California's Uninsured on the Eve of ACA Open Enrollment

Section 1: California's uninsured and the ACA

| A NOTE ON TERMINOLOGY:The ‘Eligible Uninsured’: For purposes of this report, the eligible uninsured are defined as those Californians ages 19-64 who have been without coverage for at least two months. Because the coverage expansions under the ACA do not extend to undocumented immigrants, most analysis is based on the 78 percent of the uninsured group who report being U.S. citizens or permanent residents, described for the purposes of easy understanding as the ‘eligible uninsured’.

Income categories: Because eligibility for two of the law’s main components – the Medi-Cal expansion and the tax credits to help purchase insurance on the new exchanges – is based on an individual’s family income relative to the federal poverty level (FPL), in many cases we report survey results among the eligible uninsured by FPL categories. Those with incomes 138% FPL or less (roughly $32,000 a year for a family of 4) will be eligible for Medi-Cal coverage, while those with incomes greater than 138% and up to 400% FPL (roughly $32,000-$94,000 for a family of 4), will be eligible for subsidies to purchase insurance through Covered California, the state’s new marketplace. Those with incomes above 400% FPL will be allowed to buy insurance through Covered California, but will not be eligible for subsidy assistance. For convenience, we will sometimes refer to the group with incomes 138% FPL or less as the “Medi-Cal target group”, and those greater than 138% and up to 400% FPL as the “exchange subsidy target group”. These obviously are approximations that do not allow for every real world exception to be taken into account. For example, lawfully present immigrants may remain subject to a five year wait before they may enroll in Medi-Cal, but for the purposes of this analysis they are included in the Medi-Cal target group if they meet the income criteria. Similarly, some of those in the exchange subsidy target group may not be eligible for marketplace subsidies if they have access to affordable employer coverage, a situation difficult to ascertain in a phone survey. |

Limited familiarity, cautious optimism

SUMMARY: Positive views of the ACA outnumber negative among California’s eligible uninsured, even as the large majority say they don’t yet understand how the law will impact their own families and few have heard much about either the expansion of the Medi-Cal program or the creation of the state’s Covered California insurance marketplace.

California’s uninsured tilt positive on ACA

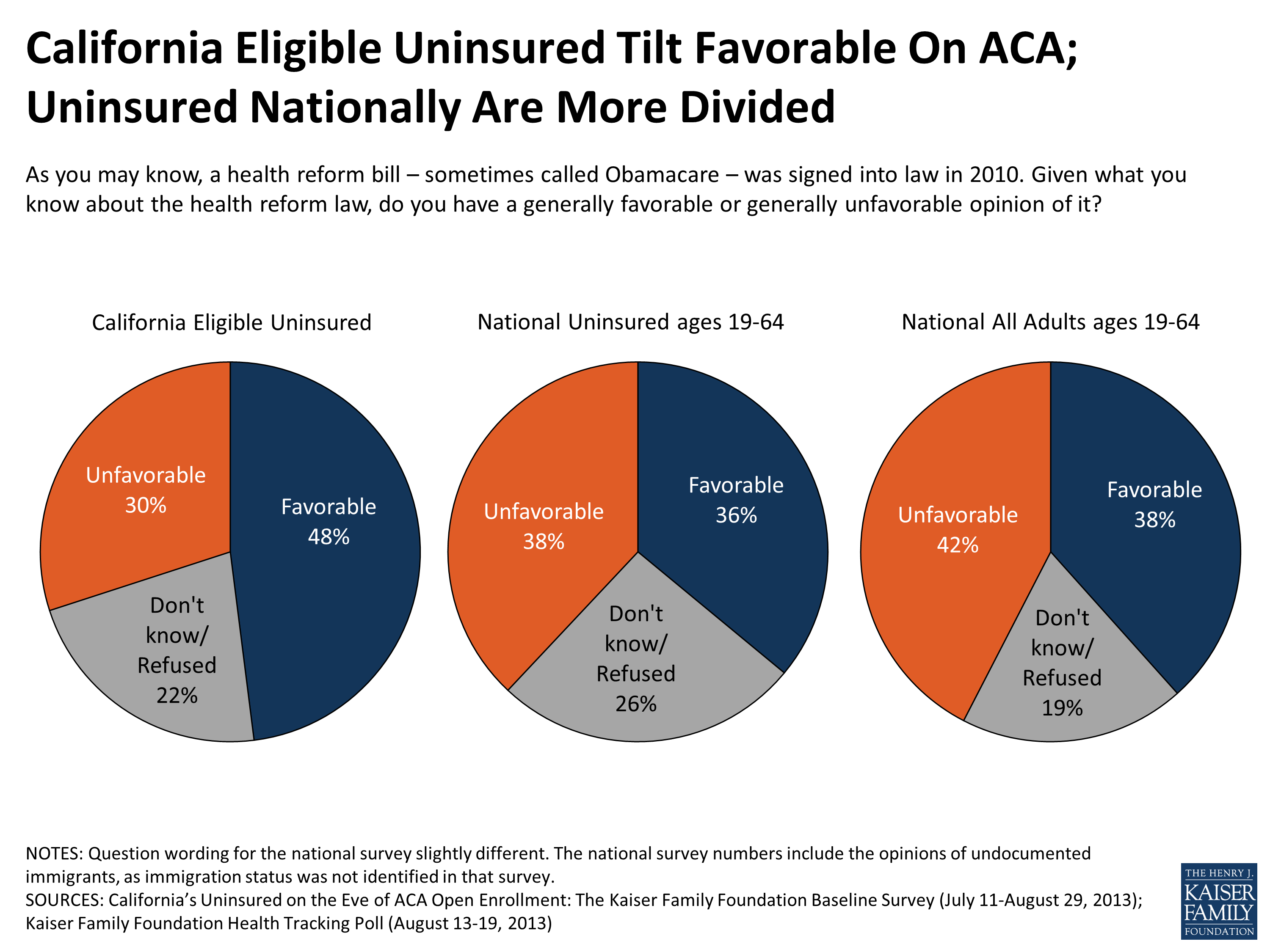

California’s eligible uninsured tilt more positive than negative on the 2010 health care law, particularly in comparison to the nation as a whole, but no one view is shared by a majority.

Overall, 48 percent of California’s eligible uninsured view the ACA favorably, while 30 percent view it unfavorably and one in five (22 percent) were not able to provide an opinion. Nationally, Americans in the same age range are more divided, 38 percent favorable versus 42 percent unfavorable in KFF’s August Health Tracking Poll, and the uninsured nationally are evenly divided at 36 percent favorable versus 38 percent unfavorable.

Figure 1

But large majority say they don’t have enough information yet to understand how ACA will impact them personally

