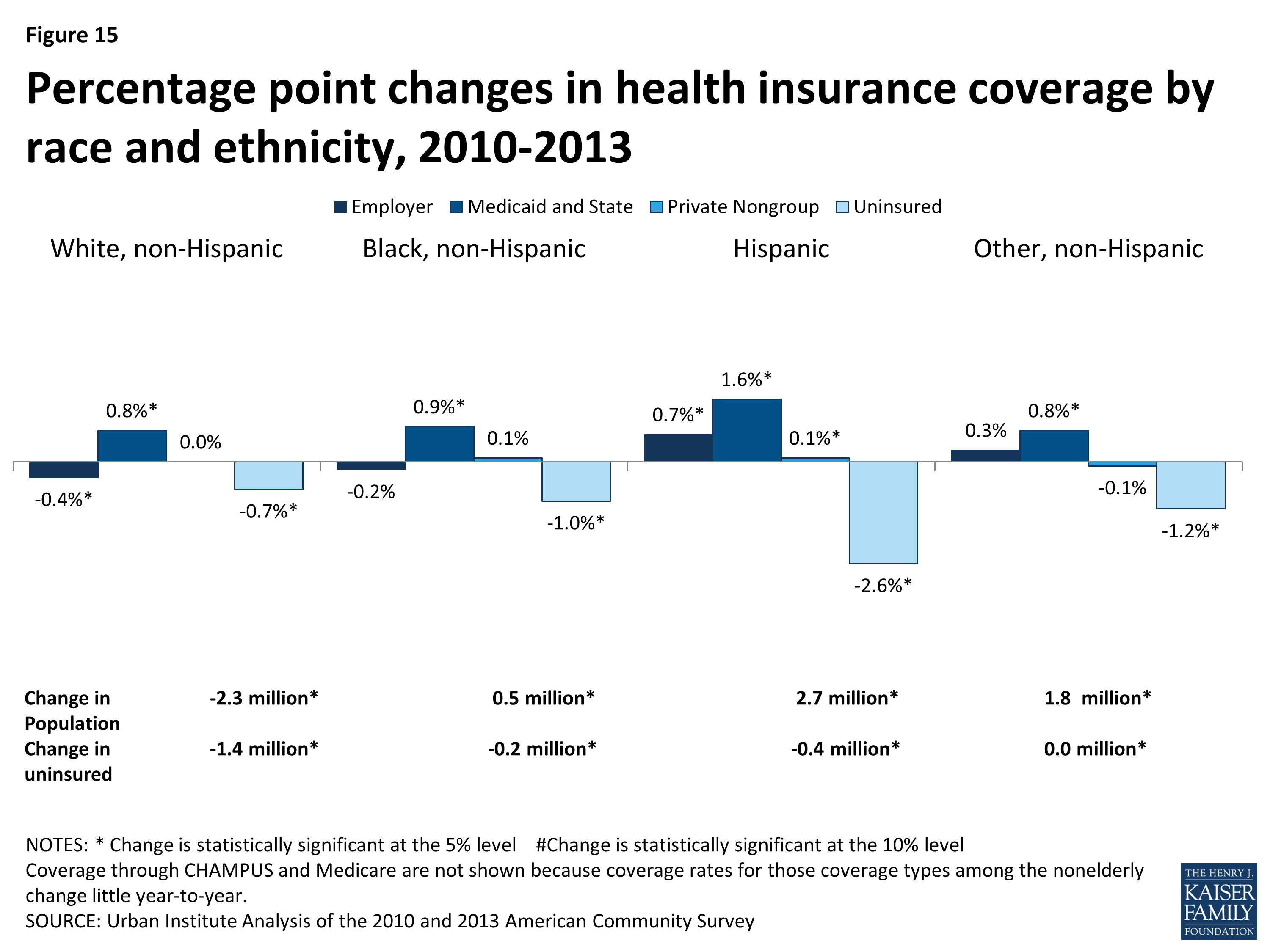

As the economy recovered between 2010 and 2013, the uninsured rate fell for all racial and ethnic groups, largely due to increases in public coverage (Figure 15). Hispanics saw the largest percentage point decrease in the uninsured rate, from 32.2 percent in 2010 to 29.7 percent in 2013. This is due to increases in both public coverage and ESI coverage among the Hispanic population.

