5 Key Facts About Medicaid and Provider Taxes

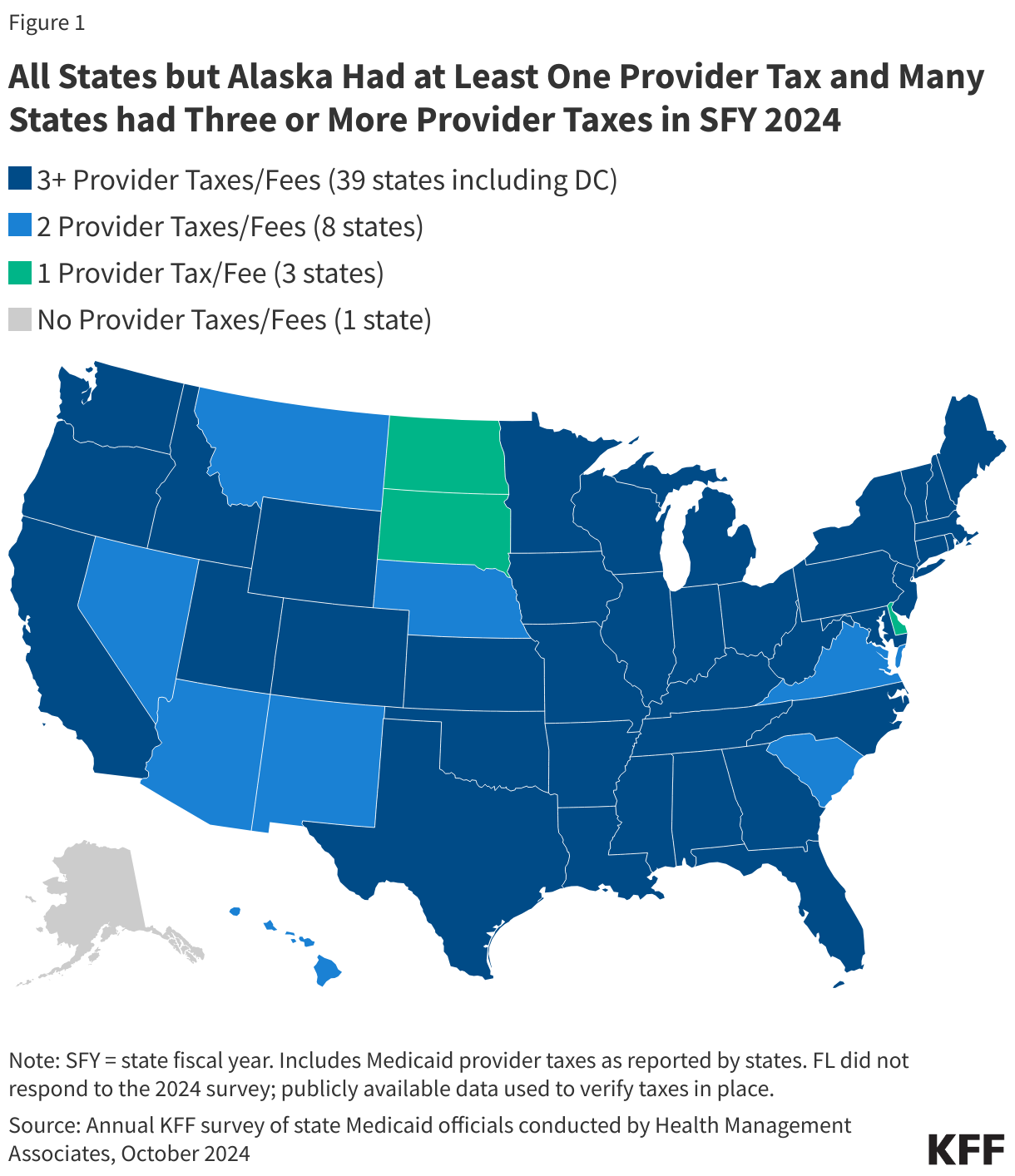

To meet House budget resolution requirements, Congress will need to make major cuts to federal spending on Medicaid. An option under consideration is to limit the use of state taxes on providers, which could save hundreds of billions of dollars according to the Congressional Budget Office (CBO). Medicaid is jointly financed by the federal government and the states, with the federal government paying close to 70% of total costs in fiscal year (FY) 2023. States are permitted to finance the non-federal share of Medicaid spending through multiple sources, including state general funds, health-care related taxes (referred to as “provider taxes” throughout this brief), and local government funds. All states except for Alaska finance some of the state costs with taxes on health care providers, which may be imposed as a percentage of provider revenues or using an alternative formula such as a flat tax on the number of facility beds or inpatient days. The most common provider taxes are levied on nursing facilities (46 states) and hospitals (45 states).

To meet House budget resolution requirements, Congress will need to make major cuts to federal spending on Medicaid. An option under consideration is to limit the use of state taxes on providers, which could save hundreds of billions of dollars according to the Congressional Budget Office (CBO). Medicaid is jointly financed by the federal government and the states, with the federal government paying close to 70% of total costs in fiscal year (FY) 2023. States are permitted to finance the non-federal share of Medicaid spending through multiple sources, including state general funds, health-care related taxes (referred to as “provider taxes” throughout this brief), and local government funds. All states except for Alaska finance some of the state costs with taxes on health care providers, which may be imposed as a percentage of provider revenues or using an alternative formula such as a flat tax on the number of facility beds or inpatient days. The most common provider taxes are levied on nursing facilities (46 states) and hospitals (45 states).

