2013 Employer Health Benefits Survey

Section Eight: High-Deductible Health Plans with Savings Option

Changes in law over the past few years have permitted the establishment of new types of savings arrangements for health care. The two most common are health reimbursement arrangements (HRAs) and health savings accounts (HSAs). HRAs and HSAs are both financial accounts that workers or their family members can use to pay for health care services. These savings arrangements are often (or, in the case of HSAs, always) paired with health plans with high deductibles. The survey treats high-deductible plans that can be paired with a savings option as a distinct plan type – High-Deductible Health Plan with Savings Option (HDHP/SO) – even if the plan would otherwise be considered a PPO, HMO, POS plan, or conventional health plan. Specifically for the survey, HDHP/SOs are defined as (1) health plans with a deductible of at least $1,000 for single coverage and $2,000 for family coverage1 offered with an HRA (referred to as HDHP/HRAs); or (2) high-deductible health plans that meet the federal legal requirements to permit an enrollee to establish and contribute to an HSA (referred to as HSA-qualified HDHPs).2

Percentage of Firms Offering HDHP/HRAs and HSA-Qualified HDHPs, and Enrollment

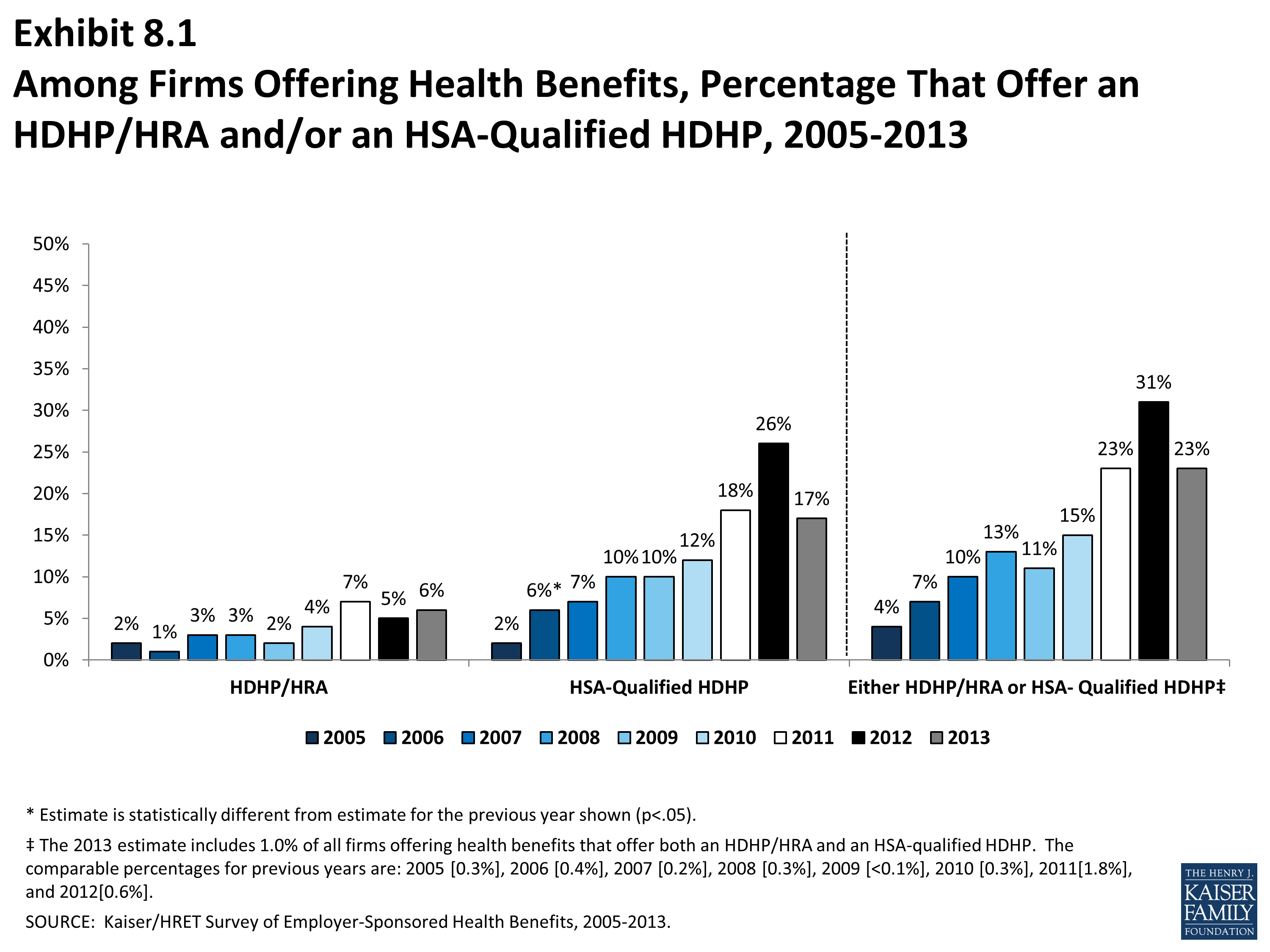

- Twenty-three percent of firms offering health benefits offer an HDHP/HRA or an HSA-qualified HDHP. Among firms offering health benefits, 6% offer an HDHP/HRA and 17% offer an HSA-qualified HDHP (Exhibit 8.1).

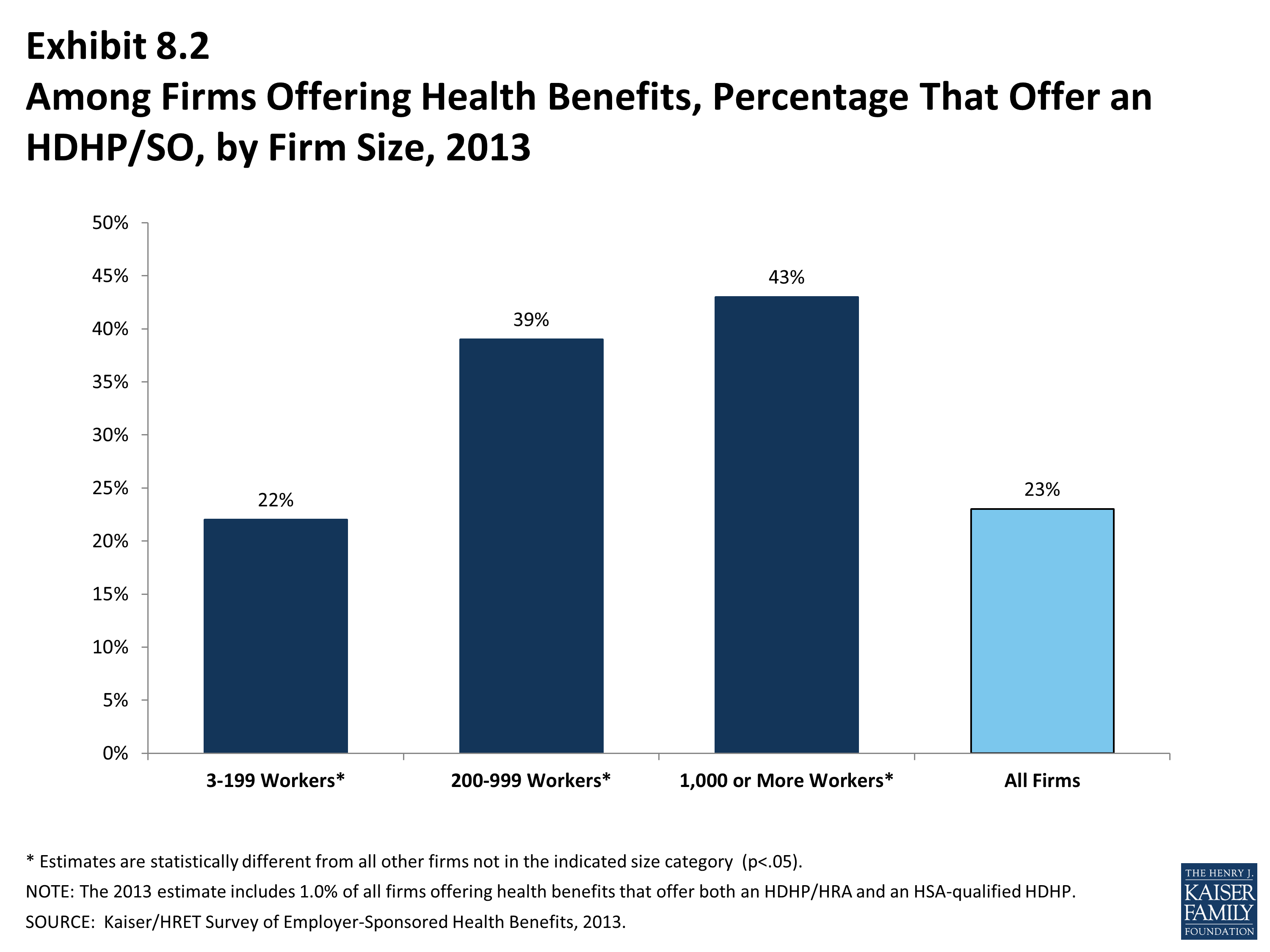

- Firms with 5,000 or more workers are significantly more likely to offer an HDHP/SO than smaller firms. Forty-three percent of firms with 1,000 or more workers offer an HDHP/SO, compared to 22% of firms with 3 to 199 workers, 39% of firms with 200-999 workers (Exhibit 8.2).