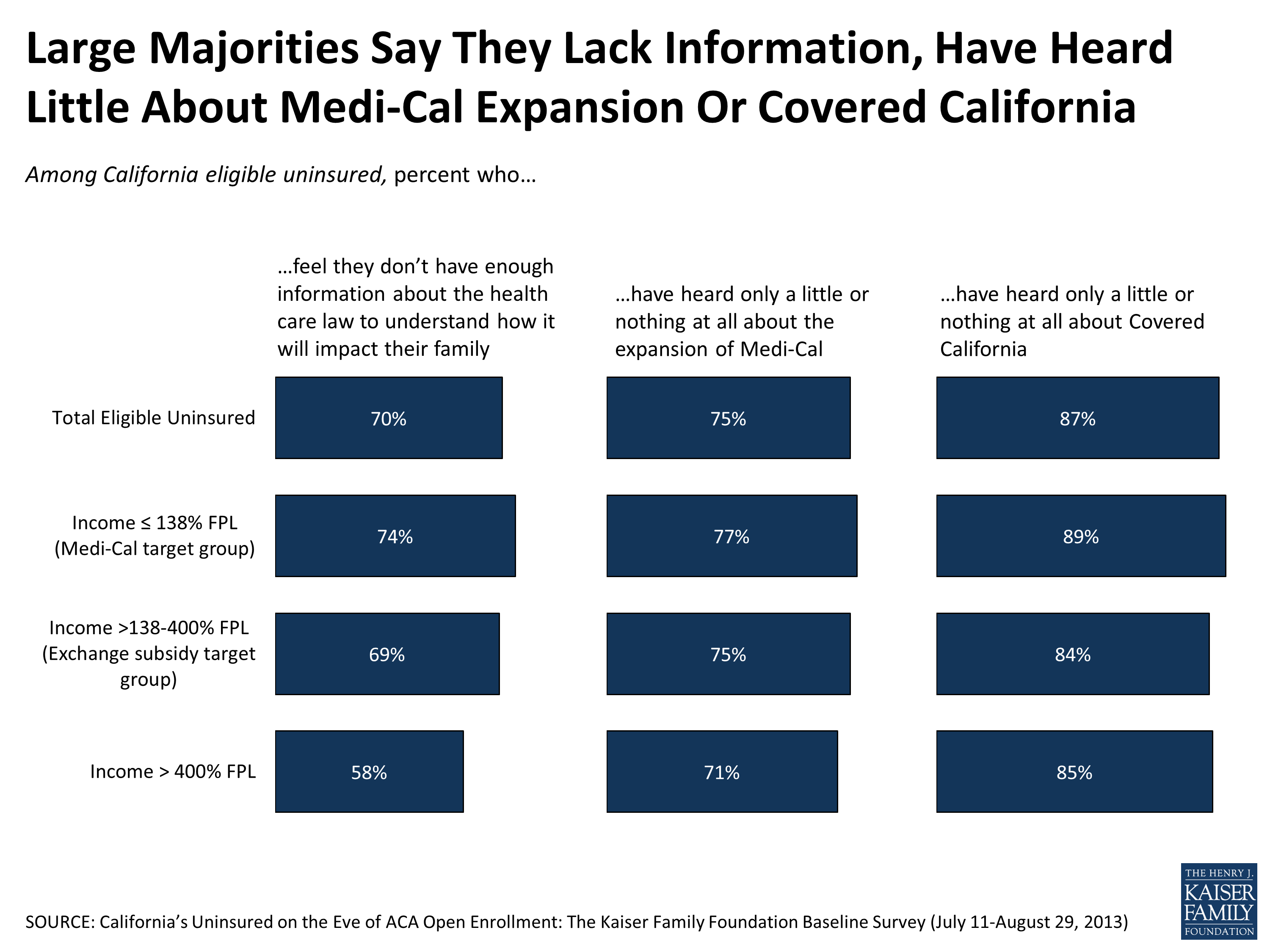

As of late August, the large majority of California’s eligible uninsured – seven in ten (70 percent) – say they don’t feel they have enough information about the law to understand how it will impact them. In no demographic subgroup we examined does a majority say they know enough about the law at this point to understand its personal ramifications.

Figure 2

As the summer of 2013 comes to a close, and the season of intensive outreach begins, three-quarters say that they have heard “only a little” or “nothing” (32 percent and 43 percent respectively) about the expansion of Medi-Cal, including 77 percent of those in the Medi-Cal target group.

And more than eight in ten (84 percent) of those in the exchange subsidy target group say they have heard little or nothing about the state’s new marketplace, Covered California.

One in five uninsured report seeing an ACA-related ad

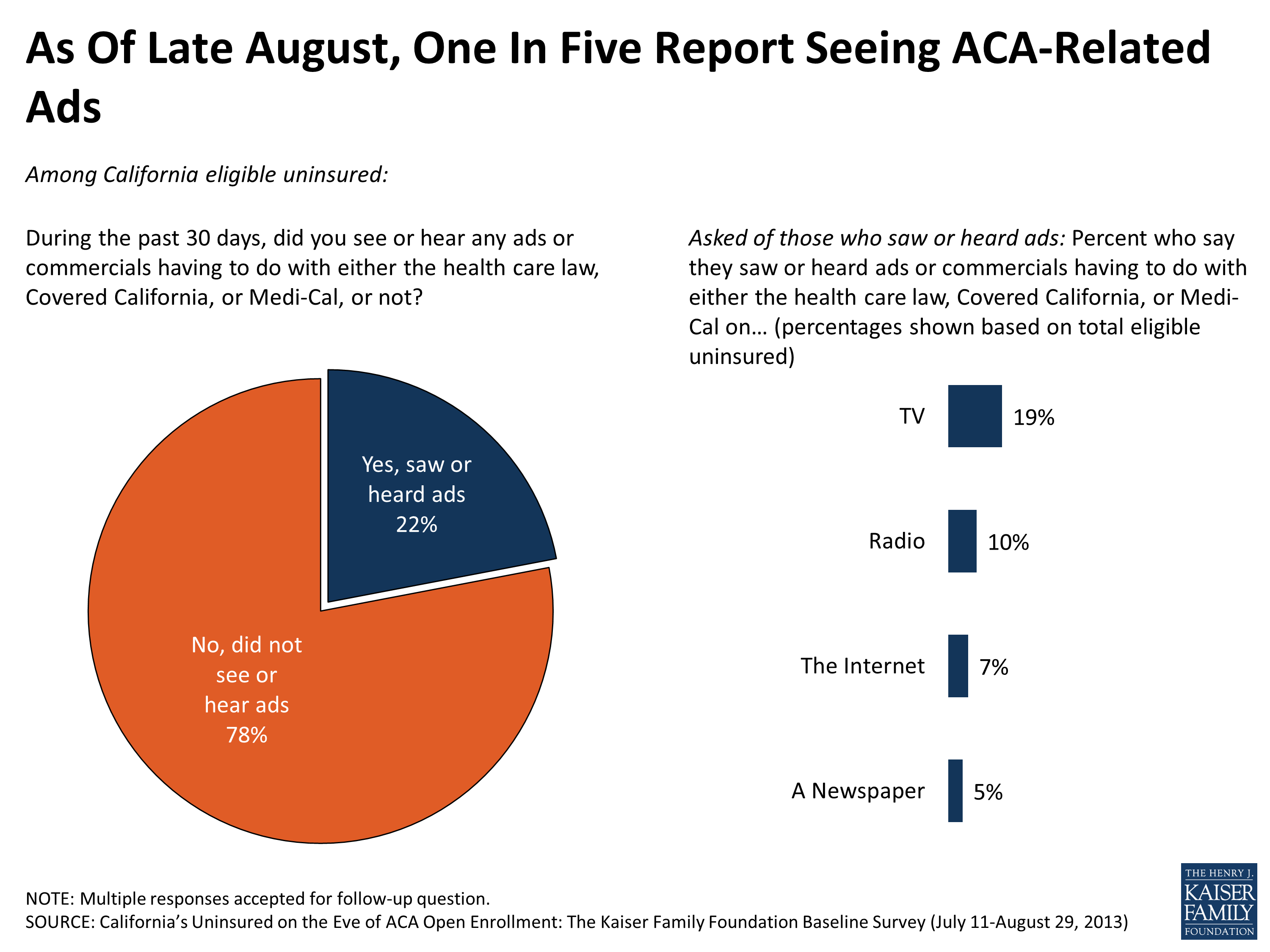

The state’s marketplace and other interested parties began an ongoing process of outreach toward the uninsured population earlier this summer, one that is still in the process of ramping up (for example, Covered California itself unveiled its first television ad in late August.) At this early point in the ad campaign, about one in five of California’s eligible uninsured report having seen or heard an ad having to do with the health care law, Covered California or Medi-Cal. Most of these reported having seen multiple ads on the topic, with TV by far the most frequently named delivery vehicle, followed by radio.

Figure 3

Nearly half in the group that have seen an ad report that at least one of the commercials they saw provided information about how to get health insurance coverage, while the other half do not remember being provided any instruction. Overall, so far six percent of California’s eligible uninsured report that the advertising has driven them to seek out further information about the law.

About half aware of Medi-Cal expansion, creation of marketplaces and availability of subsidies

About half the eligible insured are aware, however, of the two key coverage expansions being a part of the 2010 health law, even if they have not heard much about them recently. For example, half of the state’s eligible uninsured are aware that the ACA does provide for expansion of Medi-Cal, including similar shares of those in the eligible income group. And half report knowing that the law creates health insurance exchanges or marketplaces, with knowledge somewhat higher in the exchange subsidy target group (57 percent) than in the Medi-Cal target group (45 percent). Roughly the same share are aware that the federal government will subsidize the purchase of health insurance on Covered California for many in these income groups.