Figure 15: Percentage poing changes in health insurance coverage by race and ethnicity, 2010-2013

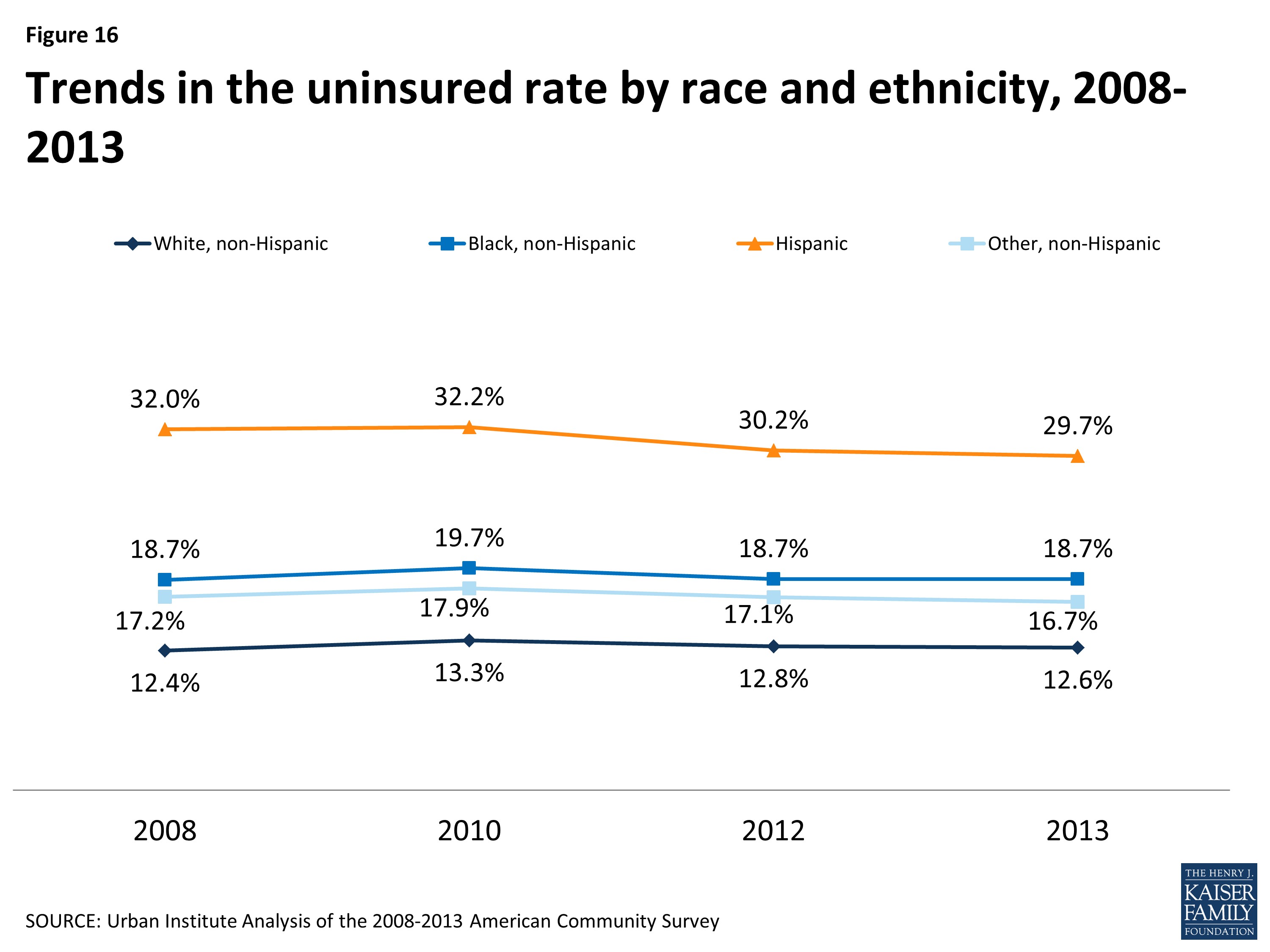

Between 2008 and 2013, the gap in the uninsured rate between non-Hispanic whites and Hispanics narrowed, from 19.6 percentage points in 2008 to 17.1 percentage points in 2013 (Figure 16). Most of this narrowing was due to increases in the Medicaid coverage rate for Hispanics, from 24.2 percent in 2008 to 29.8 percent in 2013, a gain of 4.4 million Hispanic Medicaid enrollees (Figures 14 and 15). Despite these gains, the uninsured rate for Hispanics remained more than double that for non-Hispanic Whites in 2013. The gap in the uninsured rate between non-Hispanic Whites and non-Hispanic Blacks remained virtually unchanged, narrowing by only 0.2 percentage points.