Health Reimbursement Arrangements (HRAs) are medical care reimbursement plans established by employers that can be used by employees to pay for health care. HRAs are funded solely by employers. Employers typically commit to make a specified amount of money available in the HRA for premiums and medical expenses incurred by employees or their dependents. HRAs are accounting devices, and employers are not required to expend funds until an employee incurs expenses that would be covered by the HRA. Unspent funds in the HRA usually can be carried over to the next year (sometimes with a limit). Employees cannot take their HRA balances with them if they leave their job, although an employer can choose to make the remaining balance available to former employees to pay for health care.

HRAs often are offered along with a high-deductible health plan (HDHP). In such cases, the employee pays for health care first from his or her HRA and then out-of-pocket until the health plan deductible is met. Sometimes certain preventive services or other services such as prescription drugs are paid for by the plan before the employee meets the deductible.

Health Savings Accounts (HSAs) are savings accounts created by individuals to pay for health care. An individual may establish an HSA if he or she is covered by a “qualified health plan” which is a plan with a high deductible (i.e., a deductible of at least $1,250 for single coverage and $2,500 for family coverage in 2013) that also meets other requirements.[1] Employers can encourage their employees to create HSAs by offering an HDHP that meets the federal requirements. Employers in some cases also may assist their employees by identifying HSA options, facilitating applications, or negotiating favorable fees from HSA vendors.

Both employers and employees can contribute to an HSA, up to the statutory cap of $3,250 for single coverage and $6,450 for family coverage in 2013. Employee contributions to the HSA are made on a pre-income tax basis, and some employers arrange for their employees to fund their HSAs through payroll deductions. Employers are not required to contribute to HSAs established by their employees but, if they elect to do so, their contributions are not taxable to the employee. Interest and other earnings on amounts in an HSA are not taxable. Withdrawals from the HSA by the account owner to pay for qualified health care expenses are not taxed. The savings account is owned by the individual who creates the account, so employees retain their HSA balances if they leave their job.

1 See U.S. Department of the Treasury, Health Savings Accounts, available at http://www.irs.gov/pub/irs-drop/rp-12-26.pdf

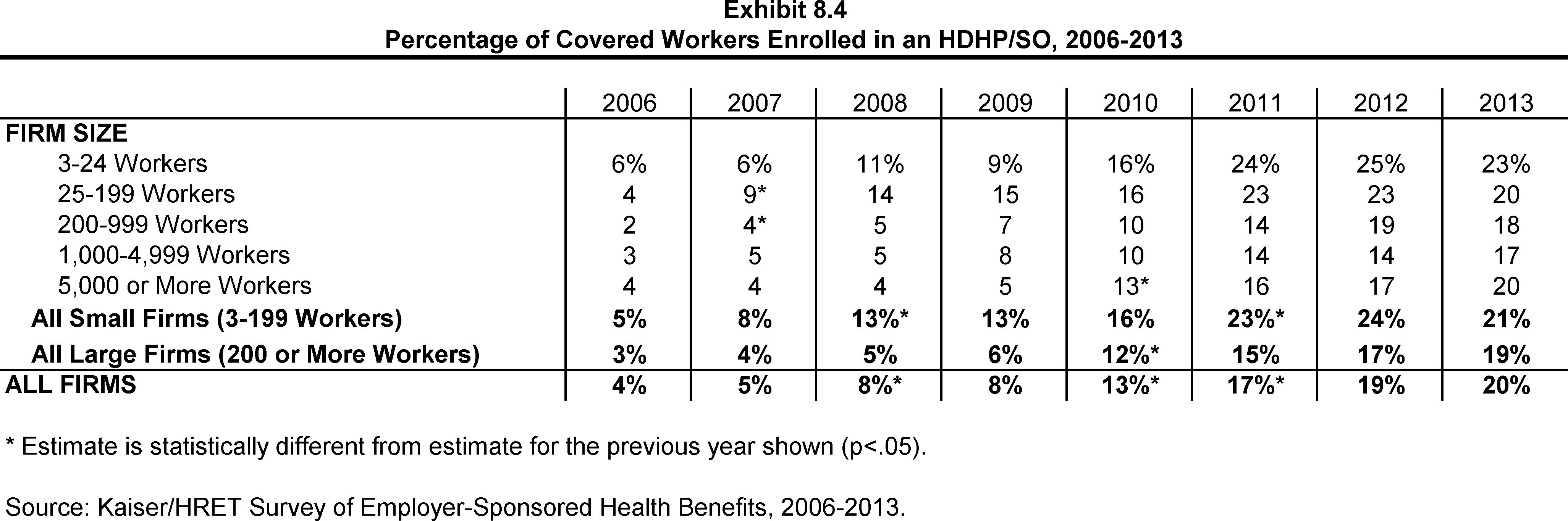

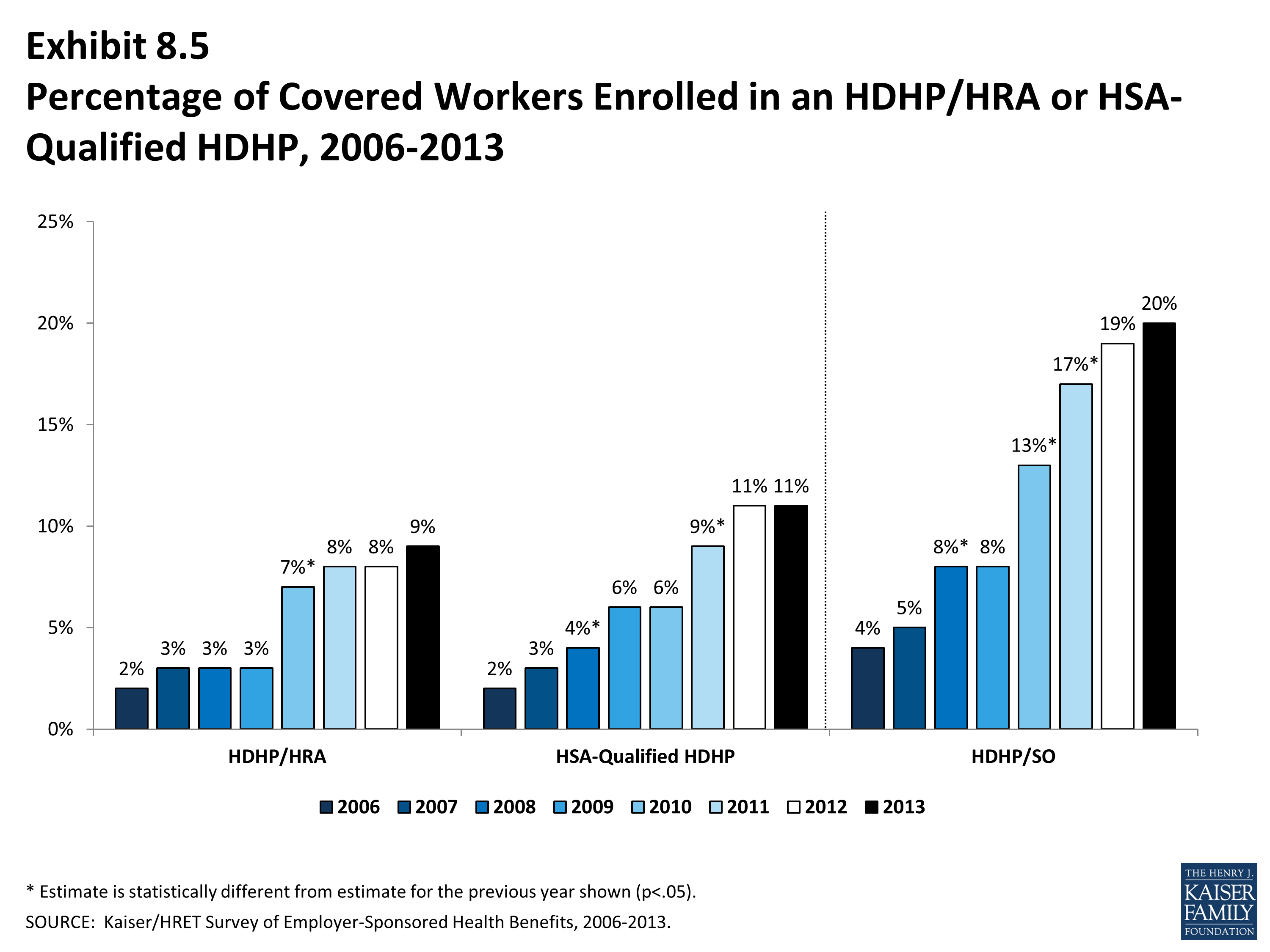

- Twenty percent of covered workers are enrolled in an HDHP/SO in 2013, similar to the 19% enrolled last year (Exhibit 8.5). Enrollment in HDHP/SOs had increased significantly in previous years (17% in 2011; 13% in 2010; 8% in 2009).

- Nine percent of covered workers are enrolled in HDHP/HRAs in 2013, and 11% percent of covered workers are enrolled in HSA-qualified HDHPs (Exhibit 8.5).

Plan Deductibles

- As expected, workers enrolled in HDHP/SOs have higher deductibles than workers enrolled in HMOs, PPOs, or POS plans.