Proponents of restricting provider tax authority say that providers and states receive federal matching funds without expending their own money, which can “inflate a state’s Medicaid match.” As the debate about broader Medicaid spending reductions continues, Republicans may try to recast restrictions on provider taxes as addressing fraud, waste, and abuse. Opponents of such restrictions note that provider taxes are permissible under current law and help fund Medicaid; and restricting provider taxes will create financing gaps for states that could result in higher state taxes, reductions in Medicaid eligibility, lower provider payment rates, and fewer covered benefits. Both proponents and opponents of new restrictions agree that the limited data about provider taxes makes it difficult to assess states reliance on them as a funding source and to understand how they affect net payments to providers. The Medicaid and CHIP Payment and Access Commission has submitted recommendations to Congress that states start reporting new data on Medicaid taxes and that those data be publicly available for analysis.

In light of the current debate, this issue brief uses data from KFF’s 2024-2025 survey of Medicaid directors, to describe states’ current provider taxes and the federal rules governing them.

1. All states except for Alaska use provider taxes to help finance the state share of Medicaid spending.

The federal government and states share responsibility for financing Medicaid, with the federal government guaranteeing states federal matching payments with no pre-set limit. States have considerable flexibility in determining how to finance the non-federal share of state Medicaid payments. In state FY 2024, states reported that about 68% of state Medicaid spending came from general funds, most of which come from income and sales taxes. The remaining 32% was funded by other sources including local government funds and provider taxes.

Medicaid provider taxes are defined as those for which at least 85% of the tax burden falls on health care items or services or entities that provide or pay for health care items or services (see Social Security Act, Section 1903(w)(3)(A)). States use provider tax revenues to fund Medicaid “base” rates and supplemental payments, to avoid Medicaid benefit cuts, and to expand Medicaid benefits. Some states have used revenue from provider taxes to finance the ACA Medicaid expansion. Beyond helping finance the state share of Medicaid, permissible tax arrangements may have potential financial benefits for providers who are subject to the tax and serve a high volume of Medicaid patients.