Figure: Trends in the insurance rate by race and ethnicity, 2008-2013

Geographic Region

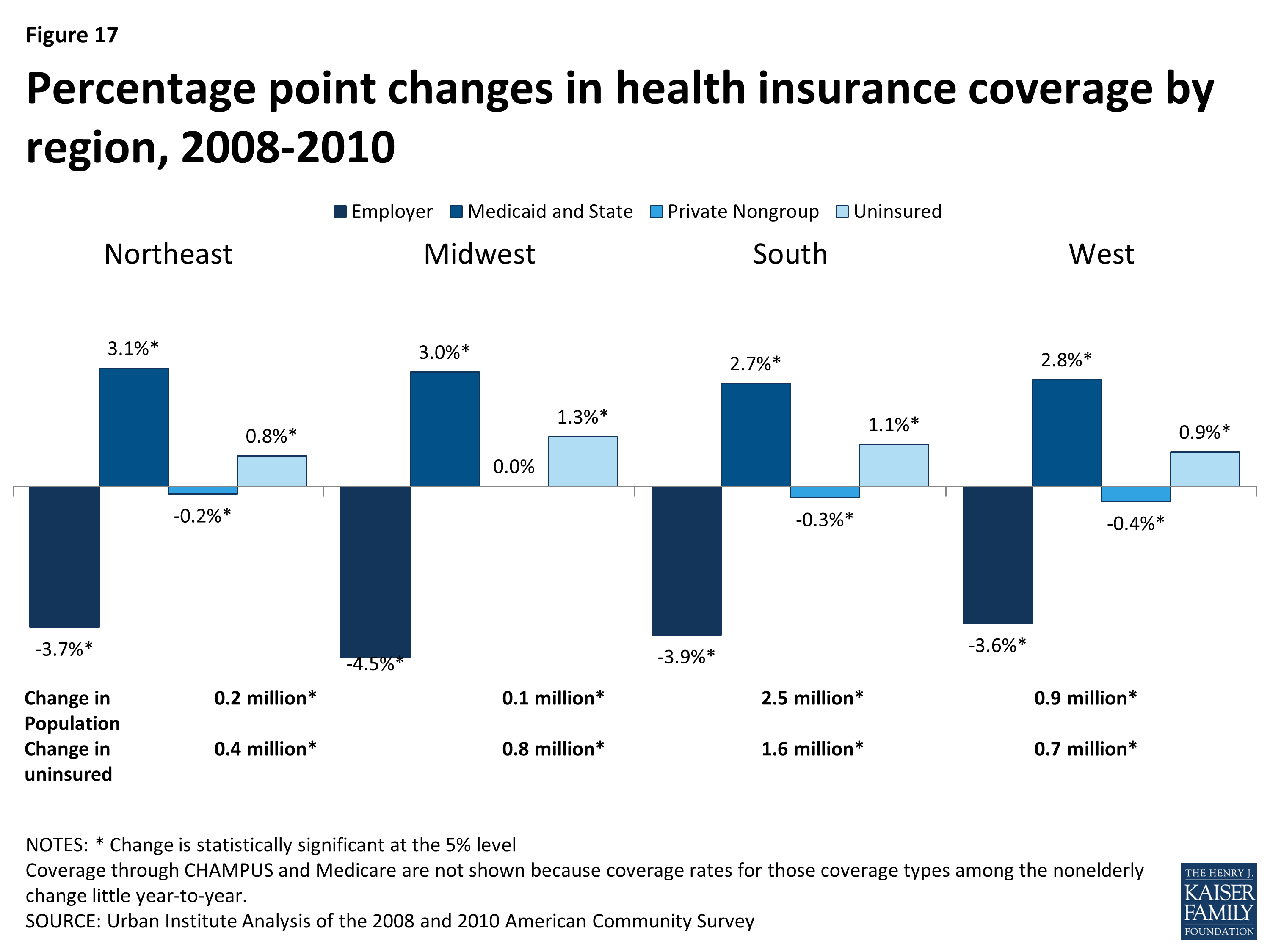

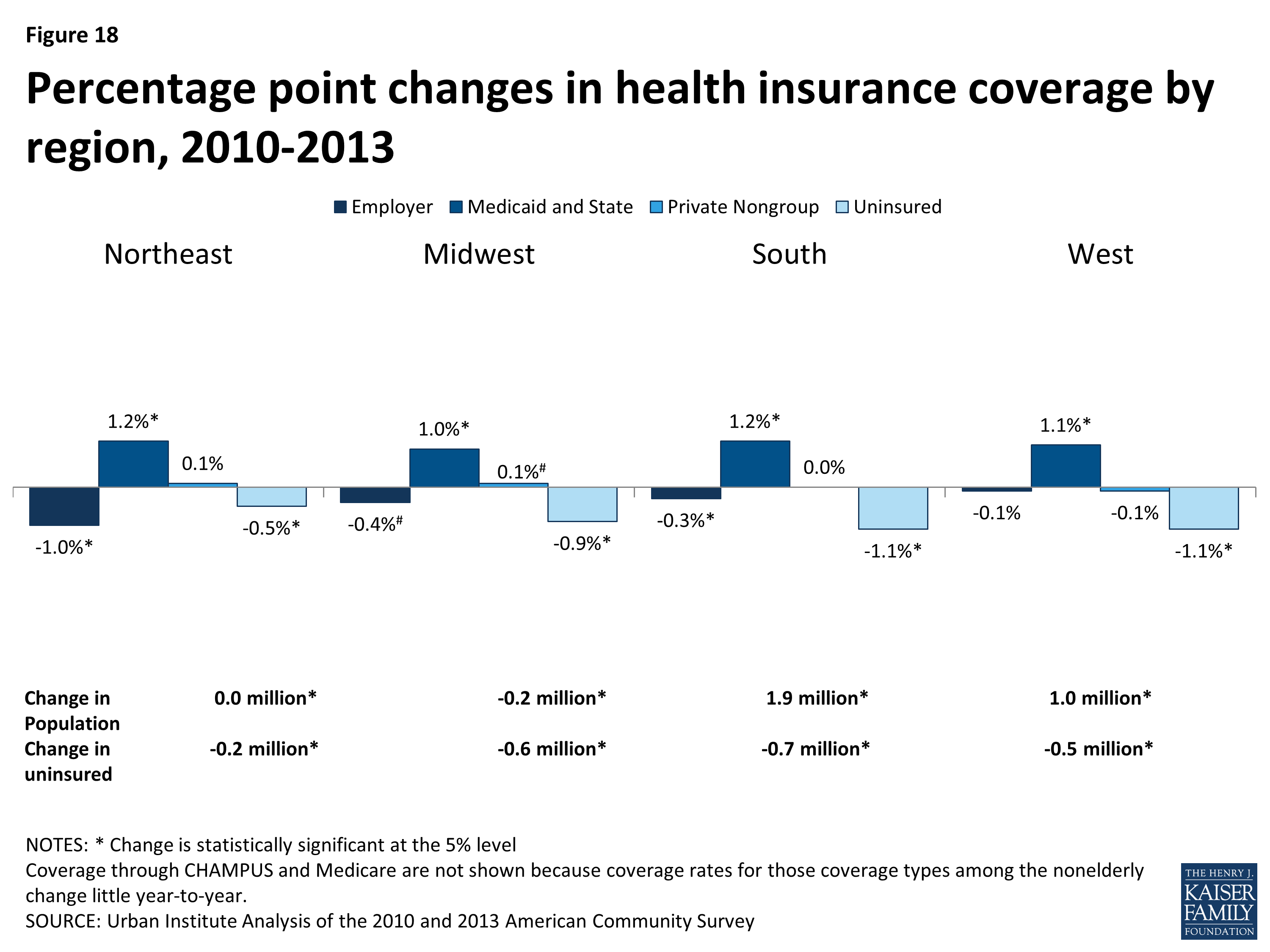

The effects of the recession and recovery on health insurance coverage were not consistent across the country, as shown in Figures 17 and 18. Between 2008 and 2010, the Midwest saw the largest losses of ESI coverage, from 66.3 percent to 61.9 percent, and the largest increase in the uninsured rate, from 12.9 percent to 14.2 percent (Figure 17). The Northeast fared the best in the early years of the recession, with only 400,000 additional uninsured. This was due, in part, to slightly larger percentage point gains in Medicaid coverage in the Northeast, which traditionally has higher income thresholds for adults and children than the South or West.