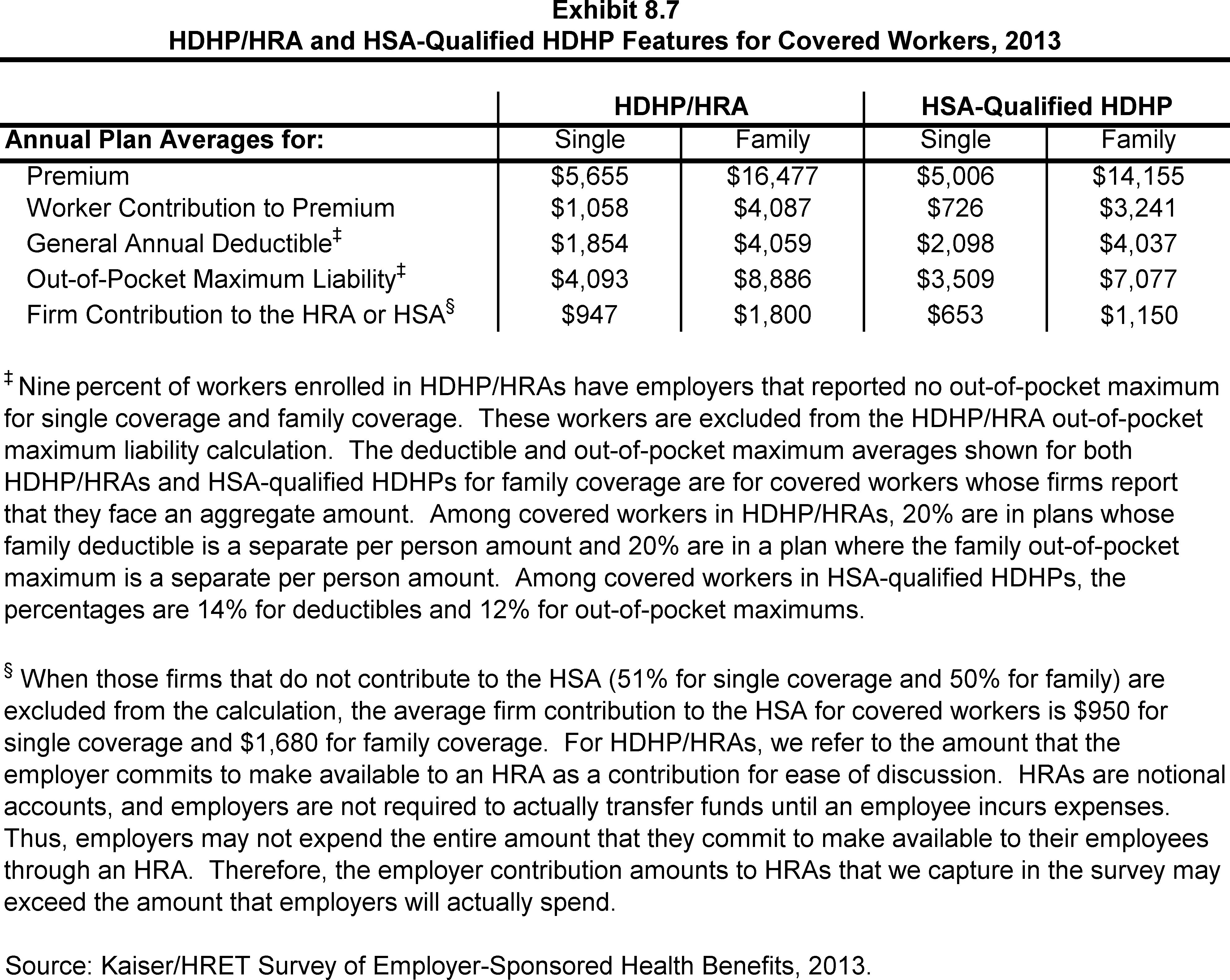

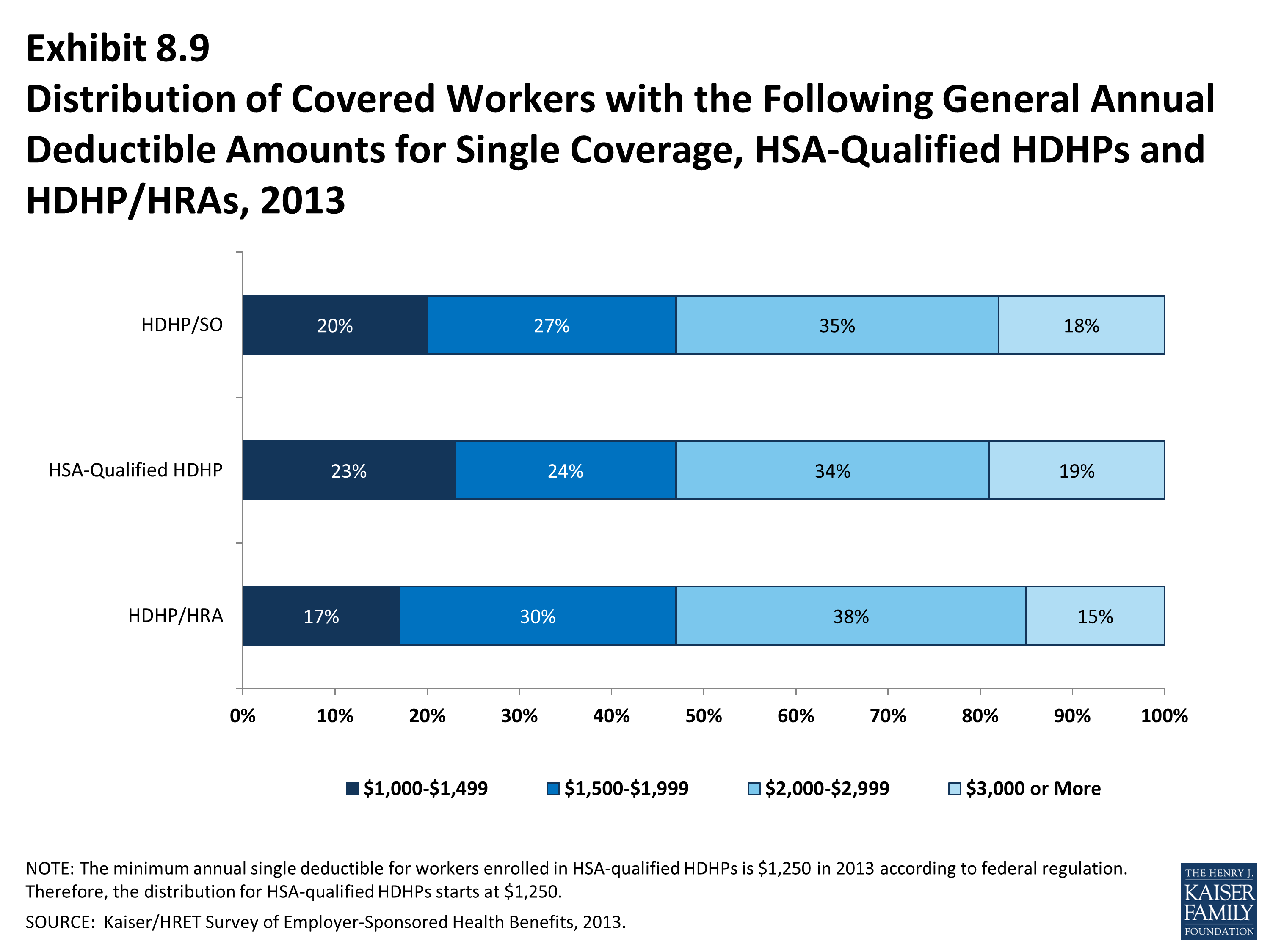

- The average general annual deductible for single coverage is $1,854 for HDHP/HRAs and $2,098 for HSA-qualified HDHPs (Exhibit 8.7). These averages are similar to the amounts reported in recent years. There is wide variation around these averages (Exhibit 8.9). Eighteen percent of covered workers are enrolled in a HDHP/SO with a deductible of $3,000 or more.