All states but Alaska finance part of the state share of Medicaid funding through at least one provider tax and 39 states have three or more provider taxes in place (Figure 1). While data are limited, the Government Accountability Office (GAO) estimated that provider taxes as a percent of the non-federal share of Medicaid spending in SFY 2018 ranged from less than 0.5% in New Mexico, South Dakota, Texas, and Virginia to more than 30% in Michigan, New Hampshire, and Ohio. Over time, states have increased their reliance on provider taxes, with expansions often driven by economic downturns. GAO reported that reliance on provider taxes had grown significantly over the preceding decade, increasing from 7% in 2008 to 17% in 2018. There are no more current estimates that are publicly available of provider taxes as a share of Medicaid spending.

2. Federal rules set limits on how states can use provider taxes.

States first began using provider taxes to finance the state share of Medicaid in the 1980s, when Medicaid providers would donate funds or agree to be taxed and the revenues from those donations and taxes would be used to finance a portion of the state’s share of Medicaid. According to the Congressional Research Service, states were essentially “borrowing funds from Medicaid providers in order to draw down federal funds and increase Medicaid payment rates to the providers that had paid taxes or donated funds.” The particularly aggressive use of those taxes by some states spurred statutory and regulatory limitations on provider taxes starting in the 1990s. Federal rules now specify that provider taxes must be:

- Broad-based, which means the tax is imposed on all providers within a specified class of providers (e.g., the tax cannot be imposed only on providers that see primarily Medicaid patients);

- Uniform, which means the tax must apply equally to all providers within the specified class (e.g., the tax rate cannot be higher on Medicaid revenue than non-Medicaid revenue); and

- Not hold taxpayers (providers) “harmless,” which means states are prohibited from directly or indirectly guaranteeing that providers will receive their tax revenues back (i.e., be “held harmless”).