Figure 17: Percentage point changes in health insurance coverage by region, 2008-2010

During the recovery, the Northeast saw the largest continued reduction in ESI coverage, resulting in approximately 500,000 fewer Northeast residents with ESI in 2013 than in 2010 (Figure 18). The South and West saw the largest percentage point decreases in the uninsured rate (1.1 percent), largely due to gains in public coverage. In addition, population shifts between regions continued between 2010 and 2013, with the Midwest experiencing a net population loss, the Northeast experiencing no net change in population, and the South and West each increasing in population by a million or more people.

Figure 18: Percentage point changes in health insurance coverage by region, 2010-2013

The effect of the recovery between 2010 and 2013 on insurance coverage also differed substantially by state (see Appendix A, Table 7 for uninsured rates by state). Overall, the uninsured rate declined in 39 states and increased in 12 states between 2010 and 2013. Oregon had largest percentage point decrease in the uninsured rate (2.3 percentage points), while Alaska had the highest percentage point increase (1.2 percentage points). In all but 4 states, the Medicaid and CHIP coverage rate increased between 2010 and 2013. Montana had the largest percentage point increase in Medicaid coverage (3.7 percentage points), and Alaska had the largest decline (1.8 percentage points). Finally, ESI coverage rates increased in 17 states and declined in 34 states. Wyoming had the largest increase in ESI at 3.2 percentage points, and Connecticut had the largest decline at 3.3 percentage points.

