2012 Employer Health Benefits Survey

Section 10: Plan Funding

Federal law (the Employee Retirement Income Security Act of 1974, or ERISA) exempts self-funded plans from state insurance laws, including reserve requirements, mandated benefits, premium taxes, and consumer protection regulations. Three in five covered workers are in a self-funded health plan. Self-funding is common among larger firms because they can spread the risk of costly claims over a large number of employees and dependents. Many self-funded plans use insurance, often called stoploss coverage, to limit the plan sponsors liability for very large claims. Almost three in five covered workers in self-funded plans are in plans with stoploss protection.

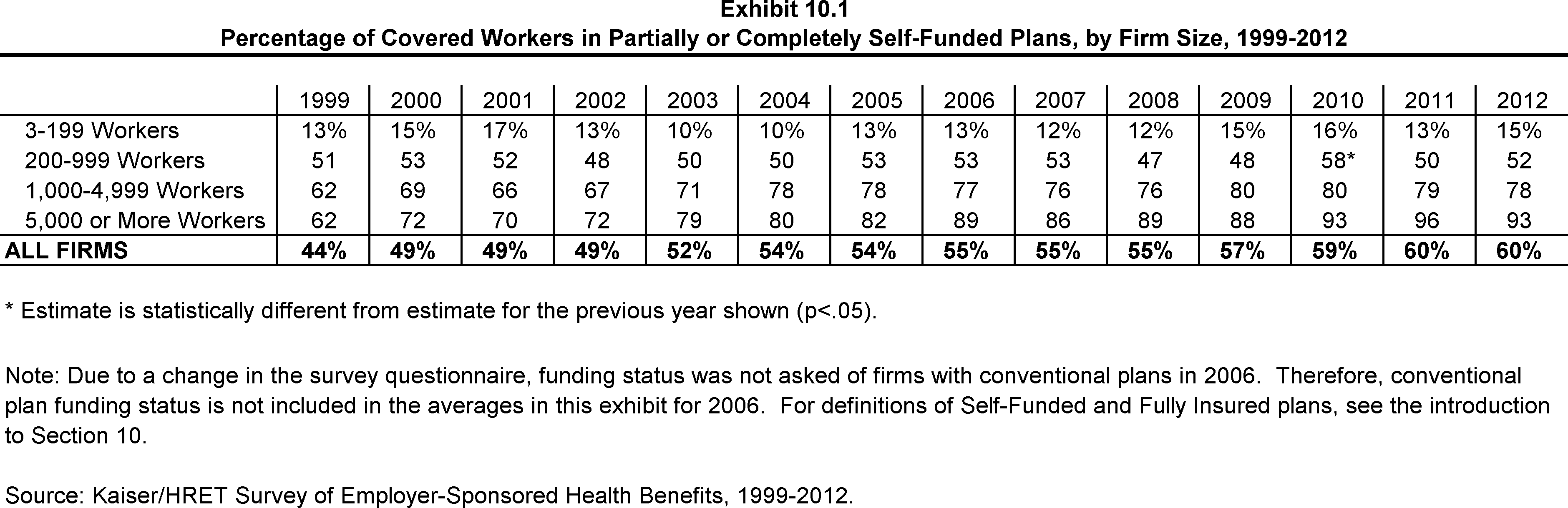

- Sixty percent of covered workers are in a self-funded plan, the same percentage reported in 2011 (Exhibit 10.1). The percentage of covered workers who are in a plan that is completely or partially self-funded has increased over time from 49% in 2000 and 54% in 2005.