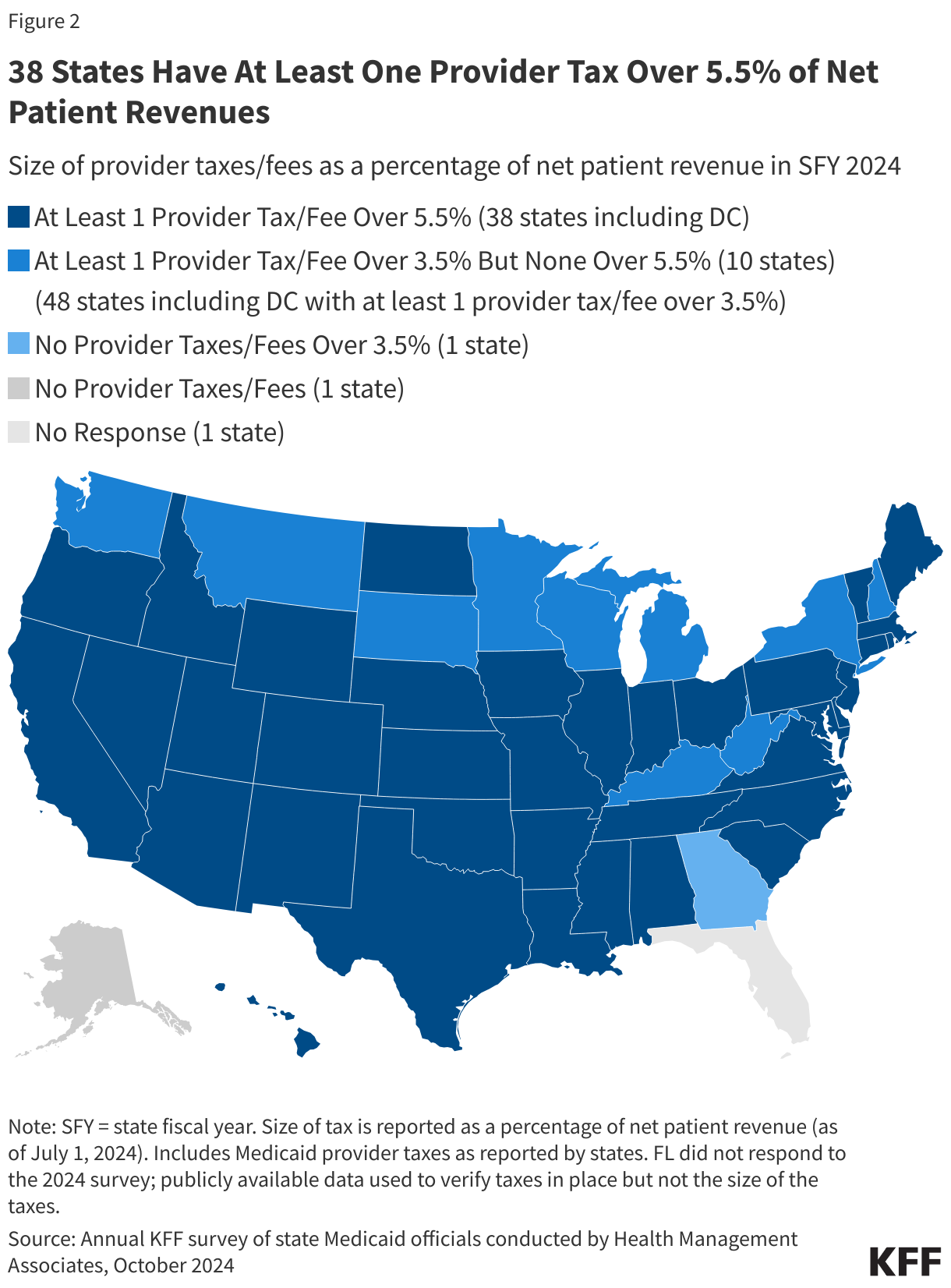

There are 19 classes of providers that the Centers for Medicare and Medicaid Services (CMS) uses to ensure that the tax programs are broad-based and uniform (see 42 CFR Section 433.56). In assessing whether provider taxes comply with federal laws, current regulations specify that the hold harmless requirement does not apply when the tax revenues comprise 6% or less of net patient revenues from treating patients (see 42 CFR Section 433.68), a level sometimes referred to as a “safe harbor” limit. States may also receive waivers of the requirement that taxes be broad-based and uniform if the state can prove the net effect of the tax is “generally redistributive,” and that the amount of tax is not directly related to Medicaid payments.

Policy proposals that would reduce the “safe harbor” limit below 6% could affect most significantly the 38 states that have one or more provider taxes that exceed 5.5% of provider net patient revenues (Figure 2). However, if the limit were reduced significantly enough, all states with provider taxes could be affected. There are 10 states with at least one provider tax that is between 3.5% and 5.5% of net patient revenues. One state (Georgia) reports that all provider taxes are below 3.5% of net patient revenues.