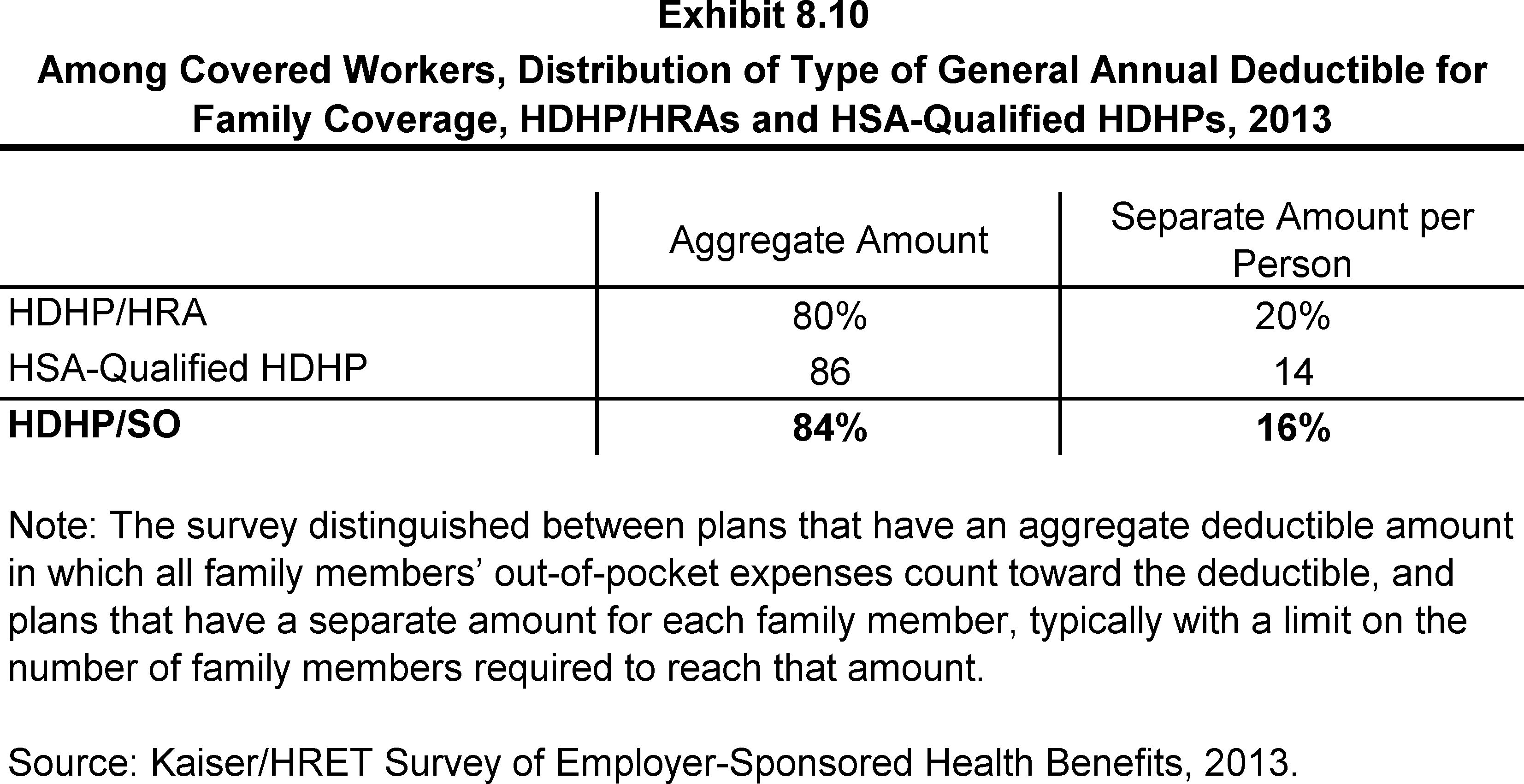

- Since 2006, the survey has collected information on two types of family deductibles. The survey asks employers whether the family deductible amount is (1) an aggregate amount (i.e., the out-of-pocket expenses of all family members are counted until the deductible is satisfied), or (2) a per-person amount that applies to each family member (typically with a limit on the number of family members that would be required to meet the deductible amount).

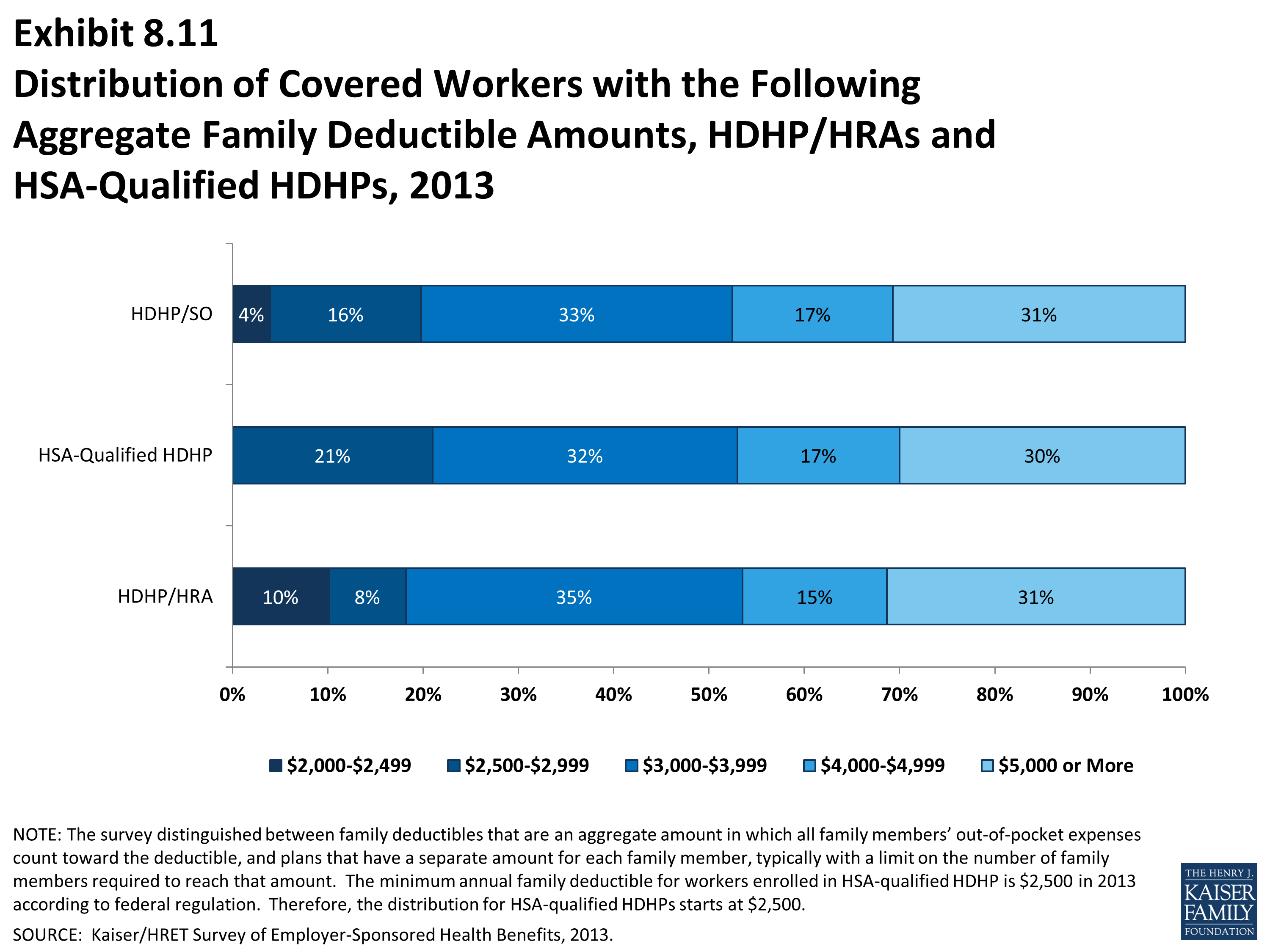

- The average aggregate deductibles for workers with family coverage are $4,059 for HDHP/HRAs and $4,037 for HSA-qualified HDHPs (Exhibit 8.7). There is wide variation around these average amounts for family coverage (Exhibit 8.1). Almost a third of covered workers enrolled in HDHP/So plans have an aggregate family deductible of $5,000 dollars or more.

Out-of-Pocket Maximum Amounts

- HSA-qualified HDHPs are legally required to have a maximum annual out-of-pocket liability of no more than $6,250 for single coverage and $12,500 for family coverage in 2013. HDHP/HRAs have no similar requirement.

- The average annual out-of-pocket maximum for single coverage is $4,093 for HDHP/HRAs3 and $3,509 for HSA-qualified HDHPs (Exhibit 8.7).

- As with deductibles, the survey asks employers whether the family out-of-pocket maximum liability is (1) an aggregate amount that applies to spending by any covered person in the family, or (2) a separate per person amount that applies to spending by each family member or a limited number of family members. The survey also asks whether spending by enrollees on various services counts towards meeting the plan out-of-pocket maximum.

- Among covered workers with family coverage whose out-of-pocket maximum is an aggregate amount that applies to spending by any covered person in the family, the average annual out-of-pocket maximums are $8,886 for HDHP/HRAs and $7,077 for HSA-qualified HDHPs (Exhibit 8.7).