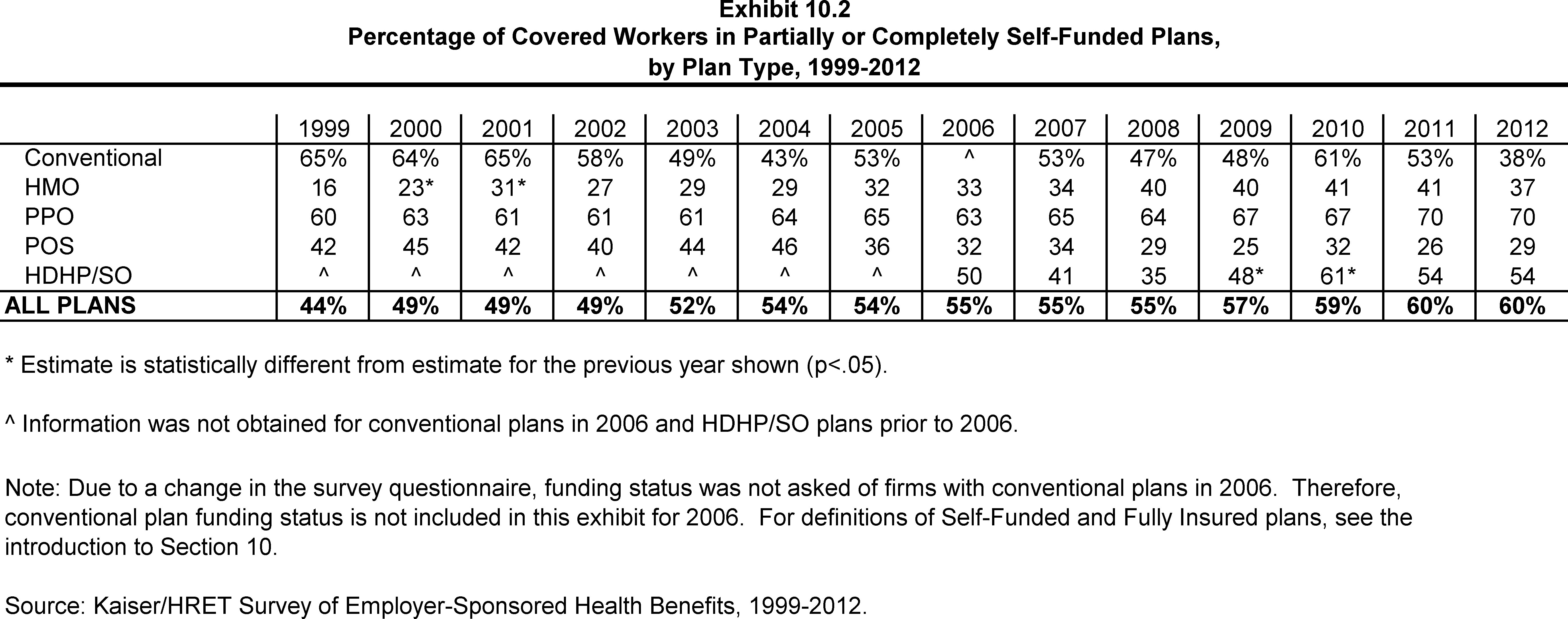

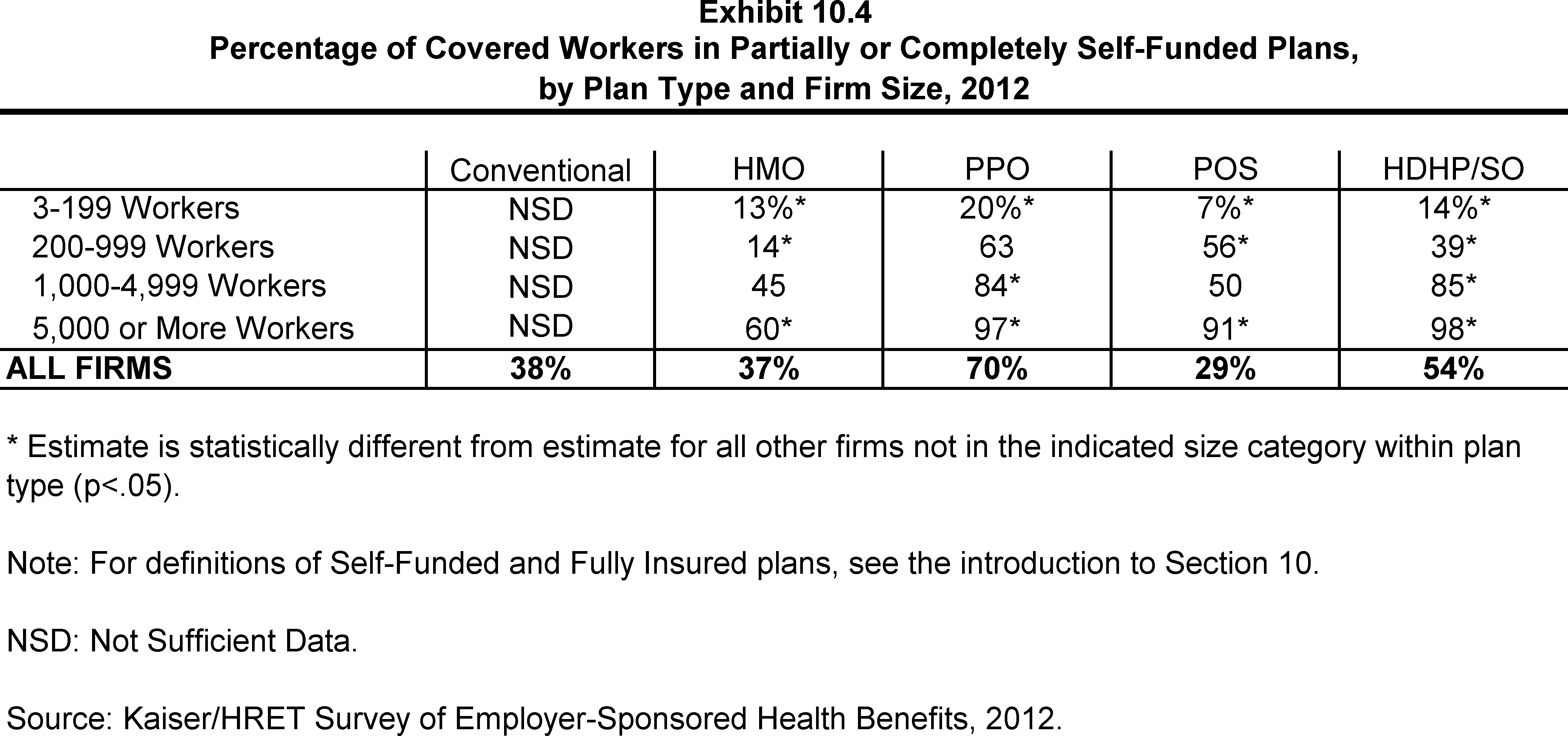

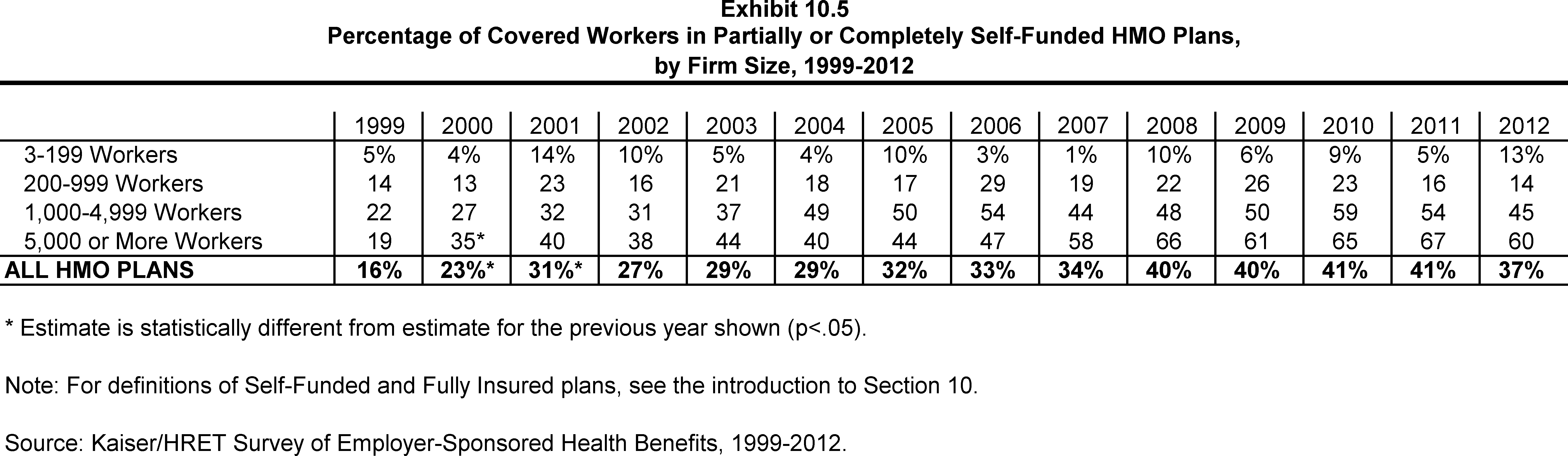

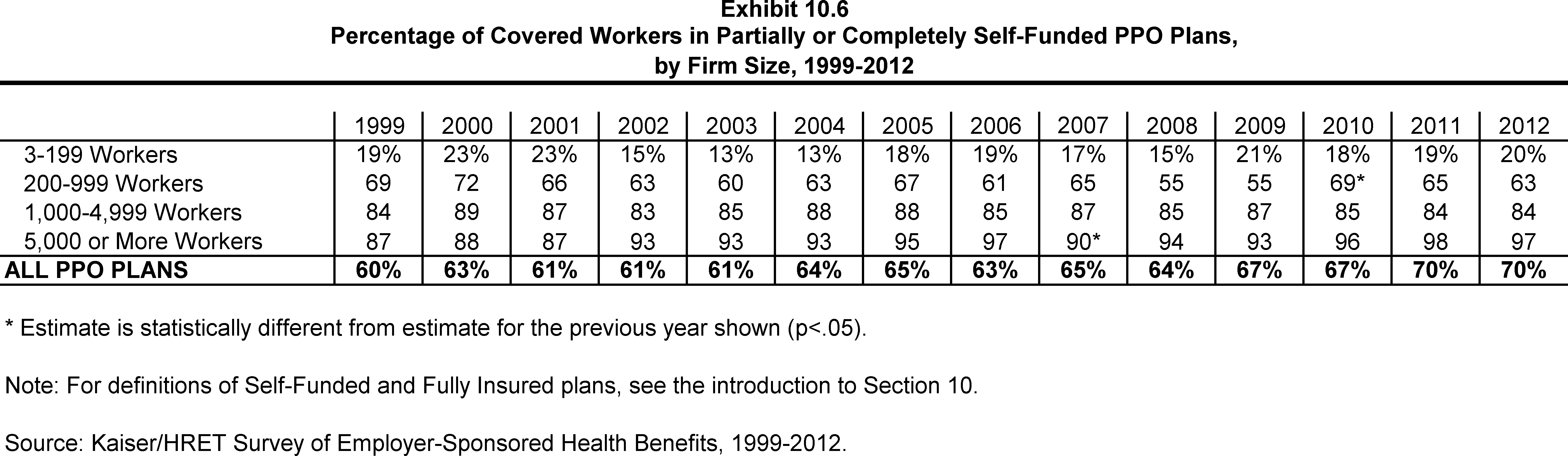

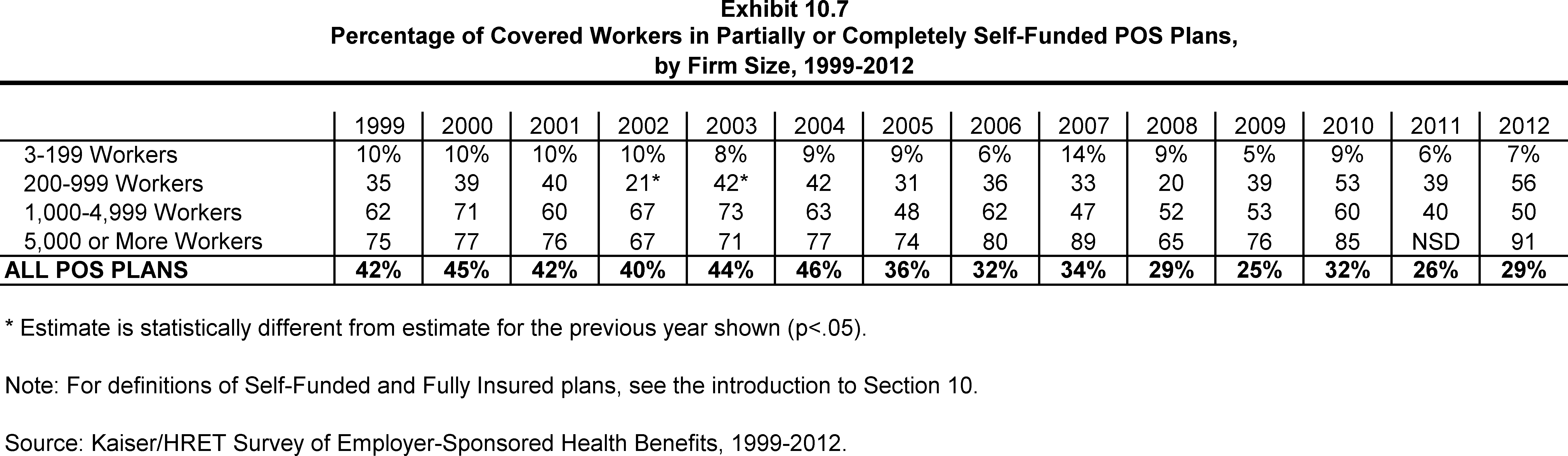

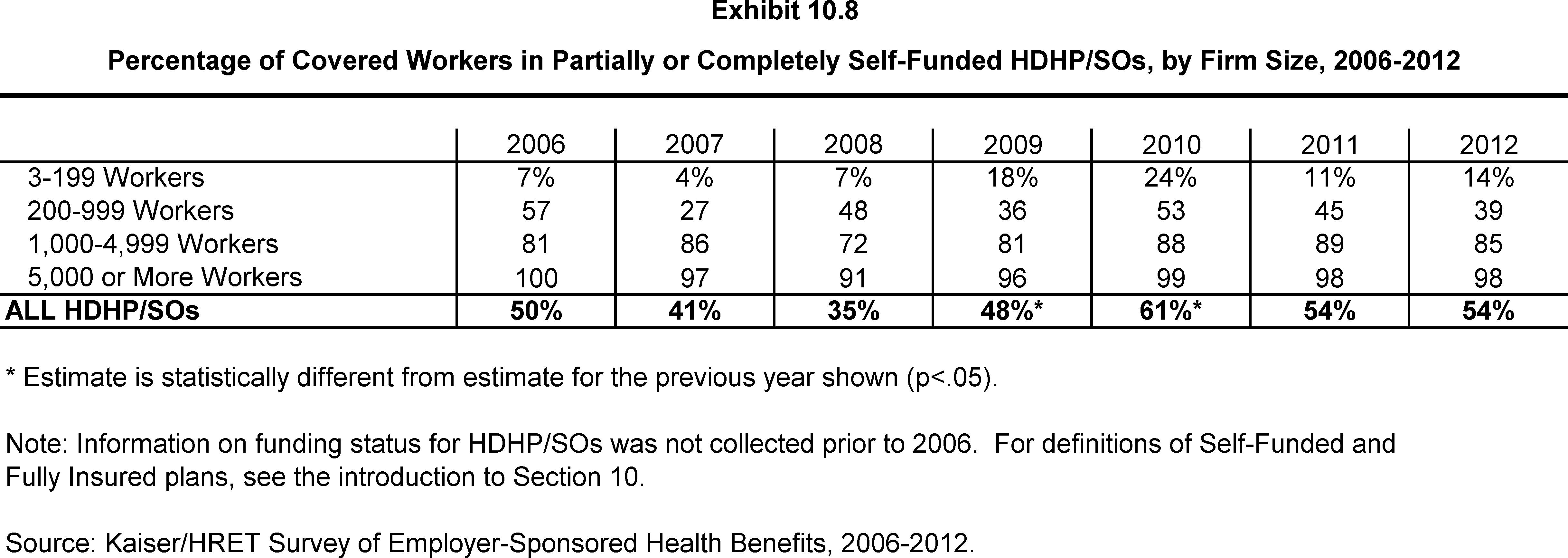