In each case, however, this does leave roughly half the target populations unaware that these provisions even exist as part of the ACA.

| Figure 4: About Half of Eligible Uninsured Aware Health Reform Law Includes Medi-Cal Expansion, Provision of Tax Credits on Exchanges | ||||

| Among California eligible uninsured: Percent who say yes, the health care law does each of the following | Total eligible uninsured | ≤138% FPL (Medi-Cal target) | >138%-400% FPL (exchange subsidy target) | >400% FPL |

| Require nearly all Americans to have health insurance by 2014 or else pay a fine | 57% | 52% | 63% | 56% |

| Expand the Medi-Cal program to cover more low-income Californians | 53 | 52 | 53 | 58 |

| Provide financial help to low and moderate income Americans who don’t get insurance through their jobs to help them purchase health insurance coverage beginning in 2014 | 52 | 52 | 54 | 48 |

| Create health insurance exchanges or marketplaces where people who don’t get coverage through their employers can shop for insurance and compare prices and benefits | 50 | 45 | 57 | 51 |

| Prohibit insurance companies from denying coverage because of a person’s medical history | 45 | 39 | 52 | 48 |

Meanwhile, more than half the uninsured (57 percent) are aware of the existence of the individual mandate, a provision that will apply to many of them. Finally, over four in ten (45 percent) are aware of the guaranteed issue provision that mean that many of the eligible uninsured – including those who say someone in their household has a pre-existing condition – will be able to qualify for health insurance that may previously have been denied them.

In the big picture, more expect the ACA to make their situations better than worse, with a third expecting no change either way

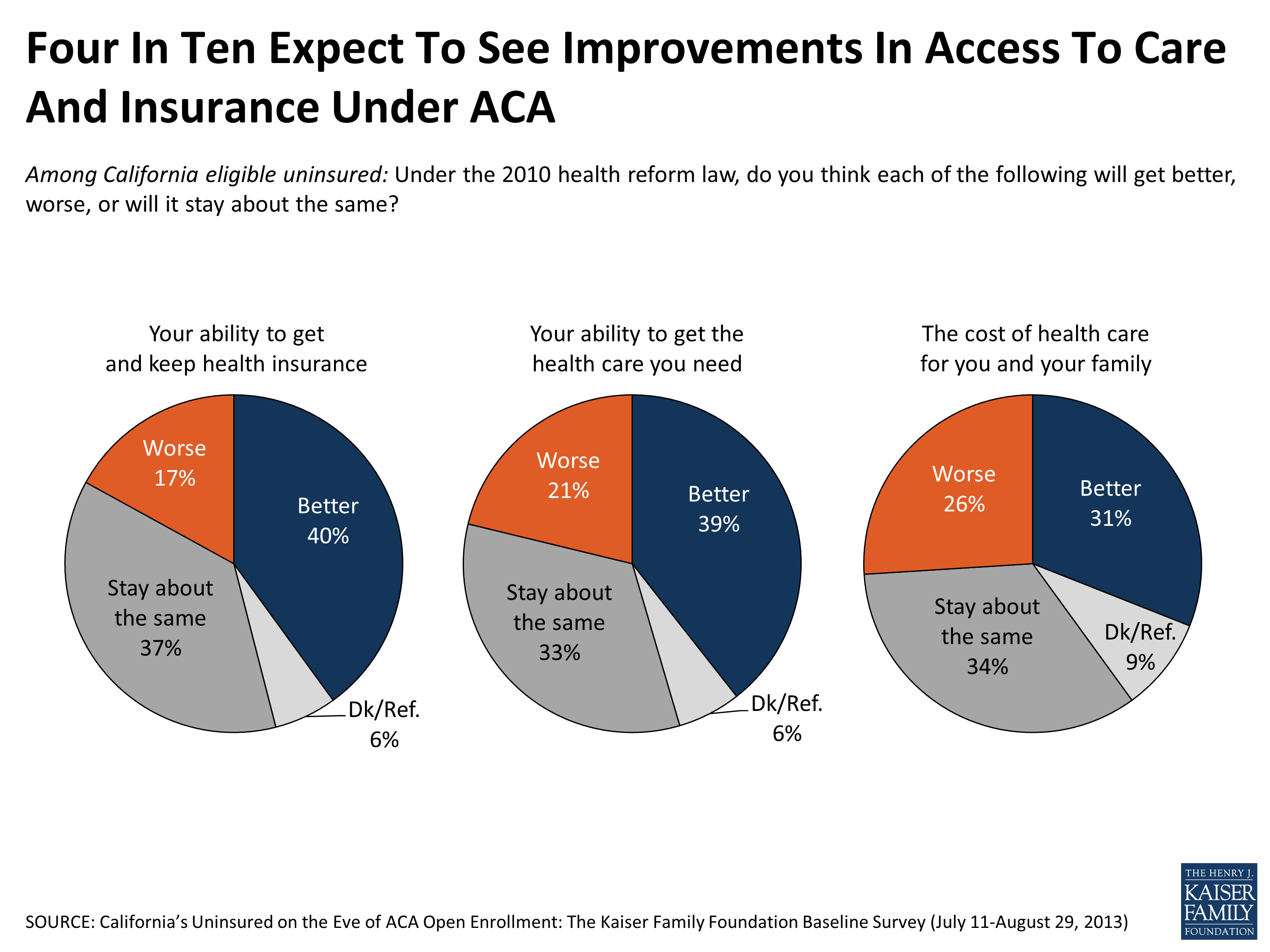

California’s eligible uninsured have mixed expectations as to whether the ACA will be of benefit to them, but overall roughly two times as many expect to be better off as to be worse off. Four in ten believe the law will enhance their ability to get the health care (39 percent) and health insurance (40 percent) they need, compared to about two in ten who expect the law to make life more difficult on these fronts. About a third don’t expect it to make any difference.

Figure 5

Views are more closely divided, however, when it comes to the thorny issue of health care costs: About one in four (26 percent) think the law will raise health care costs for their own family, while a slightly larger share think it will bring costs down (31 percent).

California’s open enrollment period: First reactions

SUMMARY: On the eve of the start of the six-month open enrollment period, there is widespread confusion among the state’s uninsured as to whether they are eligible for any of the new and expanded benefits, with three-quarters in the exchange subsidy target group either not sure or presuming they will not be eligible for such financial assistance, and only half of those in the Medi-Cal target income group presuming they will be qualified.

But there is a good deal of interest in potentially signing up for the Medi-Cal program if those eligibility uncertainties could be put to rest. Nine in ten in the Medi-Cal target group say that, if told they qualified for the state health insurance program, they would enroll. Medi-Cal is viewed quite positively as a program by the uninsured, a group that has widespread ties to the program: over four in ten of those in the Medi-Cal target income range say they have been on Medi-Cal at some point, and another three in ten know someone who has participated in the program.

The survey suggests that, as of late August, when told of the existence of the individual mandate, the preliminary impression of about half the population is that they would plan to get health coverage, with the other half either thinking they won’t get coverage or not sure what they will do. These impressions obviously will shift as the uninsured learn more about the specific ways the law will apply to their own family situation.

Focus on Covered California: Good deal of uncertainty about eligibility to shop in marketplace, get tax credits; Group with limited experience of online shopping