Premiums

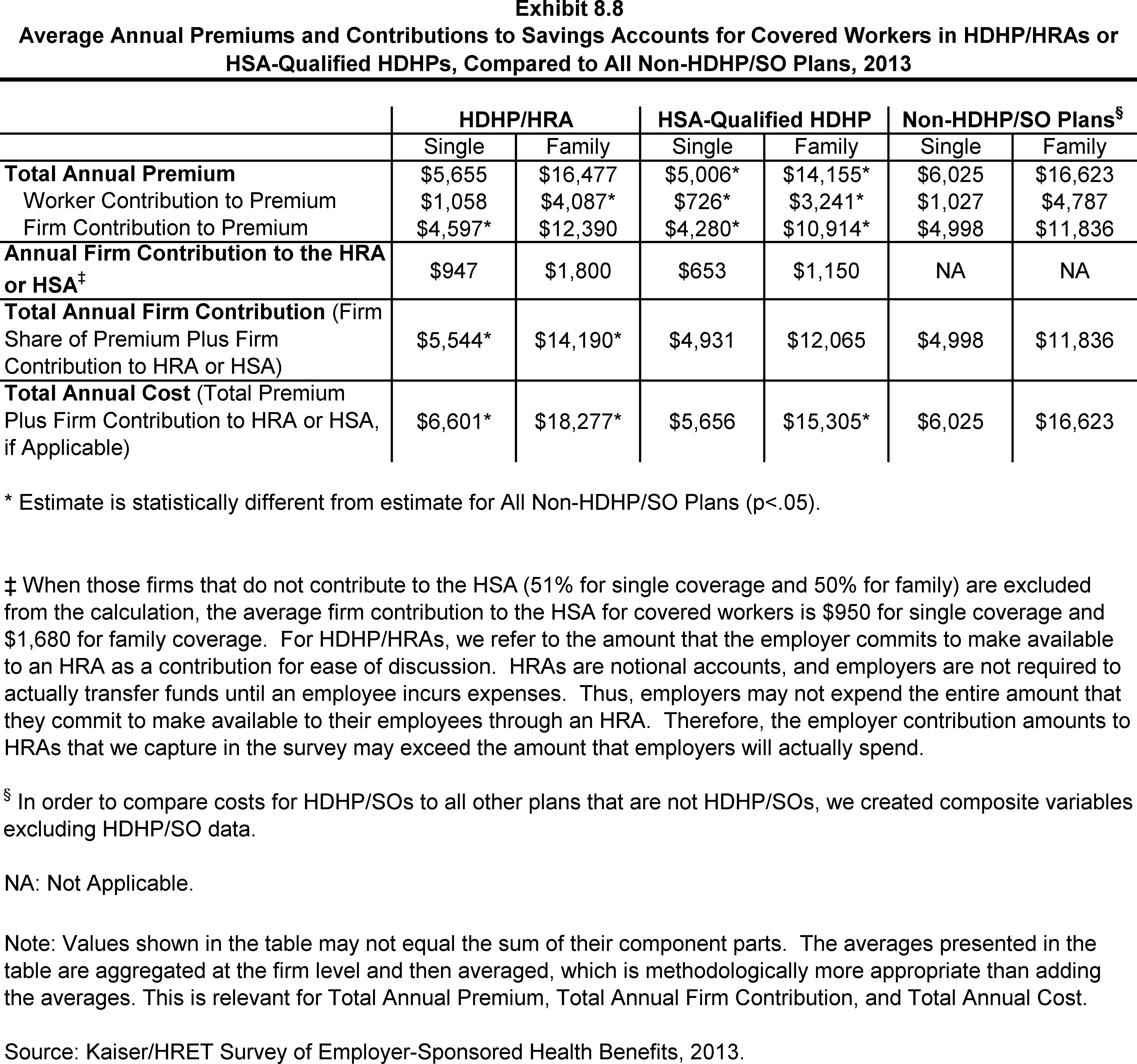

- In 2013, the average annual premiums for HDHP/HRAs are $5,655 for single coverage and $16,477 for family coverage (Exhibit 8.8).

- The average annual premium for workers in HSA-qualified HDHPs is $5,006 for single coverage and $14,155 for family coverage. These amounts are lower than the average single and family premium for workers in plans that are not HDHP/SOs (Exhibit 8.7).

Worker Contributions to Premiums

- The average annual worker contributions to premiums for workers enrolled in HDHP/HRAs are $1,058 for single coverage and $4,087 for family coverage (Exhibit 8.8).

- The average annual worker contributions to premiums for workers in HSA-qualified HDHPs are $726 for single coverage and $3,241 for family coverage (Exhibit 8.8). The average contribution for single coverage for workers in HSA-qualified HDHPs is significantly less than the average premium contribution made by covered workers in plans that are not HDHP/SOs (Exhibit 8.7).

Employer Contributions to Premiums and Savings Options

- Employers contribute to HDHP/SOs in two ways: through their contributions toward the premium for the health plan and through their contributions (if any, in the case of HSAs) to the savings account option (i.e., the HRAs or HSAs themselves).

- Looking just at the annual employer contributions to premiums, covered workers in HDHP/HRAs on average receive employer contributions of $4,597 for single coverage and $12,390 for family coverage. The average employer contribution for single coverage in HDHP/HRAs is significantly less than the average employer premium contribution for plans that are not HDHP/SOs (Exhibit 8.8).

- The average annual employer contributions to premiums for workers in HSA-qualified HDHPs are $4,280 for single coverage and $10,914 for family coverage. These amounts are lower than the average contributions for single or family coverage for workers in plans that are not HDHP/SOs (Exhibit 8.8).

- When looking at employer contributions to the savings option, workers enrolled in HDHP/HRAs receive, on average, an annual employer contribution to their HRA of $947 for single coverage and $1,800 for family coverage (Exhibit 8.8).

- HRAs are generally structured in such a way that employers may not actually spend the whole amount that they make available to their employees’ HRAs.4 Amounts committed to an employee’s HRA that are not used by the employee generally roll over and can be used in future years, but any balance may revert back to the employer if the employee leaves his or her job. Thus, the employer contribution amounts to HRAs that we capture in the survey may exceed the amount that employers will actually spend.

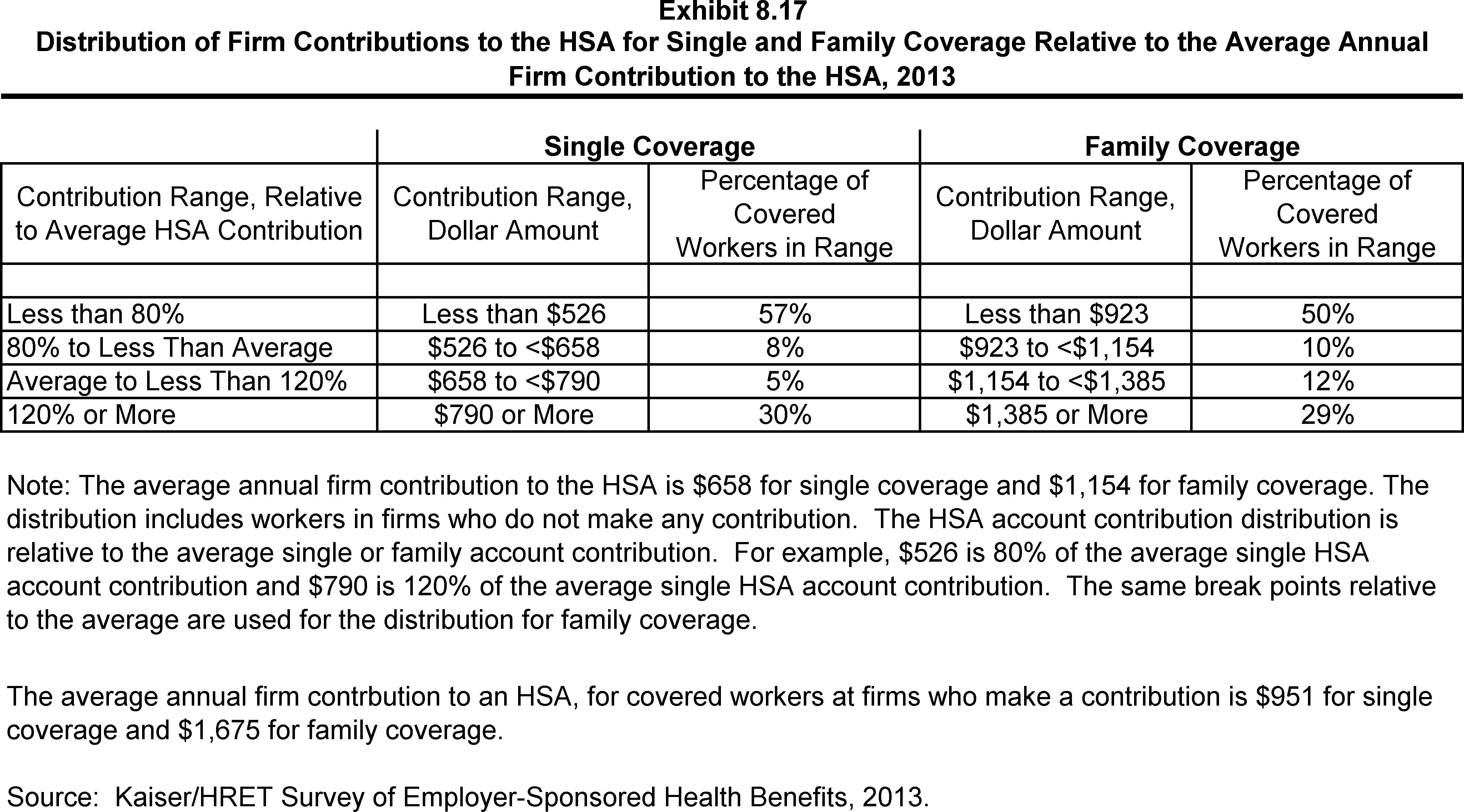

- Workers enrolled in HSA-qualified HDHPs on average receive an annual employer contribution to their HSA of $653 for single coverage and $1,150 for family coverage (Exhibit 8.8).