- The percentage of covered workers differs by plan type: 70% of covered workers in PPOs, 54% in HDHP/SOs, 38% in conventional health plans, 37% in HMOs, and 29% in POS plans are in a self-funded plan (Exhibit 10.4).

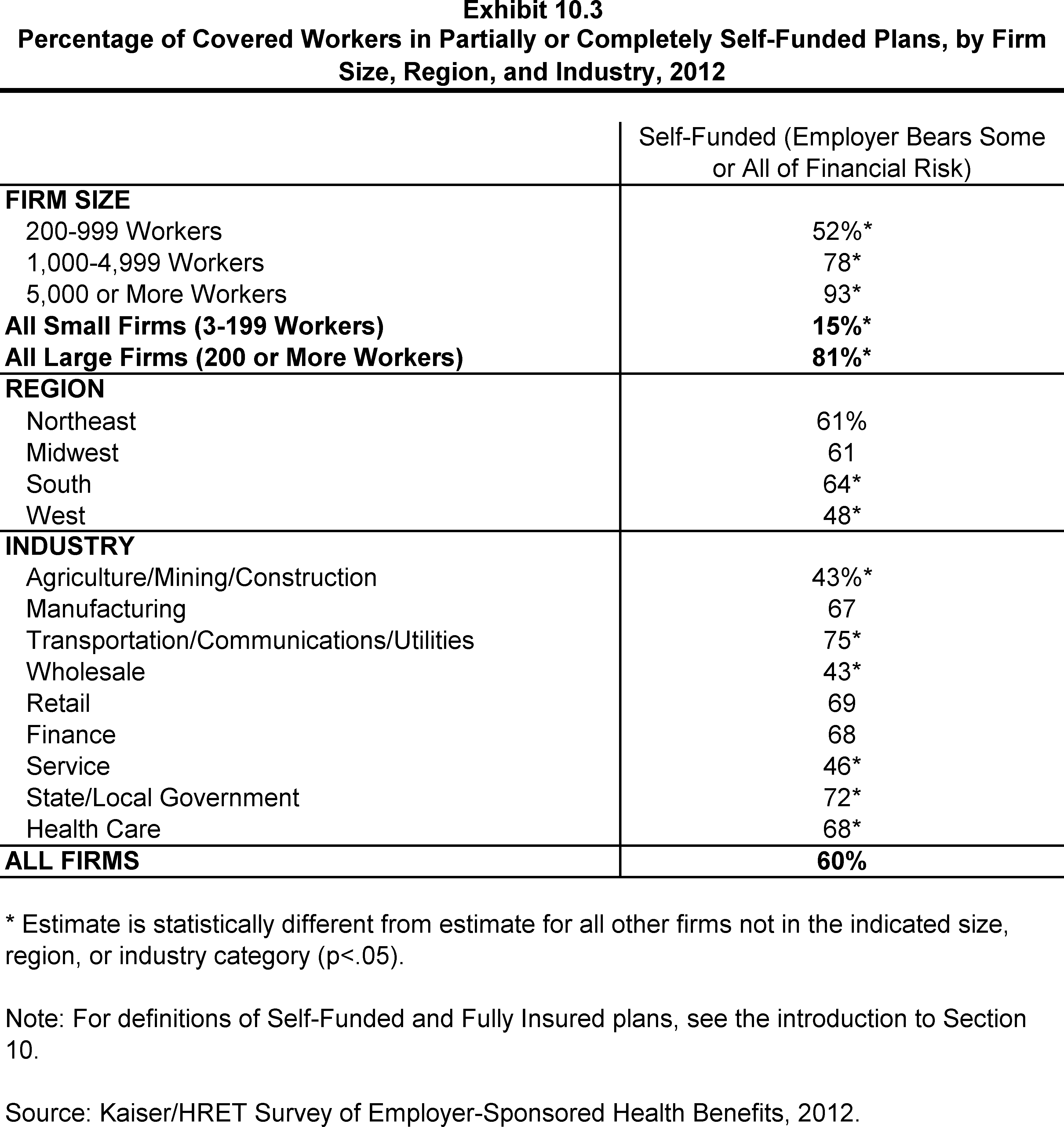

- As expected, covered workers in large firms (200 or more workers) are more likely to be in a self-funded plan than covered workers in small firms (3-199 workers) (81% vs. 15%) (Exhibit 10.3). The percentage of covered workers in self-funded plans increases as the number of employees in a firm increases. Seventy-eight percent of covered workers in firms with 1,000 to 4,999 workers and 93% of covered workers in firms with 5,000 or more workers are in self-funded plans in 2012 (Exhibit 10.3).