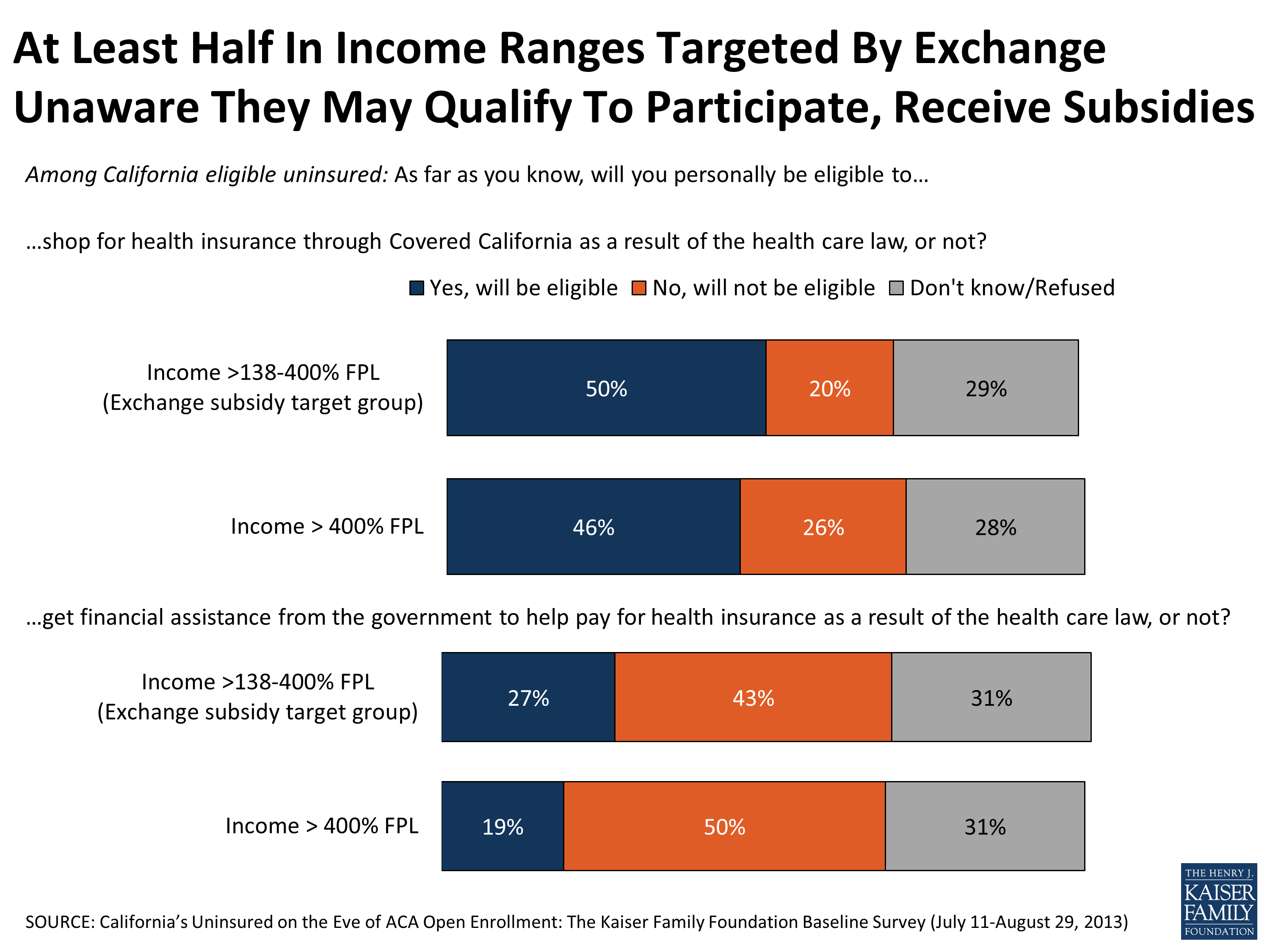

Overall, roughly 2.5 million uninsured state residents may eventually be eligible to shop for coverage using the Covered California marketplace.1 But as we saw in the previous section, familiarity with the statewide marketplace and its benefits is still relatively limited at this point. In this section we examine the uninsured’s current thinking about their own potential eligibility and find that three in four in the subsidy target income group have doubts about whether they would indeed qualify for subsidy assistance. Half are not sure whether they are eligible to shop on the exchanges at all or believe they will not have this option.

Do you think you will be eligible to buy through the state marketplace? For financial assistance from the government?

At summer’s end, half of those with household incomes that fall in the subsidy-eligible range for Covered California say they believe they will be eligible to shop for insurance on the exchange, while three in ten are unsure about whether they could participate. About one in five say they do not believe they will meet the requirements for the exchange. Views among those uninsured making over 400 percent of the FPL – a group eligible to shop in the marketplace but not to receive financial assistance – are similar.

Figure 6

Even fewer in the subsidy target group – just over a quarter – say they think they will be eligible to get financial help from the federal government to help pay for health insurance. The plurality – 43 percent – say they think they will NOT be eligible, and a third aren’t sure. At the same time, roughly one in five (19 percent) of those with incomes above 400 percent of poverty believe they will be eligible for such help, when in reality they are likely to be out of the eligible income range.

Figure 7

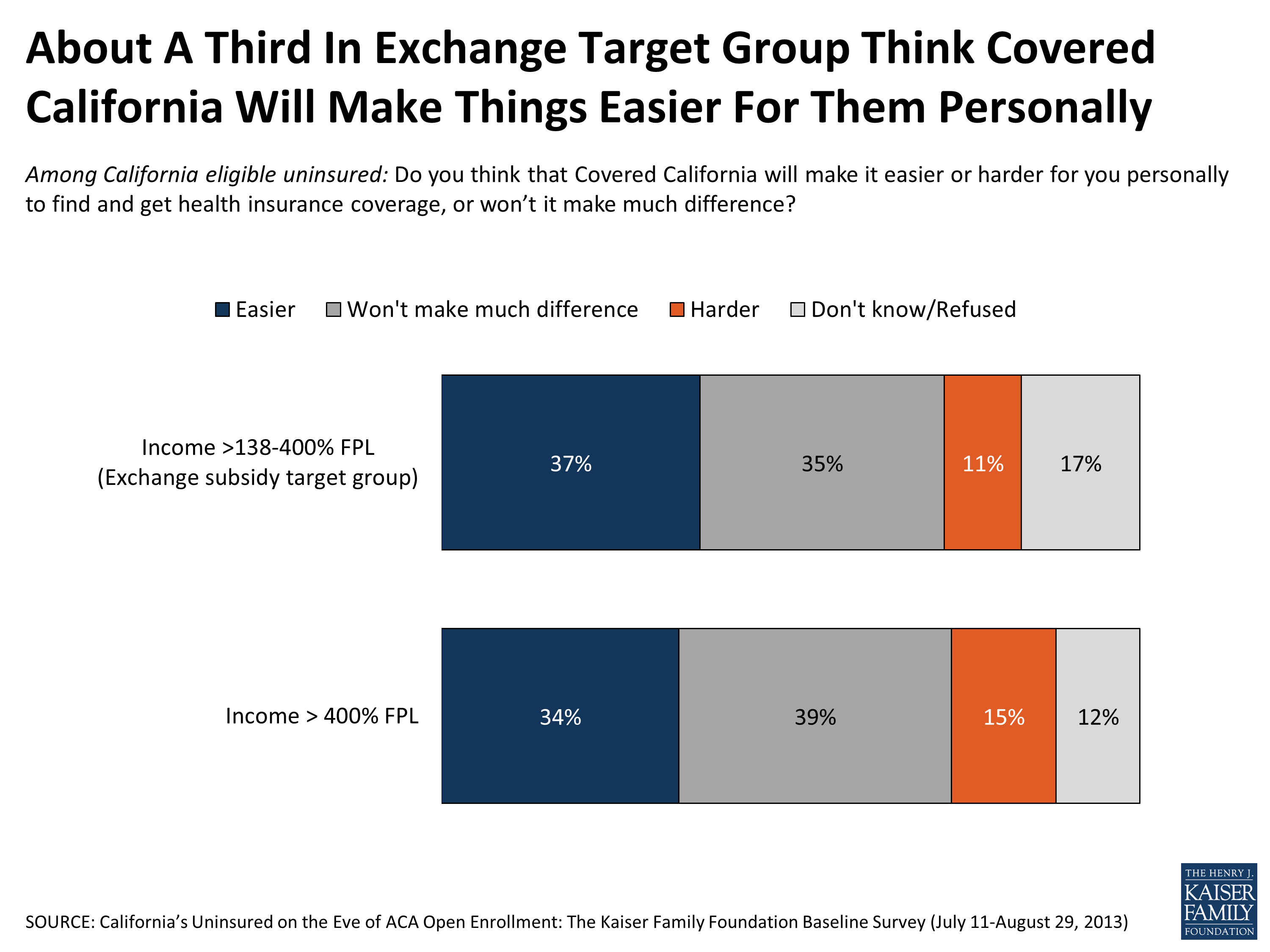

Will Covered California help you?

By better than three to one, those in the exchange subsidy target group think that the state marketplace will make it easier rather than harder for them to find and get insurance coverage (37 percent versus 11 percent). But half either say they don’t expect to see any change at all in their ability to get health insurance (35 percent) or they don’t know what to expect (17 percent).

The exchange eligible and the Internet

One of the primary methods – though not the only method – for accessing Covered California is through its website, www.CoveredCA.com, which allows for online comparison shopping and purchasing. Most of the uninsured in the income group eligible for the tax credits in the marketplace do have Internet access at home (83 percent), and another 9 percent have access somewhere other than home. But they are not intensive Internet shoppers: 25 percent say they very or somewhat often use the Internet to buy products online, 28 percent say they do so ‘just occasionally’, and nearly half say they ‘rarely’ (18 percent) or ‘never’ (29 percent) buy things online. And while 18 percent say they often use the Internet to access health information, 56 percent say they rarely or never do this.