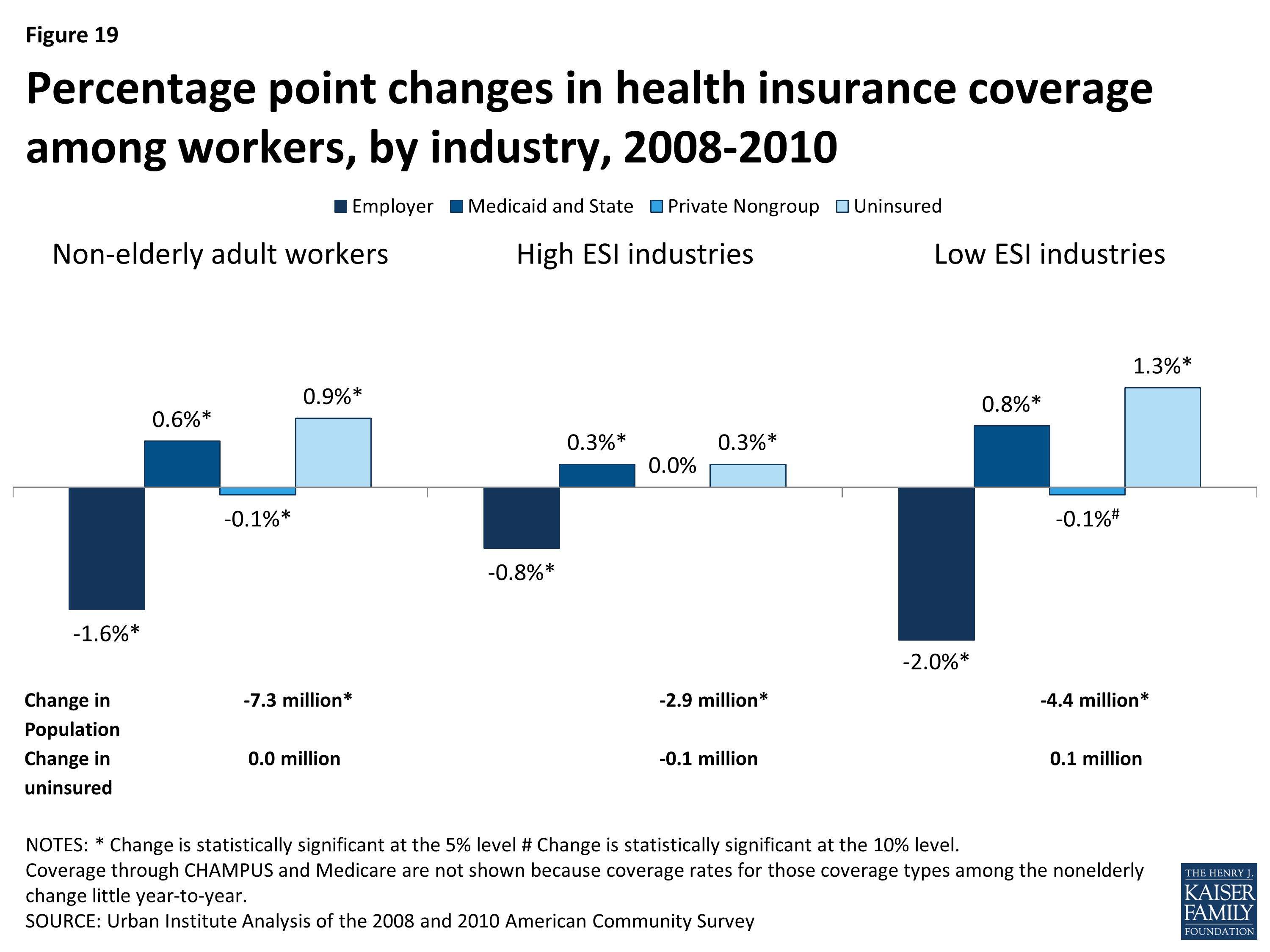

Changes in Coverage among Workers

Figure 19: Percentage point changes in health insurance coverage among workers, by industry, 2008-2010

Between 2008 and 2010, the total number of workers aged 18 to 64 declined from 140.4 million to 133.1 million. Overall, between 2008 and 2010, workers experienced a decline in ESI coverage from 72.4 percent to 70.8 percent, which translates to a loss of ESI coverage for 7.5 million workers (Figure 19). This ESI loss was partially mitigated by increases in Medicaid coverage for low-income workers, but overall the uninsured rate for workers rose 0.9 percentage points. More workers in “low ESI” industries lost ESI than those in “high ESI” industries (4.6 million and 2.8 million, respectively).9 From 2008 to 2010, the low ESI industries saw a larger decline in the number of workers than high ESI industries (4.4 million and 2.9 million, respectively). Because of the decline in the number of workers, the total number of uninsured workers was flat between 2008 and 2010 despite an increase in the uninsured rate.