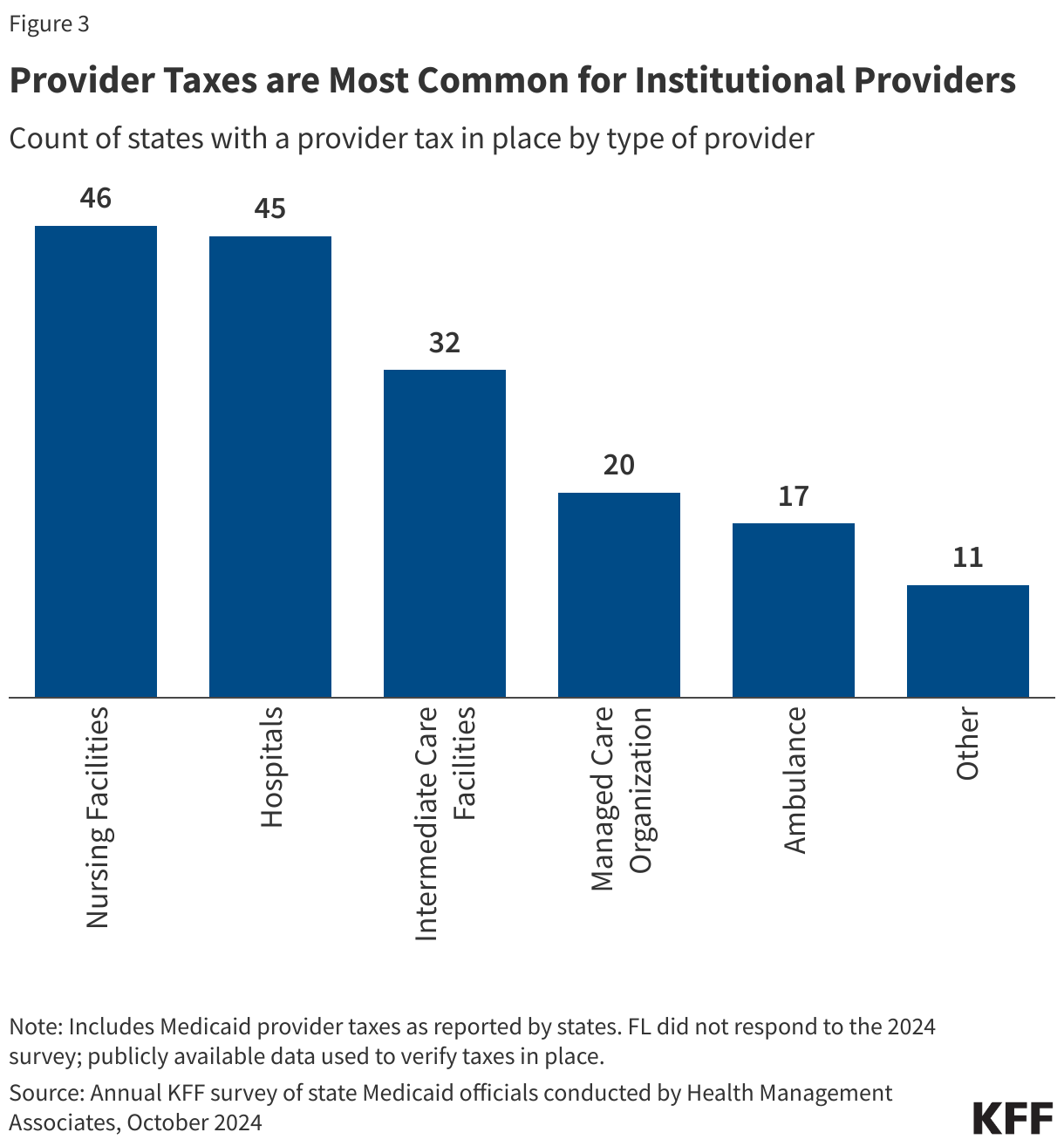

3. Provider taxes are most common for institutional providers.

Provider taxes fall on a wide range of provider types but are most common for institutional providers including nursing facilities (46 states), hospitals (45 states), and intermediate care facilities for people with intellectual or developmental disabilities (32 states, Figure 3). States often use provider tax revenues to support payment rates for providers, often by financing supplemental payments like disproportionate share hospital (DSH) payments, upper payment limit (UPL) payments, and managed care state directed payments (uniform payment increases through managed care that are similar to supplemental payments). Hospitals’ base fee-for-service rates vary considerably across states and, on average, are below hospitals’ costs of providing services to Medicaid enrollees and below Medicare payment rates for comparable services, causing some states to rely more heavily on supplemental payments than others to help cover hospitals’ costs. It is unknown from available data how much states are paying hospitals after accounting for base payments, supplemental payments, and the costs of provider taxes (e.g., the net payment rate), which is one reason why the Medicaid and CHIP Payment and Access Commission has called for greater transparency around provider taxes.

Although data on the use of revenues from provider taxes are limited, GAO found that in 2018, states financed a higher percentage of the state share of supplemental payments (e.g., DSH and non-DSH supplemental payments) using provider taxes than they did for other types of Medicaid payments (i.e., base payments). The use of provider taxes to fund supplemental payments to providers has raised some questions regarding compliance with hold harmless requirements for provider taxes. In April 2024, CMS released guidance to states about this issue, noting they will work with states to identify impermissible hold-harmless arrangements but will not take enforcement action until January 2028, allowing states time to come into compliance.