Focus on Medi-Cal: Views of the program, personal connections, and expectations for eligibility in 2014

Eligible uninsured no strangers to Medi-Cal; Majority have positive views of program

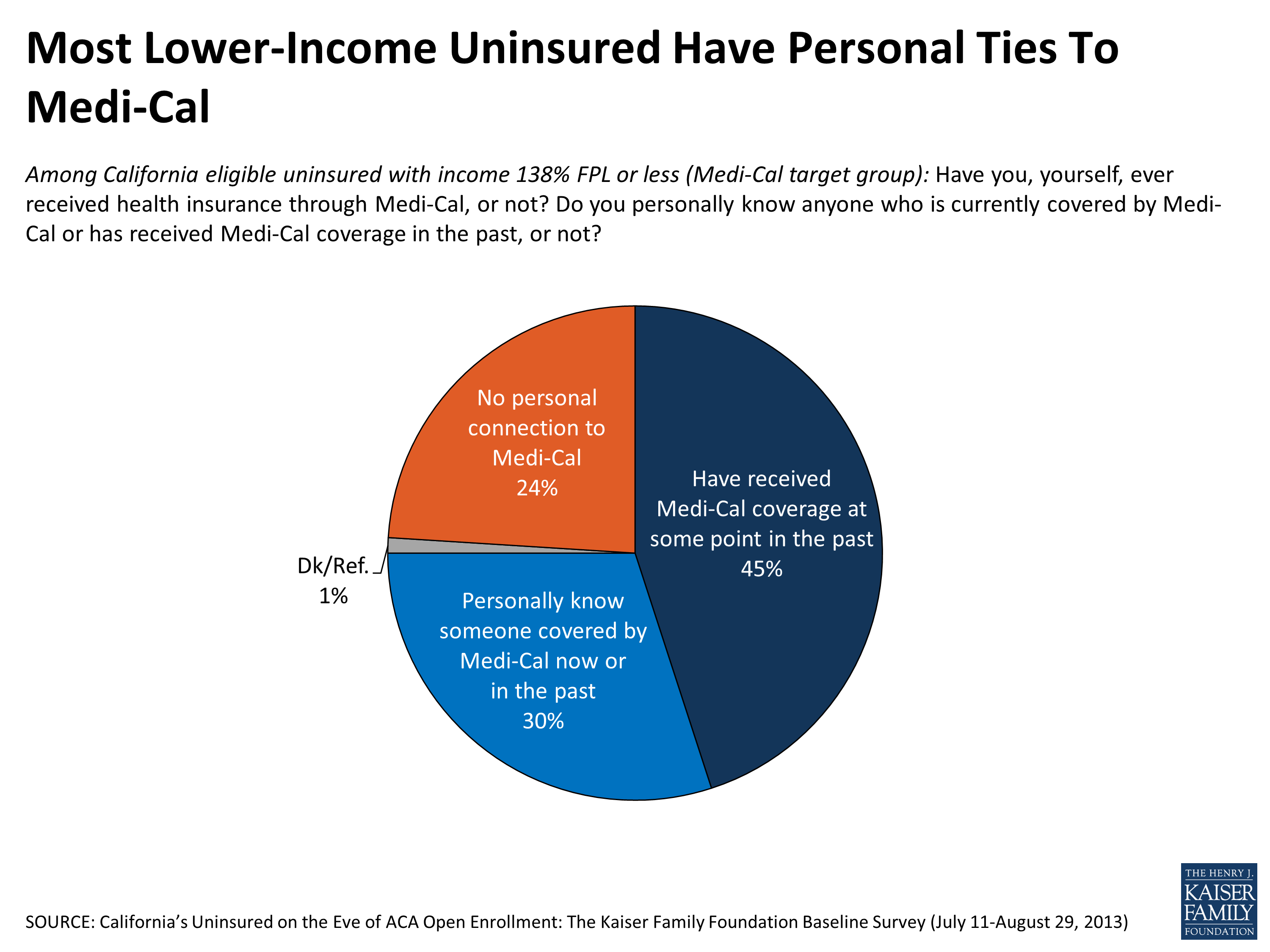

Those uninsured whose incomes put them in the range of the Medi-Cal expansion are for the most part, no strangers to the program. About four in ten (45 percent) say they have already been on Medi-Cal at some point themselves. Another 30 percent know someone that receives or has received health coverage through the program. And all told 18 percent in this income group say they have unsuccessfully tried to sign up for the health insurance program at some point or another, with most of these reporting they could not enroll in Medi-Cal because they were told they were ineligible.

Figure 8

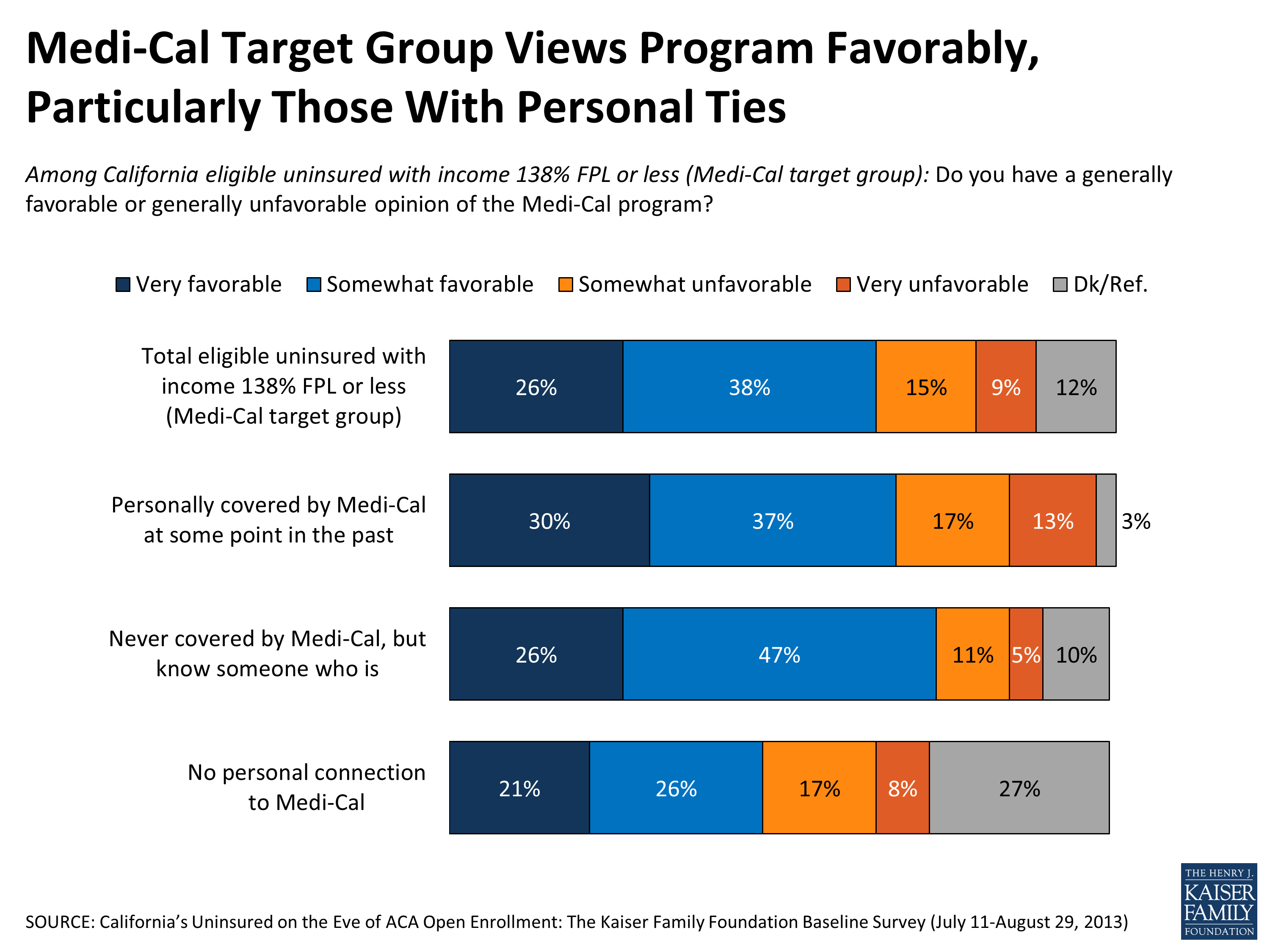

In large part, this group views the program quite positively. Overall, about two-thirds in the Medi-Cal target group have a favorable view of the program, while about a quarter have an unfavorable view. These positive views are driven by those who have themselves been on Medi-Cal or know someone who has: 67 percent and 73 percent, respectively, give the program positive reviews. Those with no connection to the program lean more positive than negative (47 percent versus 25 percent), but a quarter say they don’t know enough about Medi-Cal to offer an opinion. It’s worth noting that under the ACA, the process for Medicaid enrollment is being adjusted to remove perceived barriers to sign-up and to better coordinate with the state exchanges, a factor that could impact ratings of the program moving forward.