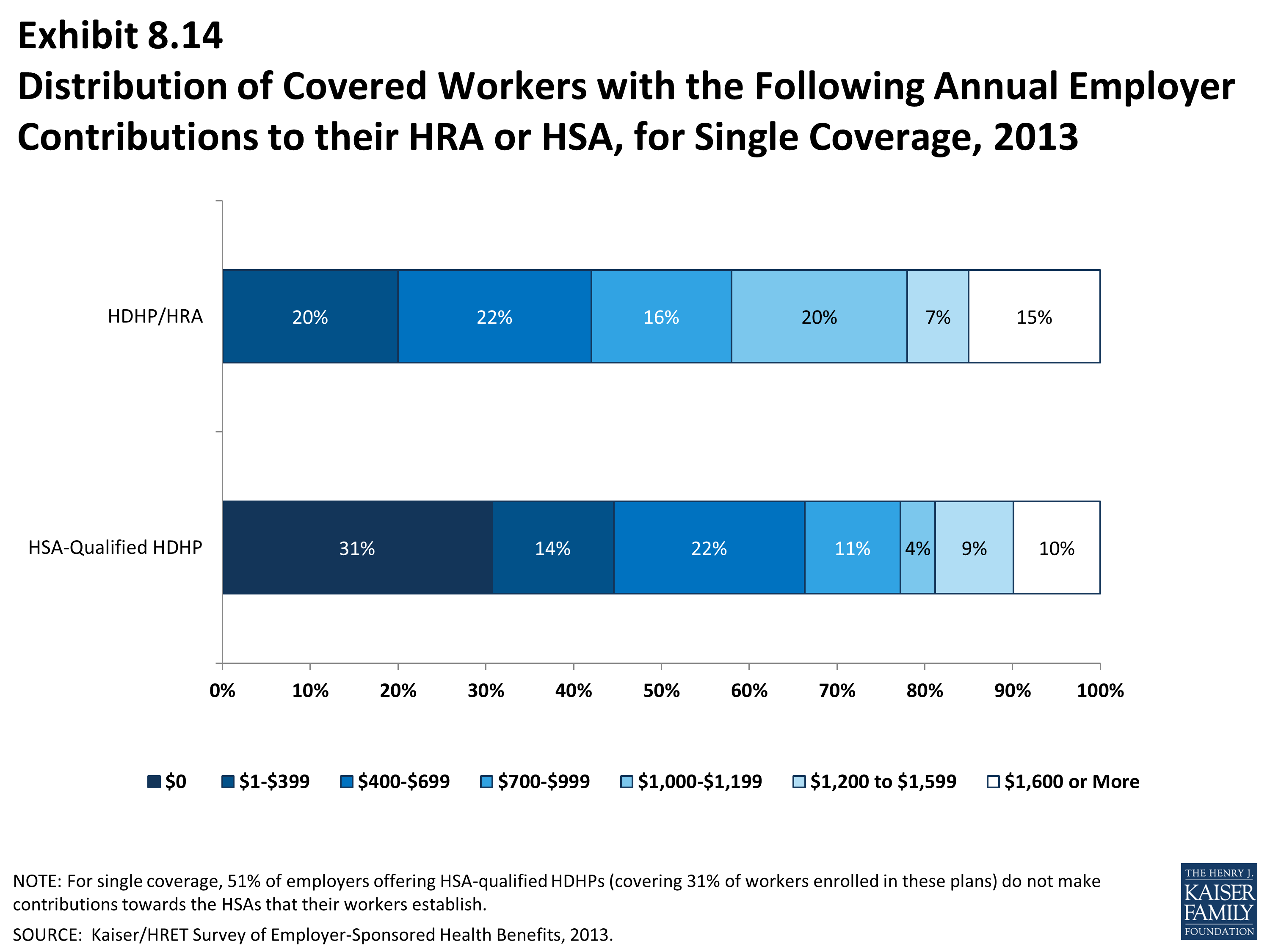

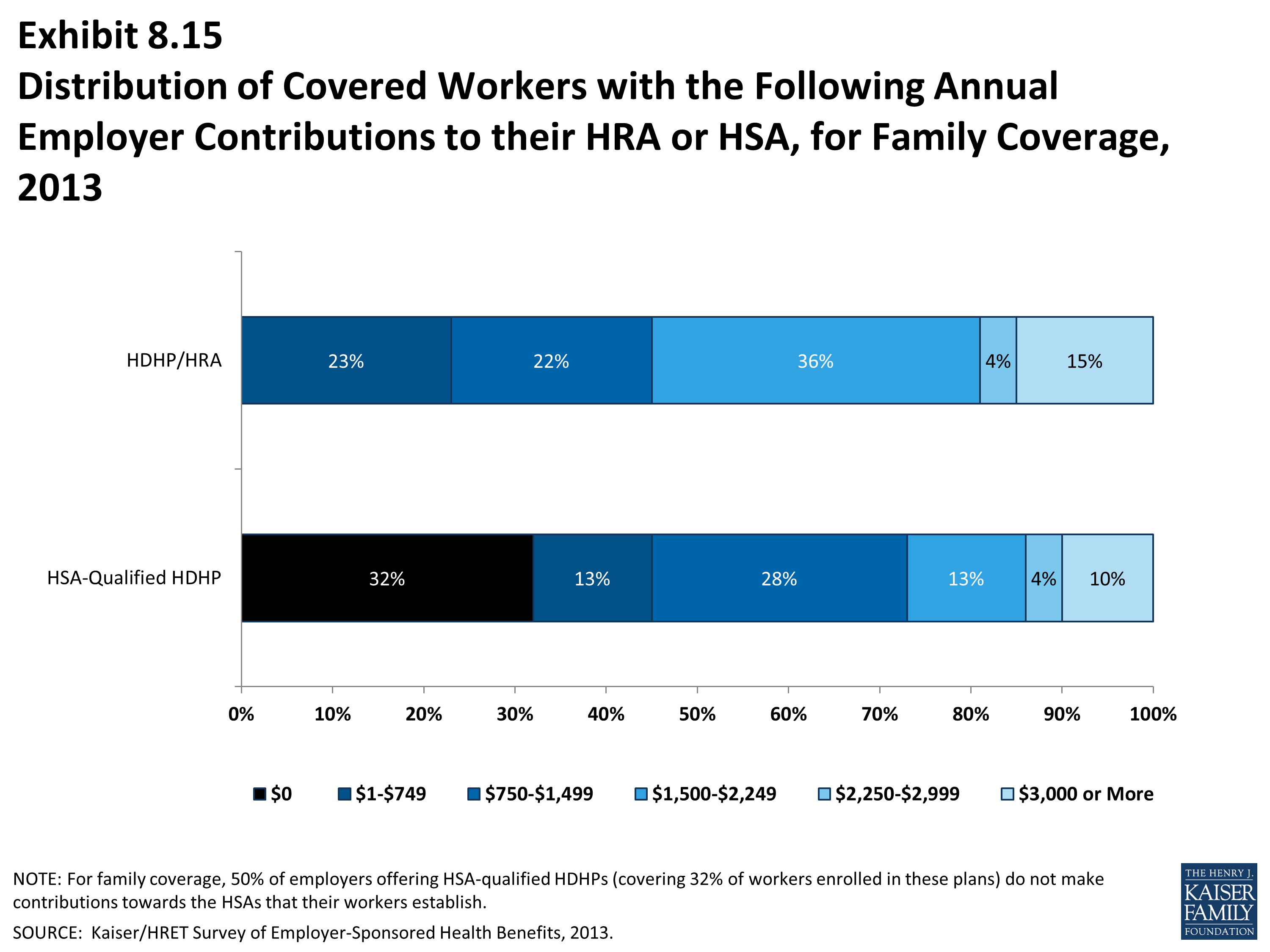

- In some cases, employers that sponsor HSA-qualified HDHP/SOs do not make contributions to HSAs established by their employees. Fifty-one percent of employers offering single coverage and fifty percent offering family coverage through HSA-qualified HDHPs do not make contributions towards the HSAs that their workers establish (Exhibit 8.8). Thirty-one percent of workers with single coverage and thirty-two percent of workers with family coverage in an HSA-qualified HDHP do not receive an account contribution from their employer (Exhibit 8.14) and (Exhibit 8.15).

- The percent of covered workers enrolled in a plan where the employer makes no HSA contribution for single coverage is similar to 34% last year and 26% five years ago.

- The average HSA contributions reported above include the portion of covered workers whose employer contribution to the HSA is zero. When those firms that do not contribute to the HSA are excluded from the calculation, the average employer contribution for covered workers is $950 for single coverage and $1,680 for family coverage (Exhibit 8.7).

- Employer contributions to savings account options (i.e., the HRAs and HSAs themselves) for their employees can be added to their health plan premium contributions to calculate total employer contributions toward HDHP/SOs.

- For HDHP/HRAs, the average annual total employer contribution for covered workers is $5,544 for single coverage and $14,190 for family coverage. The average total employer contribution amounts for single and family coverage in HDHP/HRAs are higher than the average amount that employers contribute towards single and family coverage in health plans that are not HDHP/SOs (Exhibit 8.8).

- For HSA-qualified HDHPs, the average annual total employer contribution for covered workers is $4,931 for single coverage and $12,065 for workers with family coverage. The total amounts contributed for workers in HSA-qualified HDHPs for single and family coverage are similar to the amounts contributed for workers not in HDHP/SOs (Exhibit 8.8).

Among Firms Offering Health Benefits, Percentage That Offer an HDHP/HRA and/or an HSA-Qualified HDHP, 2005-2013

Among Firms Offering Health Benefits, Percentage That Offer an HDHP/SO, by Firm Size, 2013

Among Firms Offering Health Benefits, Percentage That Offer an HDHP/SO, by Firm Size, 2005-2013

Percentage of Covered Workers Enrolled in an HDHP/SO, 2006-2013

Percentage of Covered Workers Enrolled in an HDHP/HRA or HSA-Qualified HDHP, 2006-2013