Beyond institutional providers, 20 states have provider taxes on managed care organizations (MCOs), 17 on ambulance providers, and 11 on “other” provider types such as ambulatory care facilities and home care providers (Appendix Table 1). The Deficit Reduction Act of 2005 required states that tax Medicaid MCOs to tax all MCOs uniformly, thus limiting the ability of states to only tax Medicaid MCOs. However, CMS has the authority to waive the uniformity requirement, and other federal requirements if the tax is determined to be “generally redistributive.” The formula for determining whether a waiver request is “redistributive” has allowed states to impose Medicaid taxes primarily on Medicaid enrollees, raising CMS concerns. For example, in California the tax is set at a much higher rate for Medicaid enrollees relative to privately-insured enrollees, which means that 99% of the tax burden falls on Medicaid member months. As a result, there may be issues with the hold harmless requirements because the MCOs paying for nearly all the tax payments also receive premium payments from the state to provide Medicaid coverage, and those premium payments reflect the tax expense. In its approval letter of California’s recent provider tax waiver in January 2025, CMS included a companion letter informing the state that CMS was contemplating proposed regulatory changes that could affect the legality of California’s MCO tax in future years.

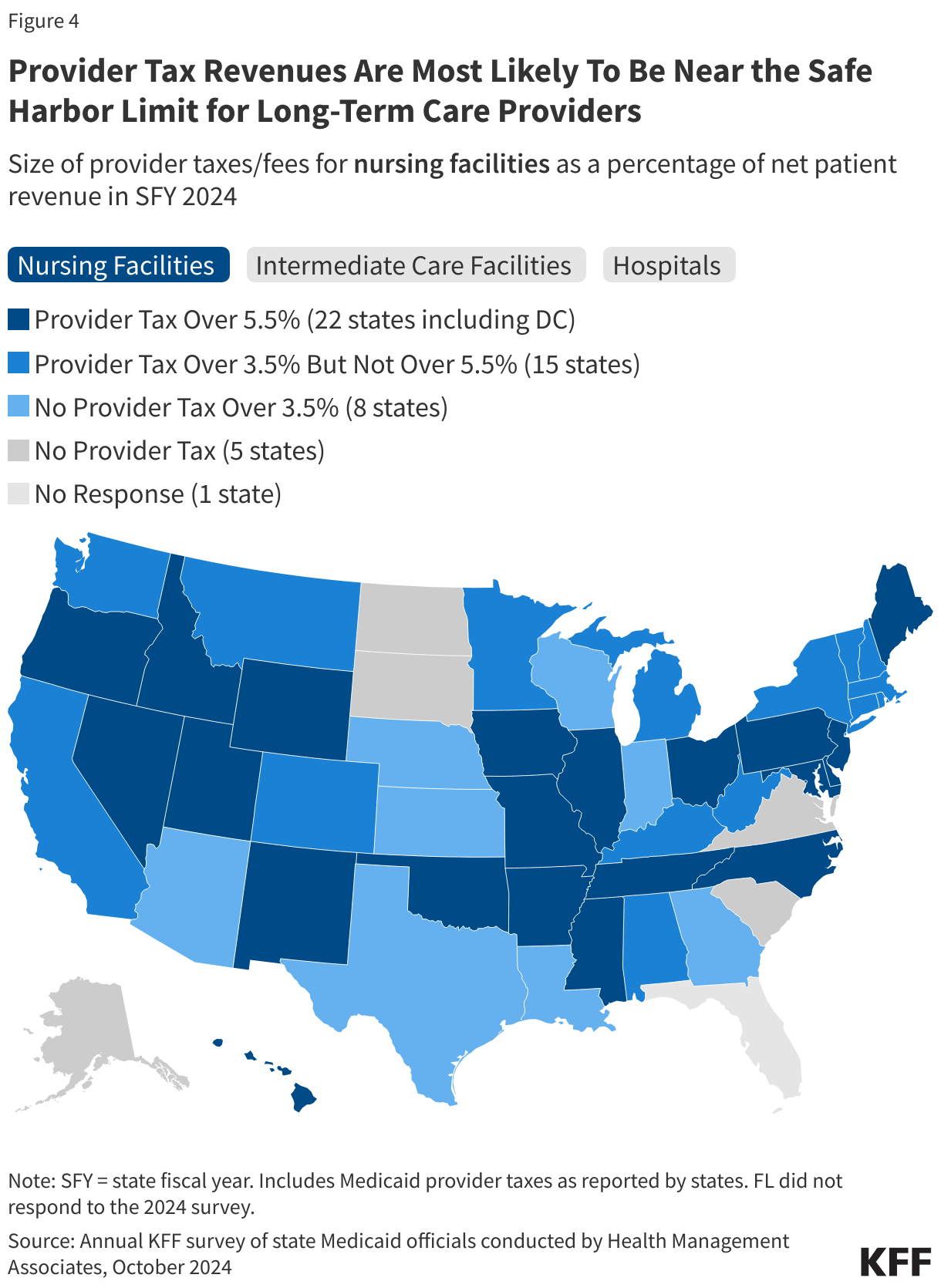

4. Provider tax revenues are most likely to be near the safe harbor limit for long-term care providers.

Tax revenues are nearest to the safe harbor limit most often for nursing facilities and intermediate care facilities for people with intellectual or developmental disabilities (Figure 4). If provider tax revenues are 6% or less of patient net revenues, they are not subject to hold harmless requirements, meaning the revenues may fund payments back to the providers being taxed. Proposals to reduce the 6% “safe harbor” limit would likely most significantly affect states with taxes already near the upper limit. Provider taxes that exceed 5.5% of net patient revenue are most common for nursing facilities (22 states) and intermediate care facilities (17 states), both of which provide long-term care for people who need help with the activities of daily living. There are also 13 states that have provider taxes exceeding 5.5% of net patient revenues for hospitals.