Figure 9

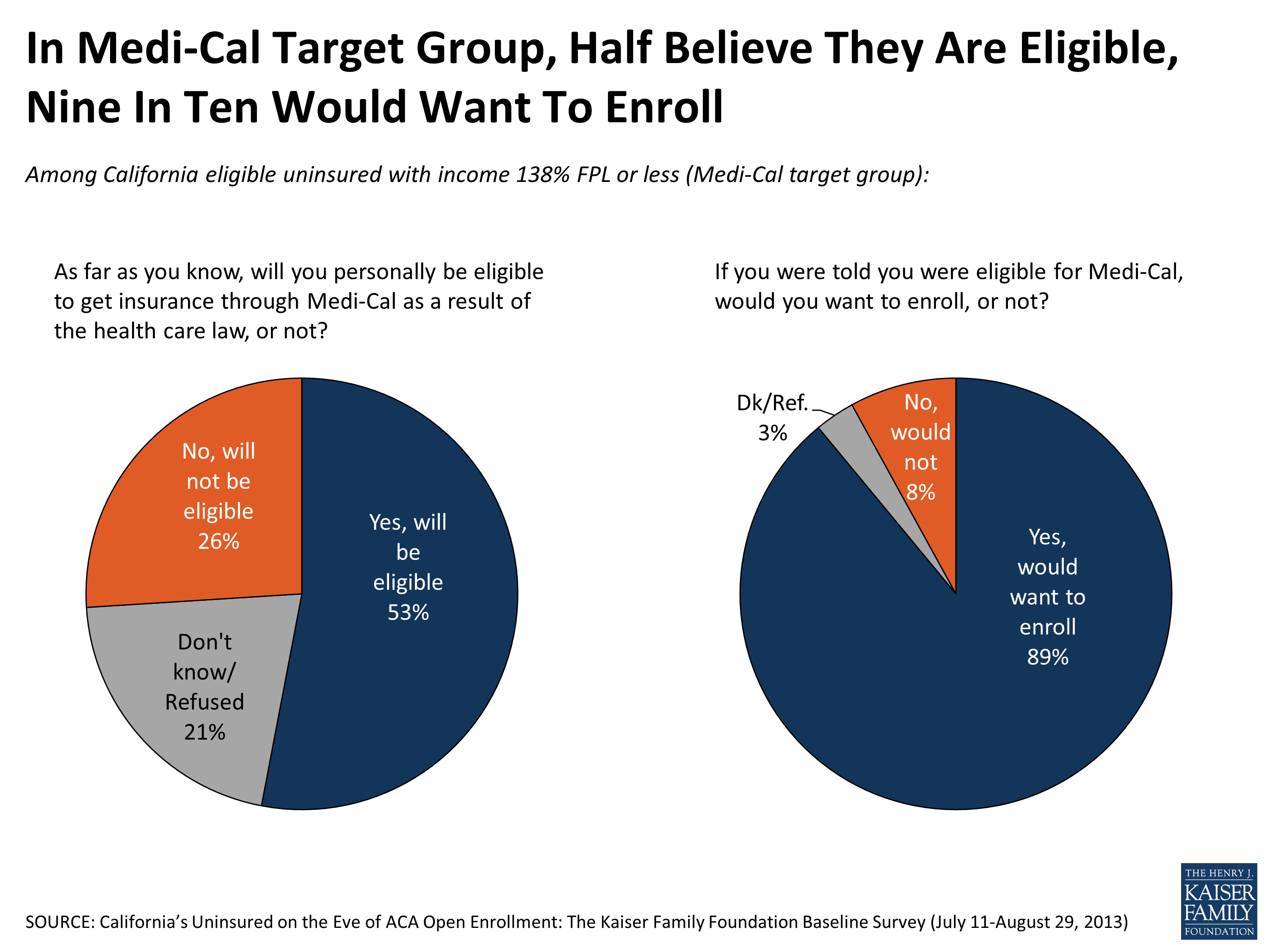

Only half believe themselves eligible for Medicaid under expansion; Nine in ten say they would sign up if told they qualified

Given their connections to the program and their positive evaluations, it follows that there would be a fair bit of interest in enrollment among this group, and the survey bears that out: Nine in ten (89 percent) in the relevant income bracket say that if they were told they were eligible for Medi-Cal, they would want to enroll. The catch at this point, at least, is eligibility confusion. While about half (53 percent) of those in the Medi-Cal target group believe they will be eligible for the program, another 21 percent are not sure and a quarter (26 percent) believe they will not be eligible. Some of this confusion may stem from the fact that eligibility standards are changing under the ACA, and public knowledge may not yet have caught up with these changes. For example, adults without dependent children were previously ineligible no matter what their household income, a standard that has changed under the law.

Figure 10

One pathway this population could use to find out about their possible Medi-Cal eligibility is the state’s new marketplace website. The survey suggests, however, that the Medi-Cal target group includes a relatively large group of people with limited Internet access and experience. More than a third (37 percent) do not have Internet access at home, and fully half have never purchased a product online.

Given knowledge of mandate, half say would likely get health insurance

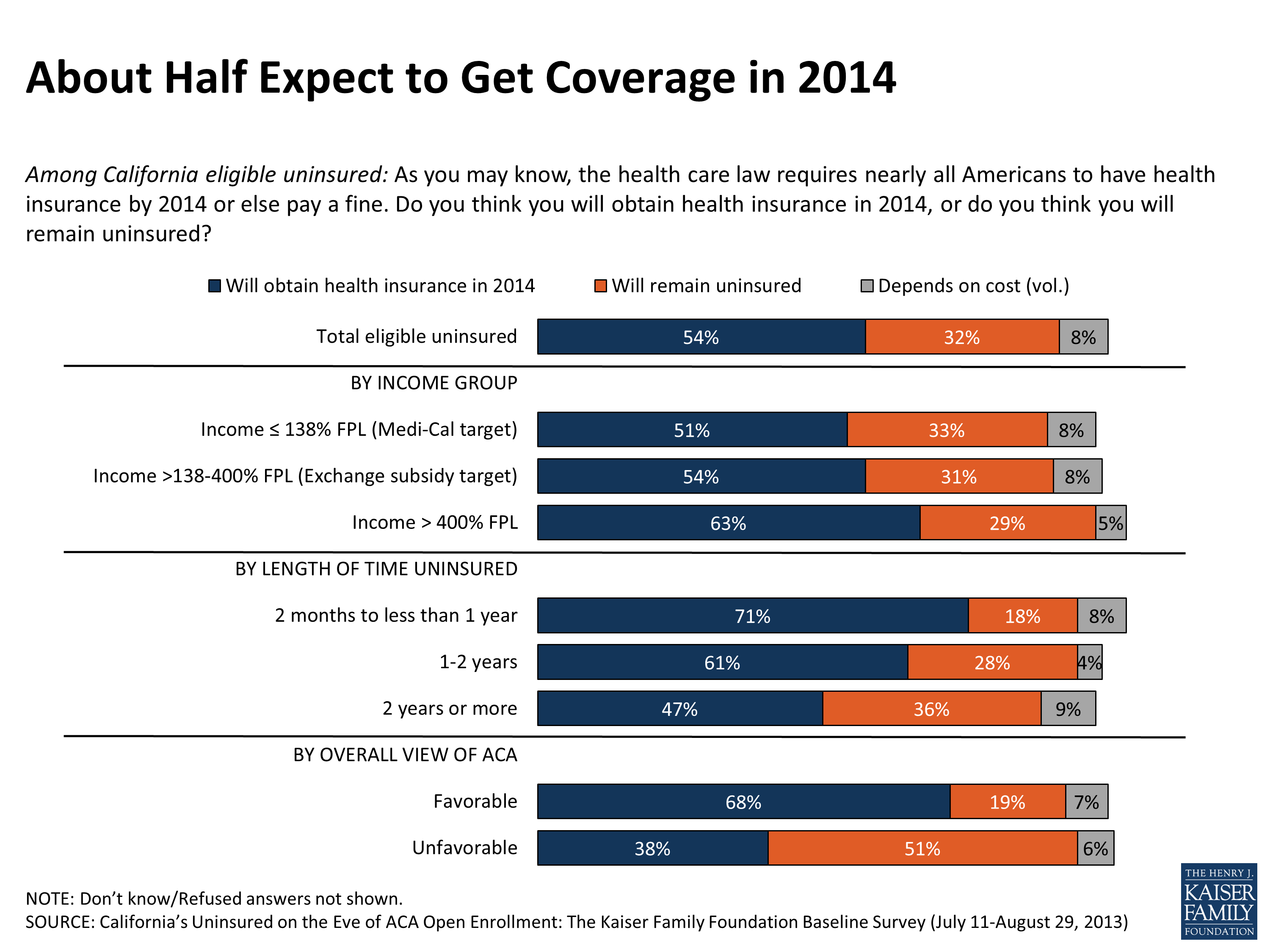

When told or reminded that “nearly all Americans [will be required] to have health insurance by 2014 or else pay a fine,” just over half (54 percent) of the eligible uninsured report they expect to obtain health insurance next year, a third (32 percent) plan to remain uninsured, 8 percent say it would depend on the cost and 7 percent don’t have a sense of how they would react.