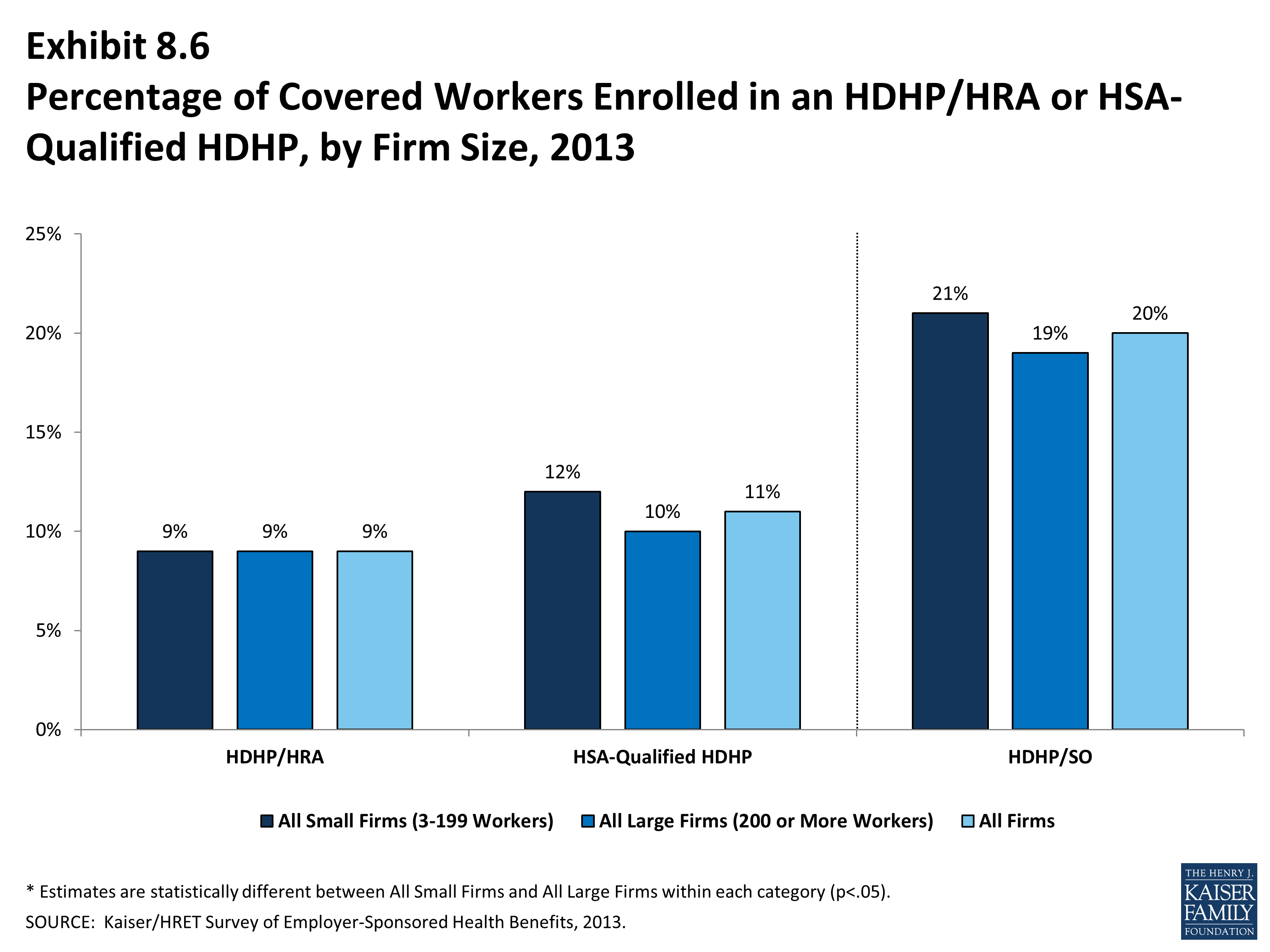

Percentage of Covered Workers Enrolled in an HDHP/HRA or HSA-Qualified HDHP, by Firm Size, 2013

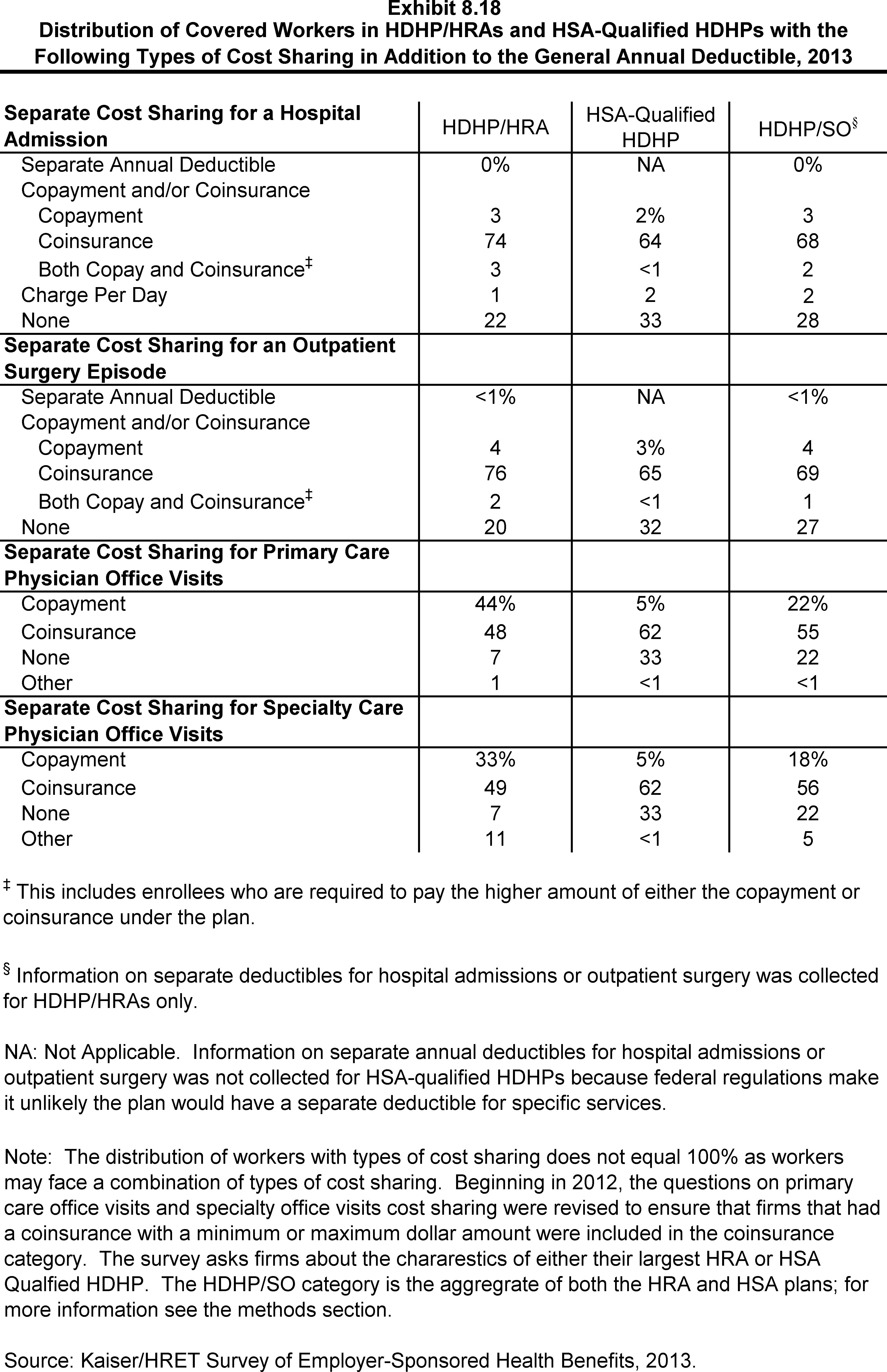

HDHP/HRA and HSA-Qualified HDHP Features for Covered Workers, 2013

Average Annual Premiums and Contributions to Savings Accounts for Covered Workers in HDHP/HRAs or HSA-Qualified HDHPs, Compared to All Non-HDHP/SO Plans, 2013

Distribution of Covered Workers with the Following General Annual Deductible Amounts for Single Coverage, HSA-Qualified HDHPs and HDHP/HRAs, 2013

Among Covered Workers, Distribution of Type of General Annual Deductible for Family Coverage, HDHP/HRAs and HSA-Qualified HDHPs, 2013

Distribution of Covered Workers with the Following Aggregate Family Deductible Amounts, HDHP/HRAs and HSA-Qualified HDHPs, 2013