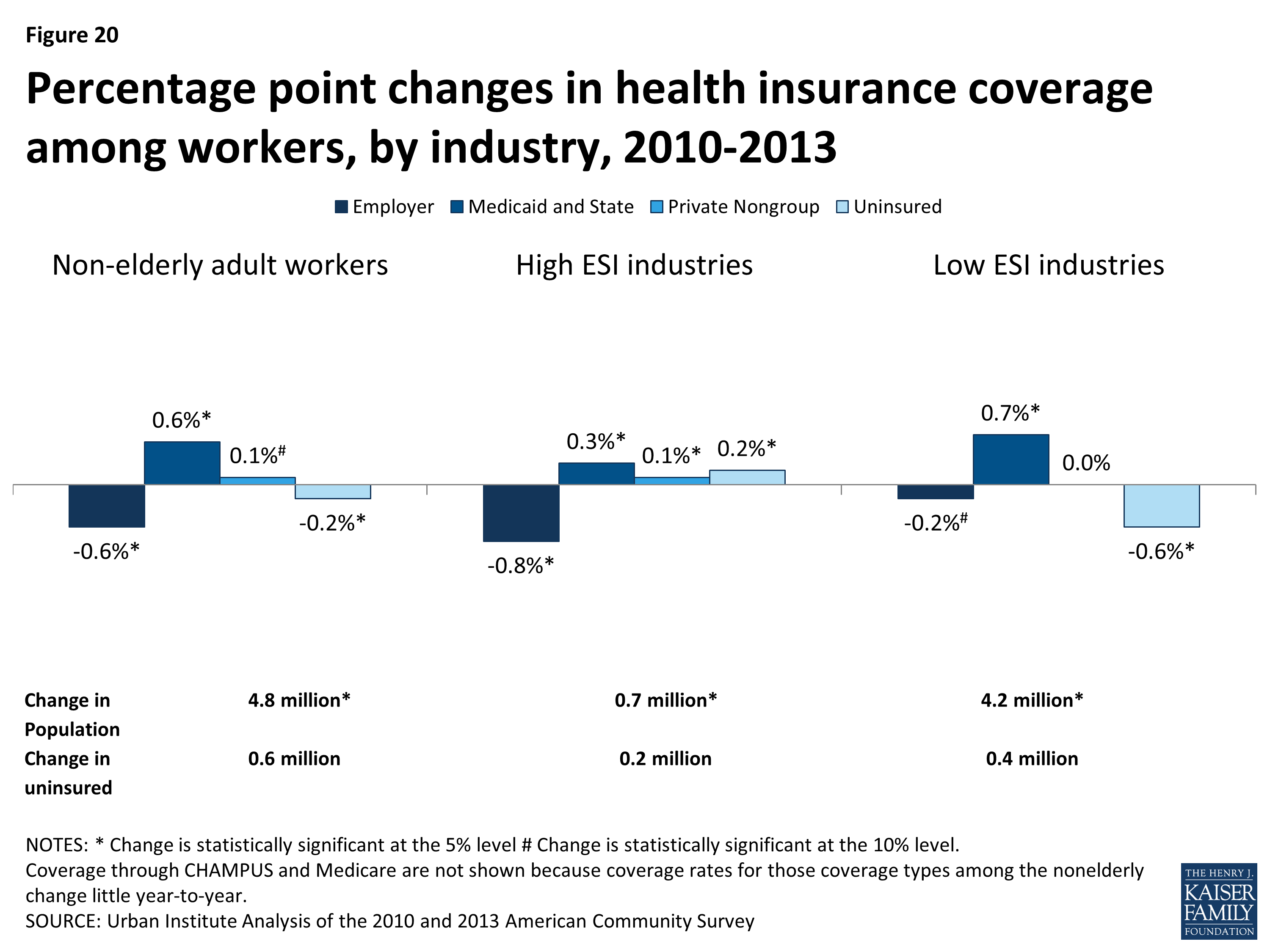

Figure 20: Percentage point changes in health insurance coverage among workers, by industry, 2010-2013

Between 2010 and 2013, the number of workers recovered from 133.1 million to 138.0 million. This increase was concentrated in low ESI industries, which grew by 4.2 million workers between 2010 and 2013. The rate of ESI coverage among all workers also continued to decline between 2010 and 2013, dropping from 70.8 percent to 70.2 percent in that time period (Figure 20). The decline in the ESI coverage rate was more substantial for high ESI industries, where the ESI coverage rate fell by 0.8 percentage points. Workers in high ESI industries saw an increase in the uninsured rate between 2010 and 2013, and 200,000 more were uninsured. Workers in low ESI industries, conversely, had a 0.6 percentage point reduction in the uninsured rate between 2010 and 2013 due to increases in Medicaid coverage. However, because of the population growth in low ESI industries, there were 400,000 more workers in low ESI industries without health insurance in 2013 than in 2010.