Figure 11

The groups most likely to say they expect to get coverage are those that became uninsured only sometime in the past year (71 percent of them are ready to sign back up) and those with favorable views of the ACA (68 percent).

In terms of who is most likely to say they plan to remain uninsured: those with dim views of the health law stand out here, with 51 percent saying they do not intend to seek health insurance. (Even here, however, four in ten do say they will likely seek coverage.) Those who feel their financial situation to be “very insecure” are also disproportionately more likely to say they expect to remain uninsured (43 percent).

Among those who expect to obtain coverage in 2014, most are unsure at this point where that coverage will come from.

| Figure 12: Most Who Expect to Obtain Insurance in 2014 Don’t Know Where They Will Get It | |

| Among California eligible uninsured: Do you think you will obtain health insurance in 2014, or do you think you will remain uninsured? (If expect to obtain coverage: Do you think you will get coverage from Medi-Cal, an employer, the marketplace known as Covered California, or are you not sure where you will get insurance?) | |

| Will obtain insurance (NET) | 54% |

| From an employer | 9 |

| From Medi-Cal | 5 |

| From Covered California | 4 |

| From Medicare (vol.) | 1 |

| Somewhere else (vol.) | 1 |

| Not sure where | 35 |

| Will remain uninsured | 32 |

| Depends on the cost (vol.) | 8 |

| Don’t know | 7 |

What’s driving the views of those that say they don’t plan to get coverage in 2014?

Most (62 percent) of those who say they don’t plan to get insurance explicitly point to cost as a reason, saying they don’t think they will be able to find an affordable plan or that they just don’t have the money to pay for insurance. Smaller shares say the reason they won’t seek coverage is that they don’t need it or don’t want it (21 percent), or that they don’t see how they will qualify for coverage (12 percent).

| Figure 13: Voices of the Uninsured | |

| Among California eligible uninsured who say they will remain uninsured in 2014: Why do you think you will remain uninsured? | |

| Cost related/Don’t think will be able to find an affordable plan – 62% |

“[I’m the] sole caregiver [taking care of my] with Alzheimer’s and head of household, therefore it’s financially restrictive.” “I’d rather [pay] health and dental for my kids instead of myself.” “The company I’m working for might not be able to help me, and if there’s no money I won’t be able to afford insurance.” “If I get a job and remain employed and if they offer benefits [I will get insurance.] If not I will have to feed and take care of my family first before I can buy health insurance.” “The fine will be less than the health insurance and medical bills combined.” |

| Don’t want/need coverage – 21% |

“I’m healthy, I pay cash when I go to the doctor.” “I don’t like being told what to do.” “Because I completely disagree. It is my choice whether or not I want insurance.” |

| Not available to me/won’t qualify – 12% |

“[My] employer has less than 50 people and will not provide health insurance.” “[I’m] falling into a gray area and I don’t fit in any of the categories.” |

| Other |

“Because there is too much of a fight right now, so I don’t think [the ACA] will be implemented.” “I don’t think I will receive good enough health insurance.” |

What do the uninsured have to say about health insurance?

To understand what will happen to California’s millions of uninsured in upcoming months, it’s helpful to understand not just what this population knows and understands about the changes ahead, but how this knowledge may interact with their existing views about health insurance: why they don’t have it, whether they actually want it and for what purpose, and whether they think that up to this point, the value of insurance has been worth its cost.

Most of California’s eligible uninsured have been without coverage for some time; Point to cost of coverage, job loss, and other factors

Two-thirds of those uninsured Californians who self-identify as either U.S. citizens or lawfully present immigrants say they have been uninsured for more than 2 years. About 17 percent have been uninsured for between one and two years, and another 17 percent are more newly uninsured than that. And about one in five say that they’ve never had insurance. The higher-income uninsured are somewhat more likely to report losing their coverage more recently: 48 percent have become uninsured in the past two years, compared to 31 percent in the lowest income bracket.

| Figure 14: Majority of Uninsured Have Been Without Coverage for Two Years or More | ||||

| Among California eligible uninsured: How long have you been uninsured? | Total eligible uninsured | ≤138% FPL (Medi-Cal target) | >138%-400% FPL (exchange subsidy target) | >400% FPL |

| 2 months to less than 1 year | 17% | 14% | 16% | 27% |

| 1 year to less than 2 years | 17 | 17 | 18 | 21 |

| 2 years or more | 66 | 69 | 66 | 53 |

The main reasons they are without health insurance? Cost tops the list, with 47 percent explicitly saying they are uninsured because health coverage is too expensive. One in five refer to job loss or unemployment, and about one in eight (12 percent) point to barriers that stop them from qualifying for coverage through their employer.

Only 3 percent volunteer they don’t have health insurance because they don’t think they need it.

| Figure 15: Voices of the Uninsured | |

| Among California eligible uninsured: What’s the main reason you do not have health insurance? | |

| Too expensive/have little or no money – 47% |

“Because we cannot afford; if health insurance would be more affordable we would try to buy it.” “My job offers it but it is too expensive.” “Because I am self-employed and have insufficient finances to obtain insurance coverage at this time.” |

| Unemployed/lost job – 19% |

“I’m unemployed, and have no money to purchase.”

“I had insurance through my job but not anymore.” |

| Employer doesn’t offer it/Not eligible for employer coverage – 12% |

“My husband’s job doesn’t offer it.” “Just started new job, health insurance won’t be in effect for 30 days.” |

| Not eligible for Medi-Cal or other government insurance program – 5% |

“I am a care giver and they don’t give medical insurance and I applied for Medi-Cal and got disqualified.” |

| Don’t need it – 3% |

“I’m not too sickly in general for the most part, usually if anything just a cold.” |

| Can’t get it/refused due to poor health – 2% |

“I tried to apply to private companies but am turned down every time.” “I became disabled and my job’s coverage did not cover me. They only covered me for 30 days because the company that bought us out won’t cover me because I have not been with the new company a year and because of my condition.” |

| Don’t know how to get it – 2% |

“I don’t have the information needed to apply.” |

This group reports having had a range of types of coverage before becoming uninsured, including employer sponsored insurance (39 percent), Medi-Cal or Medicaid (18 percent) or coverage under a parent’s plan (13 percent). One in ten (9 percent) say that at some point they have been denied health insurance coverage due to someone in their family having a pre-existing condition.