Self-Funded Plan: An insurance arrangement in which the employer assumes direct financial responsibility for the costs of enrollees medical claims. Employers sponsoring self-funded plans typically contract with a third-party administrator or insurer to provide administrative services for the self-funded plan. In some cases, the employer may buy stop-loss coverage from an insurer to protect the employer against very large claims.

Fully Insured Plan: An insurance arrangement in which the employer contracts with a health plan that assumes financial responsibility for the costs of enrollees medical claims.

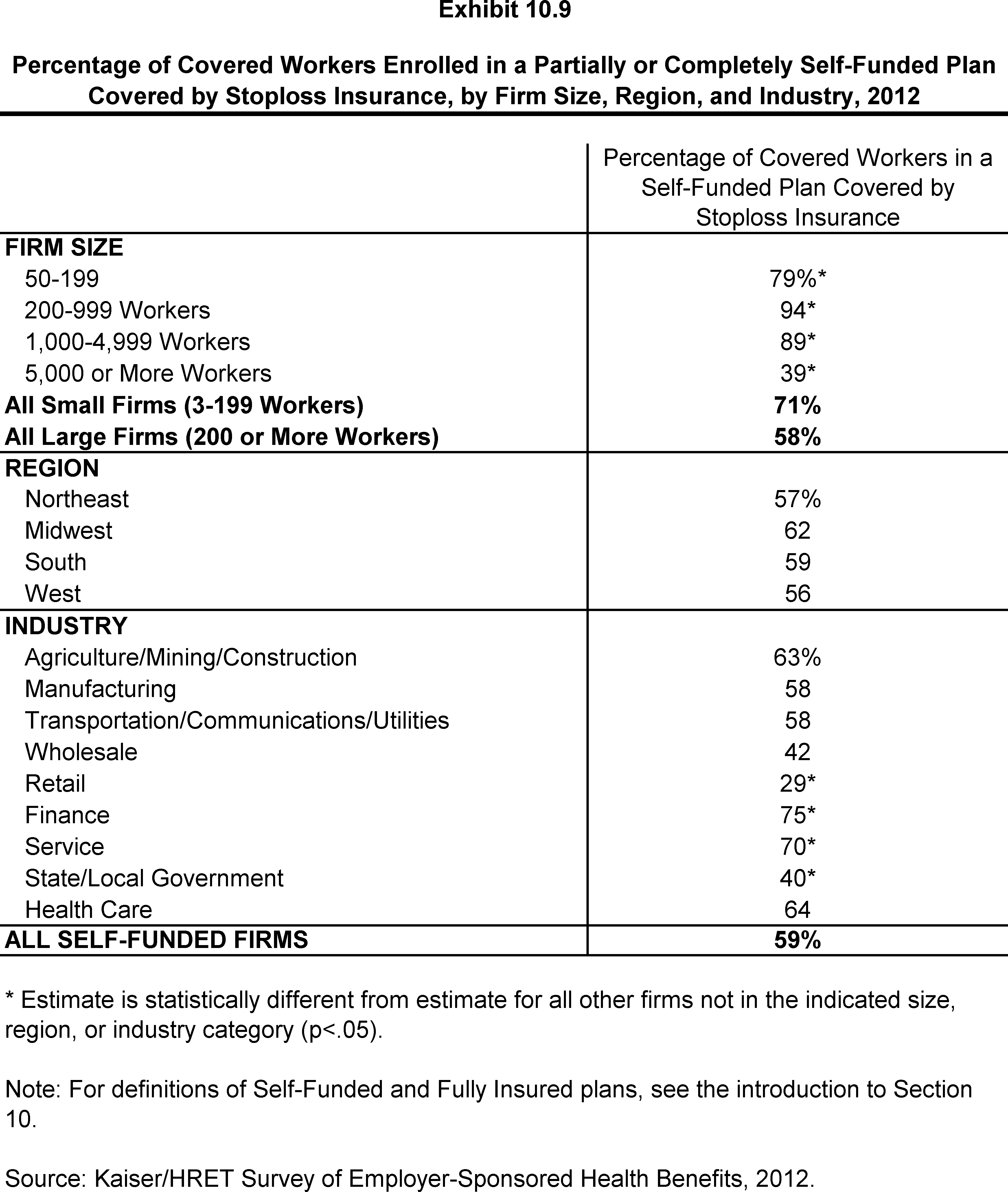

- Fifty-nine percent of workers in self-funded health plans are in plans that have stoploss insurance (Exhibit 10.9). Stoploss coverage limits the amount that a plan sponsor has to pay in claims. Stoploss coverage may limit the amount of claims that must be paid for each employee or may limit the total amount the plan sponsor must pay for all claims over the plan year.