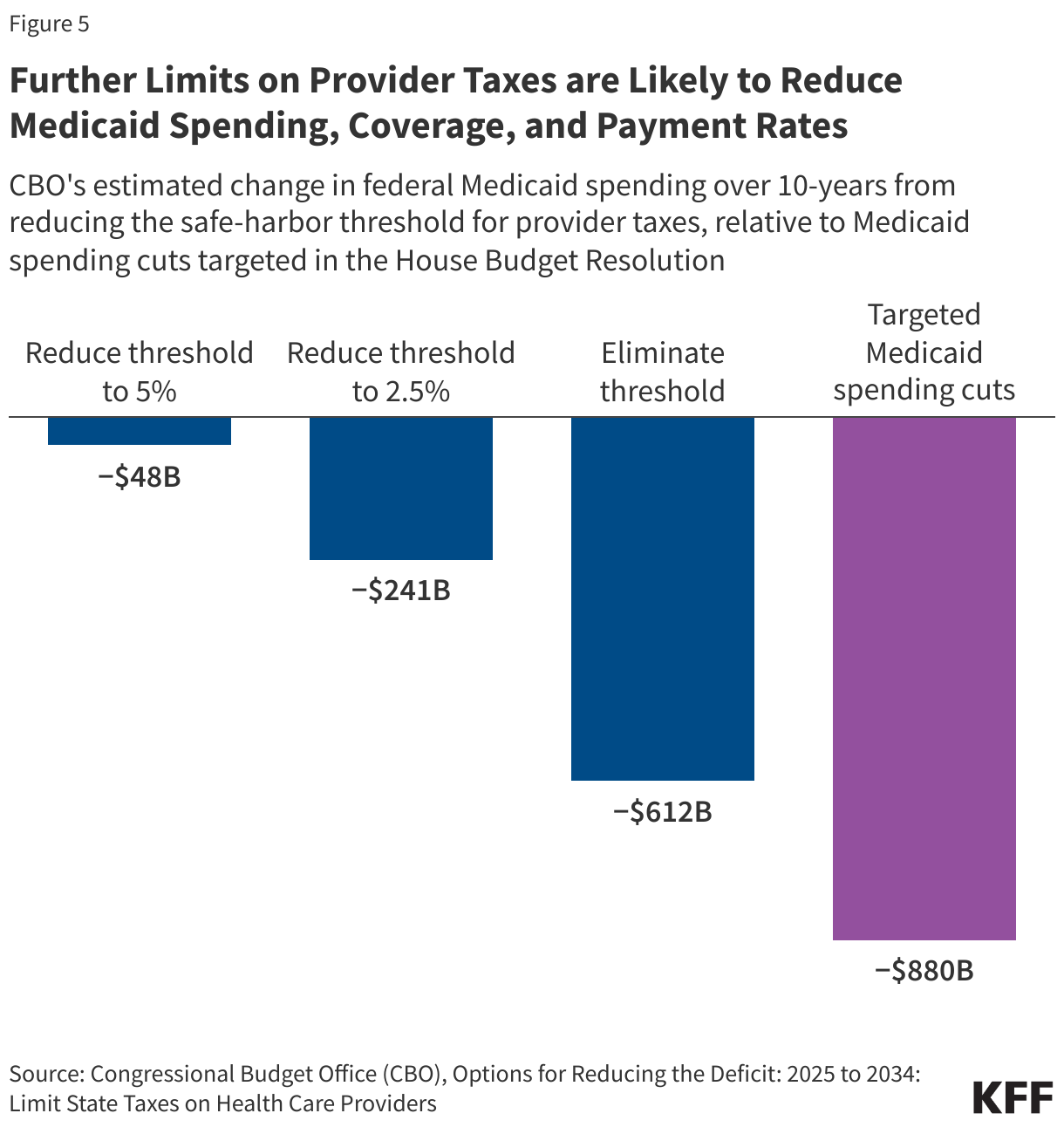

5. Further limits on provider taxes are likely to reduce Medicaid spending, coverage, and payment rates.

The recently passed House budget resolution targets cuts to federal Medicaid spending of up to $880 billion or more over a decade. To put the size of the spending cuts in perspective, $880 billion represents 6% of state taxes per resident and 19% of states’ spending on education per pupil, so offsetting the loss of federal revenues would be challenging for states, particularly considering that states generally must balance their budgets. Assuming states will be unable to replace cuts of that magnitude, they will face difficult choices about whether to reduce Medicaid spending by covering fewer people, eliminating optional benefits, or reducing provider payment rates.

There are not yet detailed proposals under consideration by Congress to achieve federal Medicaid spending reductions, but the Congressional Budget Office (CBO) estimated that reducing the safe harbor limit for provider taxes could save tens or hundreds of billions of dollars depending on the size of the reduction (Figure 5). If the hold-harmless threshold were reduced to 5%, CBO estimates the federal government would save $48 billion over 10 years. If the hold-harmless threshold were eliminated, savings would be $612 billion.

CBO’s estimates of federal spending reductions are based on the agency’s assessment that states will reduce Medicaid spending, resulting in people losing Medicaid coverage. While CBO provides national estimates, the effects would vary significantly across the states. States with provider taxes near the safe harbor limit would be affected by even modest changes whereas states with lower provider taxes would only be affected by more significant reductions. Effects on total Medicaid spending and enrollment would also vary based on how much states offset lost provider tax revenues with other sources of funding. Because provider taxes often support Medicaid payment rates, there will almost undoubtedly be downward pressure on payment rates if provider taxes are restricted, particularly for institutional providers including nursing facilities, intermediate care facilities, and hospitals.