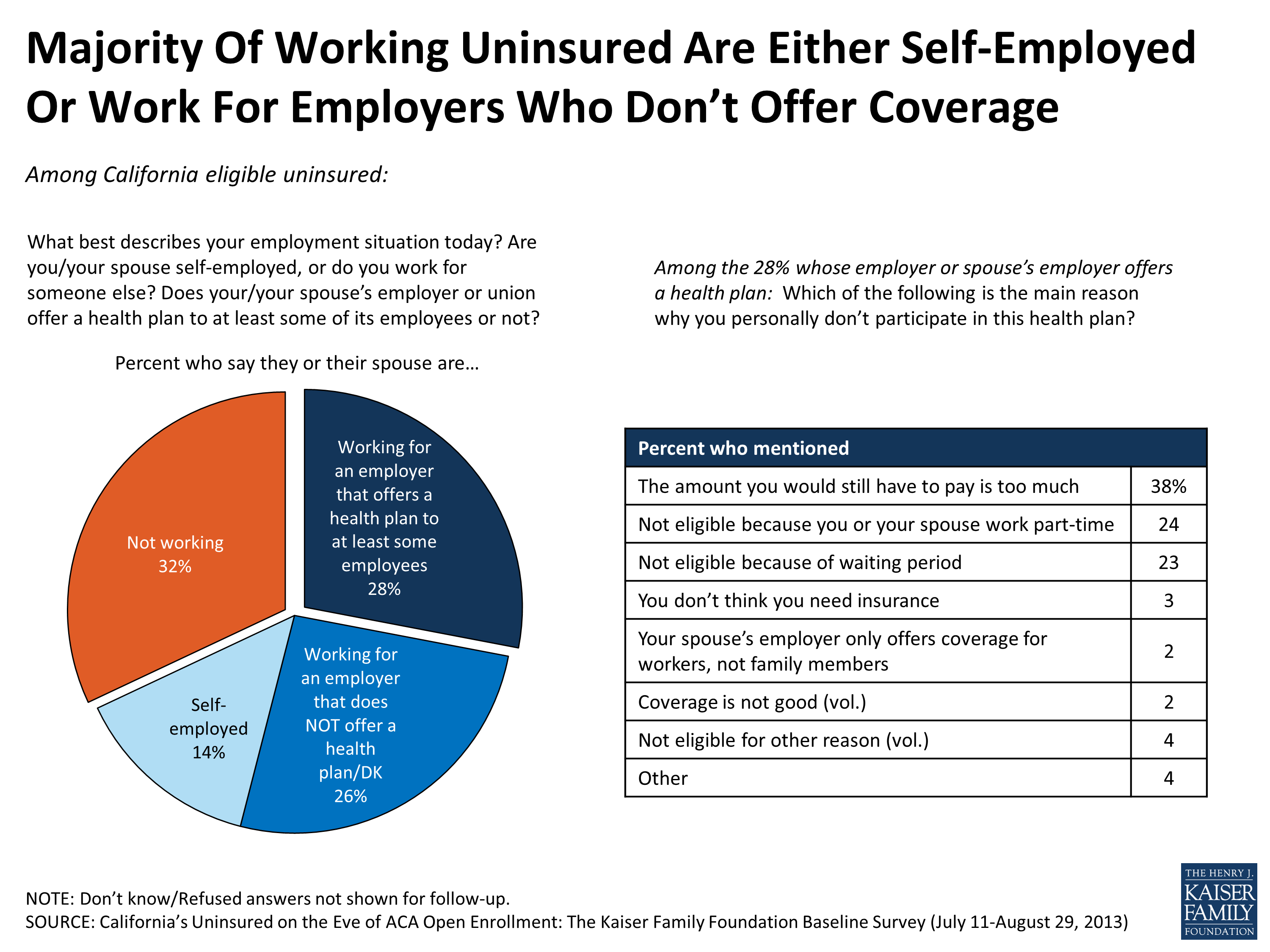

Overall, about two-thirds (68 percent) of California’s eligible uninsured say they or their spouse are working. Why, if so many are employed, are more not insured? For the majority of those who are employed or have a working spouse it’s because they are either self-employed or their employer doesn’t offer coverage. Nearly three in ten (28 percent) of the eligible uninsured do, however, have ties to an employer that offers coverage to at least some of its employees. This group gives a variety of reasons for not participating in such coverage: the most frequently mentioned option is that the cost is too high, but others say they aren’t enrolled because they aren’t eligible, either because they don’t work enough hours or haven’t worked at the firm long enough. It’s worth noting that those that do have access to affordable employer coverage will not be eligible for exchange subsidies.

Figure 16

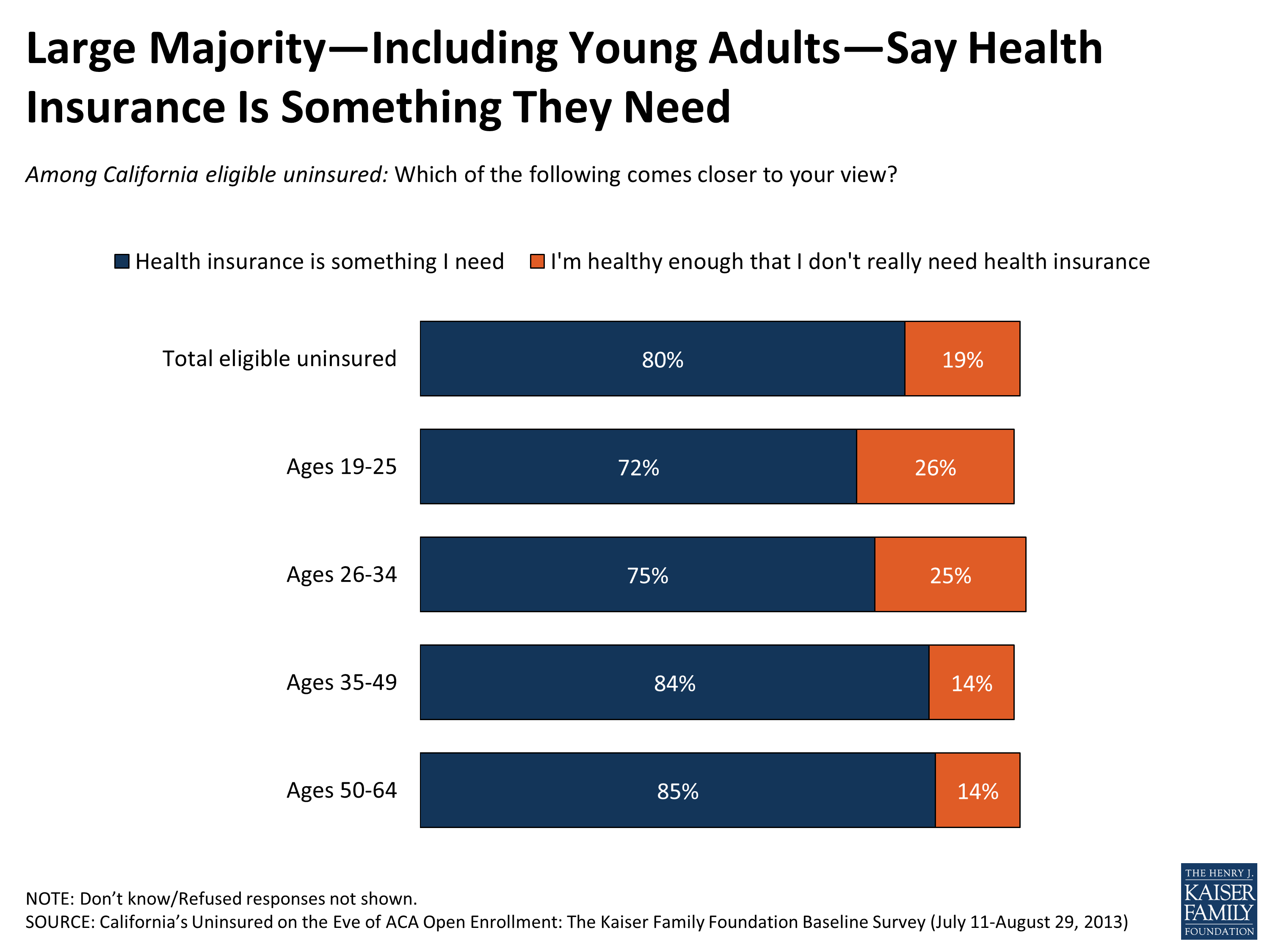

Eight in ten say health insurance is something they need, including large majority of ‘young invincibles’

Though some may presume the reason most of the state’s uninsured lack coverage is because they don’t feel they need it, the survey suggests this isn’t true. According to the survey, the large majority of California’s eligible uninsured – eight in ten – do feel they need health insurance coverage. Even seven in ten (72 percent) of the youngest uninsured Californians – those ages 19 to 25 – say they need health insurance. Overall, just under two in ten instead say they feel healthy enough that they don’t need coverage.

Figure 17

The desire for insurance is even more widespread among those with more health problems. Among those in ‘poor’ or ‘fair’ health, nine in ten feel they need coverage. But even among those who say they are in good health, a majority—three in four—feel they need health coverage.

The main reason uninsured Californians want health coverage: to protect against the kind of financial catastrophe that can accompany a major, unexpected illness or a life-changing accident. Most (seven in ten, including majorities in all age groups), say this is their primary reason to want insurance. For one in four, however, the main point of insurance is to pay for more routine health care expenses. This rises to 40 percent among those who are already grappling with a disability or chronic health problem.

| Figure 18: Those With Chronic Health Conditions More Likely to Say Insurance Is Necessary to Pay for Everyday Health Care Expenses | |||

| Among California eligible uninsured: Which one of the following do you think is the MOST important reason to have health insurance? | Total eligible uninsured | Among those who say they have a disability or chronic condition that keeps them from participating in activities | Among those with no disability/chronic condition |

| To pay for everyday health care expenses, like check-ups and prescriptions | 27% | 40% | 25% |

| To protect against high medical bills in case of severe illness or accident | 71 | 58 | 73 |

Up to this point, a majority have believed that health insurance is worth the cost, though a third disagree

At this point, a majority of the uninsured – 57 percent – do believe that health insurance is worth the money it costs, while just over a third disagree. These views are obviously based on perceptions of the cost of coverage before the opening of the exchange in October.