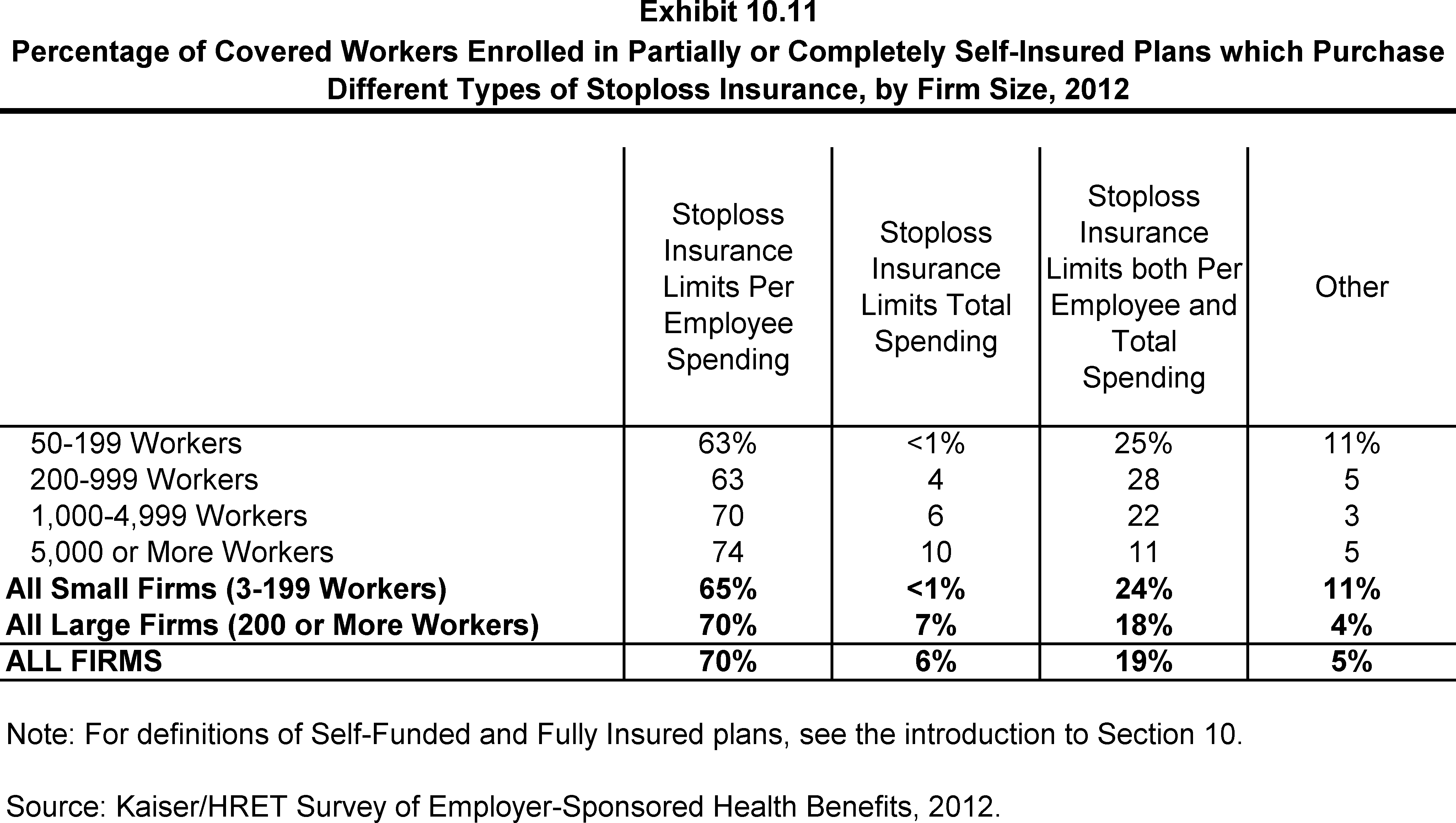

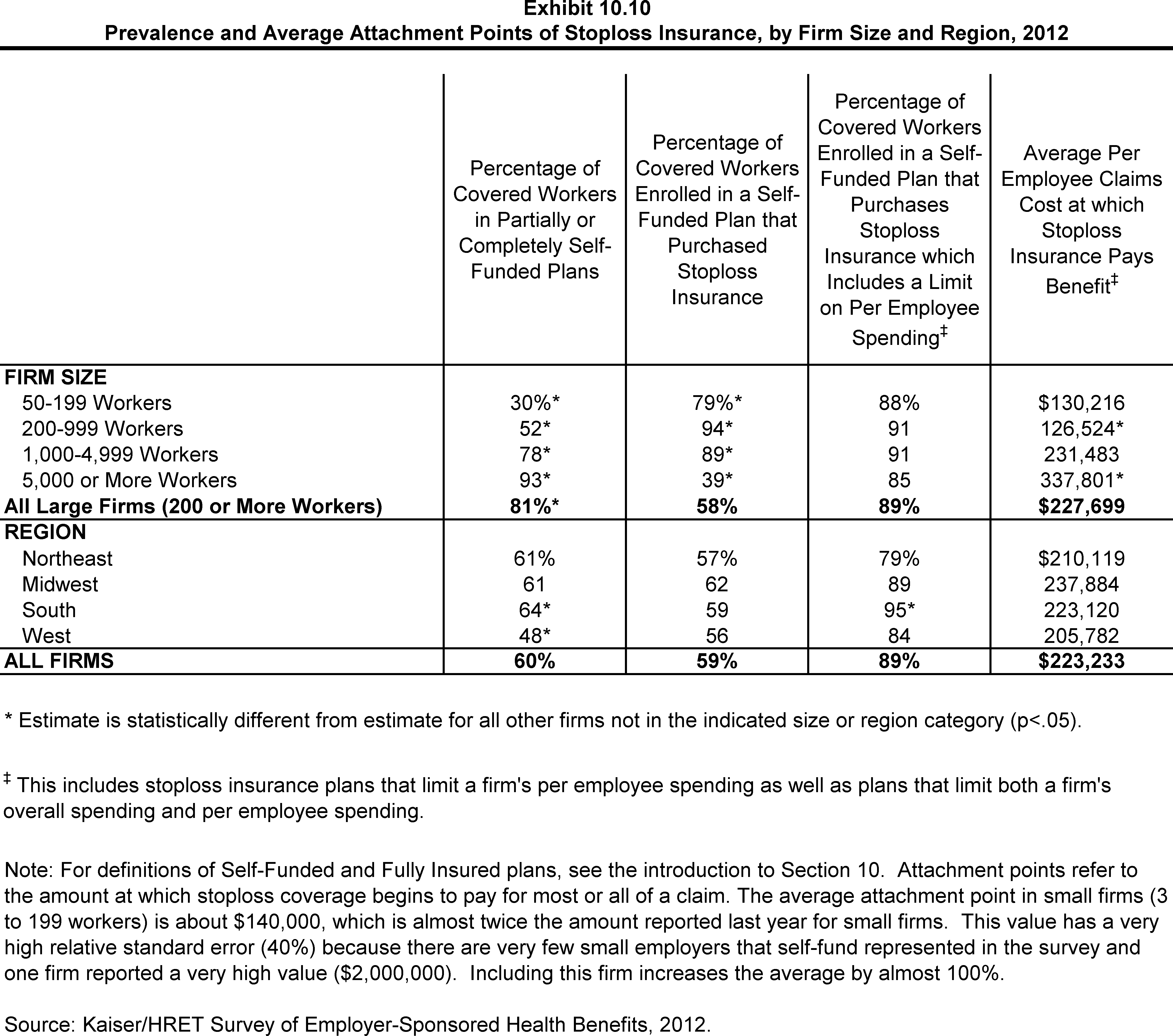

- Eighty-nine percent of covered workers in self-funded plans that have stoploss protection are in plans where the stoploss insurance limits the amount that the plan must spend on each employee (Exhibit 10.10).1

- Firms with per enrollee stoploss coverage were asked for the dollar amount where the stoploss coverage would start to pay for most or all of the claim (called an attachment point). The average attachment point in large firms (200 or more workers) is $223,233 (Exhibit 10.10).2

Percentage of Covered Workers in Partially or Completely Self-Funded Plans, by Firm Size, 1999-2012

Percentage of Covered Workers in Partially or Completely Self-Funded Plans, by Plan Type, 1999-2012

Percentage of Covered Workers in Partially or Completely Self-Funded Plans, by Firm Size, Region, and Industry, 2012

Percentage of Covered Workers in Partially or Completely Self-Funded Plans, by Plan Type and Firm Size, 2012

Percentage of Covered Workers in Partially or Completely Self-Funded HMO Plans, by Firm Size, 1999-2012

Percentage of Covered Workers in Partially or Completely Self-Funded PPO Plans, by Firm Size, 1999-2012

Percentage of Covered Workers in Partially or Completely Self-Funded POS Plans, by Firm Size, 1999-2012

Percentage of Covered Workers in Partially or Completely Self-Funded HDHP/SOs, by Firm Size, 2006-2012

Percentage of Covered Workers Enrolled in a Partially or Completely Self-Funded Plan Covered by Stoploss Insurance, by Firm Size, Region, and Industry, 2012

Prevalence and Average Attachment Points of Stoploss Insurance, by Firm Size and Region, 2012