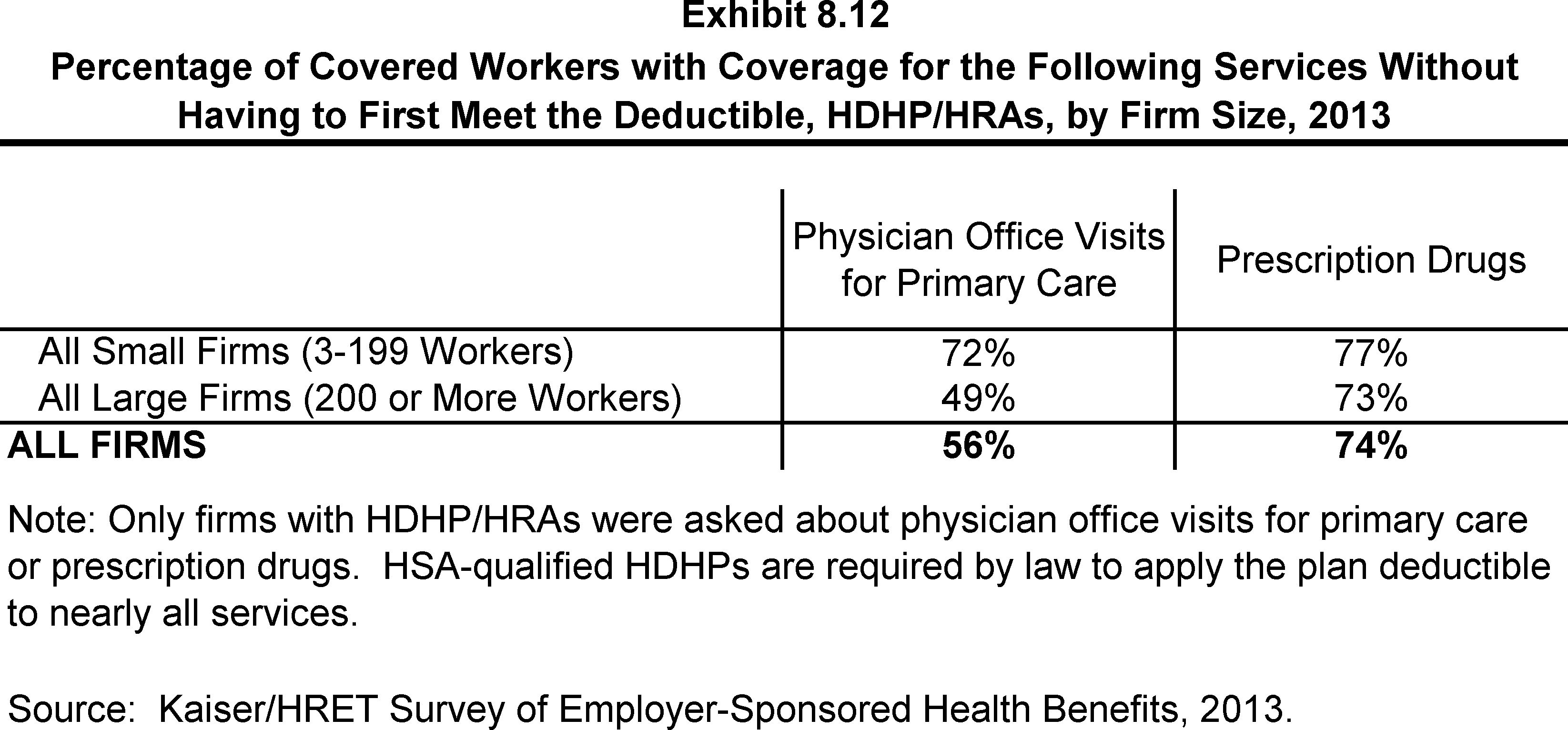

Percentage of Covered Workers with Coverage for the Following Services Without Having to First Meet the Deductible, HDHP/HRAs, by Firm Size, 2013

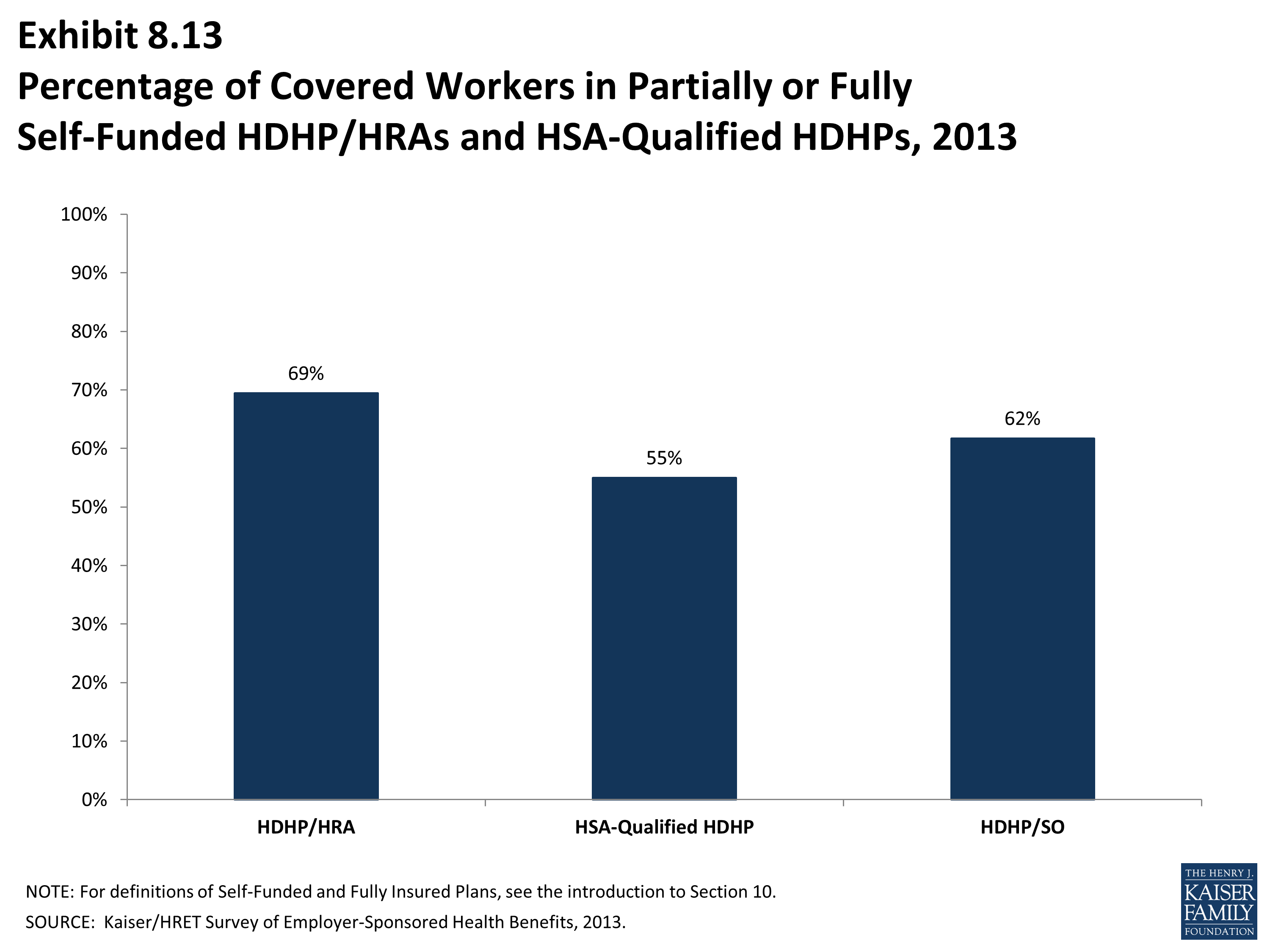

Percentage of Covered Workers in Partially or Fully Self-Funded HDHP/HRAs and HSA-Qualified HDHPs, 2013

Distribution of Covered Workers with the Following Annual Employer Contributions to their HRA or HSA, for Single Coverage, 2013

Distribution of Covered Workers with the Following Annual Employer Contributions to their HRA or HSA, for Family Coverage, 2013

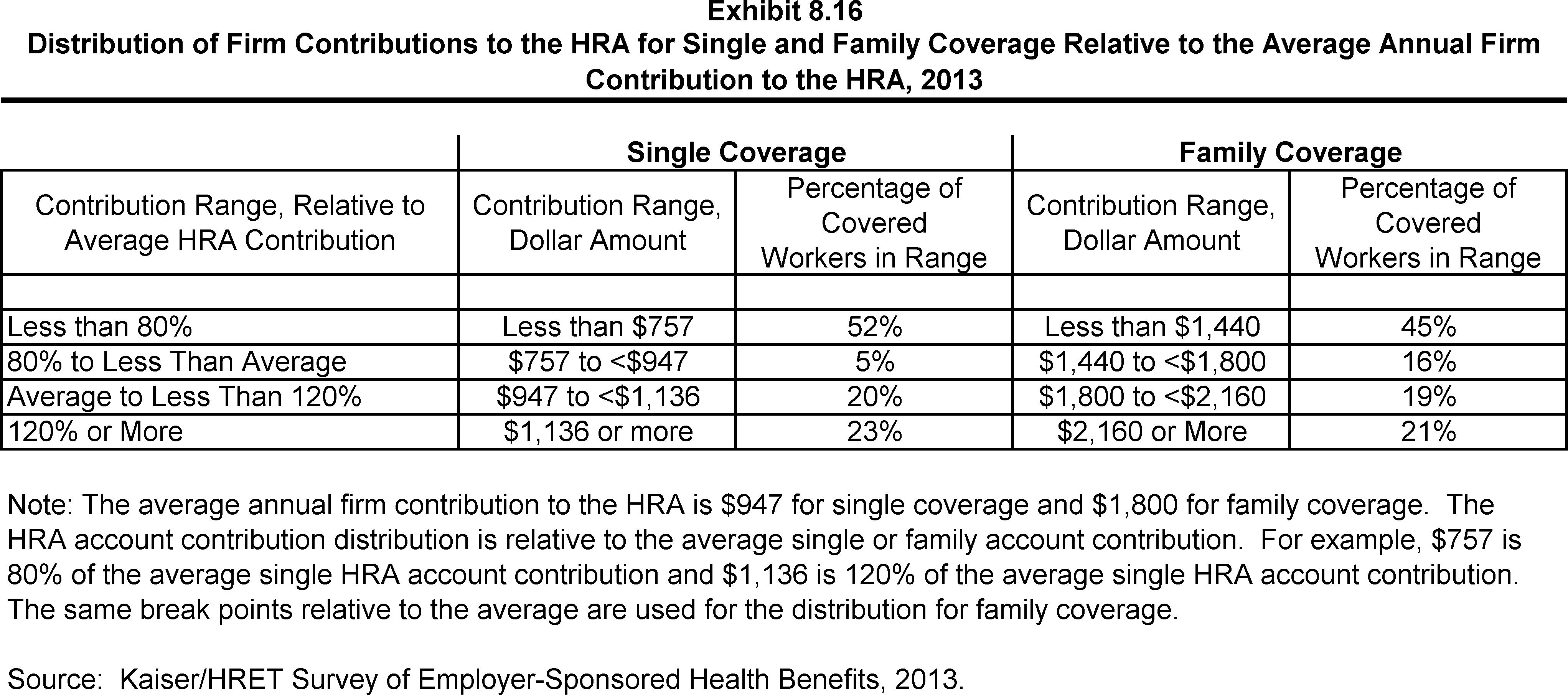

Distribution of Firm Contributions to the HRA for Single and Family Coverage Relative to the Average Annual Firm Contribution to the HRA, 2013

Distribution of Firm Contributions to the HSA for Single and Family Coverage Relative to the Average Annual Firm Contribution to the HSA, 2013